Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

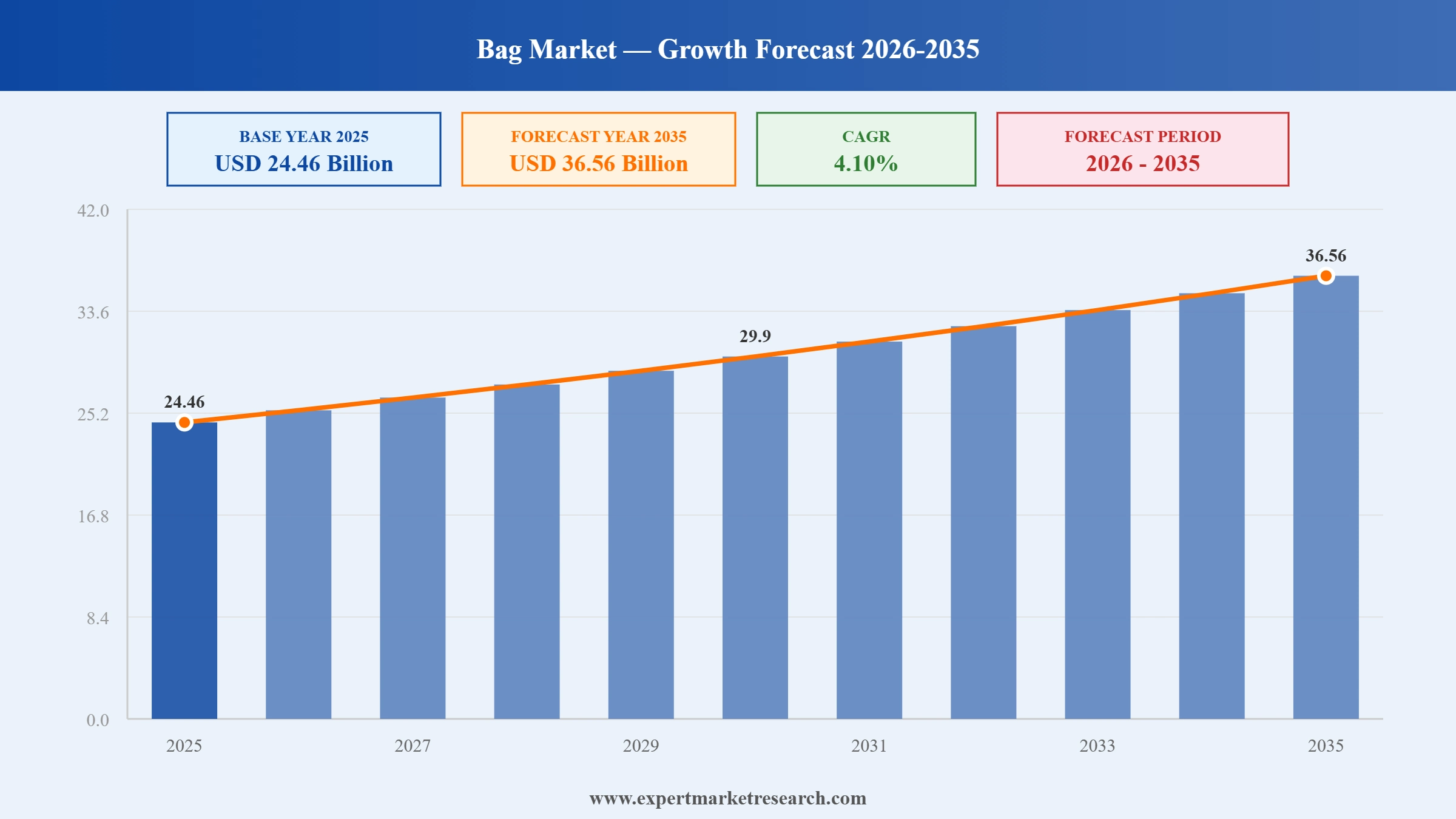

The global bag market reached a value of USD 24.46 Billion in 2025 and is projected to expand at a CAGR of around 4.10% during the forecast period of 2026-2035. Rising disposable incomes, growing social media influence on purchase decisions, e-commerce luxury expansion, and demand for sustainable bag designs are fuelling consistent market growth. The market is expected to reach USD 36.56 Billion by 2035.

Changing fashion trends are boosting demand for bags across global markets. According to Vogue Business, consumers are seeking stylish and functional products, encouraging innovation.

Manufacturers are increasingly adopting sustainable materials in bag production. According to The Guardian, eco-conscious consumers are influencing product development.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

| Global Bag Market Report Summary | Description | Value |

| Base Year | USD Billion | 2025 |

| Historical Period | USD Billion | 2019-2025 |

| Forecast Period | USD Billion | 2026-2035 |

| Market Size 2025 | USD Billion | 24.46 |

| Market Size 2035 | USD Billion | 36.56 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 4.10% |

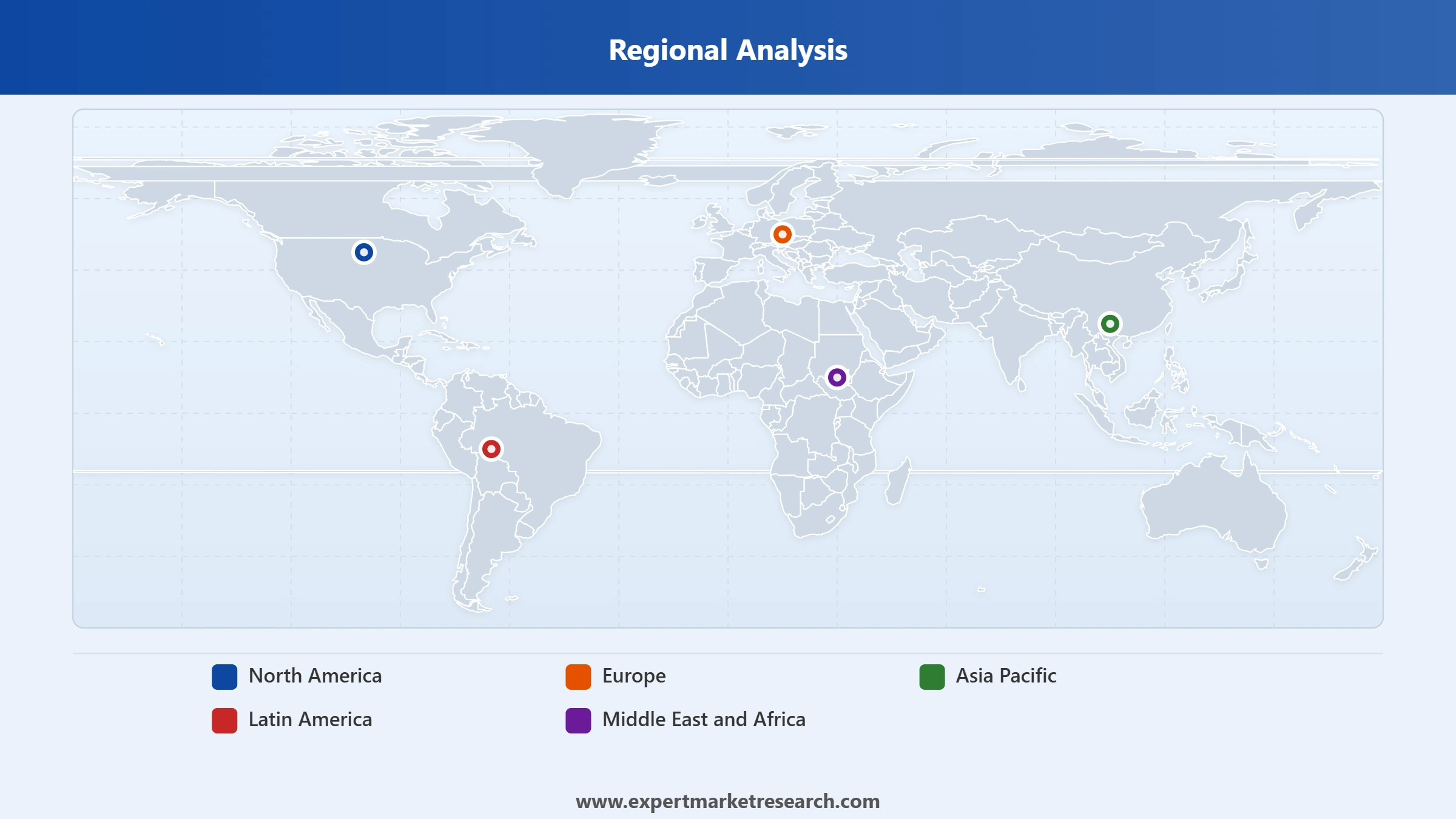

| CAGR 2026-2035 - Market by Region | Asia Pacific | 4.7% |

| CAGR 2026-2035 - Market by Country | India | 5.4% |

| CAGR 2026-2035 - Market by Country | China | 4.5% |

| CAGR 2026-2035 - Market by Product Type | Tote Bag | 4.6% |

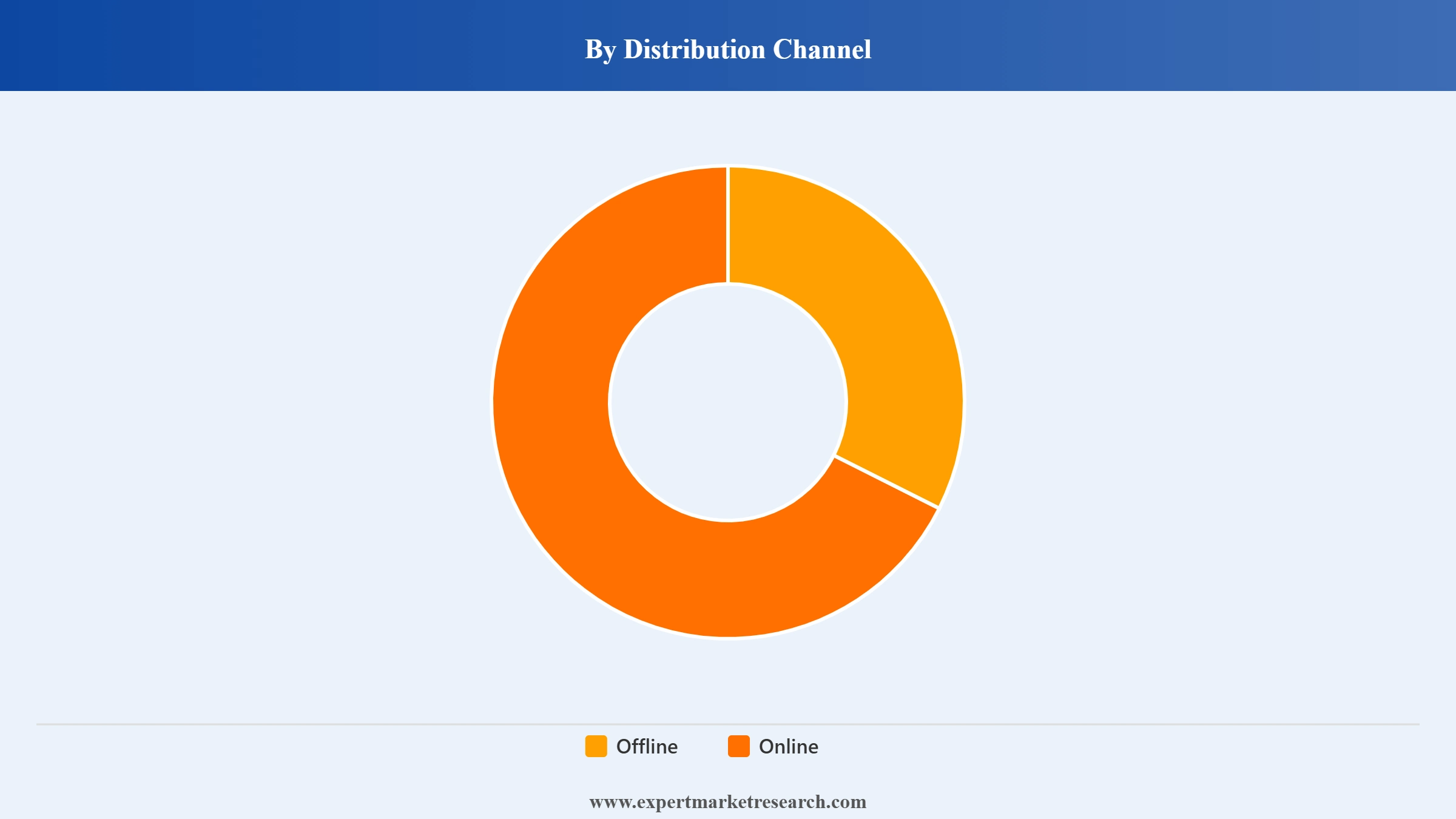

| CAGR 2026-2035 - Market by Distribution Channel | Online | 7.3% |

| Market Share by Country 2025 | India | 4.2% |

The global bag market is in a period of strategic repositioning at the luxury tier. Leading fashion conglomerates are making portfolio moves through acquisitions and joint ventures that will reshape the competitive landscape, while social commerce and direct-to-consumer digital channels are accelerating product discovery globally.

Prada Group reported a Q1 2026 growth driven by a full-price sales momentum and they confirmed strategic US and China investment plans through 2026-28. A refurbished SoHo flagship and a new Miu Miu store in Wuhan both performed exceptionally, confirming these as priority markets for the group's bag business.

Prada Group acquired Versace for EUR 1.25 billion in December 2025,specifically expanding its luxury bag and fashion portfolio. Lorenzo Bertelli was named executive chairman, with integration weighing on near-term margins as Prada begins a strategic turnaround of the Versace leather goods and bag business.

Prada Group reported 13% quarterly sales growth in November 2025,specifically, in turn, significantly outperforming peers. The Miu Miu bag and other accessory collections drove results across the Asia Pacific and Europe, affirming the brand as one of the fastest-growing luxury label portfolios in the global bag market.

Kering SA agreed a 50/50 beauty JV with L'Oreal valued at EUR 4 billion in October 2025 to monetise its fragrance portfolio and focus on core luxury under new CEO Luca de Meo. The deal includes 50-year licences for Bottega Veneta and Balenciaga while Kering concentrates capital on its bag and leather goods business.

Tote bags account for approximately 40-41% of the global bag market revenue, anchored by their versatility across the professional, casual, and sustainable use cases. Growing consumer preference for much more large, functional formats and the influence of Korean fashion aesthetics on younger consumers globally are sustaining tote bags as the dominant product type.

Offline retail retains a dominant global market share of approximately 62-76% of sales. Luxury and premium purchases have remained anchored to the physical retail, wherein the brand environment.

Online is the fastest-growing distribution channel in the global bag market, projected to expand at approximately 5.5-8.5% CAGR through the forecast period. Social commerce, influencer-driven discovery, and luxury brand direct-to-consumer platform expansion are the primary drivers, with augmented reality tools elevating digital purchase experiences.

Asia Pacific commands approximately 38-43% of global bag market revenue and is the fastest-growing region. China's luxury appetite, India's expanding middle class, and Japan's mature premium market position the region at the centre of global growth. Social commerce in China and ASEAN is accelerating brand discovery and purchase frequency among younger consumers.

Sustainability is a structural trend in the global bag market, with consumers demanding material transparency and responsible sourcing. Vegan leather alternatives and recycled material designs are influencing purchase decisions across premium and mass segments. Gen Z consumers, with purchasing power estimated at USD 143.5 billion globally, are prioritising sustainable bag formats.

The report of Expert Market Research titled "Global Bag Market Report and Forecast 2026-2035" offers a detailed analysis of the market based on the following segments:

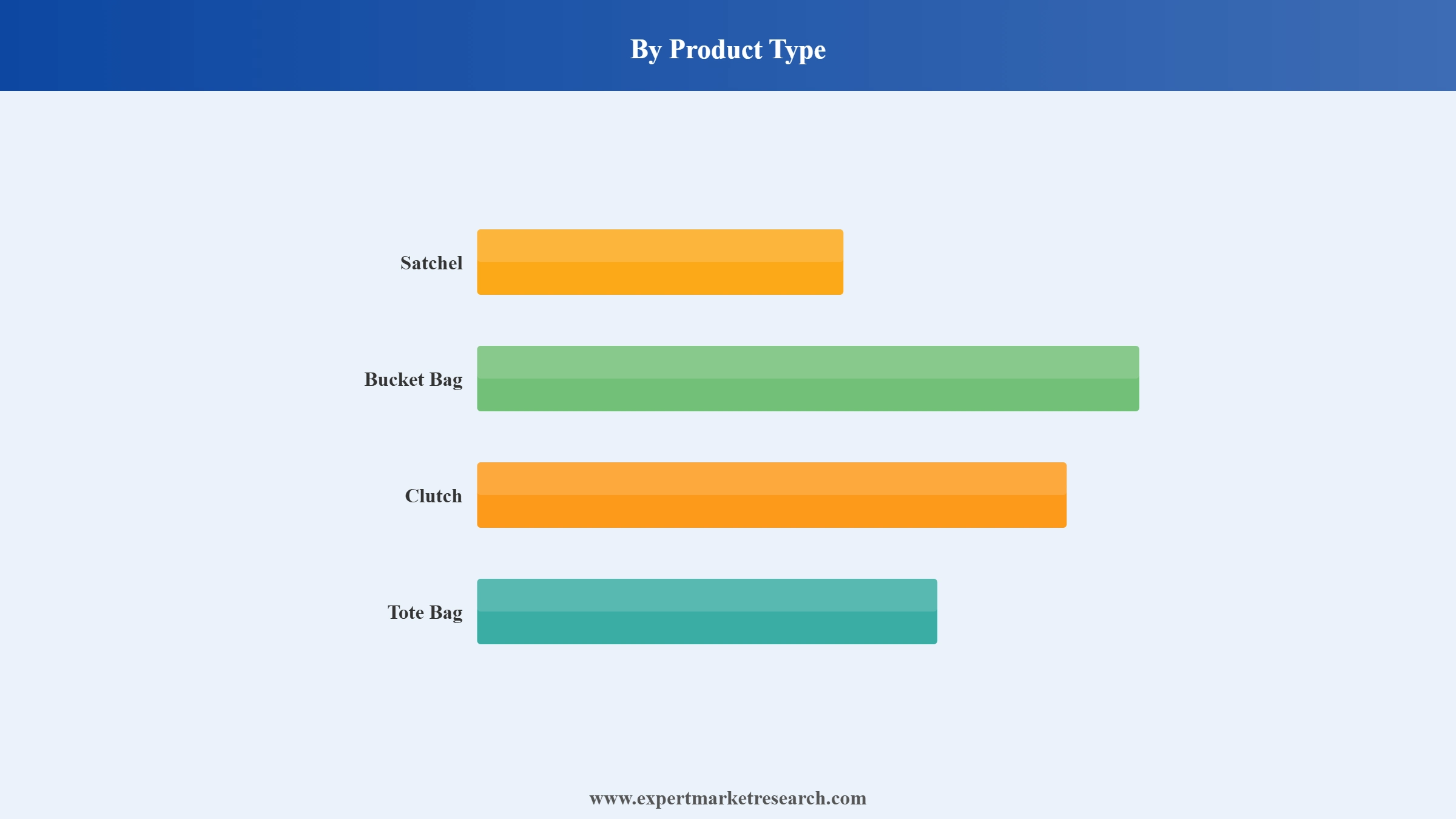

Market Breakup by Product Type

Key Insight: Tote bags lead the global bag market by revenue share at approximately 40-41%, driven by versatility and sustainable use appeal. Satchels are the fastest-growing type through consumer preference for structured, professional designs that pair functionality with premium aesthetics.

Market Breakup by Distribution Channel

Key Insight: Offline holds approximately 62-76% of the global bag market, anchored by the critical role of physical brand experience in luxury purchasing. Online is the fastest-growing channel through social commerce, influencer marketing, and direct-to-consumer platform expansion.

Market Breakup by Region

Key Insight: Asia Pacific holds the largest and fastest-growing regional share, anchored by China's luxury fashion market and India's expanding consumer base. North America and Europe are mature, high-value markets where brand equity defines competition. Latin America and the Middle East and Africa are growing through rising incomes and expanding luxury retail access.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Product Type, Tote Bags dominate the market across professional and casual consumer segments globally

Tote bags account for the largest revenue share of the global bag market. Their utility across work, shopping, travel, and casual settings, combined with premium and sustainable material availability, makes them the dominant format. Structured carrying solutions have broad appeal among professional and fashion-forward consumers globally.

Satchels are the fastest-growing type. Their structured silhouette, crossbody functionality, and versatility across professional and casual wardrobes attract consumers seeking premium practical designs. Bucket bags serve the everyday fashion market; clutches remain a premium evening and gifting product across luxury brands.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Distribution Channel, Offline retail accounts for the dominant share due to the critical role of physical brand experience in luxury globally

Offline retail commands the dominant distribution channel position. In luxury and premium segments, brand environment, product handling, and personalised service at flagship boutiques remain fundamental to the purchase decision. Hermes, Louis Vuitton, and Chanel maintain strict physical retail control, reinforcing offline's structural premium.

The online channel is growing rapidly through social commerce in China and ASEAN, influencer-led discovery, and brand-owned e-commerce expansion. Luxury brands are investing in augmented reality and virtual styling tools to replicate physical retail engagement digitally, with online projected at 5.5-8.5% CAGR through the forecast period.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Asia Pacific dominates the global bag market due to China's dominant luxury fashion consumption, India's expanding middle class, and the region's social commerce-driven acceleration of bag brand discovery

Asia Pacific commands the largest regional share at approximately 38-43% of global bag market revenues. China accounts for approximately 34% of the Asia Pacific market, driven by deep luxury leather goods affinity and a premium fashion culture reinforced by social media and live commerce. India's growing middle class and Japan's established fashion market add further regional depth.

North America and Europe are mature markets with the highest per-unit average selling prices. North America held approximately 31% of the global handbag market in 2024, driven by a fashion-conscious consumer base and deep e-commerce adoption. Europe's luxury heritage, anchored by French, Italian, and British fashion houses, supports both domestic consumption and tourism purchasing. Latin America, the Middle East, and Africa are growing through rising incomes and expanding luxury retail access.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The global bag market at the luxury and premium tier is dominated by a small number of large fashion conglomerates. LVMH, Kering, Prada Group, and Hermes collectively hold a significant portion of global luxury bag revenues. The competitive dynamic is shaped by brand heritage, retail experience investment, and pricing strategy, with major players navigating consumer sentiment volatility following years of aggressive price increases.

Founded in 1987 and headquartered in Paris, France, LVMH is the world's largest luxury goods conglomerate with Louis Vuitton at the core of its fashion and leather goods division. Louis Vuitton is the world's most valuable luxury brand, with its Monogram, Damier, and signature leather bag collections globally recognised. Under Pharrell Williams' creative direction, the Spring-Summer 2025 collection generated strong commercial and cultural momentum.

Founded in 1837 and headquartered in Paris, France, Hermes International is one of the world's most exclusive luxury houses. The Birkin and Kelly bags are the most price-resilient products in the global luxury market, with waiting lists and secondary market premiums that no other bag brand has replicated. Hermes consistently outperforms sector trends through controlled production, craftsmanship positioning, and scarcity.

Founded in 1913 and headquartered in Milan, Italy, Prada Group operates the Prada, Miu Miu, and now Versace brands. The group posted 13% quarterly growth in November 2025, driven by Miu Miu bag demand. In December 2025, Prada acquired Versace for EUR 1.25 billion, and in April 2026 confirmed US and China bag market expansion plans through 2028.

Founded in 1963 and headquartered in Paris, France, Kering is a global luxury fashion conglomerate owning Gucci, Saint Laurent, Bottega Veneta, Balenciaga, and others. Under new CEO Luca de Meo, Kering agreed a EUR 4 billion L'Oréal beauty JV in October 2025, freeing capital for core bag and leather goods portfolios. Gucci bags and Bottega Veneta's Intrecciato leather remain central to the group's revenues.

Other key players in the market are Burberry Group Plc, Chanel S.A., Tapestry Inc. (Kate Spade and Company), Capri Holdings Limited, Cambridge Satchel Company Limited, Sandqvist Bags and Items AB, and others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Our full report for 2026-2035 delivers the product analysis, regional intelligence, and competitive benchmarking to navigate the global bag market confidently. Reach out to our team to access the complete report or request a customised version for your business.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

The market is projected to grow at a CAGR of 4.10% between 2026 and 2035.

The different types of products in the market include satchel, bucket bag, clutch, and tote bag, among others.

The different distribution channels in the market are offline and online.

The different regions covered in the market report are North America, Europe, the Asia Pacific, Latin America, and the Middle East and Africa.

The key market players are Burberry Group Plc, LVMH Moet Hennessy Louis Vuitton SE, Prada Holding S.p.A., Kering S.A., Hermes International S.A., Chanel S.A., Tapestry Inc. (Kate Spade & Company), Capri Holdings Limited, Cambridge Satchel Company Limited, and Sandqvist Bags and Items AB, among others.

In 2025, the market attained a value of nearly USD 24.46 Billion.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach about USD 36.56 Billion by 2035.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Product Type |

|

| Breakup by Distribution Channel |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.