Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

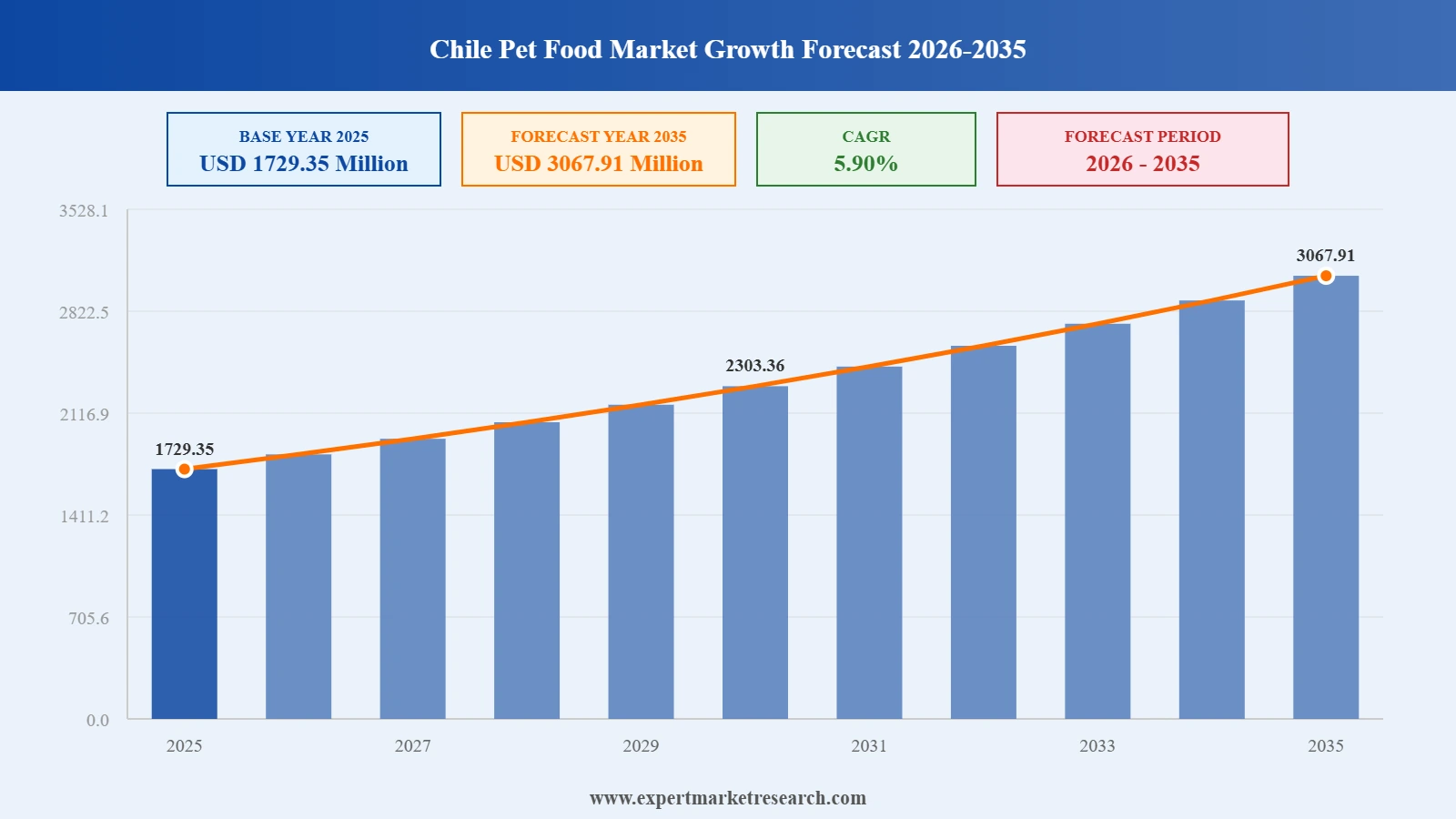

The Chile pet food market reached USD 1729.35 Million in 2025 and is projected to grow at a CAGR of 5.90% to reach USD 3067.91 Million by 2026 and 2035. Chile is emerging as one of Latin America's most pet-humanised markets, with rising household pet ownership translating directly into sustained pet food demand.

Growth is supported by rising pet humanisation, with pets increasingly treated as family members, alongside a post-pandemic adoption surge, urban household premiumisation, and growing consumer awareness of functional, breed-specific, and prescription nutrition. Pet owners are scrutinising ingredient labels more closely, favouring natural and clean-label formulations, and trading up from mass-market to premium and super-premium SKUs.

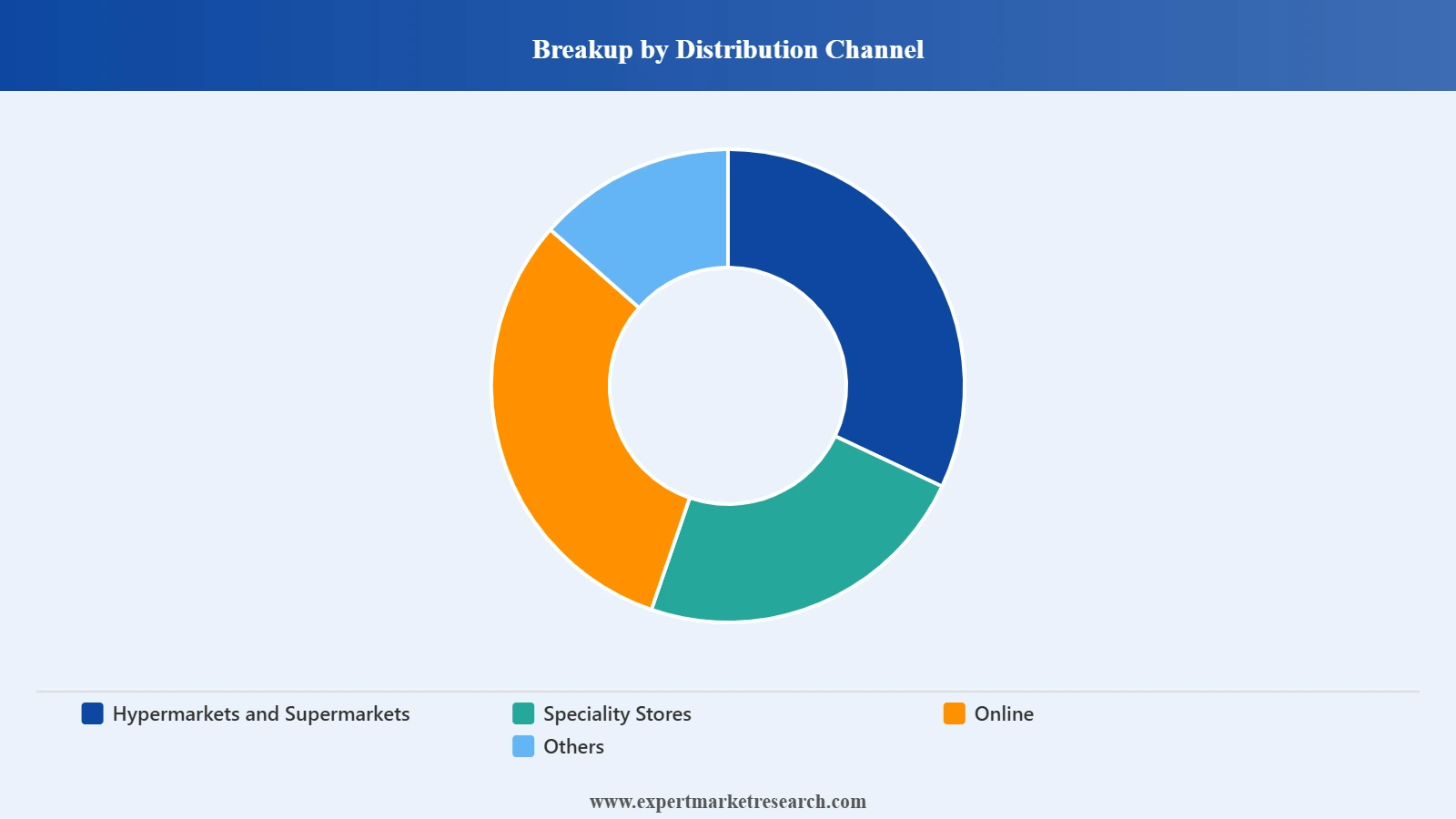

Distribution remains weighted toward modern off-trade retail, anchored by hypermarket and supermarket chains. However, e-commerce and specialty pet retail are the fastest-growing channels, particularly for premium, ultra-premium, and prescription/veterinary diets supported by subscription delivery models, direct-to-consumer brand websites, and a growing network of branded pet retail stores across Santiago and major urban centres.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Rising Pet Humanisation and Family-Member Status

Chilean households are increasingly treating pets as integral family members, driving spending on quality nutrition, premium SKUs, and functional formulations. Doctors continue to recommend pet adoption to combat anxiety, stress, and depression, leading to sustained adoption rates and per-pet spending growth across all income brackets. According to the USDA Foreign Agricultural Service Chile Pet Food Report (November 2025), pet nutrition in Chile has transitioned from a simple extension of the human diet to a sophisticated and specialised industry confirming the structural depth of this humanisation trend.

Pet Retail Infrastructure Expansion

Chile's pet retail landscape has expanded rapidly. The number of pet shops and related services has grown from 2,500 to nearly 3,400 over the past four years a 35% increase, with the broader pet retail base recorded as of late 2025. This commercial expansion reflects deepening category demand and is concentrated across Santiago and major urban centres, supporting both modern off-trade and specialty pet retail growth.

Premiumisation and Functional Nutrition Trend

Chilean consumers particularly in Santiago, Viña del Mar, and Concepción are trading up from mass-market to premium and super-premium pet food. Demand is rising for grain-free, organic, breed-specific, prescription, and life-stage-targeted formulations. Per the USDA's 2025 Chile Pet Food Report, Chilean companies are investing in research and development to create specialised formulas addressing specific pet needs including allergies, digestive issues, and aging-related concerns alongside emerging adoption of personalised nutrition technologies.

Updated Import Standards and Regulatory Tightening

Chile's regulatory environment is actively tightening. In August 2025, Chile's Ministry of Agriculture announced revised standards for international veterinary certificates for imported animal-derived products. The new rules require certificates to include specific hygiene requirements set by the Ministry, be issued by the competent veterinary authority of the country of origin, be presented in Spanish and the official language of origin, and carry validity periods of 10 days for land or air transport and 30 days for sea transport. This regulatory clarity supports consumer confidence while raising the compliance bar for international brand expansion into Chile.

Free Trade Advantage and Rising Pet Food Imports

Chile's deep free trade integration continues to support category growth. The U.S.-Chile Free Trade Agreement allows US dog and cat food to enter Chile duty-free, supporting steady import expansion. Per the USDA FAS (2025), Latin America imported approximately USD 162 million worth of US pet food in 2024 an 11% increase from 2023 with Chile among the region's most attractive destinations due to high consumer purchasing power and a favourable regulatory environment. Chile's network of 31 free trade agreements with 65 economies further diversifies sourcing and supports premium import availability.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Growth of Veterinary and Prescription Diets

Royal Canin, Hill's Pet Nutrition, and Purina Pro Plan are aggressively expanding their veterinary and prescription diet portfolios in Chile. Vet-recommended nutrition is one of the fastest-growing premium sub-segments, supported by rising vet clinic density and growing consumer willingness to invest in clinically validated, condition-specific formulations.

Functional Ingredients and Clean-Label Innovation

Functional pet food featuring probiotics, prebiotics, omega-3, and joint-support compounds is gaining traction in Chile. Per the USDA 2025 Chile Pet Food Report, manufacturers are investing in personalised nutrition technologies and specialised formulas addressing allergies, digestive health, and aging-related concerns mirroring broader Latin American humanisation trends.

E-Commerce and Direct-to-Consumer Expansion

E-commerce penetration is rising rapidly across Chile. Subscription-based pet food delivery models, breed-specific nutrition apps, and direct-to-consumer brand websites are reshaping how premium pet food reaches Chilean households, particularly in Santiago and major urban centres.

Sustainable Packaging and Plant-Based Formulations

Sustainability is reshaping the category. Chilean ingredient innovators are increasingly using local crops such as quinoa, chia, and lentils for omega-3 and fibre enrichment, while manufacturers are introducing recyclable packaging and traceable ingredient sourcing in line with Chile's tightening environmental regulations.

Heavy Import Dependence and Currency Volatility

Chile imports the majority of its commercial pet food from Argentina, the United States, China, Brazil, and the Netherlands. This import dependence exposes the category to peso-dollar volatility, ocean freight inflation, and trade-route disruptions directly affecting shelf prices and margin structures.

Price Sensitivity in Mass Segment

While premium segments grow rapidly, the mass-market category remains highly price-sensitive. Inflation-driven pressure on disposable income forces budget-conscious pet owners to trade down to value brands or private-label SKUs from major retailers.

Regulatory Compliance and Import Authorisation

Chile's tightening import standards (August 2025 veterinary certificate revisions) create compliance lead times for new international entrants. Imported product authorisation through SAG can take several months to complete, creating barriers for niche premium brands seeking to test the Chilean market.

"Chile Pet Food Market Report and Forecast 2026-2035" offers a detailed analysis of the market based on the following segments:

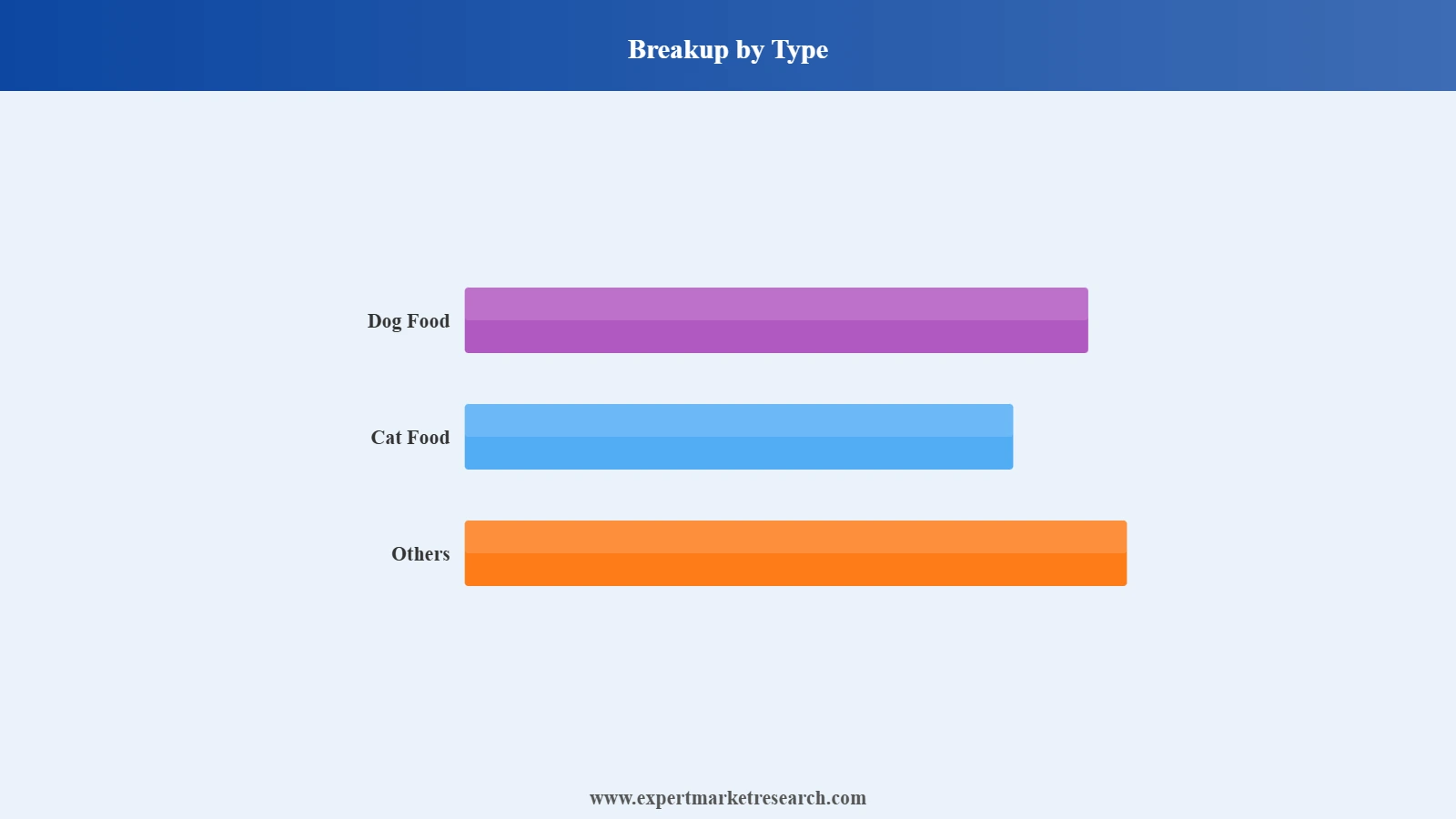

Market Breakup by Type

Dog food dominates the Chile pet food market, supported by canine ownership preferences and larger per-pet consumption. Cat food is the fastest-growing sub-segment, driven by urban apartment lifestyles and rising small-pet adoption.

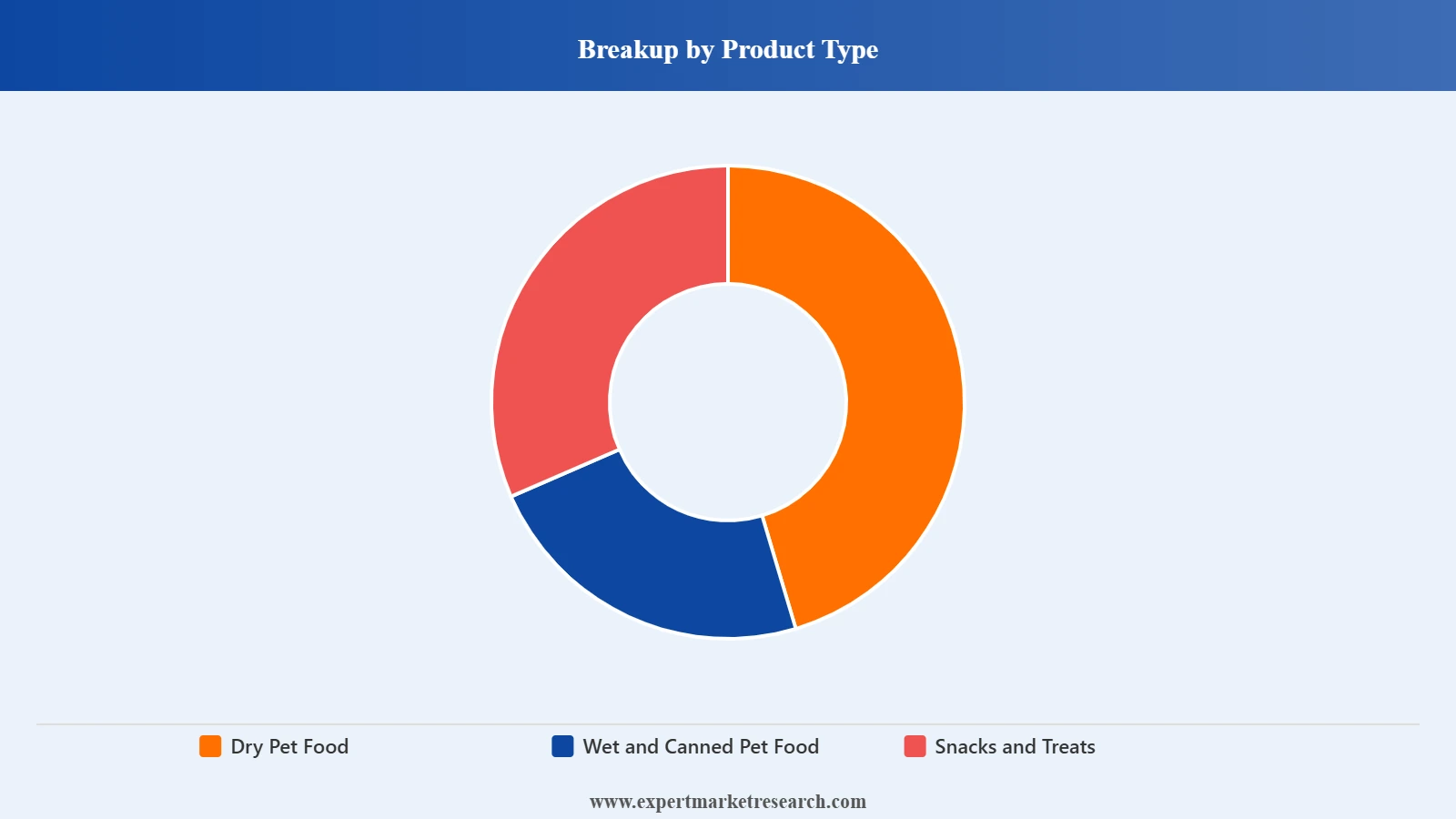

Market Breakup by Product Type

Dry pet food holds the dominant share due to affordability, shelf stability, and dental-health benefits. Wet and canned pet food is gaining share in the premium and senior-pet segments. Snacks and treats are the fastest-growing format, driven by humanisation and reward-feeding behaviour.

Market Breakup by Price

Mass products account for the volume majority, while premium products represent the value growth engine.

Market Breakup by Ingredient Type

Animal-derived ingredients dominate the category. Plant-derived ingredients are gaining share through grain-free, vegan, and sustainable positioning trends, with Chilean innovators using local crops like quinoa, chia, and lentils.

Market Breakup by Distribution Channel

Hypermarkets and supermarkets account for the largest share. Specialty pet stores anchor premium and prescription sales, while online channels are the fastest-growing distribution route.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Santiago Metropolitan Region

Santiago Metropolitan Region accounts for the majority of Chilean pet food consumption, anchored by high urban density, the country's largest concentration of veterinary clinics and pet specialty stores, and the strongest concentration of premium-receptive consumers.

Valparaíso, Concepción and Other Urban Hubs

Valparaíso and Viña del Mar combine strong tourism-driven HoReCa demand with premium urban consumer bases. Concepción (Biobío Region) is Chile's third-largest urban economy and an emerging premium pet food hub.

Maule Region - Manufacturing Hub

The Maule Region is emerging as Chile's strategic pet food production hub, with major investment in domestic manufacturing supporting supply chain resilience, export potential to neighbouring Latin American markets, and reduced import dependence.

The Chile pet food market is moderately concentrated, with global pet care giants Mars Incorporated and Nestlé S.A. anchoring the market, supported by domestic players including Empresas Carozzi, Empresas Iansa, Nutripro, and Champion SA. Market participants are increasingly focusing on premium nutrition, organic and grain-free formulations, prescription/veterinary diets, and sustainable packaging to capture the rapidly humanising Chilean pet ownership base.

Mars, Incorporated was founded in 1911 by Frank C. Mars in Tacoma, Washington, USA, and is headquartered in McLean, Virginia, USA. Through its Royal Canin Chile Ltda and Mars Southern Cone Alimentos Ltda subsidiaries, Mars is the dominant pet food player in Chile. Its portfolio spans premium veterinary nutrition (Royal Canin), mainstream pet food (Pedigree, Whiskas), and specialised diets, supported by veterinary partnerships and deep distribution across modern off-trade and specialty channels.

Nestlé S.A. was founded in 1866 by Henri Nestlé in Vevey, Switzerland, where it remains headquartered. Nestlé Chile SA operates a major Purina pet food manufacturing facility in the Maule Region, supporting super-premium production for domestic and export markets. Nestlé competes through brands including Purina Pro Plan, Purina ONE, Dog Chow, and Cat Chow, with strong distribution in hypermarkets, specialty pet retail, and veterinary clinics.

Hill's Pet Nutrition was founded in 1948 by Dr. Mark L. Morris Sr. in Topeka, Kansas, USA, where it remains headquartered. The company operates as a subsidiary of Colgate-Palmolive (acquired in 1976) and specialises in clinically proven, science-based pet nutrition. In Chile, Hill's competes through its Science Diet and Prescription Diet portfolios, distributed through veterinary clinics and premium specialty stores.

Empresas Carozzi SA was founded in 1898 in Quilpué, Chile, where it remains headquartered as one of Chile's largest food and beverage conglomerates. Carozzi participates in the pet food market through its Master Dog and Master Cat brands, leveraging extensive domestic manufacturing capacity and deep relationships with Chilean modern retail chains.

Empresas Iansa SA was founded in 1953 and is headquartered in Santiago, Chile, operating as a major Chilean agro-industrial group. Iansa participates in the pet food market through animal nutrition product lines and distribution agreements, leveraging its extensive Chilean agricultural and ingredient supply network.

Total Alimentos SA was founded in 1989 and is headquartered in Três Corações, Minas Gerais, Brazil. Total Alimentos serves the Chilean market through imports and regional distribution agreements, anchoring the affordable mid-tier and mass segments with brands tailored to Latin American consumer preferences.

The J.M. Smucker Company was founded in 1897 by Jerome Monroe Smucker in Orrville, Ohio, USA, where it remains headquartered. The company operates a global pet food portfolio including Rachael Ray Nutrish, Nature's Recipe, and Milk-Bone, competing in the Chilean market through selective imports targeting modern off-trade and specialty pet retail.

Other notable players in the Chile pet food market include Nutripro SA, Champion SA, Proa Sociedad Anónima (founded 1939), Centro Veterinario Y Agrícola Limitada, Gabrica Chile Ltda, PremieRpet®, General Mills Inc., Schell & Kampeter Inc., Alphia Inc., and Unicharm Corporation, alongside emerging artisanal and direct-to-consumer brands across Santiago and major urban centres.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market reached an approximate value of USD 1729.35 Million.

The market is estimated to grow at a CAGR of 5.90% between 2026 and 2035.

The market is estimated to witness a healthy growth during 2026-2035 to reach around USD 3067.91 Million by 2035.

The major factors contributing to the market growth are the surge in disposable incomes and the heightened focus on pet health.

The key trends in Chile’s pet food market are the growing demand for premium pet foods and the rising number of pet adoptions.

The major types in the market are dog food, cat food, and others.

The major distribution channels in the market are supermarket/hypermarket, speciality stores, and online, among others.

The major players in the market are Mars Incorporated, Nestlé S.A., Total Alimentos SA, PremieRpet®, Hill's Pet Nutrition, Inc., The J.M. Smucker Company, General Mills Inc., Schell & Kampeter, Inc., Alphia, Inc., and Unicharm Corporation, among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Type |

|

| Breakup by Product Type |

|

| Breakup by Price |

|

| Breakup by Ingredient Type |

|

| Breakup by Distribution Channel |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.