Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

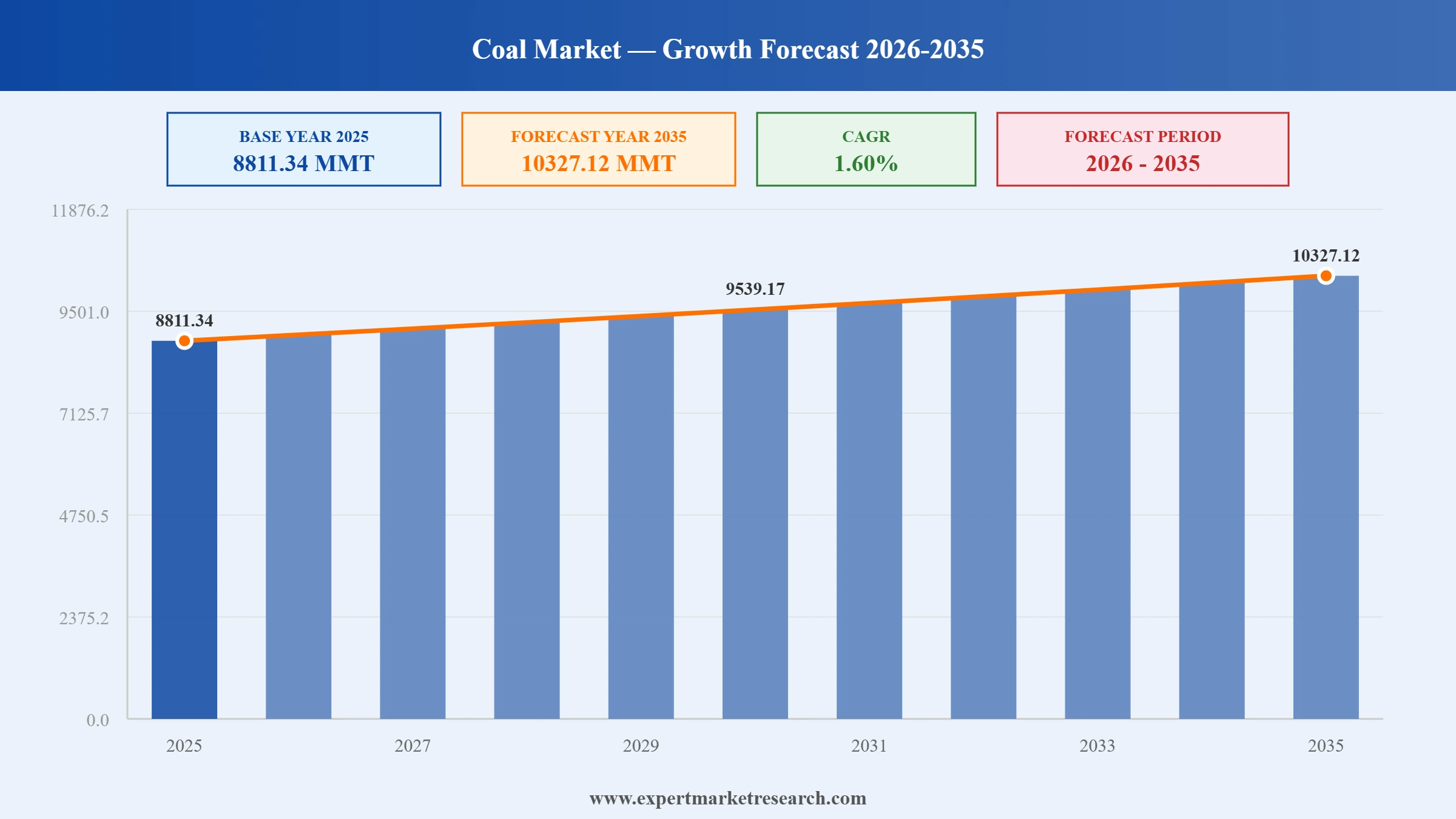

The Global Coal Market reached a volume of 8811.34 MMT at 2025 and is projected to expand at a CAGR of around 1.60% during the forecast period of 2026-2035. With the enduring centrality of metallurgical coal in blast furnace steelmaking, large-scale construction and infrastructure programmes across Asia and Africa, expanding Indian steel production capacity, and continued demand for coking coal byproducts across multiple industrial end uses, the market is expected to reach 10327.12 MMT by 2035.

According to Trading Economics, Newcastle thermal coal futures stayed above $130 per ton in April 2026, retaining most of March's surge as the Middle East conflict disrupted LNG flows through the Strait of Hormuz. Strikes on Qatari gas processing capacity accelerated gas-to-coal switching in Japan and Korea, lifting demand for high-grade Australian coal and supporting exporter margins across Indonesia, Russia, and South Africa.

According to the International Energy Agency, global coal production is expected to decline in 2026 after a record 2025, with seaborne trade volumes contracting for a second consecutive year for the first time this century. High stockpiles in China, stagnant European demand, and rising Indian domestic output are pressuring Russian and Indonesian exporters, reinforcing structural oversupply even as geopolitical shocks provide short-term price support.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

| Global Coal Market Report Summary | Description | Value |

| Base Year | MMT | 2025 |

| Historical Period | MMT | 2019-2025 |

| Forecast Period | MMT | 2026-2035 |

| Market Size 2025 | MMT | 8811.34 |

| Market Size 2035 | MMT | 10327.12 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 1.60% |

| CAGR 2026-2035 - Market by Region | Asia Pacific | 1.8% |

| CAGR 2026-2035 - Market by Country | India | 2.1% |

| CAGR 2026-2035 - Market by Country | China | 1.7% |

| CAGR 2026-2035 - Market by Type | Hard Coking Coals (HCC) | 1.9% |

| CAGR 2026-2035 - Market by End-Use Industry | Construction | 2.0% |

| Market Share by Country 2025 | India | 4.2% |

The global coal market, with specific focus on metallurgical and coking coal, is being shaped by four structural forces: the continued irreplaceability of coking coal in blast furnace steelmaking, the rapid expansion of Indian and Southeast Asian steel capacity that is reshaping seaborne trade flows, the consolidation of major mining assets into larger integrated producers, and the gradual integration of carbon reduction technology at coking and steelmaking facilities without displacing demand in the medium term.

In August 2025, China Shenhua Energy Company Limited completed the acquisition of 100 percent equity in Hangjin Energy, a strategic move aimed at consolidating coal mining, power generation, and coal-chemical assets under its listed entity. The transaction was designed to reduce internal related-party transactions, streamline corporate governance, and strengthen China Shenhua's position as an integrated coal and energy group. By consolidating Hangjin Energy's resource holdings, China Shenhua aimed to improve asset utilisation efficiency and reinforce its core resource base, which supports both domestic steelmaking and energy sector supply chains. The acquisition reflected the broader trend of consolidation among state-owned Chinese coal enterprises.

In May 2025, ArcelorMittal, one of the world's largest steel producers and a major consumer of metallurgical coal, announced that it was accelerating modifications to existing coking facilities across its European operations to integrate cleaner processing units and meet new European Union carbon reduction targets. The programme involved retrofitting coke oven installations with enhanced gas treatment and emissions reduction technology to reduce the carbon intensity of the coking process without requiring full transition to electric arc furnace steelmaking. The initiative illustrated the steel industry's approach of improving the environmental performance of existing blast furnace and coking infrastructure while the economics and infrastructure for large-scale green hydrogen-based steelmaking continue to develop.

In 2024, JSW Steel, one of India's largest steel producers, reaffirmed plans to expand its total steelmaking capacity from 34.2 million tonnes to 42 million tonnes by September 2027, a scale-up that significantly increases the company's demand for imported metallurgical coal. India emerged as the largest importer of Australian hard coking coal in 2024, absorbing approximately 29 percent of Australia's total metallurgical coal exports between January and September of that year. JSW's expansion, alongside parallel capacity increases by Tata Steel at its Kalinganagar facility, illustrates the structural growth in Indian metallurgical coal demand that is reshaping global seaborne trade flows and benefiting major exporters in Australia and the United States.

In 2024, BHP Group Limited approved an investment of over USD 1.1 billion to extend the operational life of its Blackwater and Daunia coking coal mines in Queensland, Australia. The projects are designed to sustain and enhance the supply of high-grade metallurgical coal to Asian steel producers, particularly in Japan, South Korea, China, and India, which collectively rely on Australian seaborne exports as a critical input for blast furnace coke production. The investment decision reflected BHP's long-term confidence in the structural demand outlook for premium hard coking coal, even amid broader industry transitions toward lower-emissions steelmaking technologies, and signalled continued capital commitment to metallurgical coal as a durable commodity category.

In November 2023, Glencore plc announced and completed the acquisition of a 77 percent interest in the steelmaking coal business of Teck Resources Limited for approximately USD 6.93 billion, creating one of the world's largest exporters of metallurgical coal. The transaction combined Glencore's existing coal operations with Teck's high-quality Queensland coking coal assets, significantly expanding Glencore's seaborne metallurgical coal supply capacity. The deal also incorporated additional payments tied to POSCO and Nippon Steel's attributable shares in the divested business. The acquisition positioned Glencore as a key supplier to blast furnace steelmakers across Asia Pacific, reinforcing the strategic importance of premium hard coking coal assets in an era of sustained steel demand from infrastructure-intensive emerging economies.

India's steel industry is expanding at a pace that is reshaping global metallurgical coal trade patterns, with the country becoming the largest importer of Australian hard coking coal and accounting for 29 percent of Australia's total metallurgical coal exports in the first nine months of 2024. The government's National Infrastructure Pipeline, which involves substantial investment in roads, rail, ports, and real estate, has elevated steel consumption projections by over 130 million tonnes by 2025, directly increasing blast furnace coal requirements. India's domestic coking coal production, which stood at 54.5 million tonnes in FY2023, remains far below national steel production needs, making import dependency structural and persistent. JSW Steel's planned capacity increase to 42 million tonnes by 2027 and Tata Steel's Kalinganagar expansion are driving global coking coal market growth over the forecast period.

The global seaborne metallurgical coal market is undergoing significant ownership consolidation as major miners seek scale, supply chain integration, and cost efficiency in the face of long-term energy transition pressures. Glencore's USD 6.93 billion acquisition of Teck Resources' steelmaking coal assets in 2023 created one of the world's largest exporters of hard coking coal and signalled that premium metallurgical coal assets retain high strategic value despite environmental headwinds. This consolidation trend is reshaping competitive dynamics, as smaller producers find it increasingly difficult to compete with vertically integrated global miners that benefit from direct customer relationships, established port and logistics infrastructure, and the balance sheet capacity to invest in mine life extensions. BHP's USD 1.1 billion commitment to its Queensland operations in 2024 reinforced the same logic.

Steelmakers globally are under increasing regulatory and investor pressure to reduce the carbon intensity of coke-based steelmaking, but the timeline and economics of full transition to hydrogen-based direct reduced iron or electric arc furnace routes continue to limit near-term displacement of metallurgical coal. ArcelorMittal's 2025 initiative to integrate cleaner processing units into existing European coking facilities illustrates the steel industry's preferred near-term approach: improving the environmental performance of established infrastructure rather than abandoning the blast furnace route prematurely. Many major steel producers still rely on the blast furnace route, and their long capital investment cycles make the demand base for coking coal relatively sticky through the forecast period, even as alternative technologies mature.

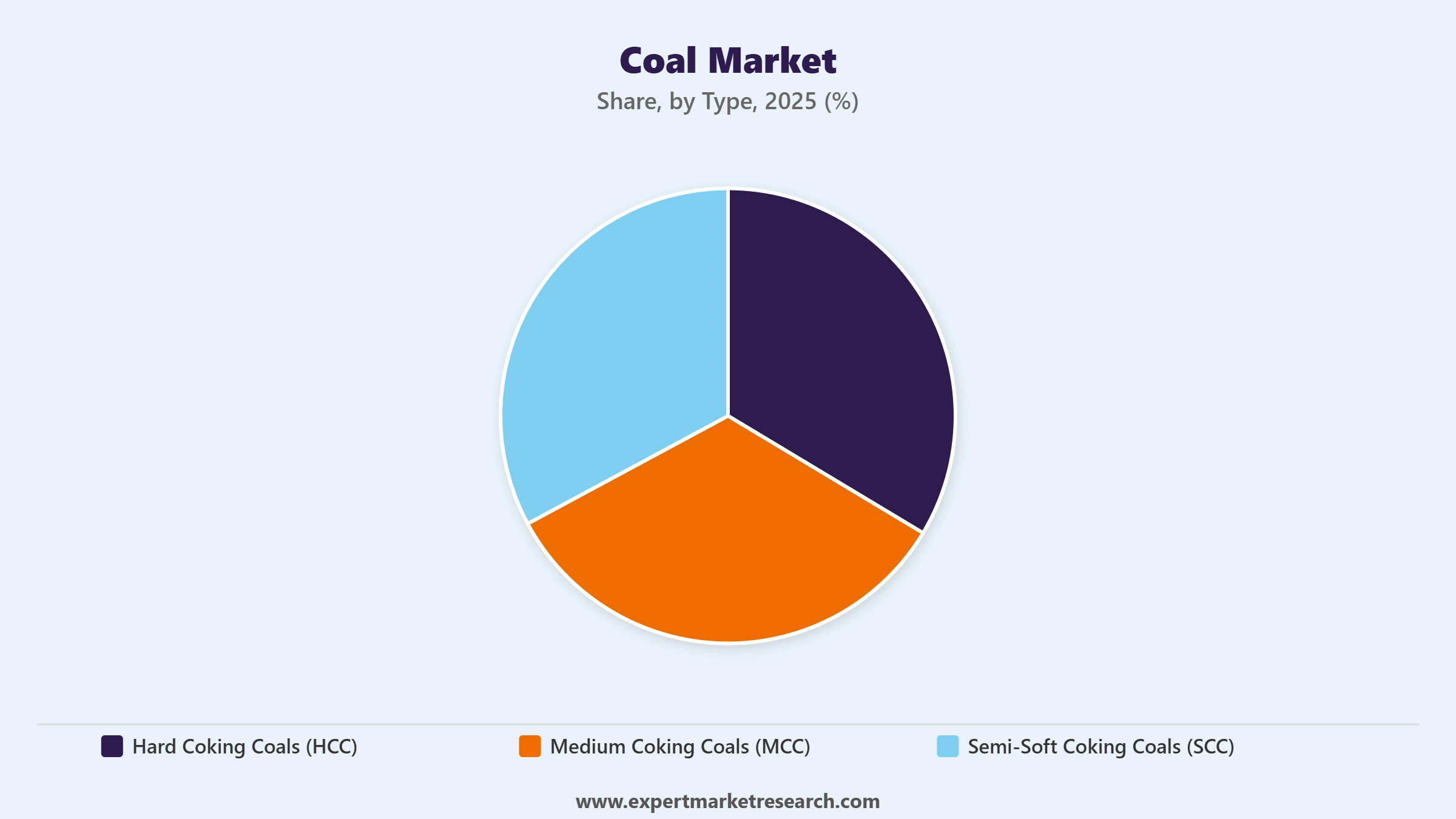

Hard coking coal continues to command a significant premium over semi-soft and medium coking coal grades in global seaborne markets, reflecting its superior coking properties including high carbon content, low sulphur levels, and strong coke strength after reaction metrics that make it the preferred input for high-productivity blast furnace operations. In 2024, HCC held a 56.3 percent share of the global metallurgical coal market by type, anchored by consistent demand from Japanese, South Korean, and Indian integrated steel mills that require high-grade coke for optimal blast furnace efficiency. China's growing role in spot market pricing, accounting for approximately 45 percent of all premium hard coking coal transactions in 2024, has added new dynamics to price discovery and trade flow patterns in the seaborne metallurgical coal market.

The Expert Market Research's report titled “Global Coal Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

Market Breakup by Type

Key Insight: Hard Coking Coals (HCC) hold the dominant share of the global coal market by type, accounting for approximately 56 percent of total metallurgical coal market revenue in 2024. HCC commands the highest prices in the seaborne market due to its exceptional coking properties, including high carbon content, low sulphur and ash levels, and high coke strength after reaction, which make it the benchmark input for blast furnace-based steelmaking. Australia's Queensland coalfields produce much of the world's premium HCC supply, exported predominantly to Japan, South Korea, India, and China. Semi-Soft Coking Coals (SCC) are used in blended coke formulations to manage production costs while maintaining acceptable coke quality, and represent an important complementary grade for steel mills operating in cost-sensitive markets. Medium Coking Coals (MCC) serve a similar blending function, providing steel producers with flexibility to optimise their coal procurement strategies across grades and origins.

Market Breakup by Application

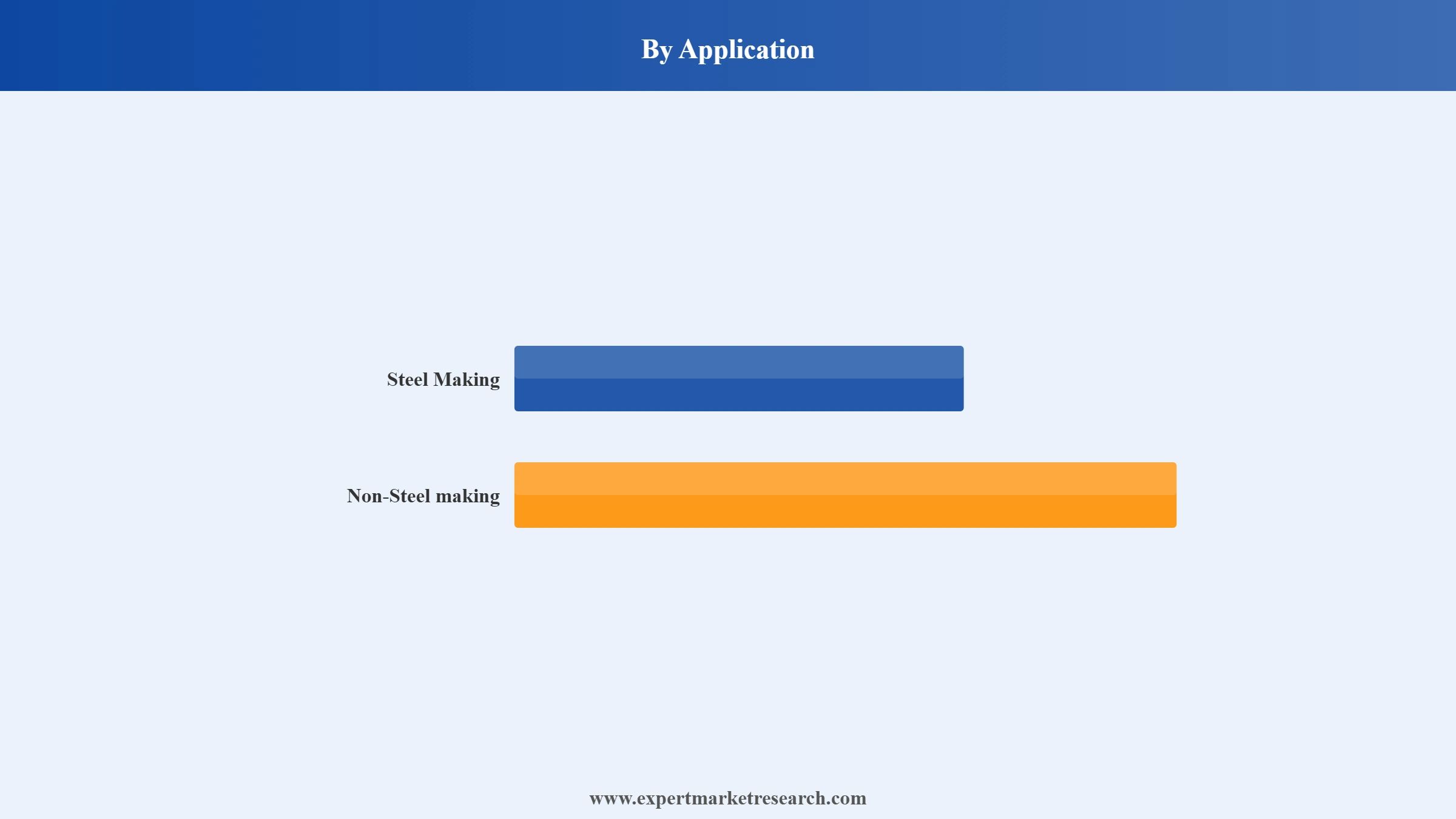

Key Insight: Steel Making is the overwhelmingly dominant application in the global coking coal market, accounting for approximately 65 to 75 percent of total consumption. Coking coal is converted into metallurgical coke in large-scale coke oven batteries and serves as both a fuel and a reducing agent in blast furnaces, facilitating the conversion of iron ore into molten pig iron that is subsequently refined into steel. Approximately 640 kilograms of coal is required to produce one tonne of steel via the blast furnace route, underpinning a large and relatively stable demand base. Non-Steel Making applications encompass the use of coking coal in foundry coke production, ferroalloy smelting, direct carbon injection in steelmaking, and a range of industrial chemical and energy applications. While smaller in volume, the non-steel segment benefits from diversified end-user demand across construction materials, transportation, healthcare infrastructure, and agricultural equipment manufacturing.

Market Breakup by End Use Industry

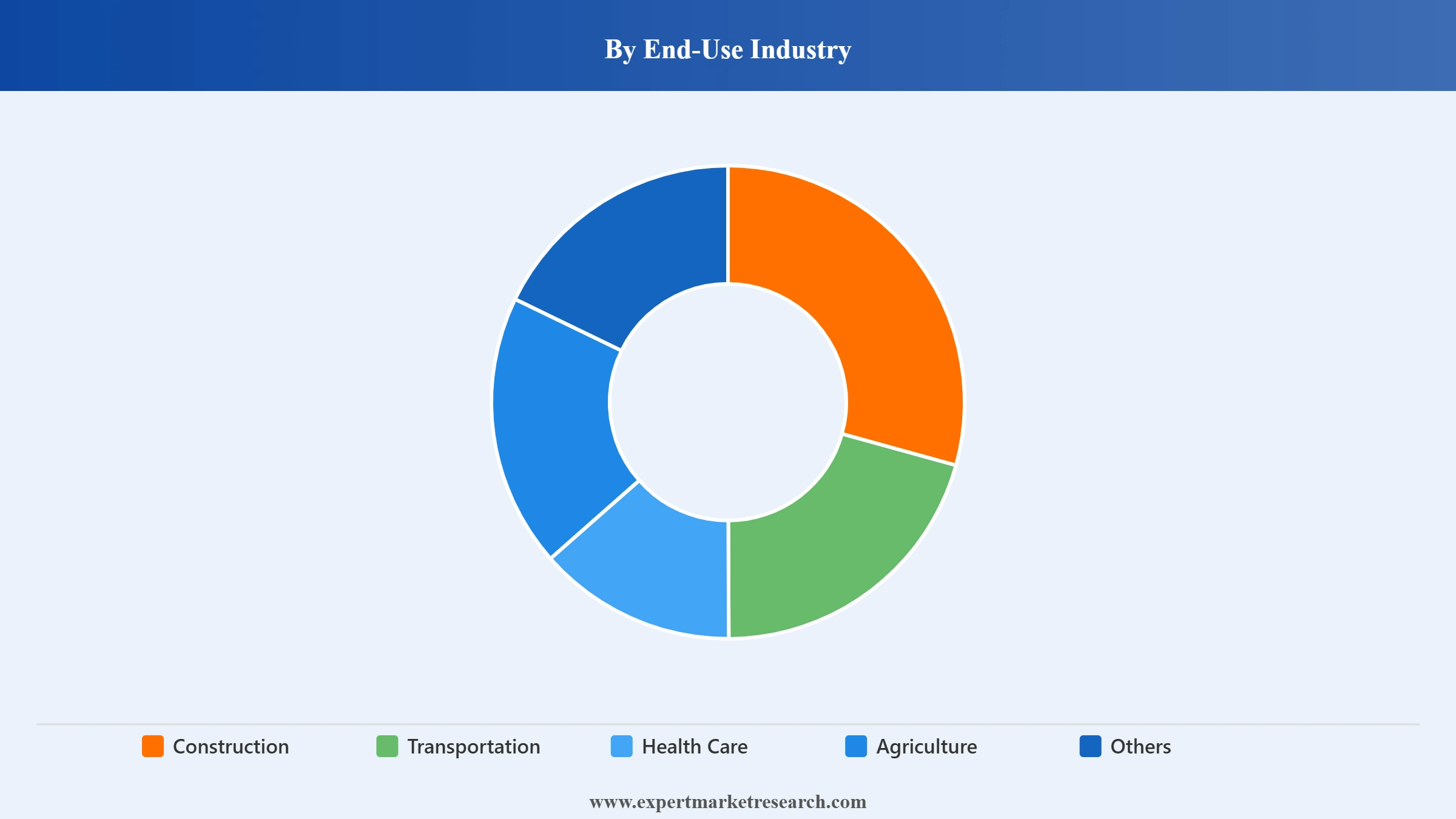

Key Insight: The Construction industry is the dominant end-use sector driving coking coal demand, as the steel produced from blast furnace operations flows directly into structural steel for buildings, bridges, residential towers, commercial real estate, and public infrastructure projects. Emerging economies across Asia, Africa, and Latin America are investing heavily in construction and infrastructure at a scale that sustains long-term coking coal requirements well beyond current forecasts. The Transportation sector consumes steel for railways, shipbuilding, automotive manufacturing, and heavy equipment, all of which contribute to metallurgical coal demand. Healthcare infrastructure investment, particularly in hospital construction and medical equipment manufacturing in developing markets, and agricultural equipment production add further breadth to the end-use demand profile of the coking coal market.

Market Breakup by Region

Key Insight: Asia Pacific dominates the global coal market with over 55 percent of total metallurgical coal demand, driven by China's massive blast furnace steelmaking capacity and India's rapidly expanding steel sector. China alone produced approximately 1.05 billion metric tons of crude steel in 2025, requiring enormous volumes of metallurgical coke derived from domestic and imported coking coal. Japan and South Korea each consume over 10 million metric tons of imported coking coal annually for their integrated steel mills. North America is a significant producer and exporter of metallurgical coal, with US Appalachian and Western Canadian coalfields supplying both domestic steel producers and seaborne export markets. Europe demonstrates moderate consumption, largely tied to blast furnace operations in Germany, France, Poland, and the United Kingdom, with increasing pressure from EU carbon regulations to reduce coke intensity. The Middle East and Africa show the highest projected growth rate among smaller markets, driven by greenfield steel investments in Gulf states and sub-Saharan Africa.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Type

Hard Coking Coals (HCC) command the largest share of the global coking coal market by type, reflecting the irreplaceable role of premium-grade metallurgical coal in high-efficiency blast furnace operations. HCC's price premium over semi-soft and medium coking coal grades reflects genuine quality differentiation in terms of coking properties, and major integrated steel producers in Japan, South Korea, India, and increasingly China consistently prioritise HCC in their blending strategies to maximise coke quality and blast furnace productivity. BHP and Glencore, following the latter's acquisition of Teck's steelmaking coal assets in 2023, are the two largest suppliers of seaborne premium HCC to Asian markets, giving them significant influence over pricing and contract terms.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Application

The Steel Making application accounts for the dominant share of global coking coal demand by application, as blast furnace-based steelmaking remains the predominant route for primary steel production globally. Despite the gradual growth of electric arc furnace technology and early-stage hydrogen-based direct reduction processes, the blast furnace route continues to account for the majority of the approximately 1.95 billion metric tons of crude steel produced globally in 2025. Asia Pacific's steel production infrastructure, which was built at enormous scale over the past three decades and is still expanding in India and Southeast Asia, ensures that steel making will continue to dominate metallurgical coal end use through the forecast period and well beyond.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By End-Use Industry

Within the end-use industry segmentation, the Construction sector is the largest consumer of coking coal’s derivative products, particularly steel for structural applications in buildings, bridges, and civil infrastructure. Asian construction activity, especially in India and Southeast Asia, continues to generate substantial incremental steel demand. The Transportation sector is the second-largest end-use, consuming significant volumes of high-grade steel for automotive, rail, and shipbuilding applications. Healthcare and Agriculture represent smaller but structurally stable end-use categories that rely on steel for medical equipment manufacturing and agricultural machinery production respectively.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Asia Pacific is both the dominant and fastest-growing region in the global coal market. China's blast furnace steelmaking infrastructure is the largest in the world, and despite cyclical fluctuations tied to the residential construction sector, the country's monthly iron ore imports of over 105 million tonnes in mid-2025 pointed to strong forward-looking demand for metallurgical inputs. India represents the most significant growth story in the seaborne coking coal market, with JSW Steel's capacity expansion to 42 million tonnes, Tata Steel's Kalinganagar investment, and the government's National Infrastructure Pipeline collectively driving a step-change in coking coal import requirements. Japan and South Korea are mature but stable consumers of premium HCC, with long-term procurement contracts with Australian and North American producers ensuring supply security for their integrated steel mills.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

North America is a significant producer and net exporter of metallurgical coal, with the US Appalachian basin and Canadian Western coalfields supplying both domestic steel producers and seaborne export markets in Asia and Europe. Key North American producers including Arch Resources, Peabody Energy, and Coronado Global Resources maintain export terminals along the Gulf Coast and Eastern Seaboard. Europe represents a moderate but structurally constrained demand base, as EU carbon regulations are gradually increasing the cost pressure on blast furnace and coking operations, though complete displacement of coking coal from European steelmaking remains a decade or more away. The Middle East and Africa region is expanding its steel production footprint, with Saudi Arabia, South Africa, and emerging producers in sub-Saharan Africa investing in new blast furnace and coking coal infrastructure that is projected to drive above-average regional demand growth through the forecast period.

The global coking coal market is dominated by a small number of large, vertically integrated mining companies with substantial seaborne export capacity and long-term supply relationships with major Asian and European steel producers. Competitive advantage is determined primarily by coal quality (particularly HCC grade purity), production cost efficiency, access to port and rail infrastructure, and the ability to offer reliable supply through multiple commodity price cycles. Market concentration has increased significantly following the 2023 Glencore-Teck transaction, and further consolidation is possible as smaller producers face mounting capital requirements and environmental compliance costs.

Chinese state-owned enterprises including China Coal Energy Group and China Shenhua dominate domestic supply within China, which produces the majority of its coking coal needs from domestic mines but selectively imports premium grades for quality-sensitive applications. Coal India Ltd. serves the Indian domestic market as the country's largest producer but does not supply significant volumes of the hard coking coal grades that Indian integrated steel mills require from seaborne sources. Australian producers, led by BHP and Whitehaven Coal, hold the strongest position in the premium seaborne HCC segment due to the unmatched quality of Queensland coking coal deposits.

Arch Resources, Inc. (formerly Arch Coal) is a leading US producer of metallurgical coal, founded in 1969 and headquartered in St. Louis, Missouri. The company operates mines in the Appalachian basin and the Powder River Basin, with its metallurgical coal operations focused on West Virginia and Virginia. Arch Resources supplies premium low-vol and high-vol coking coal to domestic steelmakers and seaborne export markets in Europe and Asia. The company has consistently invested in safety and operational efficiency improvements at its mines and maintains a disciplined approach to capital allocation that targets returns across the commodity price cycle.

Founded in 1883 and headquartered in St. Louis, Missouri, Peabody Energy Corp. is one of the world's largest private-sector coal companies, with significant metallurgical coal operations in Queensland, Australia and the Appalachian region of the United States. The company supplies high-quality coking coal to steel producers across Asia and the Americas and has maintained a focus on enhancing mine productivity and adopting cleaner extraction practices to comply with evolving environmental standards. Peabody's Australian assets in the Bowen Basin provide direct access to the seaborne HCC market, making it a natural supplier to Japanese, South Korean, and Indian integrated steel producers.

China Coal Energy Group Co. is a major state-owned coal producer and trader headquartered in Beijing, China, with operations spanning coal mining, coal processing, equipment manufacturing, and chemical production. The company is among the largest producers of coking coal in China and plays a key role in supplying metallurgical coal to China's domestic steel industry. China Coal Energy also manages significant coal trading operations and maintains coal import and export capabilities that allow it to participate in seaborne market dynamics when domestic supply and demand conditions warrant. The company has been expanding its coal chemical and diversification activities alongside its core mining business.

Founded in 1975 and headquartered in Kolkata, India, Coal India Ltd. is the world's largest coal mining company by production volume, operating as a state-owned enterprise under the Indian government. The company produces primarily thermal and non-coking coal for the Indian power sector, with coking coal production forming a smaller but strategically important segment of its portfolio. India's domestic coking coal output significantly lags behind national steel production requirements, making the gap between Coal India's coking coal production capacity and India's import dependency a structural feature of the Indian metallurgical coal market and a sustained driver of seaborne import volumes from Australia and the United States.

Other key players in the market are Anglo American plc, China Shenhua Energy Company Limited, BHP Group Limited, Glencore plc, Whitehaven Coal Limited, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Understand the trajectory of the global coal market from 2026 to 2035 with our comprehensive research report. Whether you are a mining company assessing capital allocation, a steel producer evaluating long-term supply security, a commodity trader analysing seaborne market dynamics, or an investor sizing the metallurgical coal opportunity, our report provides the data, analysis, and competitive intelligence you need. Download your free sample today and explore the full scope of demand, trade, and competitive dynamics across the global coking coal sector.

Coal Infrastructure and Bulk Energy Logistics

Coal Demand and Industrial Energy Transition

Coal Trade Flows and Energy Security Strategy

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market reached an approximate volume of 8811.34 MMT.

The market is projected to grow at a CAGR of 1.60% between 2026 and 2035.

The market is estimated to witness healthy growth in the forecast period of 2026-2035 to reach around 10327.12 MMT by 2035.

The different regions considered in the market report include North America, Europe, the Asia Pacific, Latin America, and the Middle East and Africa.

The different types of coal in the market are hard coking coals, medium coking coals, and semi-soft coking coals.

The different applications of coal in the market are Steel Making and Non-Steel making.

The different end use industries in the market include construction, transportation, health care, and agriculture, among others.

Key players in the market are Arch Resources, Inc., Peabody Energy Corp., China Coal Energy Group Co., Coal India Ltd., Anglo American plc, CHINA SHENHUA, BHP Group Limited, Glencore plc, and Whitehaven Coal Limited, among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Type |

|

| Breakup by Application |

|

| Breakup by End-Use Industry |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.