Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

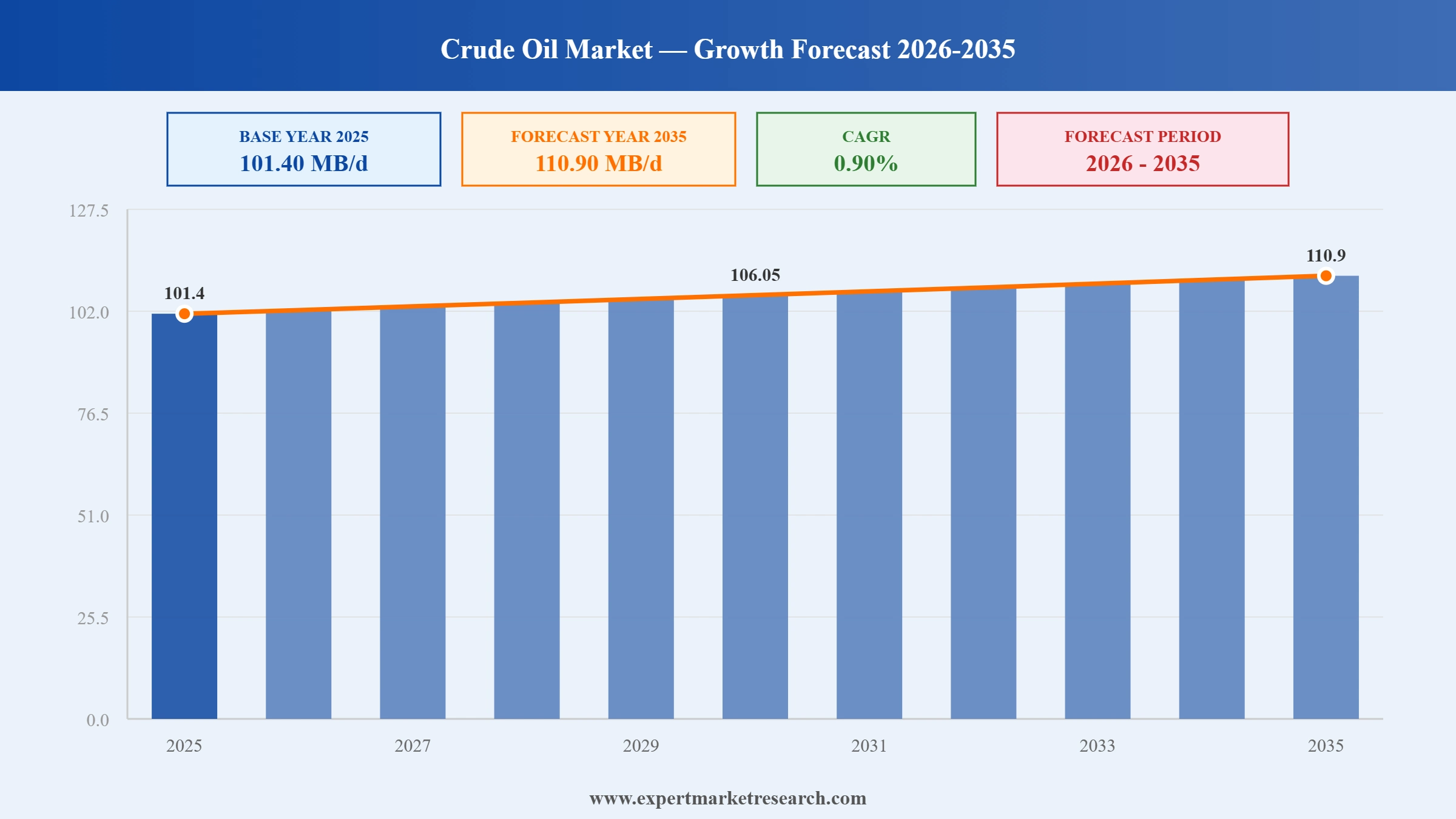

The global crude oil market reached a volume of 101.40 MB/d at 2025 and is projected to expand at a CAGR of around {{CAGR}}% during the forecast period of 2026-2035. With continued demand from transportation, petrochemical feedstocks, and industrial applications across emerging economies, alongside growing exploration and production activity in key upstream regions, the market is expected to reach 110.90 MB/d by 2035 by 2035.

According to The Economic Times, the International Energy Agency reported in April 2026 that global oil supply and demand growth is set to contract this year as the ongoing Middle East war sharply disrupts flows through key routes like the Strait of Hormuz. This shift is relevant to the crude oil market because slower demand growth and supply challenges continue to support price volatility and influence trading and procurement strategies worldwide.

According to Economy Middle East, OPEC and its allies agreed to boost crude oil output by around 206,000 barrels per day starting in April 2026 after pausing increases for three months. The decision aims to help balance tightening markets and mitigate price spikes caused by geopolitical tensions. For the crude oil market, this production adjustment signals coordinated efforts to stabilize supply amid ongoing global uncertainty.

Read more about this report -REQUEST FREE SAMPLE COPY IN PDF

| Global Crude Oil Market Report Summary | Description | Value |

| Base Year | MB/d | 2025 |

| Historical Period | MB/d | 2019-2025 |

| Forecast Period | MB/d | 2026-2035 |

| Market Size 2025 | MB/d | 101.40 |

| Market Size 2035 | MB/d | 110.90 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 0.90% |

| CAGR 2026-2035 - Market by Region | Asia Pacific | 1.0% |

| CAGR 2026-2035 - Market by Country | India | 1.3% |

| CAGR 2026-2035 - Market by Country | China | 1.2% |

| Market Share by Country 2025 | UK | 3.5% |

The global crude oil market is shaped by evolving geopolitical dynamics, OPEC+ production management, sustained demand from transportation and petrochemical sectors, and long-cycle upstream investment decisions. While energy transition initiatives are influencing long-term demand trajectories, near-term market fundamentals remain supported by continued consumption growth in Asia Pacific, strategic capacity expansions by national oil companies, and consolidation activity among major independent exploration and production companies.

CNOOC Limited announced its highest-ever annual oil and gas production of 777.3 million barrels of oil equivalent (MMboe) for the full year 2025 in March 2026, reflecting approximately 11.7% year-on-year growth. The company unveiled capital expenditure guidance of RMB 112-122 billion for 2026 and set production targets of 780-800 MMboe, underpinned by continued development of deep-water and unconventional assets across its Chinese and international portfolio.

Devon Energy reported record Permian Basin oil production in September 2025, driven by the deployment of its enhanced well completion techniques across the Delaware Basin. The company also advanced integration of assets acquired through prior consolidation, demonstrating improved capital efficiency and well productivity metrics that support its multi-year production growth outlook in the US lower 48 unconventional crude oil resource base.

OPEC+ announced the commencement of a phased and gradual unwinding of its voluntary production cuts in April 2025, signalling a cautious return of withheld supply to the global crude oil market. The decision reflected the group's assessment of improving demand fundamentals and inventory levels, with participating members committing to data-dependent monthly adjustments designed to balance global supply without triggering price dislocation across benchmark markets.

ConocoPhillips completed its USD 22.5 billion all-stock acquisition of Marathon Oil Corporation in November 2024, creating one of the largest US independent exploration and production companies. The combination added approximately 2 billion barrels of oil equivalent in US resource inventory, with primary positions in the Eagle Ford, Bakken, and Permian Basin shale plays, significantly enhancing ConocoPhillips's low-cost of supply portfolio and long-term production growth runway.

US Shale Resilience: Continued improvements in horizontal drilling efficiency, multi-well pad development, and advanced completion techniques are enabling US tight oil producers to maintain near-record production volumes at lower breakeven costs. The sustained productivity gains across the Permian Basin, Eagle Ford, and Bakken are reinforcing US crude oil's structural role as a swing supply source in the global market, limiting price recovery cycles and altering traditional OPEC+ supply management dynamics.

Energy Transition Investment: Major international oil companies are navigating the competing imperatives of near-term oil production profitability and long-term portfolio decarbonisation. Capital allocation strategies increasingly reflect a dual approach of investing in high-return, low-cost upstream oil assets while simultaneously expanding renewable energy, carbon capture, and hydrogen capabilities, reflecting regulatory pressure and investor expectations for credible transition pathways alongside sustained hydrocarbon returns.

Deepwater Expansion: A new wave of deepwater project sanctions in Guyana's Stabroek Block, Brazil's pre-salt Santos Basin, and West African offshore acreage is set to deliver significant volumes of high-quality light crude oil to global markets through the forecast period. These long-cycle projects offer competitive economics, high reservoir recovery rates, and low carbon intensity per barrel, attracting sustained capital commitment from major operators despite broader energy transition pressures on upstream investment.

National Oil Company Expansion: State-backed oil producers across the Middle East, Asia Pacific, and Latin America are driving the majority of new upstream capacity investment, with NOCs from Saudi Arabia, UAE, Iraq, Kuwait, and Brazil advancing multi-year development programmes targeting sustained production capacity growth. These investments are underpinned by sovereign fiscal priorities, long-term demand management strategies, and the competitive advantage of NOCs in maintaining low finding and development costs across their resource-rich producing basins.

Refinery Rationalization: Global refinery configurations are adapting to changing crude oil quality differentials, with medium and heavy sour crude processing capacity in Asia Pacific and the Middle East expanding to process cost-advantaged OPEC+ barrels. Simultaneously, US and European refiners are optimising their crude slates to maximise lighter product yields as transportation fuel specifications tighten and petrochemical feedstock integration expands across integrated downstream complexes.

"Global Crude Oil Market Report and Forecast 2026-2035" offers a detailed analysis of the market based on the following segments:

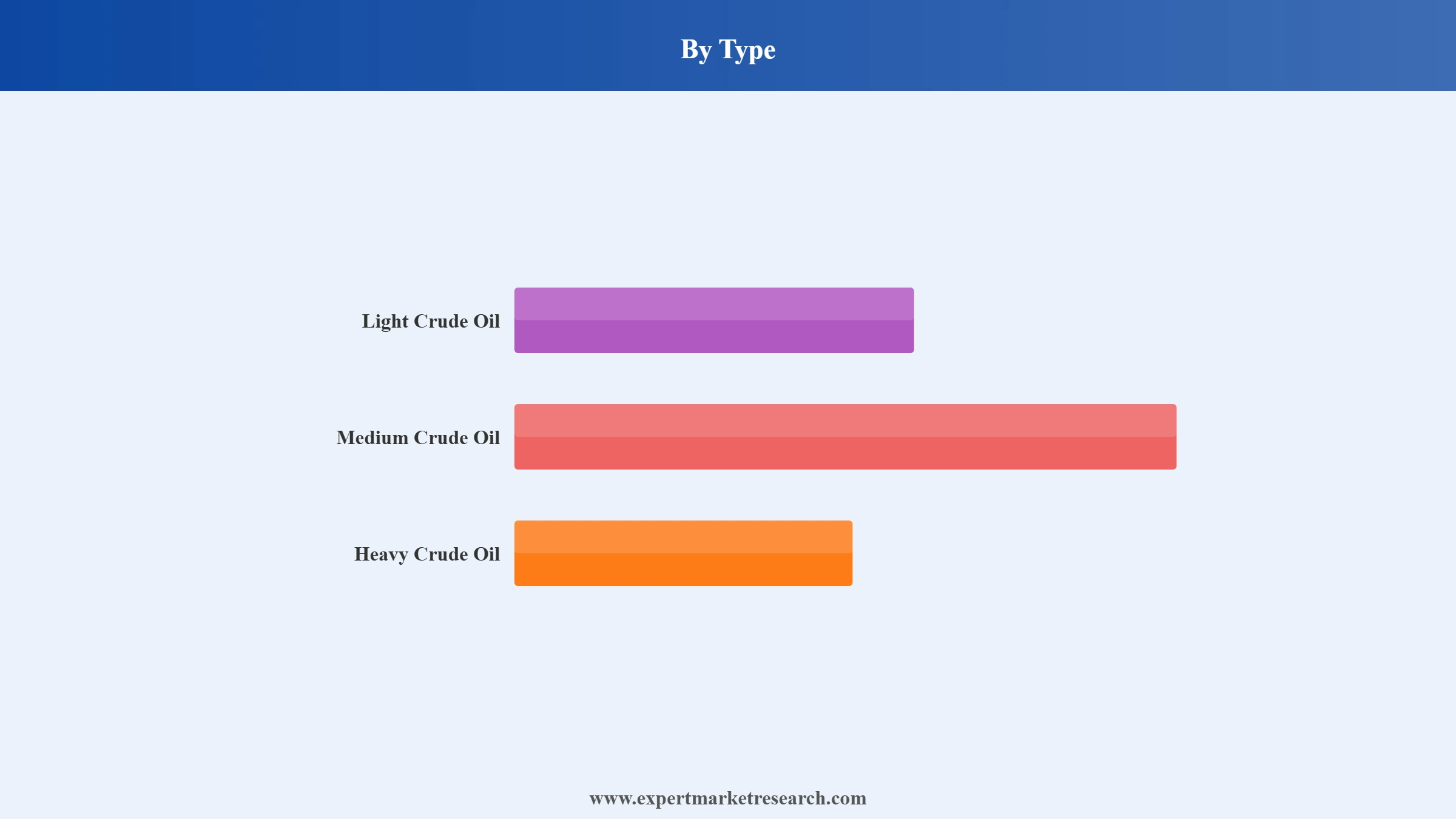

Market Breakup By Type

Key Insight: Light crude oil holds the largest share in the global crude oil market by type, driven by its superior refinery yields of high-value transportation fuels and its lower processing costs relative to heavier grades. The dominance of light crude is supported by growing US tight oil production from the Permian Basin and other shale plays, which consistently produce lighter API gravity barrels. Medium crude oil is the most widely traded grade globally, balancing refinery economics with broad availability from OPEC+ member states, while heavy crude oil remains strategically important for complex deep-conversion refineries in Asia Pacific and the Americas.

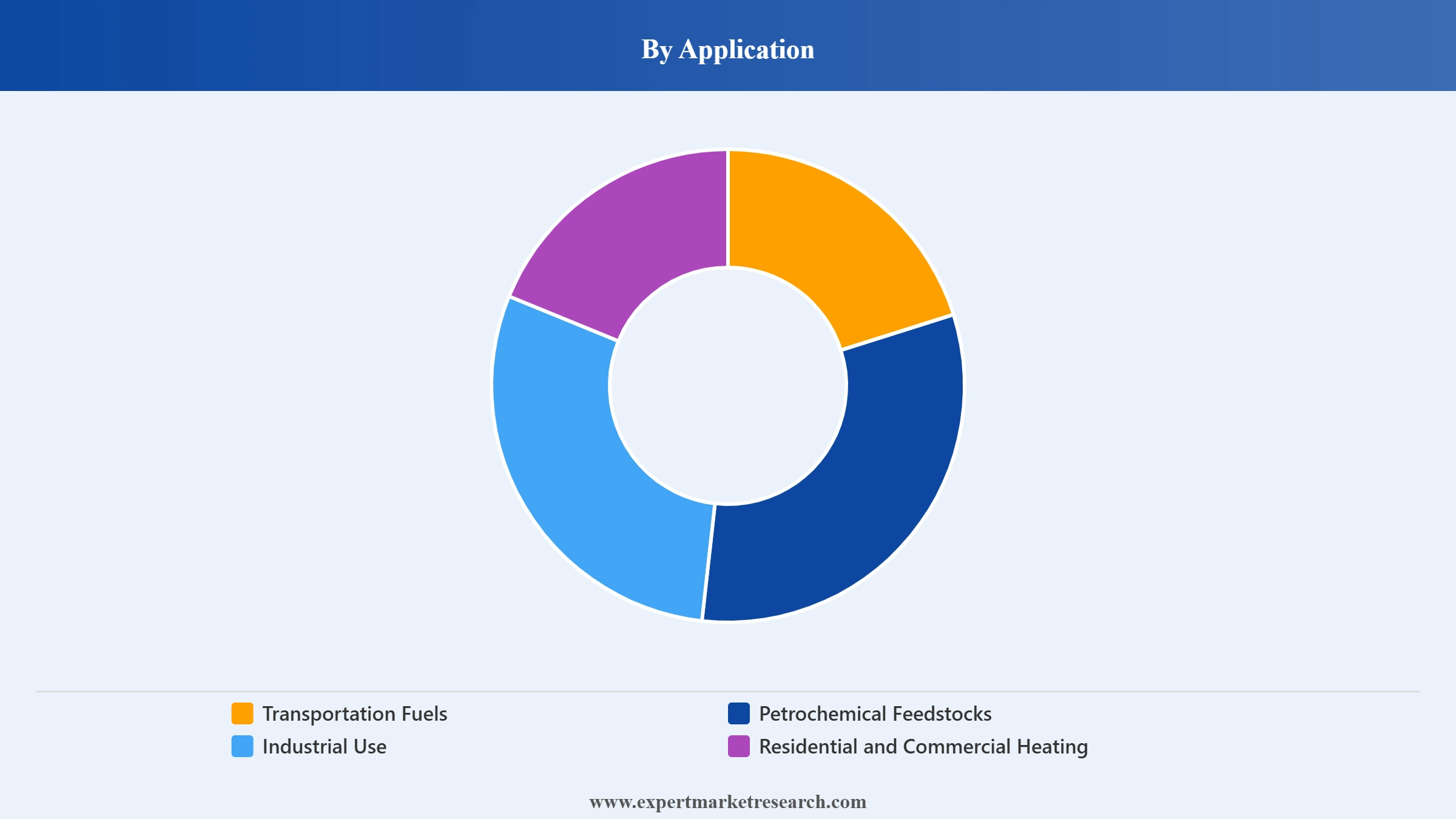

Market Breakup By Application

Key Insight: Transportation fuels represent the dominant application segment for crude oil, consuming approximately 57% of global refined product output through gasoline, diesel, and jet fuel. Continued vehicle fleet growth in emerging markets across Asia Pacific, Africa, and Latin America sustains transportation fuel demand despite increasing electric vehicle penetration in developed markets. Petrochemical feedstocks represent the fastest-growing application segment, with strong demand for naphtha, ethane, and LPG from Asian petrochemical complexes expanding the petrochemical share of crude oil consumption as chemical demand growth outpaces fuel demand growth in the long term.

Market Breakup By Extraction Method

Key Insight: Onshore production remains the dominant extraction method, accounting for approximately 70% of global crude oil output, supported by the large-scale conventional fields in the Middle East, Russia, and North America. Onshore production benefits from lower development and operating costs relative to offshore alternatives, with US shale development reinforcing its pre-eminence through sustained horizontal drilling and completion programme investment. Deepwater and ultra-deepwater extraction represent the fastest-growing offshore segment, driven by major project sanctions in Guyana, Brazil, and Sub-Saharan Africa, where reservoirs offer prolific production rates and competitive full-cycle economics.

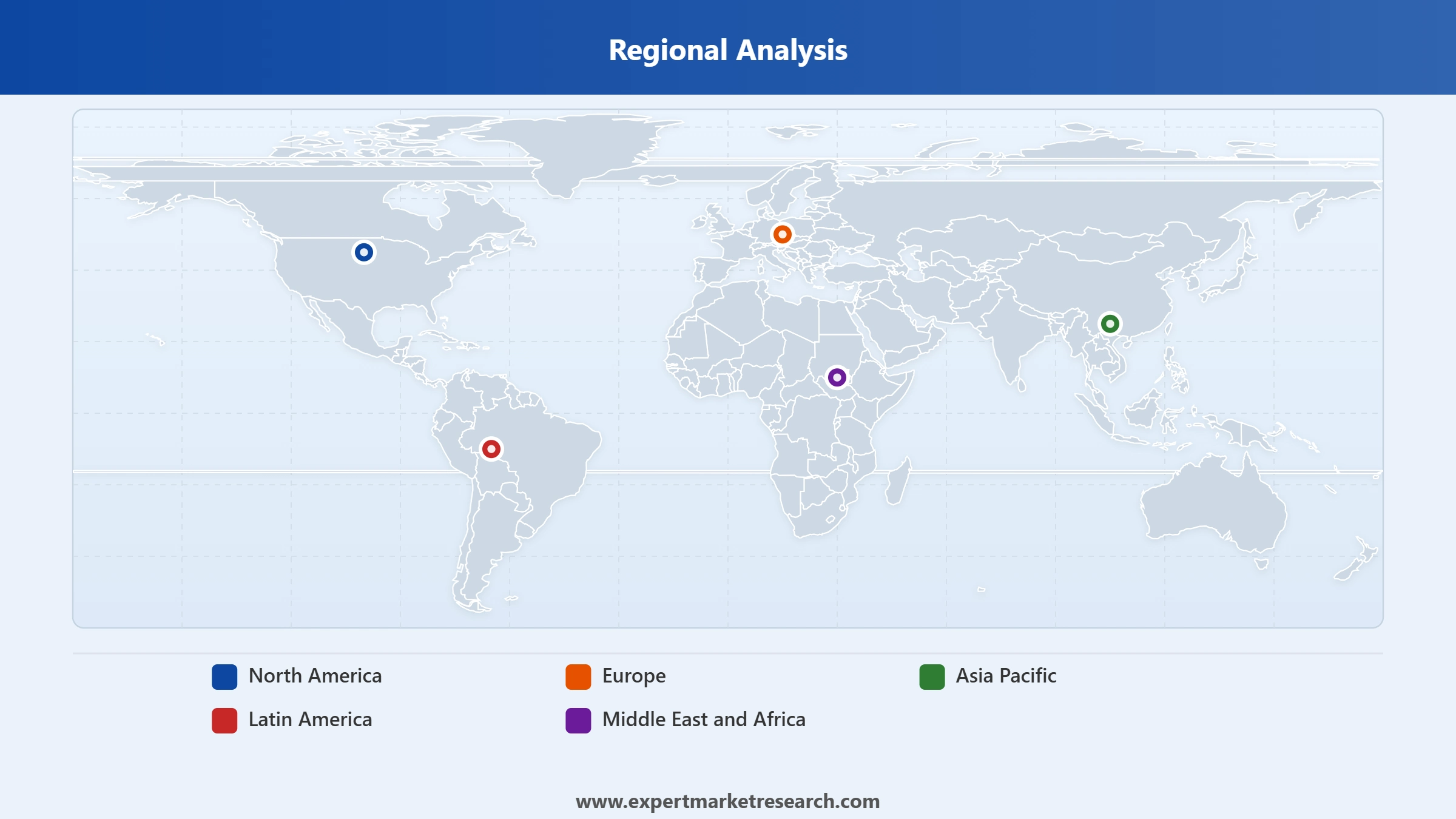

Market Breakup by Region

Key Insight: The Middle East and Africa region holds the dominant share of global crude oil production, accounting for approximately 32% of global supply, underpinned by the vast conventional reservoirs of Saudi Arabia, Iraq, UAE, Kuwait, and Iran. The region benefits from the world's lowest lifting costs, highest reserve life indices, and OPEC+ coordination capacity. North America is the second-largest producing region, driven by record US tight oil output and Canadian oil sands production, while Asia Pacific represents the highest-demand region and a growing production contributor through CNOOC's deepwater expansion programmes.

Read more about this report -REQUEST FREE SAMPLE COPY IN PDF

By Type, light crude oil commands the largest market share due to superior refining economics and growing US tight oil production volumes

Light crude oil's dominance in the global market reflects the alignment between its physical properties and the refinery configurations most prevalent across North America, Europe, and Asia Pacific. US tight oil production from the Permian Basin, Eagle Ford, and Bakken has consistently delivered light API gravity crude that commands premiums over heavier benchmarks at complex refinery gate configurations. The light crude segment also benefits from the prolific deepwater developments in Guyana and Brazil, which produce high-quality light barrels with low sulphur content suited to gasoline and petrochemical feedstock production.

Read more about this report -REQUEST FREE SAMPLE COPY IN PDF

Heavy crude oil maintains strategic market relevance for deep-conversion refineries configured to process heavier, higher-sulphur grades from Venezuela, Canada, Mexico, and parts of the Middle East. The economic advantage of heavy crude lies in its discounted pricing relative to light benchmarks, enabling complex refinery operators to achieve superior margin capture through conversion of residual fractions into high-value distillate products. However, environmental regulations and carbon pricing mechanisms in key markets are gradually pressuring heavy crude demand as refiners optimise crude slates toward lower-carbon-intensity barrels.

By Application, transportation fuels account for the dominant share of crude oil end-use consumption across all major consuming regions globally

Transportation fuels consume the largest share of global crude oil output, reflecting the continued dependence of road, aviation, and maritime transport on liquid petroleum products. Despite structural shifts in vehicle ownership trends in Western markets, absolute transportation fuel demand continues to grow in Asia Pacific, Africa, and the Middle East, where vehicle fleet expansion, rising middle-class incomes, and limited public transport infrastructure sustain consumption growth. Aviation fuel demand recovery following disruption in prior years has also contributed to the transportation segment's dominant consumption position.

Read more about this report -REQUEST FREE SAMPLE COPY IN PDF

Petrochemical feedstocks represent the most strategically significant growth application in the global crude oil market, with naphtha and ethane cracking capacity expansion in China, India, and the Middle East driving incremental crude oil demand from the chemicals sector. In September 2025, Devon Energy's Permian Basin production record highlighted the continued competitiveness of US light crude as an ethane and naphtha feedstock supplier for domestic and export chemical production. The International Energy Agency projects petrochemical applications to account for the majority of net crude oil demand growth through the forecast period as transportation fuel demand matures in developed markets.

By Region, the Middle East and Africa holds the largest production share due to its conventional reservoir scale and lowest global lifting cost base

The Middle East and Africa region's production dominance in the global crude oil market reflects the geological endowment of the Arabian Peninsula and the operational scale of national oil companies including Saudi Aramco, ADNOC, Iraq's SOMO, and Kuwait Petroleum Corporation. These producers maintain the world's largest proven reserves, multi-decade reserve lives, and production costs averaging USD 3-8 per barrel, enabling sustained competitive supply even during extended price downturns. OPEC+ coordination among Middle Eastern producers provides additional market management capacity that underpins regional market share stability.

Read more about this report -REQUEST FREE SAMPLE COPY IN PDF

North America is the world's largest crude oil producing region by volume growth, driven by the remarkable expansion of US tight oil output from the Permian Basin. In November 2024, ConocoPhillips's completion of the Marathon Oil acquisition exemplified the consolidation trend reshaping the US E&P sector toward larger, more cost-efficient operators capable of sustaining high-return capital programmes through commodity price cycles. Canada's oil sands production further contributes to North America's production base, while Mexico's Pemex is stabilising output through priority field development programmes supported by government capital injection.

Asia Pacific leads the market in crude oil consumption growth, driven by transportation fleet expansion and petrochemical sector development across emerging economies

Asia Pacific is the world's largest crude oil consuming region and the primary growth driver for global demand, with China, India, Japan, and South Korea representing the dominant refining and consumption centres. China's refinery throughput expansion, India's rapidly growing vehicle fleet, and Southeast Asian industrial development collectively sustain the region's 1.2% CAGR demand growth projection through the forecast period. The region's consumption is overwhelmingly met through imports, making Asia Pacific the key destination market for Middle Eastern, Russian, and West African crude oil exports, and the primary pricing reference point for key benchmark grades including Dubai and Oman.

North America is the world's largest crude oil producing region, with the United States maintaining record production levels supported by unconventional resource development. The region benefits from diversified production geography, advanced upstream technology deployment, and a fully integrated pipeline, refinery, and export terminal infrastructure. US crude oil export growth has fundamentally reshaped global trade flows, with American light sweet crude now competing for Asian market share against traditional Middle Eastern and Russian barrels. Canada's oil sands operations and growing offshore production further strengthen North America's strategic position in the global crude oil supply balance.

The global crude oil market features a complex competitive structure comprising national oil companies (NOCs), international oil companies (IOCs), and independent exploration and production companies. National oil companies representing state interests in major producing countries control the majority of global reserves and production capacity, while IOCs and independents compete for acreage positions in frontier and non-OPEC producing regions. Competitive dynamics are shaped by exploration success rates, production cost structures, access to capital, reserve replacement, and the ability to navigate regulatory and geopolitical environments in diverse operating jurisdictions.

Founded in 1925 and headquartered in New York, United States, Hess Corporation is an independent exploration and production company with operations focused on the United States, Guyana, the Gulf of Mexico, and Southeast Asia. Hess holds a significant equity stake in the prolific Stabroek Block offshore Guyana, operated by ExxonMobil, which represents one of the world's largest recent deepwater crude oil discoveries with multiple major projects delivering growing production volumes.

Founded in 1998 and headquartered in Beijing, China, China Petrochemical Corporation (Sinopec Group) is one of the world's largest integrated energy and chemical companies, with extensive upstream crude oil exploration and production operations across China and international assets in the Middle East, Africa, and Central Asia. Sinopec's upstream business focuses on supplying feedstock to its large-scale domestic refinery and petrochemical operations.

Founded in 1917 and headquartered in Houston, Texas, United States, ConocoPhillips is one of the world's largest independent exploration and production companies following the completion of its acquisition of Marathon Oil Corporation in November 2024. ConocoPhillips operates a diversified portfolio of low-cost upstream assets spanning the United States, Norway, Canada, Australia, Malaysia, and Qatar, with a strategic focus on low cost of supply, disciplined capital allocation, and competitive shareholder returns.

Nobel Energy Management LLC is an oil and gas exploration and production company with a portfolio of onshore and offshore upstream assets. The company participates in crude oil production across multiple international jurisdictions, contributing to global supply through conventional and unconventional resource development programmes aligned with its production growth and capital efficiency objectives.

Other key players in the market are Devon Energy, Marathon Oil, PJSC NK Rosneft, Saudi Aramco, Kuwait Petroleum Corporation, China National Petroleum Corporation, Occidental Petroleum, Valero Energy, CNOOC Limited, Reliance Industries, Petroleo Brasileiro, Equinor ASA, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Navigate the complexities of the evolving global crude oil market with our comprehensive market report for 2026. Whether you are an energy company assessing upstream investment priorities, a refinery optimising its crude procurement strategy, a financial institution evaluating energy sector exposure, or a policy analyst tracking global supply dynamics, our research delivers the data-driven insights you need. Access detailed volume forecasts by segment, competitive profiles of leading operators, and regional supply and demand analysis. Download your free sample today and gain a decisive advantage in understanding the global crude oil market.

Energy Transition Impact On Crude Oil Demand

Downstream Oil Refining Petrochemical Insights

Crude Oil Market Innovations Trading Systems

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market attained a volume of nearly 101.40 MB/d.

The market is assessed to grow at a CAGR of 0.90% between 2026 and 2035.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach about 110.90 MB/d by 2035.

The major market drivers are the increasing popularity of air travel and the extensive usage of hydrocarbons in everyday products.

The key trends aiding the market growth are the rising demand for petrochemicals, advancements in extraction technologies, and increasing exploration of shale oil reserves and deposits.

The major regions in the market are North America, Latin America, the Middle East and Africa, Europe, and the Asia Pacific.

The major players in the market are Hess Corporation, China Petrochemical Corporation, ConocoPhillips Company, Nobel Energy Management LLC, Devon Energy Corporation, Marathon Oil Corporation, PJSC NK Rosneft, Saudi Arabian Oil Company (Saudi Aramco), Kuwait Petroleum Corporation, China National Petroleum Corporation, Occidental Petroleum Corporation, Valero Energy Corporation, China National Offshore Oil Corporation, Reliance Industries Limited, Petróleo Brasileiro S.A., and Equinor ASA, among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Type |

|

| Breakup by Application |

|

| Breakup by Extraction Method |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.