Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

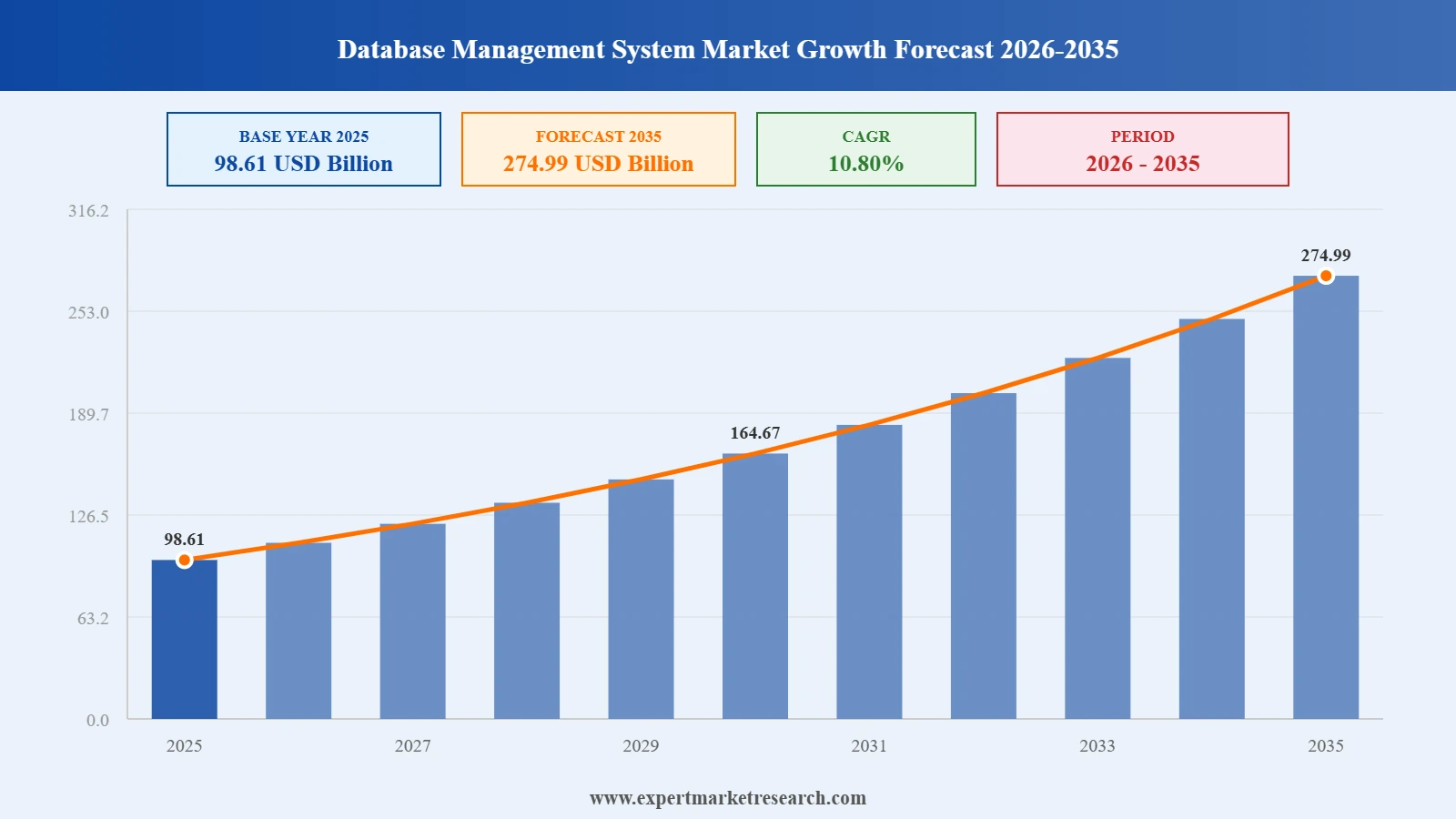

The Global Database Management System (DBMS) Market reached a value of USD 98.61 Billion at 2025 and is projected to expand at a CAGR of around 10.80% during the forecast period of 2026-2035. With cloud-first adoption, AI and automation integration, multi-model database deployment, and rising enterprise data security needs, the market is expected to reach USD 274.99 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

| Global Database Management System (DBMS) Market Report Summary | Description | Value |

| Base Year | USD Billion | 2025 |

| Historical period | USD Billion | 2019-2025 |

| Forecast Period | USD Billion | 2026-2035 |

| Market Size 2025 | USD Billion | 98.61 |

| Market Size 2035 | USD Billion | 274.99 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 10.80% |

| CAGR 2026-2035 - Market by Region | Asia Pacific | 11.7% |

| CAGR 2026-2035 - Market by Country | India | 12.0% |

| CAGR 2026-2035 - Market by Country | China | 11.2% |

| CAGR 2026-2035 - Market by Type | NoSQL | 12.3% |

| CAGR 2026-2035 - Market by Deployment Model | On Premise | 11.2% |

| Market Share by Country | USA | 33.4% |

The Global Database Management System (DBMS) market growth is being shaped by AI-native databases, accelerated cloud migration, the rise of vector and multi-model engines, and tightening data sovereignty requirements that are reshaping enterprise data architectures.

Amazon Web Services moved Amazon Aurora DSQL to general availability at re:Invent 2025, introducing a fully serverless, distributed SQL engine designed for active-active multi-region deployments. The service targets globally distributed applications that require strong consistency without operational overhead, complementing Aurora PostgreSQL and Aurora MySQL. AWS also brought S3 Vectors to general availability, providing native vector storage for AI workloads. Together, the launches sharpen AWS's competitive position against Oracle, Microsoft, and Google in the cloud database management market.

Microsoft made SQL Server 2025 generally available at Ignite 2025, positioning it as an AI-ready enterprise database with built-in vector search, native JSON, REST endpoint invocation, regular expression support, and change-event streaming via Azure Event Hubs. The release lifted Standard edition limits to 32 cores and 256 GB of memory and introduced ZSTD backup compression, secondary-replica backups in Always On Availability Groups, and ARM64 support through SQL Server Management Studio 22, deepening Microsoft's role in enterprise data platforms globally.

Oracle and Amazon Web Services made Oracle Database@AWS generally available, allowing customers to run Oracle Exadata Database Service and Oracle Autonomous AI Database directly inside AWS regions. The launch unifies low-latency networking, native AWS service integration, and Oracle's mission-critical engines, simplifying multi-cloud architectures for banks, insurers, and large enterprises that need to modernise legacy databases without re-platforming. The collaboration also previewed Oracle Autonomous AI Lakehouse, signalling a deeper push into AI-ready, hybrid data infrastructure.

IBM announced its intent to acquire DataStax to deepen the watsonx.data platform with NoSQL and vector-database capabilities derived from Apache Cassandra and Langflow. The deal targets enterprise generative AI workloads where unstructured data, semantic search, and low-code agent development are pivotal. By bringing AstraDB and DataStax Enterprise inside IBM's data fabric, the company aims to strengthen retrieval-augmented generation and accelerate adoption of agentic AI applications across regulated industries such as banking, healthcare, and the public sector.

MongoDB acquired Voyage AI, a developer of embedding and reranking models, to integrate high-accuracy retrieval directly into its document database. The move addresses LLM hallucinations by improving context retrieval for domain-specific applications in finance, law, and healthcare. By embedding Voyage AI's models into Atlas Vector Search, MongoDB strengthens its position as an AI-native operational data platform and reduces customer dependence on bolt-on retrieval pipelines, making mission-critical generative AI deployments more reliable for enterprise developers.

Enterprise database vendors are embedding AI features such as vector search, semantic indexing, and natural-language querying into core engines, moving these capabilities from add-on tools to first-class citizens. The shift is fuelled by demand for retrieval-augmented generation, agentic workflows, and faster developer onboarding. In November 2025, Microsoft released SQL Server 2025 with native vector search, REST endpoint invocation, and AI-assisted SQL Server Management Studio, demonstrating how mainstream relational systems are absorbing AI capabilities and accelerating Database Management System (DBMS) market growth.

Hyperscalers and database leaders are acquiring specialised vector and NoSQL providers to fortify generative AI stacks. The trend reflects an industry view that retrieval quality, embedding management, and unstructured data handling are now strategic differentiators. In February 2025, IBM announced its agreement to acquire DataStax, bringing AstraDB, DataStax Enterprise, and Langflow into watsonx.data. The deal positions IBM to compete more directly with MongoDB, Oracle, and AWS in AI-driven enterprise data platforms and signals continued consolidation around vector-ready engines.

Enterprises are increasingly demanding the ability to run their preferred database engines across multiple public clouds without re-architecting workloads. This drives investment in cross-cloud control planes, shared identity, and consistent operational tooling. In July 2025, Oracle and AWS launched Oracle Database@AWS into general availability, allowing Oracle Exadata Database Service and Autonomous AI Database to run inside AWS regions. The move underscores how hyperscalers are partnering rather than competing on every layer to capture mission-critical database workloads.

Database vendors are extending beyond storage and query engines into AI-powered application modernisation, helping customers refactor legacy schemas, generate APIs, and migrate to cloud-native architectures. The shift recognises that database choice is increasingly entangled with application strategy. In September 2025, MongoDB introduced MongoDB AMP, an AI-powered Application Modernisation Platform built on Atlas, designed to accelerate the migration of legacy relational and mainframe applications to a document-model architecture suitable for modern, AI-enabled workloads.

The Expert Market Research’s report titled “Global Database Management System (DBMS) Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

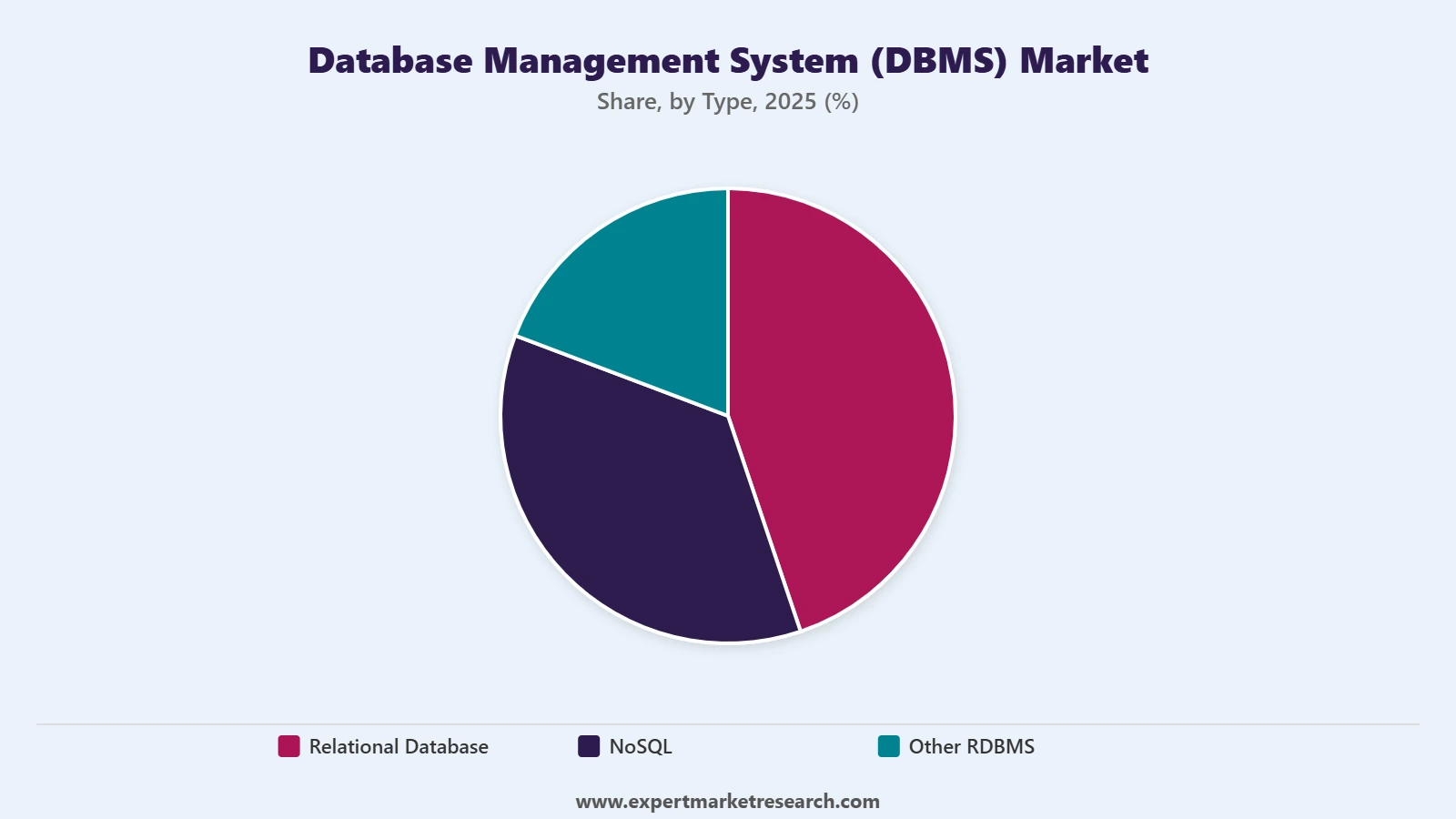

Market Breakup by Type

Key Insight: Relational databases continue to anchor the global DBMS market, accounting for the majority of revenue thanks to their pivotal role in BFSI, government, and ERP-driven environments where transactional integrity, schema discipline, and regulatory compliance are non-negotiable. Microsoft's release of SQL Server 2025 in November 2025 with built-in vector search, Oracle's continued investment in Autonomous AI Database, and PostgreSQL 17's enhanced JSON, partitioning, and incremental backup features are all extending the relevance of relational engines into AI workloads. NoSQL is the fastest-growing sub-segment as document, key-value, graph, and vector models gain traction for unstructured data and generative AI use cases.

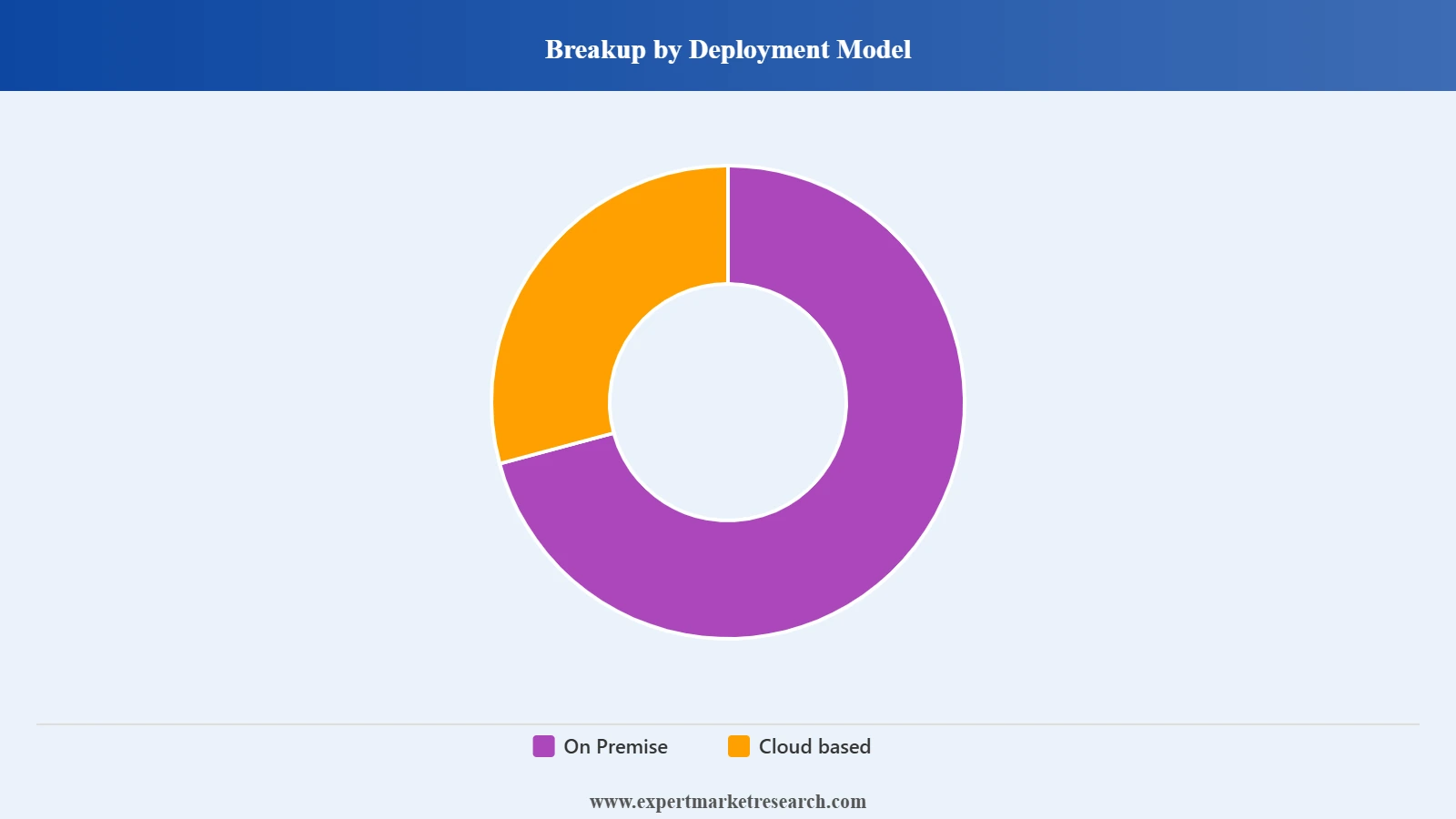

Market Breakup by Deployment Model

Key Insight: Cloud Based deployment is the fastest-growing sub-segment, propelled by managed database services such as Amazon Aurora, Azure SQL, Google Cloud Spanner, and MongoDB Atlas, which reduce operational overhead and align with enterprise AI strategies. Aurora DSQL's general availability in December 2025 illustrates how distributed SQL is consolidating cloud preference. On-premise deployment retains a meaningful share in regulated verticals and large enterprises with sovereign-data requirements, particularly in BFSI, defense, and healthcare. Oracle Database@AWS, launched in July 2025, exemplifies the rise of hybrid models that bridge on-premise governance with cloud elasticity.

Market Breakup by Organization size

Key Insight: Large Enterprises hold the largest share of the DBMS market because they manage the highest data volumes, run the most complex transactional systems, and operate stringent compliance regimes that require enterprise-grade licensing, support, and tooling. Most spend on Oracle Exadata, IBM Db2, Microsoft SQL Server, and SAP HANA flows from this segment. SMEs, however, are emerging as the faster-growing buyer cohort, propelled by consumption-based cloud pricing and free tiers from MongoDB, AWS, Microsoft, and PostgreSQL. MongoDB's expanded MongoDB for Startups program, refreshed in 2025, illustrates how vendors are courting smaller customers earlier in their lifecycle.

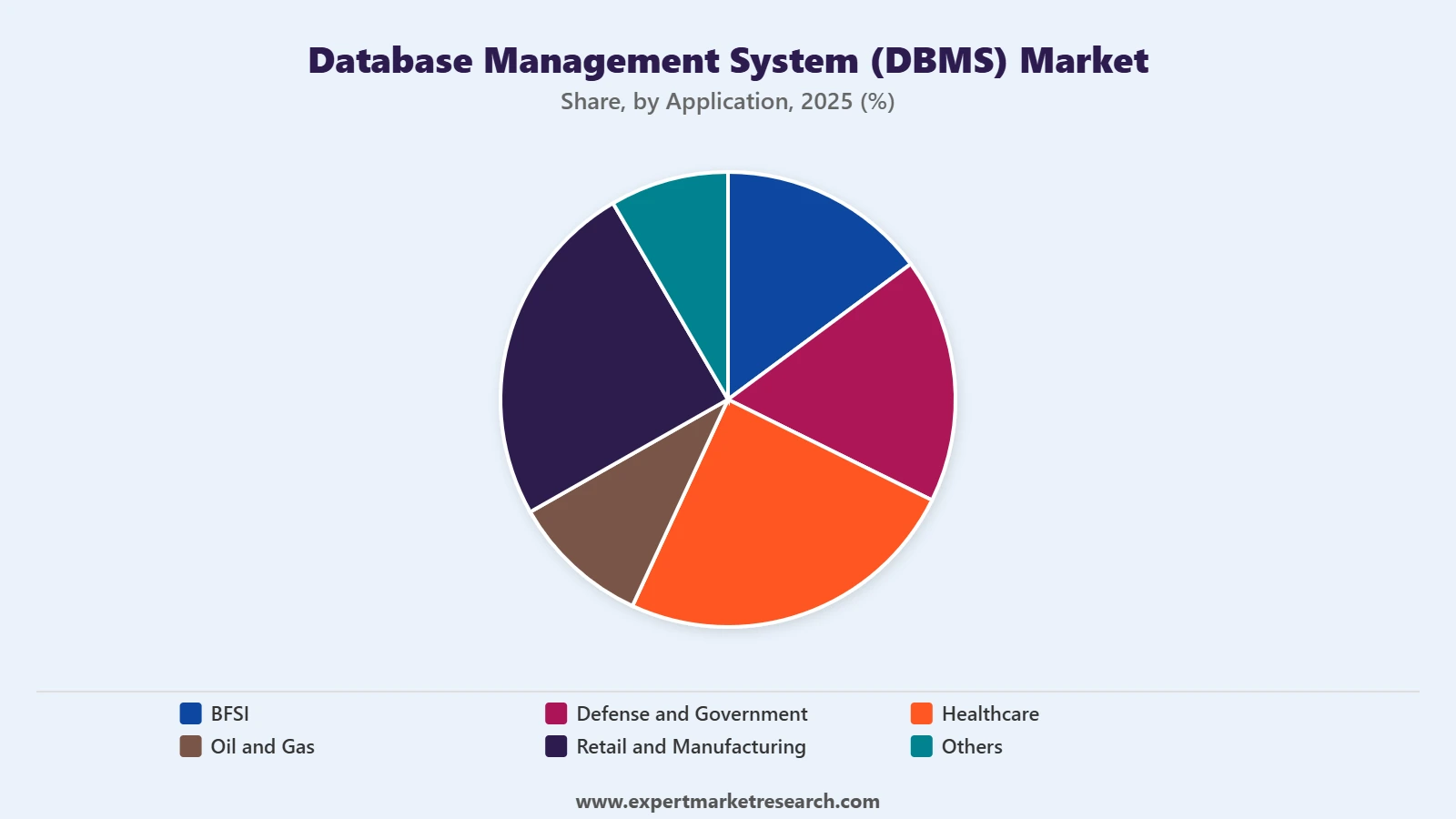

Market Breakup by Application

Key Insight: BFSI is the largest application segment, supported by stringent data integrity, fraud-detection, and regulatory needs that favour high-performance relational and increasingly vector-enabled engines. Healthcare and Defense and Government rank as fast-growing verticals as electronic health records, AI diagnostics, citizen-services platforms, and cyber-resilient data architectures expand. Retail and Manufacturing leverage DBMS to power omnichannel commerce, real-time inventory, and IIoT analytics. Oil and Gas adoption is driven by upstream analytics, asset performance management, and ESG reporting, where time-series and historian databases now interoperate with cloud-native platforms.

Market Breakup by Region

Key Insight: North America leads the global DBMS market, anchored by mature cloud infrastructure, the headquarters of leading vendors, and high spending on AI-driven data platforms by BFSI, healthcare, and government buyers. Asia Pacific is the fastest-growing region, driven by accelerating digitalisation in India, China, and ASEAN, public-cloud build-outs by AWS, Microsoft, Oracle, and Alibaba, and rising adoption among fintech and e-commerce firms. Europe shows steady growth shaped by GDPR-aligned sovereign-cloud initiatives. Latin America and the Middle East and Africa are smaller but expanding, supported by hyperscaler region launches in Mexico, Brazil, the United Arab Emirates, and South Africa.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Market by Type: Relational Database remains the dominant sub-segment, contributing the largest share of global DBMS revenue. The dominance reflects the historical embedding of relational engines such as Oracle Database, Microsoft SQL Server, IBM Db2, and PostgreSQL into mission-critical systems including core banking, ERP, and government registries. Continued investment, including PostgreSQL 17's improved vacuum, partitioning, and JSON capabilities and SQL Server 2025's vector and AI features, is helping relational engines defend share even as AI workloads expand. NoSQL leads in growth velocity, as document and vector engines such as MongoDB, Cassandra, and Elasticsearch capture new generative AI workloads, but relational systems retain their incumbency-driven majority.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Market by Deployment Model: Cloud Based deployment is the dominant share leader within new spending and the fastest growing sub-segment. Hyperscaler-managed databases including Amazon Aurora, Azure SQL Database, Google Cloud SQL, MongoDB Atlas, and Snowflake are absorbing migration budgets as enterprises retire on-premise hardware. AWS's general availability of Aurora DSQL in December 2025, alongside Oracle Database@AWS in July 2025, has reinforced cloud as the default deployment posture for new workloads. On-premise still commands meaningful spend in highly regulated verticals, but the trajectory of net-new licensing strongly favours cloud and hybrid environments across all major regions.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Market by Application: BFSI is the largest application sub-segment, given the sector's combination of high transaction volumes, stringent compliance requirements, and accelerating AI use cases such as fraud analytics, customer intelligence, and algorithmic credit scoring. Investments by JPMorgan Chase, HSBC, and major insurers in modernising data estates with Oracle Autonomous, IBM Db2, and Snowflake illustrate the segment's depth. Defense and Government rank as a fast-growing application thanks to sovereign-cloud rollouts and AI-driven citizen services. Healthcare adoption is rising as hospital systems standardise on cloud DBMS to support electronic health records, genomics workloads, and AI-assisted diagnostics that demand multi-model data handling.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

North America: North America commands the largest share of the global DBMS market, supported by the presence of category leaders such as Oracle, Microsoft, IBM, AWS, and MongoDB, dense data-centre infrastructure, and aggressive enterprise AI adoption. Strong demand from BFSI, healthcare, and federal government buyers, combined with new offerings like Aurora DSQL, Oracle Database@AWS, and SQL Server 2025, sustains spend. Recent investments include AWS's expansion of vector storage with S3 Vectors in December 2025 and Microsoft's continued build-out of Azure regions across the United States and Canada. Strict frameworks such as HIPAA, SOX, and emerging AI governance rules continue to favour mature, well-supported enterprise database platforms in this region.

Asia Pacific: Asia Pacific is the fastest-growing region in the DBMS market, driven by rapid digitalisation in India, China, Japan, and ASEAN, expanding fintech and e-commerce ecosystems, and large public-cloud investments by AWS, Microsoft Azure, Oracle, Alibaba Cloud, and Tencent Cloud. National digital programmes, smart-city initiatives, and rising adoption of AI in manufacturing are reinforcing demand for both relational and NoSQL engines. India's rapid growth in fintech, supported by UPI volumes, and China's ongoing localisation of cloud and database platforms are key demand drivers. Vendors are responding with regional partnerships, language-specific tooling, and investments in local data residency, positioning the region for sustained above-average growth through 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The global Database Management System market is moderately consolidated at the top, with a small group of vendors capturing the bulk of enterprise spend through deep integrations into ERP, analytics, and AI ecosystems. Oracle, Microsoft, IBM, and AWS dominate large-enterprise relational and cloud-native segments, while MongoDB, Elasticsearch, and Apache Cassandra-based providers lead in document, search, and vector workloads.

Competitive priorities now centre on AI readiness, multi-cloud portability, and developer experience. Vendors are differentiating through native vector search, retrieval-augmented generation tooling, application modernisation platforms, and consumption-based pricing models that lower the barrier to entry. Open-source-aligned communities such as PostgreSQL, MariaDB, and Apache Software Foundation continue to influence market direction, while strategic acquisitions and hyperscaler partnerships reshape the boundary between database, analytics, and AI.

Founded in 1977 and headquartered in Austin, Texas, Oracle Corporation is one of the largest enterprise software companies globally. Its database portfolio includes Oracle Database, Oracle Autonomous AI Database, MySQL HeatWave, and Oracle Exadata, deployed across on-premise, Oracle Cloud Infrastructure, and now AWS. Oracle's strengths lie in mission-critical workloads, tight ERP integration, and a strong installed base in BFSI and government.

Founded in 1975 and headquartered in Redmond, Washington, Microsoft is a leading provider of enterprise software and cloud services. Its DBMS offerings include SQL Server, Azure SQL Database, Azure Cosmos DB, Azure Database for PostgreSQL, and Microsoft Fabric. Microsoft has tightly integrated AI capabilities such as Copilot and vector search across its database portfolio and benefits from deep developer adoption, broad enterprise sales reach, and a global Azure footprint.

Founded in 1911 and headquartered in Armonk, New York, IBM Corporation provides hybrid cloud and AI platforms anchored by watsonx.data, Db2, Informix, and Cloud Pak for Data. IBM's DBMS strengths include strong positioning in regulated industries, decades of mainframe and enterprise data expertise, and an expanding generative AI portfolio. The 2025 acquisition of DataStax extends IBM's NoSQL and vector database capabilities for enterprise AI applications.

Founded in 2007 and headquartered in New York, MongoDB, Inc. is the developer of MongoDB, a document-oriented NoSQL database, and the MongoDB Atlas managed cloud service. The company has expanded into vector search, application modernisation through MongoDB AMP, and AI partnerships with more than forty vendors. MongoDB's strengths include developer-friendly tooling, flexible data models, and a strong position in cloud-native, AI-driven enterprise applications.

Other key players in the market are The PostgreSQL Global Development Group, Elasticsearch B.V., MariaDB Foundation, Amazon Web Services, Inc., Splunk Inc., The Apache Software Foundation, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Discover the latest insights on the Global Database Management System (DBMS) Market 2026 with our comprehensive report. Stay ahead of the curve with valuable data on AI-native database innovation, cloud migration patterns, and high-growth verticals. Whether you're modernising a legacy data estate, launching a new SaaS platform, or planning a strategic acquisition, this report gives you the clarity you need. Download your free sample now and discover the key opportunities in the thriving Global Database Management System (DBMS) industry.

Upto 15% Off

USD

$2999 $2699

$4839 $4355

$5999 $5099

$7259 $6170

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the database management system (DBMS) market reached an approximate value of USD 98.61 Billion.

The market is projected to grow at a CAGR of 10.80% between 2026 and 2035.

Key strategies driving the database management system (DBMS) market include cloud-first adoption for scalability, integration of AI and automation for advanced data insights, hybrid and multi-cloud deployment models, focus on security and compliance, expansion into emerging markets, and partnerships to deliver tailored industry-specific DBMS solutions.

The key trends in the market are the adoption of multi-model databases and cloud-based management systems and the rising integration of AI and machine learning in DBMS systems.

The major regions in the market are North America, Latin America, the Middle East and Africa, Europe, and the Asia Pacific.

The major applications of DBMS are BFSI, defence and government, healthcare, oil and gas, and retail and manufacturing, among others.

The different deployment models of DBMS are on premise and cloud based.

The key players in the market include Oracle Corporation, Microsoft Corporation, The Postgresql Global Development Group, MongoDB, Inc., Elasticsearch B.V, IBM Corporation, MariaDB Foundation, Amazon Web Services, Inc., Splunk Inc., and The Apache Software Foundation, among others.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach USD 274.99 Billion by 2035.

The key challenges found in the database management system (DBMS) market are managing growing data complexity, shortage of skilled professionals, and balancing performance with scalability in real-time, data-intensive applications.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Type |

|

| Breakup by Deployment Model |

|

| Breakup by Organization Size |

|

| Breakup by Application |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,999

USD 2,699

tax inclusive*

Single User License

One User

USD 4,839

USD 4,355

tax inclusive*

Five User License

Five User

USD 5,999

USD 5,099

tax inclusive*

Corporate License

Unlimited Users

USD 7,259

USD 6,170

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.