Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

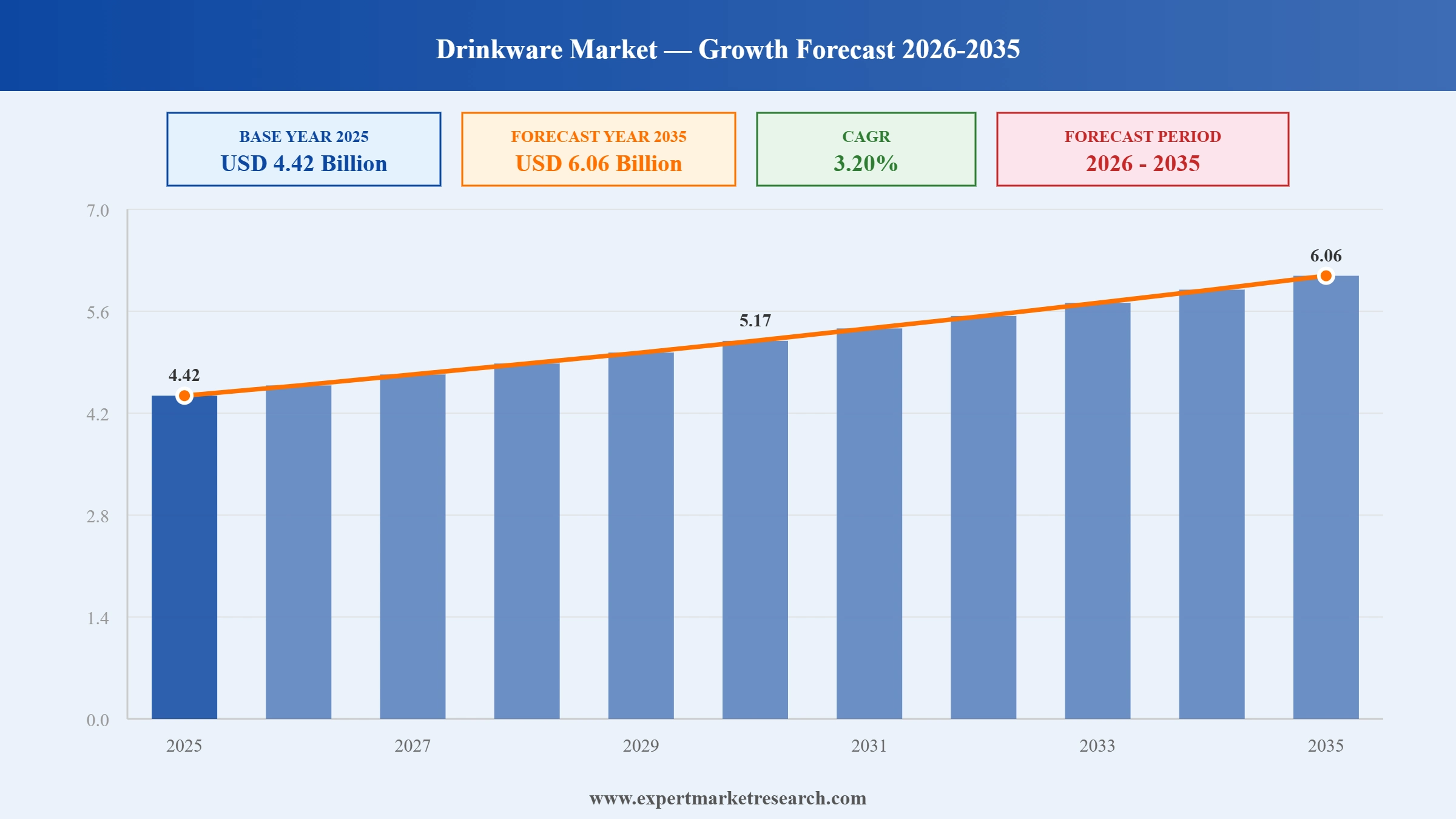

The Global Drinkware Market reached a value of USD 4.42 Billion at 2025 and is projected to expand at a CAGR of around 3.20% during the forecast period of 2026-2035. With sustained demand from the hospitality and foodservice sectors, accelerating premiumisation in stainless-steel insulated tumblers, sustainability-led shifts away from single-use plastics, and rising disposable incomes across Asia Pacific and Latin America, the market is expected to reach USD 6.06 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The Global Drinkware Market is being shaped by the ongoing premium stainless-steel insulated tumbler boom, sustainability-led decarbonisation of legacy glass furnaces, the regulatory push against single-use plastics, and continued consolidation among leading hospitality drinkware suppliers, with Asia Pacific anchoring both demand growth and manufacturing capacity additions.

Arc International SA, the world's largest tableware and drinkware manufacturer by daily output, underwent a major financial restructuring during 2024-2025 following a EUR 160 million loan from the French state's FDES (Fonds de Développement Économique et Social). Ownership now sits between private equity led by Peaked Hill Partners and significant state-backed financial influence, with the group continuing to manufacture around four million pieces per day from its Arques (France) base and delivering revenue of approximately EUR 688 million in 2024. The intervention preserved a strategically important French manufacturing base and underscored the capital intensity of large-scale glass tableware operations under European energy-cost pressure.

Steelite International, a global leader in hospitality tabletop solutions backed by Arbor Investments, announced the acquisition of Utopia Tableware Ltd, a Chesterfield, UK-based supplier of tableware, glassware, and accessories serving the hospitality and branded glass market. The deal extends Steelite's geographic footprint across the United Kingdom and continental Europe, adds a centralised distribution centre and decorating facility, and represents the seventh acquisition under Arbor's ownership since December 2019. The transaction strengthens Steelite's position in the global hospitality drinkware and tabletop value chain, complementing its 140-country network and 30,000-plus end-user locations.

Şişecam, the parent of the Paşabahçe drinkware brand, completed a USD 29 million cold repair of its second furnace at the Eskişehir Glassware Production Facility in Türkiye, lifting annual gross capacity to roughly 64,000 tonnes for the upgraded furnace and around 190,000 gross tonnes for the broader glassware site. The expansion, part of a wider USD 174 million Eskişehir investment programme, was paired with new packaging furnace activity to make Eskişehir what Şişecam describes as the world's largest single glass production complex, with combined glass-packaging and glassware capacity of approximately one million tonnes per year. The move reinforces Paşabahçe's cost position and export reach across Europe, the Middle East, and Asia.

Libbey Inc., the leading North American foodservice glassware producer, was selected to receive up to USD 45.1 million in funding from the US Department of Energy to support a five-year USD 90 million programme replacing four conventional regenerative glass-melting furnaces with two larger hybrid-electric units. The project, part of the DOE Industrial Demonstrations Program, is projected to cut up to 60% of the company's furnace-related carbon dioxide and other greenhouse-gas emissions, while improving glass quality and operating flexibility. The investment positions Libbey as one of the first US foodservice drinkware producers to materially decarbonise its melting base and aligns the company with tightening procurement standards from large hospitality and retail customers.

Bormioli Luigi S.p.A., the Parma-based premium glass tableware specialist, completed the merger of Bormioli Rocco S.p.A. into the parent group via merger deed dated 20 June 2023, with operational integration effective 1 July 2023. The combined entity unifies premium and mass-market drinkware lines across the Bormioli brand, supports a 10-year corporate Power Purchase Agreement with Axpo Italia for 30 GWh per year of renewable electricity, and has been investing in proprietary gas-and-electricity hybrid melting technology. The merger consolidates one of Italy's most recognised drinkware platforms and equips the combined group to compete more efficiently against Şişecam, Libbey, and Arc on both retail and hospitality channels.

The premium stainless-steel insulated tumbler category, led by Stanley (PMI Worldwide), YETI Holdings, and Owala, has transformed the drinkware mix between 2022 and 2025. Stanley grew from approximately USD 73 million in 2019 to over USD 800 million in 2024 on the back of its Quencher tumbler franchise, while YETI Drinkware delivered USD 1.09 billion in fiscal 2024 and returned to 6% growth in Q4 2025 after a category cooling earlier in the year. The category is supporting Global Drinkware Market growth by lifting average selling prices, encouraging brand collaborations and limited-edition drops, and pulling capital and shelf space toward stainless-steel formats and premium colourways at the expense of low-end disposable plastic.

Glass drinkware, the largest material segment, is being reshaped by capital investment in lower-carbon melting technology and renewable power. Libbey's USD 90 million hybrid-electric furnace programme (USD 45.1 million DOE-funded) targets a 60% cut in furnace CO2 emissions, Bormioli Luigi's 10-year 30 GWh/year corporate PPA with Axpo Italia anchors renewable-power supply, and Şişecam continues capacity additions in coated and standard glass with USD 114 million committed to three new coated-glass lines. The trend is supporting market growth by extending the competitive runway of glass against plastic and stainless-steel substitutes, while creating premium positioning opportunities for low-carbon drinkware in retail and corporate-gifting channels.

Regulatory pressure under the EU Single-Use Plastics Directive, which targets a 77% bottle collection rate by 2025 and 90% by 2029, alongside corporate sustainability commitments such as Starbucks' 2025 single-use plastic ban, are accelerating the structural shift to reusable drinkware in Europe and North America. The reusable water bottle market alone reached approximately USD 10.17 billion in 2025 and is forecast to grow to USD 15.27 billion by 2034 at a 4.62% CAGR. The trend supports Global Drinkware Market growth by structurally enlarging the reusable bottles, tumblers, and travel-mug categories, while encouraging stainless-steel and premium glass over single-use plastic in foodservice and on-premise channels.

The hospitality drinkware and tabletop channel continues to consolidate as private-equity-backed platforms scale through acquisition. Steelite International's June 2024 acquisition of Utopia Tableware Ltd represents the seventh acquisition under Arbor Investments' ownership and follows the January 2023 Steelite/Paşabahçe/Utopia joint venture for the US hospitality market. The Bormioli Luigi-Bormioli Rocco merger in June 2023 similarly consolidated Italian premium drinkware. The trend supports Global Drinkware Market growth by deepening multi-category platforms (glass, ceramic, accessories), improving distribution density across hotels, restaurants, and cruise lines, and creating scale to fund product innovation in patterns, branded glassware, and lightweight tableware.

“Drinkware Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

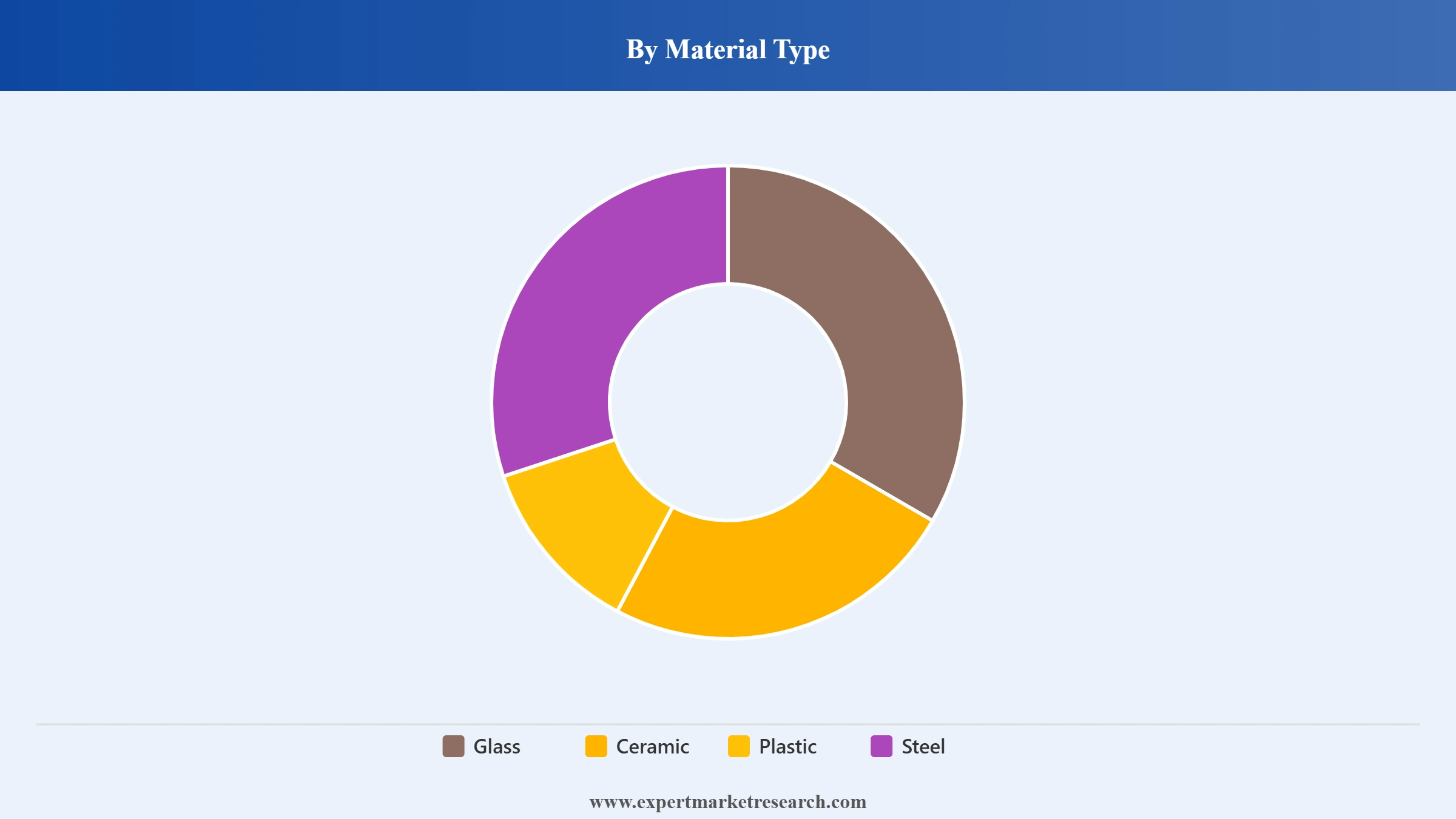

Market Breakup by Material Type

Key Insight: Glass is the dominant material category in the Global Drinkware Market, supported by its 100% recyclability, premium-look positioning across hospitality and on-premise foodservice, and continued capacity investments by Şişecam, Libbey, and the Bormioli group. Steel (predominantly stainless steel) is the fastest-growing category, with the insulated-tumbler boom led by Stanley, YETI, and Owala lifting average selling prices and shelf space across North America and Europe; YETI Drinkware alone generated USD 1.09 billion in revenue in fiscal 2024, while Stanley's brand revenue exceeded USD 800 million in 2024. Ceramic remains anchored in mug and on-premise hospitality usage, while plastic continues to serve price-sensitive and emerging-market demand under increasing regulatory and consumer pressure to shift toward reusable formats.

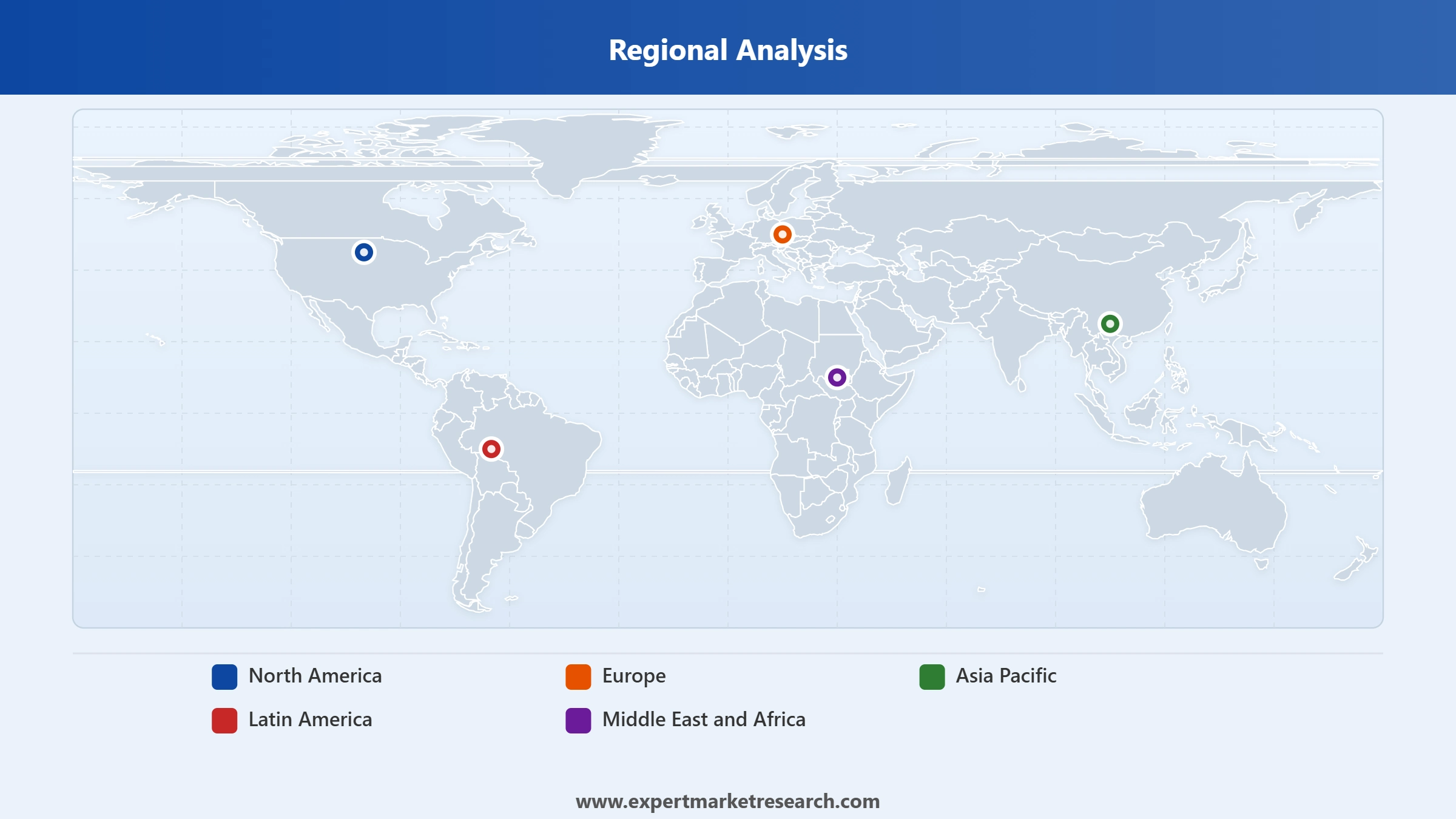

Market Breakup by Region

Key Insight: Asia Pacific commands the largest regional share of the Global Drinkware Market and is also the fastest-growing major region, anchored by China's combined role as the world's largest manufacturing hub and a rapidly modernising consumer market, plus structurally rising hydration and on-the-go consumption demand in India, ASEAN, and Australia. North America is the largest premium market, led by the United States and supported by the rapid scale-up of stainless-steel insulated tumbler brands and the foodservice glassware base operated by Libbey. Europe remains a stable, sustainability-led market underpinned by Şişecam's Türkiye and Hungary operations, the Bormioli group's Italian platform, Arc International's French manufacturing base, and the EU Single-Use Plastics Directive. Latin America and Middle East and Africa are growing on hospitality, tourism, and rising urban middle-class consumption.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Within the Material Type segmentation, Glass and Steel represent the most strategically important categories of demand and revenue. Glass anchors the largest share of the market thanks to its premium positioning, recyclability, and entrenched presence across hospitality, foodservice, and home dining; capacity additions and decarbonisation investments by Şişecam (Eskişehir), Libbey (US hybrid-electric furnaces), and the Bormioli group reinforce its long-run competitive runway. Steel, while smaller in absolute share, is the fastest-growing material on the back of stainless-steel insulated tumblers; YETI Drinkware revenue of USD 1.09 billion in fiscal 2024 and Stanley's brand revenue exceeding USD 800 million in 2024 illustrate how the steel sub-segment has reset average selling prices and growth expectations across the entire industry, drawing capital, retail shelf space, and brand investment toward premium reusable formats.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Within the Region segmentation, Asia Pacific and North America dominate demand and shape industry profitability. Asia Pacific is the largest regional market and is also the world's manufacturing hub, with China's Anhui Deli Household Glass Co. operating more than five production bases and 90 production lines, and Şişecam's Eskişehir glassware capacity expanding to roughly 190,000 gross tonnes per year. North America is anchored by the rapid scale-up of stainless-steel insulated drinkware led by Stanley, YETI, and Owala, alongside Libbey's foodservice glassware footprint. Europe, while slower-growing, remains pivotal for premium positioning and decarbonisation investment, with Bormioli Luigi's renewable-energy PPA and Arc International's restructuring shaping the region's supply economics.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Asia Pacific is the leading regional market in the Global Drinkware Market and is forecast to grow at the fastest pace through 2035, supported by China's role as both the largest manufacturing hub and a fast-modernising consumer market, India's rapidly expanding middle class, and rising on-the-go hydration and foodservice demand across ASEAN and Australia. Major Chinese producer Anhui Deli Household Glass Co. (Shenzhen-listed, 002571.SZ) ranked fourth globally by output and operates more than five production bases, 90 production lines, and 18 furnaces, supplying both the domestic market and global private-label customers. Şişecam's Eskişehir complex in Türkiye, while geographically straddling Asia and Europe, anchors export flows into Asia Pacific and the broader EMEA region following its USD 174 million capacity programme.

North America and Europe represent the two largest premium markets in the Global Drinkware Market. In North America, the stainless-steel insulated tumbler category led by Stanley, YETI, and Owala has reset average selling prices and lifted overall category growth, while Libbey's USD 90 million hybrid-electric furnace programme (USD 45.1 million DOE-funded) decarbonises the foodservice glassware base. In Europe, Bormioli Luigi's 2023 incorporation of Bormioli Rocco, Şişecam's continued Türkiye and Hungary capacity additions, and Arc International's 2024-2025 ownership restructuring with EUR 160 million state-backed support are shaping the region's supply economics. Latin America and Middle East and Africa are smaller but rising demand pools, supported by hospitality, tourism, and urban middle-class growth across Mexico, Brazil, the United Arab Emirates, and South Africa.

The Global Drinkware Market is moderately consolidated at the top end among integrated glass and tableware majors and is increasingly shaped by acquisitive private-equity-backed hospitality platforms and viral consumer brands. Producers compete on scale, design and brand strength, distribution density across hospitality and retail, sustainability credentials, and the ability to operate cost-efficient melting and decoration capacity. Integrated leaders such as Arc International, Libbey Inc., Paşabahçe (Şişecam Group), and Steelite International anchor global supply across glass, ceramic, and stainless-steel categories.

Mid-tier specialists including Anhui Deli Household Glass Co., Bormioli Rocco (Bormioli Luigi), and The Oneida Group (Anchor Hocking Holdings) compete on regional service, premium design, and category depth. Competitive priorities have shifted toward stainless-steel insulated formats, sustainability-led furnace upgrades, hospitality channel consolidation, and direct-to-consumer brand activation, particularly given the rapid scale-up of Stanley, YETI, and Owala in North America and the regulatory tailwinds from the EU Single-Use Plastics Directive.

Founded in 1825 and headquartered in Arques, France, Arc International is the world's largest tableware and drinkware manufacturer by daily output, producing approximately four million pieces per day for a 2024 turnover of around EUR 688 million. In 2024-2025, the group received a EUR 160 million loan from the French state's FDES and was restructured under private equity led by Peaked Hill Partners with significant state-backed influence, preserving the strategic Arques manufacturing base.

Founded in 1818 and headquartered in Toledo, Ohio, USA, Libbey Inc. is the leading North American foodservice glassware producer and a major supplier to the global retail and hospitality channels. In 2024, the company was selected to receive up to USD 45.1 million in US DOE funding toward a USD 90 million hybrid-electric glass-furnace programme projected to cut up to 60% of furnace-related greenhouse-gas emissions, complementing its lead-free, BPA-free Signature glassware family produced via the company's ClearFire glassmaking process.

Founded in 1935 and headquartered in Istanbul, Türkiye, Paşabahçe is the drinkware brand of Şişecam Group, one of the world's largest integrated glass producers. In 2024, Şişecam completed a USD 29 million cold repair of its second Eskişehir glassware furnace as part of a broader USD 174 million site investment programme, lifting glassware capacity at the world's largest single glass production complex and reinforcing the brand's export competitiveness across Europe, the Middle East, and Asia.

Founded in 1875 and headquartered in Stoke-on-Trent, United Kingdom (with US headquarters in Youngstown, Ohio), Steelite International is a leading global hospitality tabletop and drinkware supplier serving more than 30,000 end-user locations across 140 countries. In June 2024, Steelite acquired Utopia Tableware Ltd in its seventh acquisition under Arbor Investments' ownership, accelerating expansion across the United Kingdom and continental Europe and deepening its hospitality drinkware platform alongside the January 2023 Steelite/Paşabahçe/Utopia US joint venture.

Other key players in the market are Anhui Deli Household Glass Co., Ltd, Bormioli Rocco S.p.A. (Bormioli Luigi), The Oneida Group Inc. (Anchor Hocking Holdings), and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Discover the latest insights on the Global Drinkware Market 2026 with our comprehensive report. Stay ahead of the curve with valuable data on premium stainless-steel tumbler adoption, sustainability-led decarbonisation of glass production, EU regulatory tailwinds, and hospitality channel consolidation. Whether you are scaling a reusable bottle brand, expanding hospitality drinkware distribution, or modernising legacy glass-melting capacity, this report gives you the clarity you need. Download your free sample now and discover the key opportunities in the thriving Global Drinkware industry.

Upto 15% Off

USD

$3999 $3599

$2499 $2249

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the global drinkware market attained a value of nearly USD 4.42 Billion.

The market is projected to grow at a CAGR of 3.20% between 2026 and 2035.

The major drivers of the market include the growing demand for drinkware in the hospitality and foodservice sectors, a rise in the consumption of beverages, increasing demand for luxury products, and rising disposable incomes.

The availability of the product in a variety of designs and material types and the increasing number of pubs, restaurants, hotels, and home bars are expected to be the key trends guiding the growth of the market.

The major regions in the market are North America, Latin America, the Middle East and Africa, Europe, and the Asia Pacific.

Glass, ceramic, plastic, and steel are the major material types of drinkware in the global market.

The major players in the market are Arc Group, Anhui Deli Household Glass Co., Ltd, Libbey Inc., Pasabahce (Sisecam Group), Bormioli Rocco S.p.A., The Oneida Group Inc., and Steelite International Limited, among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Material Type |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

| Report Price and Purchase Option | Explore our purchase options that are best suited to your resources and industry needs. |

| Delivery Format | Delivered as an attached PDF and Excel through email, with an option of receiving an editable PPT, according to the purchase option. |

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.