Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

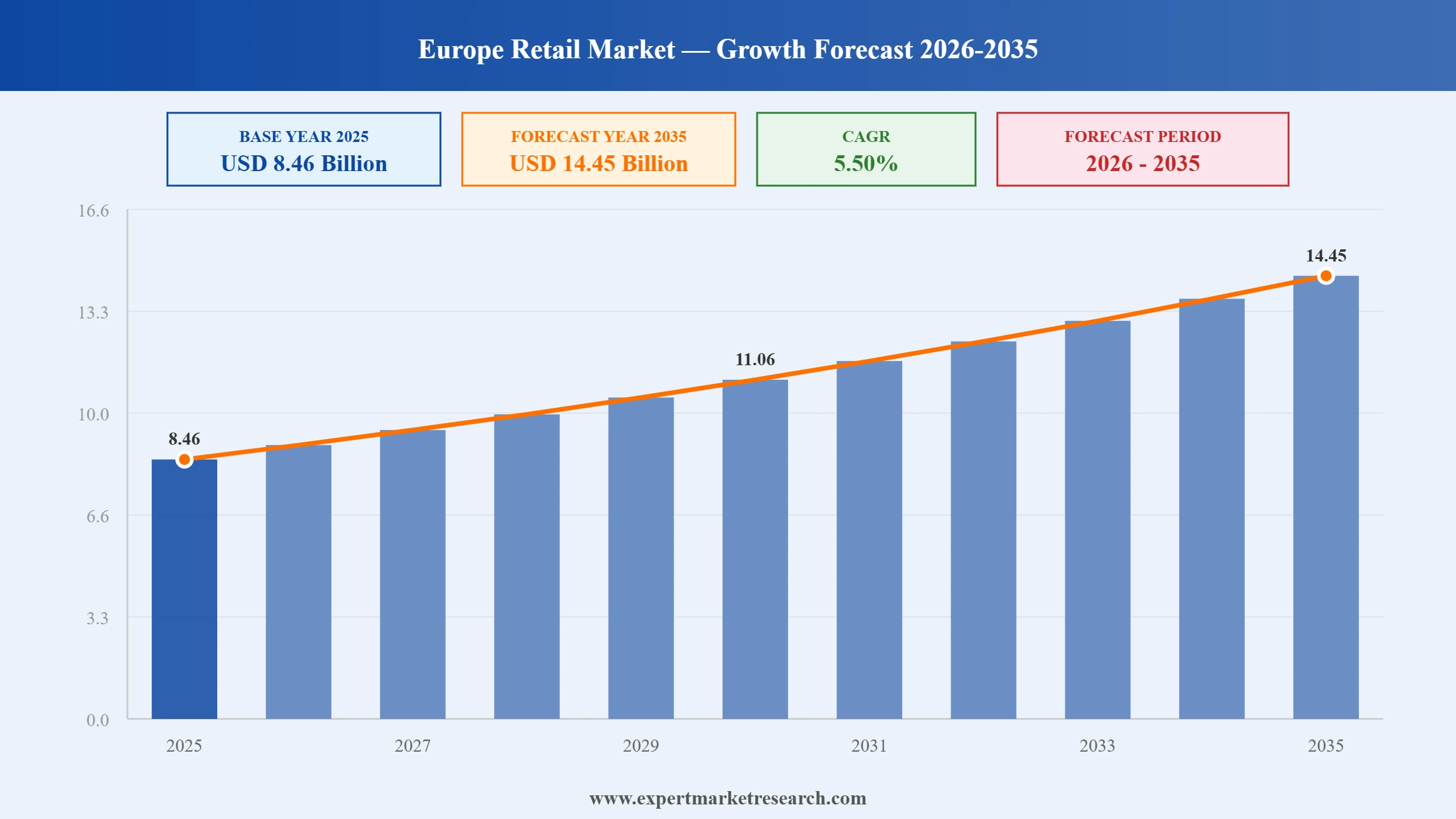

The Europe Retail Market reached a value of USD 8.46 Billion at 2025 and is projected to expand at a CAGR of around 5.50% during the forecast period of 2026-2035. With sustained consumer spending recovery, rapid e-commerce growth, increasing adoption of omnichannel retail strategies, growing demand for sustainable products, and significant retailer investment in AI-driven analytics and fulfilment automation, the market is expected to reach USD 14.45 Billion by 2035.

According to the European Commission, flash consumer confidence in the EU and euro area fell again in April 2026 as energy price volatility weakened household sentiment. The update is relevant to the Europe retail market because softer consumer confidence can affect discretionary spending, promotional intensity, and inventory planning across apparel, grocery, and general merchandise retail channels.

According to Eurostat, retail trade volume in January 2026 slipped by 0.1% in the euro area while remaining only marginally positive across the EU. Published in March 2026, the data points to a cautious retail environment. This matters for the Europe retail market because weaker volume growth can pressure store traffic, pricing strategies, and short-term expansion decisions.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

| Europe Retail Market Report Summary | Description | Value |

| Base Year | USD Billion | 2025 |

| Historical Period | USD Billion | 2019-2025 |

| Forecast Period | USD Billion | 2026-2035 |

| Market Size 2025 | USD Billion | 8.46 |

| Market Size 2035 | USD Billion | 14.45 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 5.50% |

| CAGR 2026-2035 - Market by Country | Germany | 6.1% |

| CAGR 2026-2035 - Market by Country | United Kingdom | 5.9% |

| CAGR 2026-2035 - Market by Product Type | Food, Beverage, and Grocery | 6.3% |

| CAGR 2026-2035 - Market by Distribution Channel | Online | 9.4% |

| 2025 Market Share by Country | Germany | 10.1% |

The European retail market is undergoing a structural transformation shaped by the accelerating rise of e-commerce, consumer-led demands for sustainable retail practices, retailer investment in AI and logistics technology, and the growing strength of private label brands as cost-conscious consumers respond to inflationary pressures.

In September 2025, Schwarz Group introduced a new line of plant-based private label products under both its Lidl and Kaufland banners across multiple European markets. The launch reflects the group's strategic commitment to expanding its sustainable and alternative food offerings in response to rising consumer demand for plant-based and environmentally conscious food products. Lidl's private label food range has long been a competitive weapon against both premium supermarket brands and discount rivals, and the plant-based extension reinforces the group's positioning as an affordable destination for sustainability-conscious European shoppers who are unwilling to pay premium prices for eco-friendly alternatives.

In July 2025, Zalando SE expanded its same-day delivery capabilities by acquiring a minority stake in a Germany-based last-mile delivery startup, reinforcing its position as one of Europe's leading fashion e-commerce platforms. The investment is intended to reduce Zalando's reliance on third-party logistics providers for time-sensitive urban deliveries and improve its ability to fulfil orders within hours in key metropolitan markets. Last-mile delivery has become a critical battleground among European e-commerce retailers, with same-day and next-day service increasingly cited as a primary purchase driver by consumers in Germany, France, the Netherlands, and the UK.

In May 2025, Carrefour Group partnered with a leading logistics technology firm to implement AI-driven warehouse automation solutions across its distribution centres in France and Spain. The deployment is designed to enhance picking efficiency, reduce order fulfilment times, and lower operational costs in Carrefour's grocery and general merchandise supply chain. The initiative is part of Carrefour's broader omnichannel transformation strategy, which aims to strengthen its click-and-collect and home delivery capabilities. AI-driven fulfilment automation is becoming a key competitive differentiator among large European food retailers as they compete with pure-play e-commerce platforms on delivery speed and product availability.

In February 2025, H&M announced the rollout of a new rental fashion service across select European markets, targeting the growing consumer appetite for sustainable consumption and circular retail models. The service allows customers to rent curated clothing items rather than purchase them outright, directly addressing concerns about fast fashion's environmental footprint. H&M's move into fashion rental signals a structural shift in how major European apparel retailers are responding to regulatory pressure and consumer demand for more sustainable retail practices, and it positions the company to capture a younger demographic increasingly drawn to access-over-ownership consumption models.

In 2024, online retail sales in Europe accelerated across all major markets, with e-commerce expected to account for approximately 15% of total retail sales by 2029, up from 16.1% of all retail in 2021, according to European industry data. Germany maintained the highest e-commerce penetration at around 80% of internet users shopping online, while France and the UK saw sustained growth in cross-border and mobile-driven purchases. Eurostat recorded a 5.6% year-on-year increase in EU retail trade turnover in late 2023, driven largely by non-food categories including electronics and furniture, reflecting broader consumer spending momentum that carried into 2024.

Online channels are projected to account for 66% of total projected retail sales growth in the UK and 68% in continental Europe between 2025 and 2029, fundamentally redefining how European consumers engage with retail brands. Retailers are responding with aggressive omnichannel investments, integrating click-and-collect, same-day delivery, and seamless returns across physical and digital channels. In July 2025, Zalando's acquisition of a stake in a German last-mile startup illustrates the strategic priority that leading e-commerce players are placing on delivery speed and fulfilment capability as the primary determinants of competitive advantage in European online retail growth.

European consumers are increasingly incorporating sustainability criteria into their purchasing decisions, and major retailers are responding with structural changes to their business models. Over 62% of European consumers report preferring brands that demonstrate environmental responsibility, according to Deloitte. H&M's launch of a rental fashion service in February 2025 and Schwarz Group's plant-based private label expansion in September 2025 exemplify how large retail chains are embedding circular economy principles into product strategy. Regulatory frameworks such as the EU's extended producer responsibility directives and Green Deal initiatives are expected to further accelerate sustainable retail adoption through the forecast period.

Retailer investment in AI-driven analytics and warehouse automation is accelerating across Europe, as companies seek to reduce operational costs, improve inventory accuracy, and shorten fulfilment cycles. Carrefour's May 2025 partnership for AI warehouse automation in France and Spain illustrates the scale of investment that major grocery retailers are committing to supply chain modernisation. According to industry data, approximately 57% of retail investments between 2023 and 2025 focused on digital transformation, with 49% targeting warehouse automation and robotics. These investments are expected to compress operating margins in the near term but create durable competitive advantages in speed, scale, and product availability that will define market leadership through the forecast period.

Private label products are capturing an increasing share of European grocery retail baskets as cost-conscious consumers seek value alternatives to branded goods. Discount retailers led by the Schwarz Group through Lidl and Kaufland, ALDI, and CONAD have all invested significantly in expanding and upgrading their private label ranges. The food, beverage, and grocery segment commands approximately 37.3% of the European retail market by product type, and within this segment, private label penetration continues to grow at the expense of branded alternatives. Supermarkets and hypermarkets, which hold a 43.2% distribution channel share, are the primary beneficiaries of this trend as they offer the widest private label assortments and benefit from the operational scale to price them competitively.

The increasing use of e-commerce platforms, driven by improvements in digital technology, is reshaping the retail landscape in Europe. The shift to online shopping, accelerated by the COVID-19 pandemic, continues to promote Europe retail market growth.

The Expert Market Research's report titled “Europe Retail Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

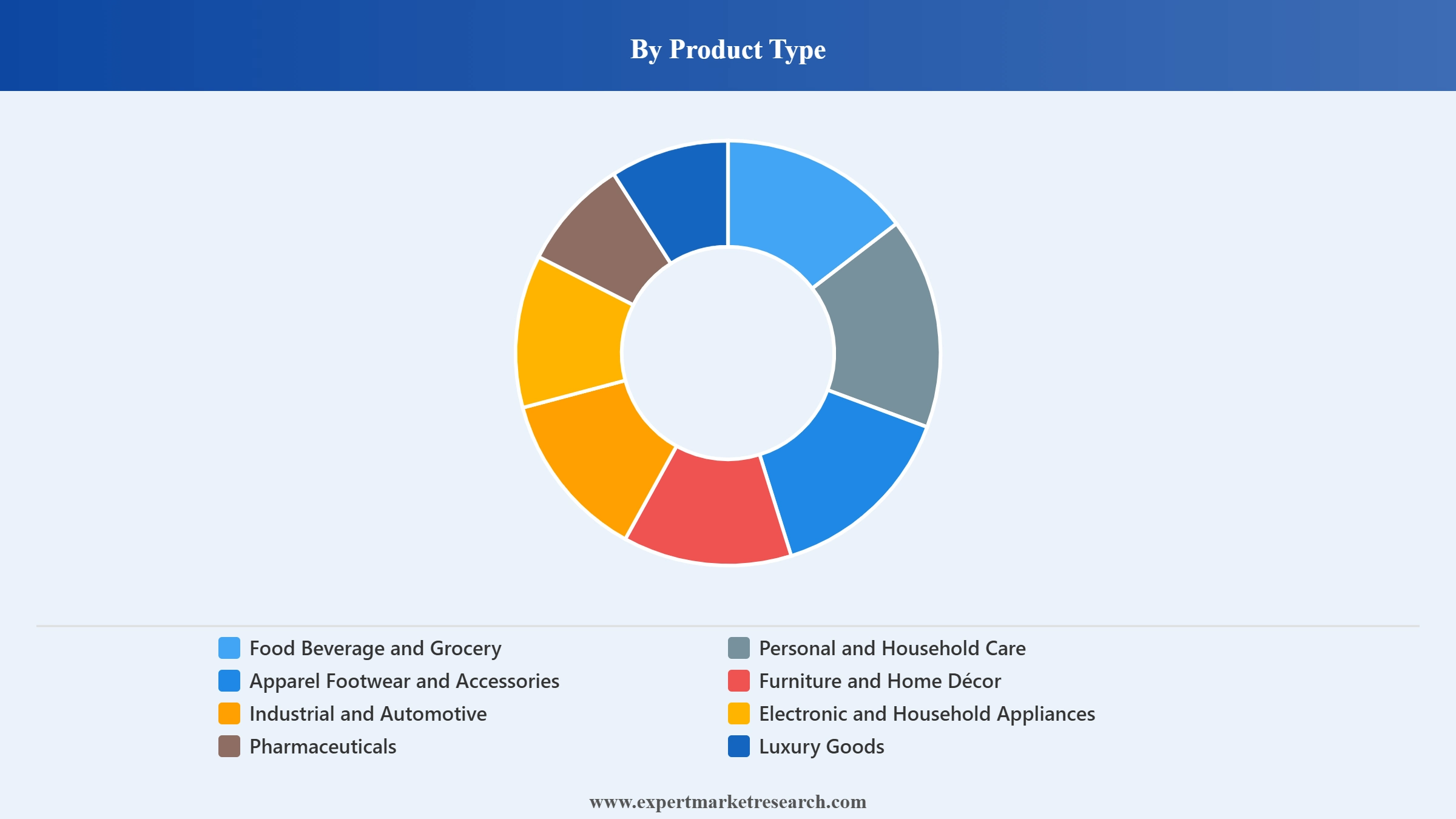

Market Breakup by Product Type

Key Insight: Food, Beverage, and Grocery is the dominant product type segment, accounting for approximately 37.3% of the European retail market in 2025, supported by the essential nature of grocery purchases and their resilience across economic cycles. The segment is growing at a CAGR of approximately 6.3%, fuelled by expansion in discount supermarket formats, growth of private label offerings, and increasing adoption of click-and-collect and home delivery grocery services. The Pharmaceuticals segment is the fastest-growing category at approximately 8.6% CAGR, driven by an ageing European population, rising chronic disease prevalence, and the expansion of online pharmacy platforms. Luxury Goods and Apparel are experiencing varying performance, with premium segment resilience contrasting with broader apparel challenges in a cost-conscious consumer environment.

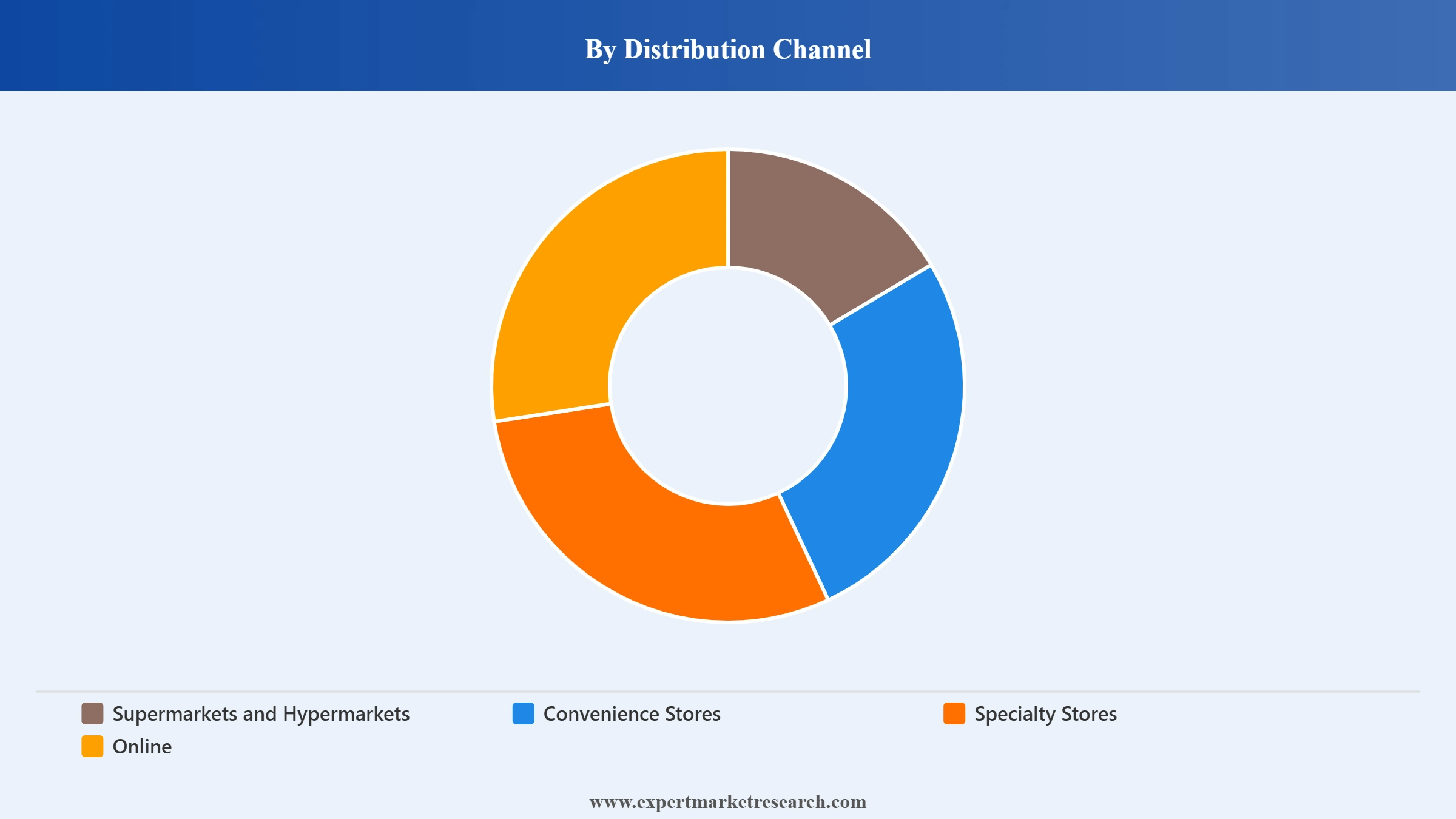

Market Breakup by Distribution Channels

Key Insight: Supermarkets and hypermarkets command the largest distribution channel share at approximately 43.2% of the European retail market, sustained by their ability to offer comprehensive one-stop shopping experiences, competitive pricing, and increasingly sophisticated omnichannel integration including click-and-collect and home delivery. Approximately 72% of European urban households visit hypermarkets or supermarkets at least once a week. The Online channel is the fastest-growing distribution format at approximately 11.2% CAGR, driven by mobile commerce growth, platform ecosystem expansion by major players including Amazon and Zalando, and the growing consumer expectation for next-day or same-day fulfilment. E-commerce is expected to account for 15% of total European retail sales by 2029.

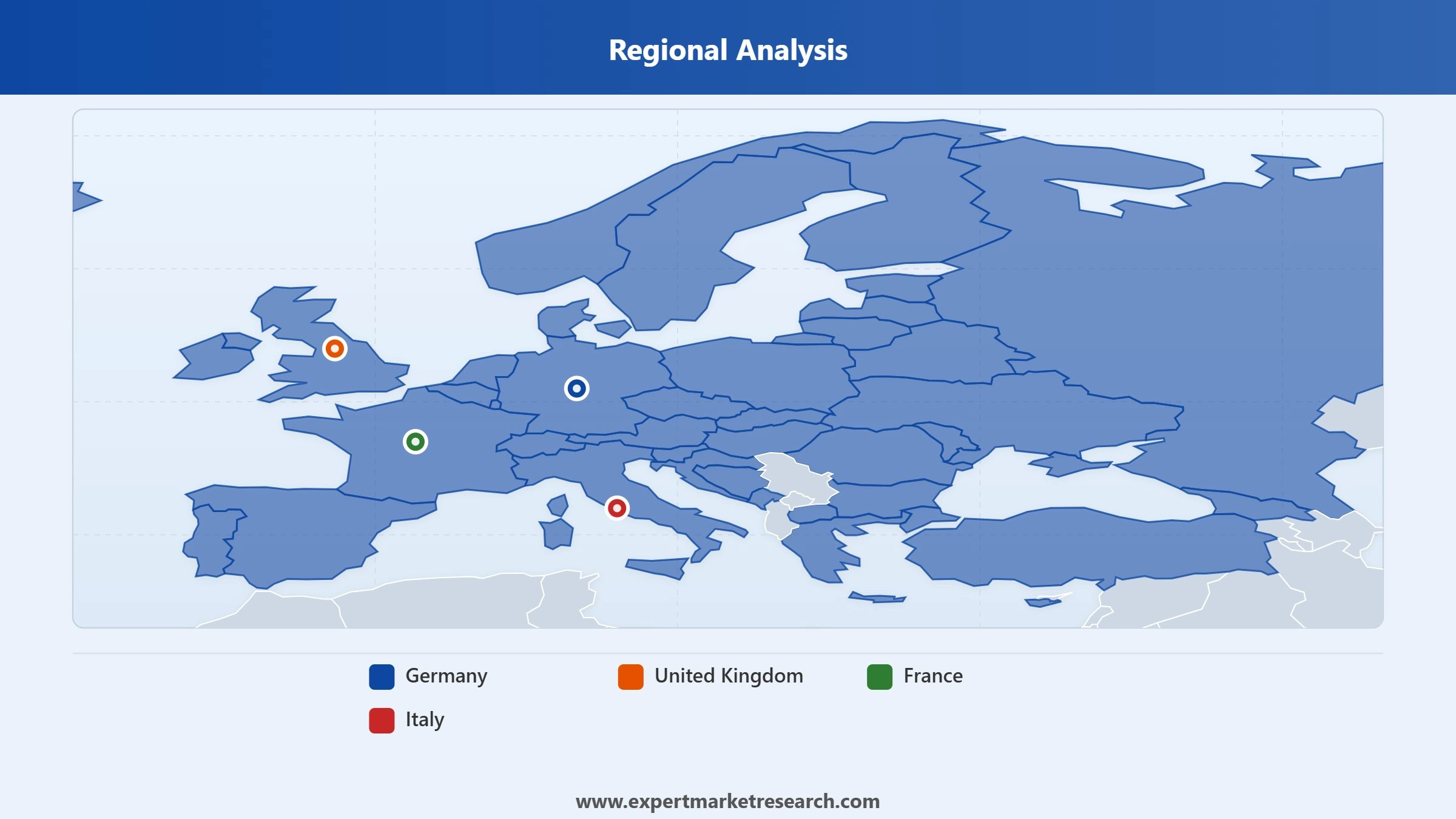

Market Breakup by Country

Key Insight: Germany is the largest European retail market and is expected to sustain its leadership through the forecast period, driven by the continent's highest e-commerce penetration at approximately 80% of internet users and strong performance in electronics and clothing retail categories. The UK is Europe's second-largest clothing market and leads in watch, jewellery, print media, and sports equipment sales. France is anticipated to experience the highest prime retail rental growth, reflecting the strength of its domestic consumer market and premium retail ecosystem. Italy's retail market has shown recovery momentum, particularly in luxury goods and food retail, supported by growing tourism and domestic consumption. The broader 'Others' category includes high-growth Eastern European markets led by Poland, Romania, and Bulgaria.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Product Type

Food, Beverage, and Grocery holds the commanding share of the European retail market by product type at approximately 37.3%, benefiting from the essential nature of grocery purchases and the continued strength of in-store shopping among older demographic segments. Electronic and Household Appliances is the second-largest non-grocery product type, with Germany commanding a dominant position in this category driven by strong online demand and a well-developed e-commerce infrastructure. The Pharmaceuticals segment is gaining share rapidly, with the expansion of online pharmacy platforms including Amazon Pharmacy into select European markets contributing to broadening distribution and increasing consumer access.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Distribution Channel

Supermarkets and hypermarkets retain the largest share of the European retail distribution landscape, serving as the primary shopping destination for the majority of European households across all major markets. Their competitive advantage lies in the scale of product assortment, competitive pricing through private label, and the ability to integrate digital ordering and click-and-collect capabilities into their existing store networks. Online retail is the clear growth driver, with pure-play e-commerce operators including Amazon, Zalando, and Vinted competing alongside the digital arms of traditional brick-and-mortar retailers. Mobile commerce and social commerce channels are increasingly significant, particularly among younger European consumers in Germany, France, and the UK.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Germany

Germany is the anchor of the European retail market, maintaining its leadership through a combination of high consumer spending, the continent's most advanced e-commerce ecosystem, and a strong domestic manufacturing and distribution infrastructure. Germany's e-commerce penetration stands at approximately 80% of internet users, the third-highest globally, and the country commands the largest share of the European electronics retail market. In 2024, Eurostat data showed a 5.6% year-on-year increase in EU retail trade turnover driven significantly by Germany's non-food sectors. Retail prime rents in Germany's key high streets are stabilising and projected to recover modestly through the forecast period, supported by recovering consumer confidence and sustained e-commerce investment.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

United Kingdom

The United Kingdom is Europe's most advanced omnichannel retail market, with online sales expected to account for 66% of projected total UK retail growth between 2025 and 2029. Major UK retailers including Tesco, Marks and Spencer, and Next are investing heavily in digital infrastructure, same-day delivery capabilities, and loyalty program personalisation. In-store retail sales in the UK declined by approximately 6% relative to pre-pandemic 2019 levels by 2025, creating pressure on traditional retail formats and accelerating the closure of underperforming stores. However, prime high street and shopping centre locations are demonstrating resilience, and the UK leads Europe in specialty retail categories including watches, jewellery, and sports equipment.

The European retail market features a highly competitive landscape dominated by large multinational supermarket groups, specialty retailers, and a rapidly growing e-commerce platform ecosystem. Traditional brick-and-mortar retailers are competing intensively with digital-native platforms, prompting substantial investment in omnichannel integration, private label expansion, and supply chain modernisation.

The Schwarz Group, operating Lidl and Kaufland, is the largest European food retailer by revenue, competing on aggressive pricing and private label quality. Carrefour and Tesco anchor the traditional hypermarket segment in France and the UK respectively. Zalando dominates fashion e-commerce, while Amazon commands growing share across categories through its Prime fulfilment ecosystem.

Founded in 1958 and headquartered in Massy, France, Carrefour Group is one of Europe's largest and most globally established retailers, operating hypermarkets, supermarkets, convenience stores, and e-commerce platforms across multiple European countries including France, Spain, Belgium, Italy, and Poland. The company generates revenues exceeding EUR 90 billion annually. In May 2025, Carrefour partnered with a logistics technology firm to deploy AI-driven warehouse automation across its French and Spanish distribution network. Carrefour's strategy focuses on price leadership, private label expansion, and accelerating omnichannel integration through digital ordering, click-and-collect, and same-day delivery.

Founded in 1919 and headquartered in Welwyn Garden City, United Kingdom, Tesco plc is the UK's largest supermarket chain and one of Europe's most recognised retail brands. The company operates thousands of stores across the UK, Ireland, and Central Europe under the Tesco banner. Tesco's Clubcard loyalty program is one of the UK's most widely used retail loyalty schemes, providing the company with extensive consumer data that it leverages for personalisation, targeted promotions, and supplier negotiations. Tesco's omnichannel operations include a major online grocery delivery business and the Tesco Whoosh rapid delivery service, reflecting the company's commitment to meeting evolving consumer expectations for convenience.

Founded in 2008 and headquartered in Berlin, Germany, Zalando SE is Europe's leading online fashion and lifestyle platform, serving customers across more than 25 European markets. The company offers an extensive assortment of clothing, footwear, accessories, and beauty products from thousands of international and local brands. In July 2025, Zalando acquired a minority stake in a last-mile delivery startup to strengthen its same-day delivery capabilities in key urban markets. Zalando's partner program enables third-party brands to manage their own fulfilment directly from the Zalando platform, significantly expanding its product catalogue while sharing logistics investments with brand partners.

Schwarz Group, the parent organisation operating both Lidl and Kaufland banners, is the world's largest retailer by revenue after Walmart and Amazon, headquartered in Neckarsulm, Germany. The group operates thousands of Lidl discount stores across Europe and a network of Kaufland hypermarkets in Germany, Central and Eastern Europe. In September 2025, Schwarz Group launched a new plant-based private label range across both banners, reinforcing its strategy of delivering sustainability-oriented products at competitive price points. The group's scale and supply chain efficiency enable it to consistently undercut rivals on price while maintaining acceptable quality standards, making it the dominant force in European discount grocery retail.

Other key players in the market are CONAD, Unieuro SPA, Amazon.com, Inc., Euronics International, Coop, Esselunga SpA, Auchan Retail International, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

European retail is at a pivotal intersection of digital transformation, sustainability imperatives, and consumer behaviour change. Our comprehensive Europe Retail Market report for 2026 provides the granular analysis you need to stay ahead, covering e-commerce growth dynamics, country-specific demand trends, category performance forecasts, and competitive strategies across the continent's leading retail players. Whether you are a retailer planning your omnichannel roadmap, a brand evaluating distribution strategy, or an investor assessing opportunities in European consumer markets, this report delivers the data-driven clarity you need. Download your free sample today.

European Retail Supply Chain Trends

Europe Retail Infrastructure Development

Europe Omnichannel Retail Adoption

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market attained a value of nearly USD 8.46 Billion.

The market is assessed to grow at a CAGR of 5.50% between 2026 and 2035.

The market is estimated to reach around USD 14.45 Billion by 2035.

The market is being driven by the growth of the e-commerce sector and evolving consumer preferences in the region.

The key trends aiding the market expansion include the rise in cross-border shopping and technological advancements.

The major distribution channels in the market are hypermarket and supermarket, convenience stores, specialty stores, and online, among others.

The major countries considered in the market are the United Kingdom, Germany, France, and Italy, among others.

The major players in the market are CONAD, Unieuro SPA, Amazon.com, Inc., Euronics International, Schwarz Unternehmenskommunikation GmbH & Co. KG, Zalando SE, Tesco plc, Coop, Carrefour Group, Esselunga SpA, and Auchan Retail International, among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Product Type |

|

| Breakup by Distribution Channel |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.