Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

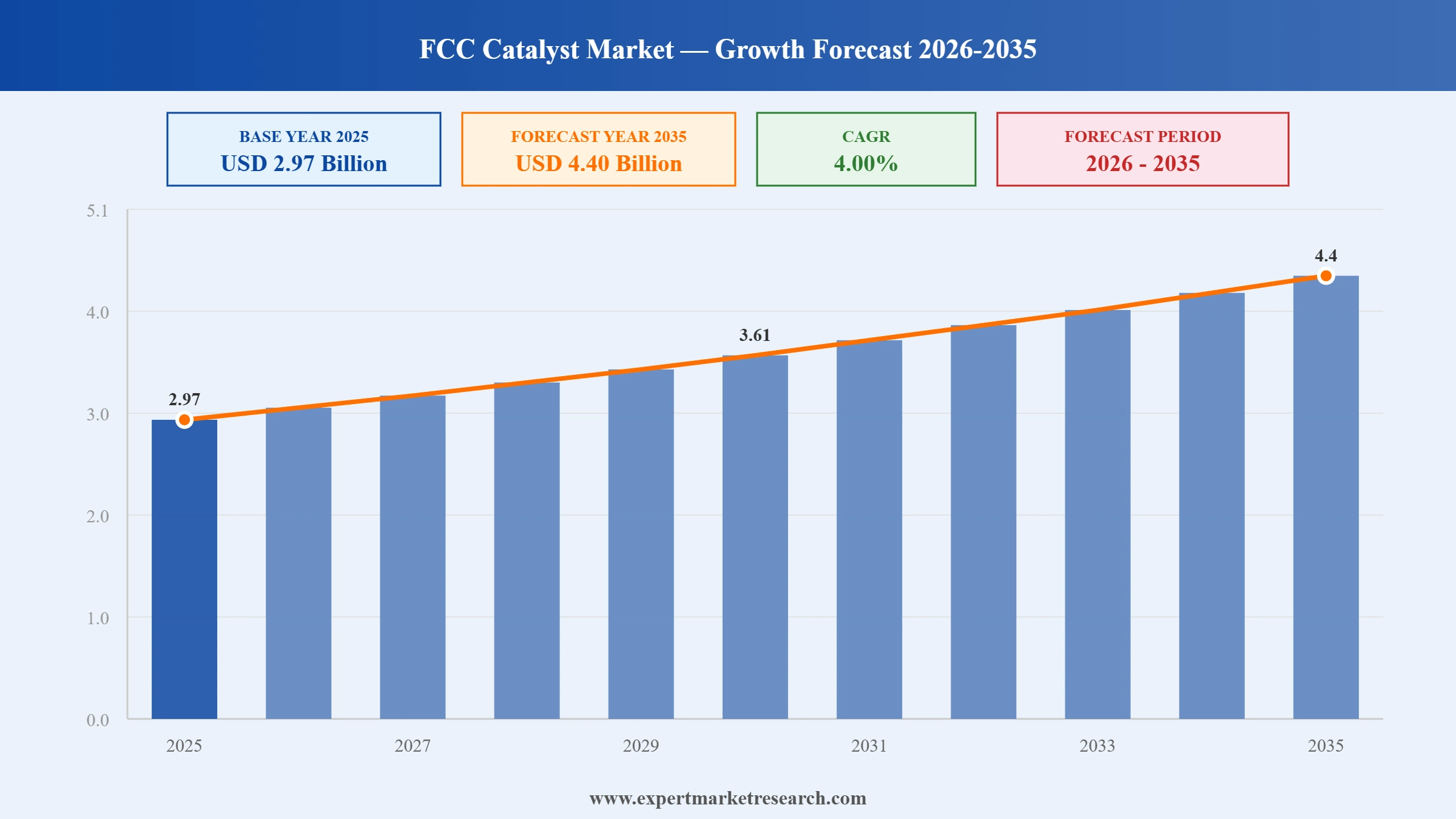

The global FCC catalyst market was valued at USD 2.97 Billion in 2025. The market is expected to grow at a CAGR of 4.00% during the forecast period of 2026-2035 to reach a value of USD 4.40 Billion by 2035. Technological collaboration between catalyst manufacturers and refinery operators is supporting innovation and performance improvements in the market.

An industry capacity outlook released on 7 April 2026 highlighted that several large-scale greenfield and expansion fluid catalytic cracking projects are set to come online between 2026 and 2030, particularly in Asia, the Middle East and Africa, driven by export-oriented refining demand. The findings, summarised in Hydrocarbon Engineering, point to renewed catalyst replacement demand after a flat 2020–2025 cycle.

In a technical case study published in the March 2026 issue of Hydrocarbon Processing, BASF and Marathon Petroleum reported that next-generation FCC catalysts unlocked an incremental USD 1.40 per barrel in profitability through higher butylene selectivity and stronger alkylate yields. The findings underscore the continued value of advanced zeolite catalyst chemistry in maximising premium gasoline output.

Ongoing efforts toward refinery optimization and the necessity for improved product yield efficiencies represent two significant factors driving the FCC catalyst market growth. The increased application of innovative catalyst formulations helps achieve greater conversion efficiencies of heavy feedstock, such as vacuum gas oil, while increasing the yields of gasoline and propylene products. In addition, the growing regulatory pressure for cleaner transportation fuels the need for catalysts able to help lower the sulfur content in fuels. The continuous innovations and technological developments in the refining process are thus accelerating demand in the market.

Additionally, considering the growing requirements for refinery efficiency, increased yield production, and environmentally safer fuels, catalyst manufacturers are increasingly collaborating with energy producers to jointly develop new catalyst systems. These partnerships enable incorporating experience from refinery operations into catalyst development processes and developing more customized catalyst systems that ensure higher efficiency in producing gasoline and propylene products. Through such initiatives, the R&D efforts within the global FCC catalyst market are expected to intensify, helping refiners introduce more efficient catalyst solutions.

An example of the above trend was seen in March 2026 when Ketjen Corporation and SATC signed an agreement on joint development in which the two companies would collaborate to develop, test, and implement advanced FCC catalysts and additives for improving refinery efficiency, yields in the production of valuable products, including gasoline and propylene, and reducing their environmental impact.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Ketjen developed a new type of catalyst technology that can be used to solve iron poisoning issues in the refineries and improve their efficiency. The innovation improves heavy crude processing and helps catalyst manufacturers develop high-end catalysts.

Johnson Matthey established new facilities to develop FCC catalyst additives at its Savannah site. Such innovations encourage FCC catalyst market players to conduct research and development activities related to advanced catalyst technologies.

BASF established a new Catalyst Development and Solids Processing Center at Ludwigshafen, Germany, for synthesizing pilot-scale catalysts to enable quick commercialization. The move propels the company’s capability in catalyst research and promotes other companies to build up their facilities to improve refinery efficiencies.

BASF developed the Fourtiva catalyst, which can boost yields of butylene and enhance gasoline blending performance. This move promotes technological development in the FCC catalyst market and encourages other companies to develop high-efficiency catalysts.

The use of analytics and AI is increasingly becoming common among refineries, whereby they help to monitor catalysts, optimize feedstock processes, and increase operational efficiency through fluid catalytic cracking. This makes it possible for refineries to make changes in operating parameters in order to extend the life of catalysts while, at the same time, improving the yield of their products. As a result, companies are seeking digital solutions that support the functioning of their catalyst technologies, which, in turn, influence the FCC catalyst market trends and dynamics. One notable example is Ketjen's introduction of real-time refinery catalyst intelligence in partnership with Imubit in May 2026.

Strategic collaborative partnerships between catalyst developers and technology licensors are becoming more important in influencing innovations in refining technologies. Such collaborative partnerships help leverage expertise in catalyst manufacturing and process technology, improving overall conversion efficiency and selectivity in FCC processes. Collaborative partnerships thus help in the quicker introduction of innovative catalyst technologies in addition to enabling refineries to refine higher-boiling feedstock materials, propelling the growth of the FCC catalyst market. An example of this industry trend was seen in October 2025, when Ketjen and Axens signed new agreements under their existing Eurecat collaboration to strengthen their strategic partnership.

The increase in refining processes that use crude oil, which contains more metallic content, necessitates the development of catalysts with higher capacity to withstand metal poisoning. The presence of metallic compounds like iron reduces the effectiveness of catalysts and refinery operations, prompting industry participants to design new catalyst products that have better performance even under harsh conditions. The continuous improvement in metals' tolerance is leading to the ability of refiners to be more flexible and stable in their operations. An example of this trend is the advancement of FCC catalysts by Grace in August 2024.

The increased need for petrochemical raw materials such as propylene is prompting refiners to utilize additives that maximize the production of light olefins through FCC process units. The use of ZSM-5 additives is becoming popular for increasing propylene and butylene outputs and boosting the octane content of the gasoline produced. In response to high demands at the refinery level, additive manufacturers are emphasizing capacity increase programs, thereby boosting the FCC catalyst market expansion. This makes it possible for refineries to increase the profitability of their operations. For instance, in March 2024, Ketjen announced its latest investment in ZSM-5 production.

Restructuring activities and strategic alignment in the catalyst manufacturing industry are leading to innovations and improved performance in their businesses. Through specialization of the catalytic technology into certain business organizations, firms are being able to facilitate faster research activities and an efficient production process, and also improve the ability to respond to demands from refineries. These kinds of strategies also lead to investment in the long run aimed at developing and commercializing catalysts. In line with such trends, Ketjen was established as a catalyst business in January 2023 by Albemarle Corporation.

The Expert Market Research's report titled “Global FCC Catalyst Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

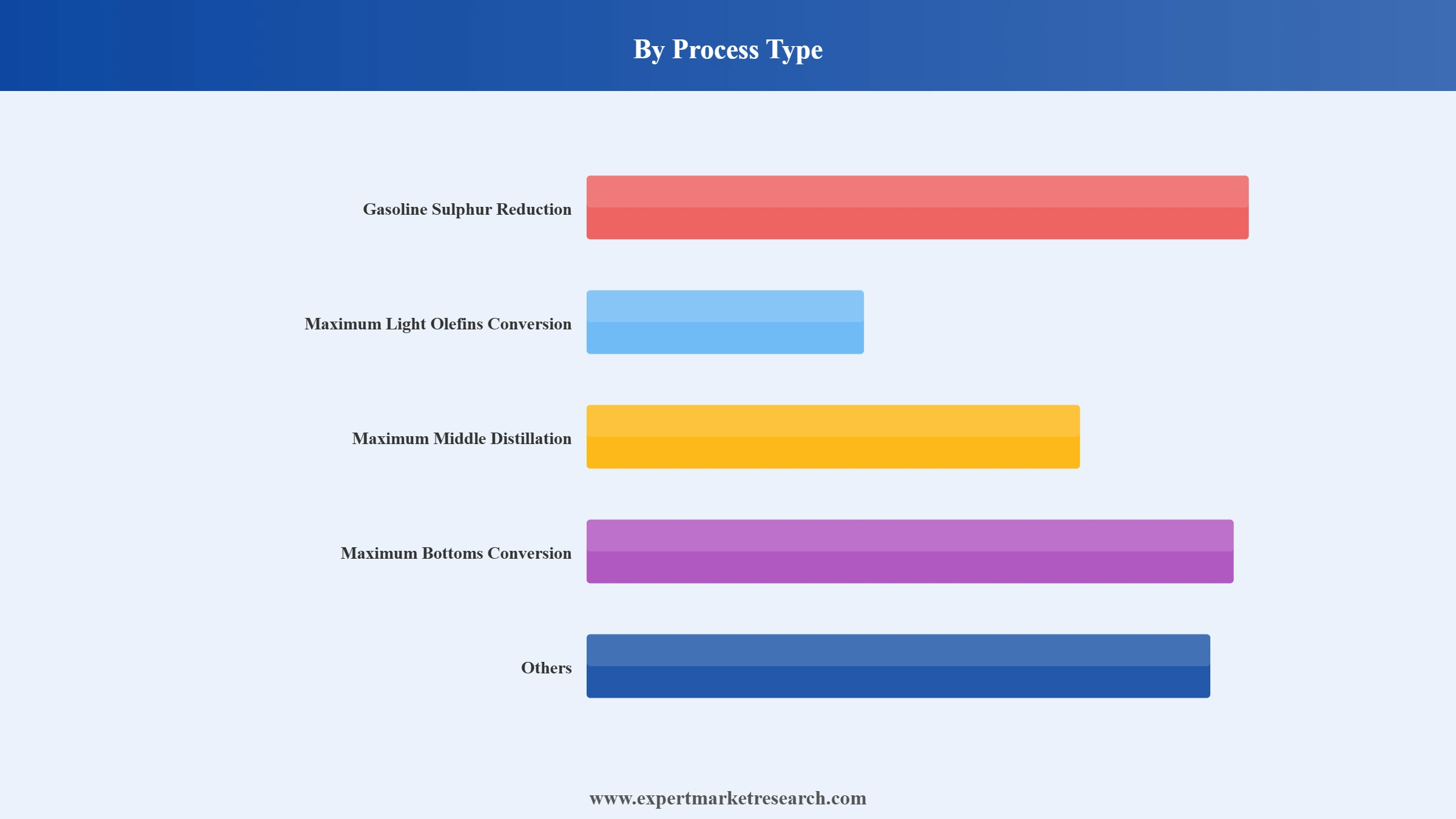

Market Breakup by Process Type

Key Insight: The global FCC catalyst market scope comprises process types that are driven by catalyst technology suited to meet the objectives of the refineries. The catalyst used in gasoline sulfur reduction assists in complying with tighter restrictions on fuel emissions. The maximum light olefin conversion catalyst assists in maximizing the yield of propylene for petrochemical uses. Maximum middle distillation catalysts increase production of diesel and jet fuels, while maximum bottoms conversion catalysts optimize the conversion of heavy ends. Firms that produce process-specific catalyst technology include W. R. Grace & Co., BASF, and Ketjen.

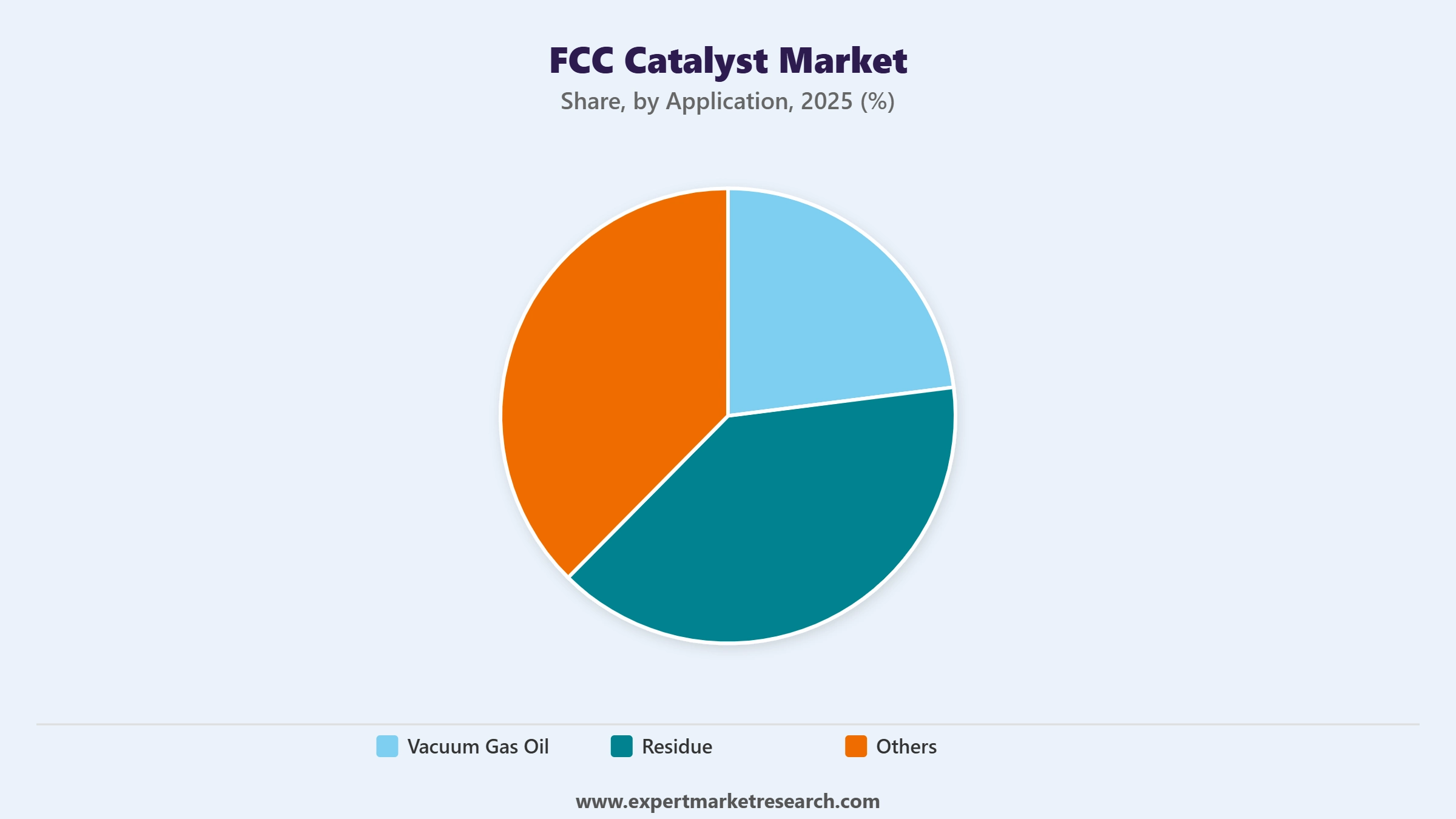

Market Breakup by Application

Key Insight: The FCC catalyst market growth is driven by different needs for feedstocks in refineries. The catalysts for use in the process involving vacuum gas oil are able to produce high yields of gasolines and light products, while those intended for use with residues place greater emphasis on high metal tolerance and better conversion of heavy hydrocarbons. Suppliers like Albemarle Corporation, W. R. Grace & Co., and BASF are constantly working to develop their technology.

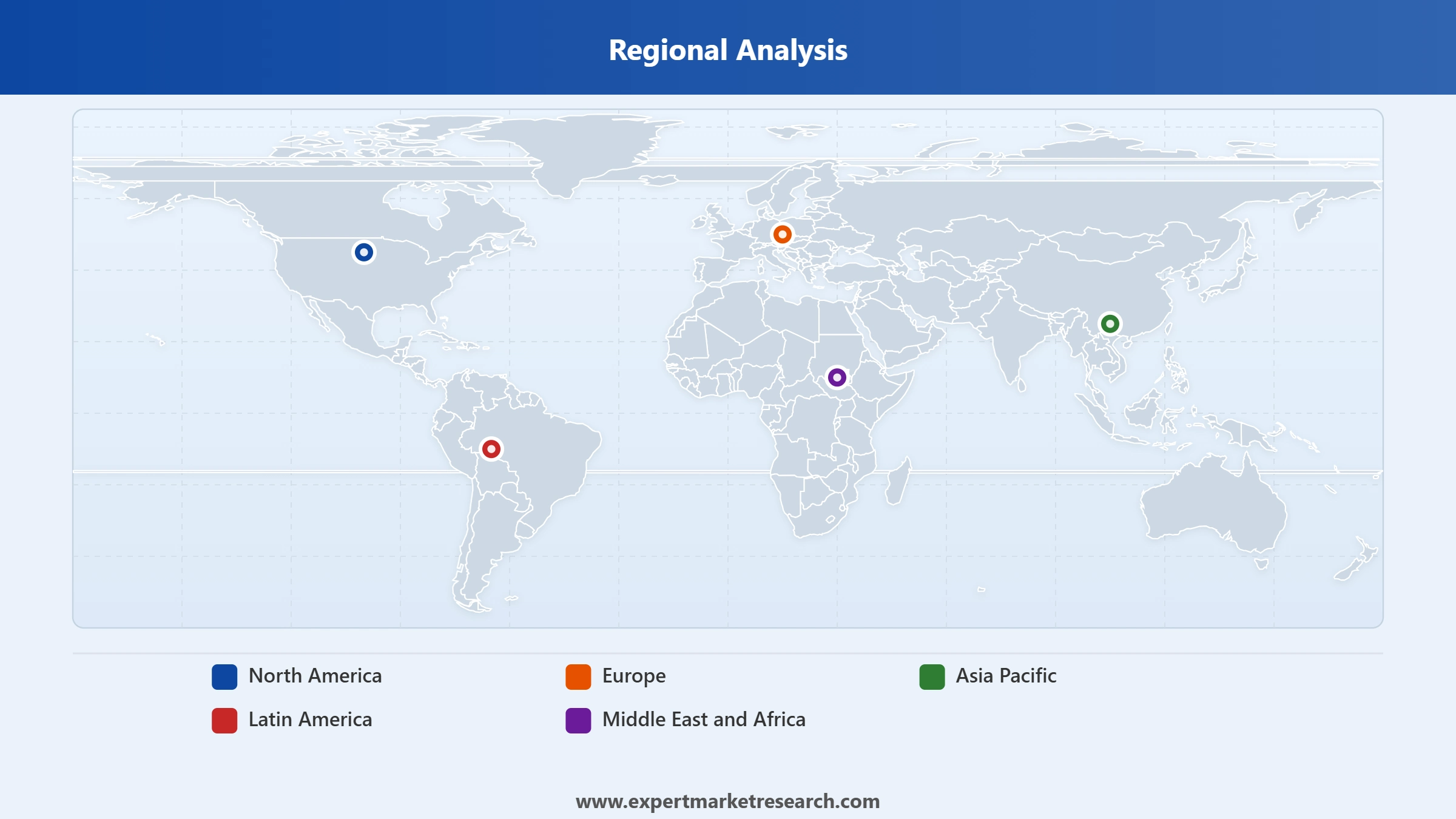

Market Breakup by Region

Key Insight: The global FCC catalyst market landscape shows different growth drivers that apply to the various regions. For example, in North America and Europe, there is an emphasis on the development of catalysts that can be used to manufacture fuels that conform to regulations. In the Asia Pacific, there is rapid growth in the construction of new refineries, which are leading to increased demand for catalysts that can convert feeds more effectively.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By process type, the gasoline sulfur reduction category records a notable growth rate driven by innovations in sustainable desulfurization catalysts

The gasoline sulfur reduction category accounts for a significant share of the FCC catalyst market, attributed to stricter fuel emission regulations and more efficient desulfurization techniques. Catalytic companies are producing sustainable products that allow improved sulfur reduction without affecting the quality of the fuel. As per the report published by Evonik Industries AG, in March 2024, Evonik introduced its Octamax catalyst for cracked gasoline hydrodesulfurization units, making it possible for oil refining companies to increase their sulfur reduction efficiency without changing octane level and requiring fresh catalysts.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

On the other hand, maximum bottoms conversion is one of the categories that is largely contributing to the FCC catalyst market revenue. This process is primarily driven by refiners’ increasing emphasis on improving the conversion efficiency of heavier bottom fractions to produce more valuable fuel outputs. Therefore, catalyst companies are formulating more advanced FCC catalysts and additives that allow high tolerance to metals and surface area for matrix and cracking activities.

By application, the residue category leads the market growth, driven by advanced catalyst technologies for sustainable fuel production

The residue treatments form an important fraction of the FCC catalyst market share as a result of the advancement of the FCC technology with regard to the capability of producing clean fuel from the heavy feedstock. The innovation is geared towards improving the feedstock flexibility, having high conversions as well as minimal emissions during the refining process. For example, W. R. Grace & Co., in October 2023, announced the launch of PARAGON FCC catalyst technology that will aid in producing clean fuels.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The market for FCC catalysts is gaining momentum in the vacuum gas oil sector as refiners aim to increase gasoline and olefins yields out of heavy feedstock. The focus of major manufacturers is now on innovations aimed at improving the catalytic activity and cracking selectivity in addition to increasing feedstock flexibility within FCC units. Leading market players such as Honeywell UOP, BASF SE, and Albemarle Corporation are introducing innovative FCC catalysts to assist refiners in maximizing their vacuum gas oil conversion.

By region, Asia Pacific dominates the market, owing to Indigenous catalyst innovation and refinery modernization

The growth in the Asia Pacific FCC catalyst market can be attributed to the increasing efforts towards refining technology improvement and investments in domestic catalyst technologies. Refineries operating in the Asia Pacific region are focusing on heavy oil processing capabilities along with improving refining efficiency using advanced catalysts and additives. In October 2024, Bharat Petroleum Corporation Limited introduced its own indigenous FCC bottoms cracking additive, “BHARAT BCA,” at its Mumbai refinery for enhancing the heavy fractions to fuels conversion process in India.

In addition, North America registers a notable growth rate in the FCC catalyst industry, driven by research and development activities aiming to enhance the performance of FCC catalysts. The refineries that operate in North America are emphasizing the use of advanced types of catalysts, which not only offer high feedstock flexibility but also reduce costs. Companies such as W. R. Grace & Co., Albemarle Corporation, and Honeywell UOP continue to invest in research and development to advance FCC catalyst technology.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The growing interest of FCC catalyst market players in innovation in catalysts can be attributed to the need to increase refinery efficiency and selectivity. In this regard, the majority of companies' resources are being invested into the development of catalysts capable of processing heavier crudes with increased gasoline and light olefin outputs. Market players also invest in the development of catalysts demonstrating high metals resistance and good stability.

Furthermore, market players are expanding their global presence through capacity enhancements while collaborating on technological innovations and service solutions for refineries. Therefore, with improved technical services, specialized products, and monitoring capabilities, FCC catalyst companies ensure that the refiners operate effectively and efficiently.

BASF SE was established in 1865 and has its headquarters located in Ludwigshafen, Germany. The company mainly focuses on chemical production all over the world and provides advanced catalyst technologies and refining processes that improve efficiency and sustainability in the overall petroleum and petrochemical value chains.

W.R. Grace & Co.-Conn. was founded in 1854 and operates from the headquarters located in Columbia, Maryland, United States of America. Its main area of specialization is catalyst and materials production; its advanced FCC catalyst technologies and refining innovations improve innovations in the global FCC catalyst industry.

The Albemarle Corporation was established in 1994 and located in Charlotte, North Carolina, United States of America. It specializes in activities such as providing services of refining catalysts and performance materials for increasing hydrocarbon conversion in the sphere of specialty chemicals and catalyst technologies.

Haldor Topsoe A/S was founded in 1940 and is located in Kongens Lyngby, Denmark. The company provides services in catalysis and process technologies for providing advanced solutions in terms of refining catalysts, contributing to the advancement of the FCC catalyst industry.

Other key players in the market include JGC Holdings Corporation, Sinopec Catalyst Co., Ltd., Royal Dutch Shell plc, China Petroleum & Chemical Corporation, and Clariant AG, among others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Explore the latest trends shaping the global FCC catalyst market 2026-2035 with our in-depth report. Gain strategic insights, future forecasts, and key market developments that can help you stay competitive. Download a free sample report or contact our team for customized consultation on global FCC catalyst market trends 2026.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the global FCC catalyst market attained a value of nearly USD 2.97 Billion.

The market is projected to grow at a CAGR of 4.00% between 2026 and 2035.

The market is estimated to grow in the forecast period of 2026-2035 to reach about USD 4.40 Billion by 2035.

The major market drivers include the increasing demand for gasoline, olefinic gases, and petroleum products, growing government investments in petroleum refining sector, and upgradations of oil and gas refineries.

Technological advancements and the increasing demand for catalytic cracking processes are the key trends guiding the growth of the market.

The major regions in the market are North America, Latin America, the Middle East and Africa, Europe, and the Asia Pacific.

Gasoline sulphur reduction, maximum light olefins conversion, maximum middle distillation, and maximum bottoms conversion, among others, are the leading FCC catalyst process types in the market.

The significant applications of the product are vacuum gas oil and residue, among others.

The major market players are BASF SE, W. R. Grace & Co.-Conn., Albemarle Corporation, Haldor Topsoe A/S, JGC Holdings Corporation, Sinopec Catalyst Co., Ltd., Royal Dutch Shell plc, China Petroleum & Chemical Corporation, Clariant AG and Others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Process Type |

|

| Breakup by Application |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

| Report Price and Purchase Option | Explore our purchase options that are best suited to your resources and industry needs. |

| Delivery Format | Delivered as an attached PDF and Excel through email, with an option of receiving an editable PPT, according to the purchase option. |

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.