Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

The global hemoglobinopathies market attained a value of USD 7.57 Billion in 2025. The market is further expected to grow in the forecast period of 2026-2035 at a CAGR of 9.70%, to reach USD 19.11 Billion by 2035.

Compound Annual Growth Rate

9.7%

Value in USD Billion

2026-2035

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

hemoglobinopathies are a group inherited blood disorders, affecting hemoglobin in the red blood cells. They are often caused by genetic mutations that lead to alteration of hemoglobin structure, function, or production. Sickle cell anemia and thalassemia are amongst the most common types of hemoglobinopathies.

It is estimated that sickle cell anemia affects approximately 100,000 United States citizens, with a higher prevalence in Black or African American race (1 in every 365 individuals ). Consequently, the hemoglobinopathies market demand is on the rise to combat the rising incidence of diseases. The market growth is driven by advancements in treatment and diagnostics. Innovations and growth in gene therapy activities is one of the major market trends. In December 2023, the United States FDA approved Exa-cel , the first CRISPR treatment for sickle cell disease. Lovo-cel, developed by Bluebird Bio is another gene therapy accepted by the FDA and will be used to treat sickle cell anemia in patients. The increasing integration of novel technologies to aid impactful treatment alternatives is expected to drive market growth in coming years.

The hemoglobinopathies market share is also poised to elevate with rising emphasis on detecting the condition early. In June 2023, Florida Atlantic University released their latest research on developing a portable tool to diagnose and monitor sickle cell anemia. Based on electrical impedance sensor, the device can analyze the rate of cell sickling and the concentration of sickled cells in the body. It can assist in quality treatment and mitigate the comorbidities associated with the disease.

The market is witnessing several trends and developments to improve the current scenario. Some of the notable trends are as follows:

To combat the rising incidence of hemoglobinopathies across the globe, many countries have started implementing new screening programs to detect any abnormalities at an early stage.

Rising partnerships between pharmaceutical companies, healthcare providers, and research institutions is a notable market trend. The collaborations are aimed at developing effective and precise solutions for patients.

Tailoring treatment plans based on the genetic profile of the patient is a significant trend in the market. Precision medicine can help in minimizing side effects while offering improved outcomes for patients.

To provide new diagnostic methods and treatment, there has been an increase in fundings and investments by government as well as non-governmental organizations.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Hemoglobinopathies Market Report and Forecast 2026-2035 offers a detailed analysis of the market based on the following segments:

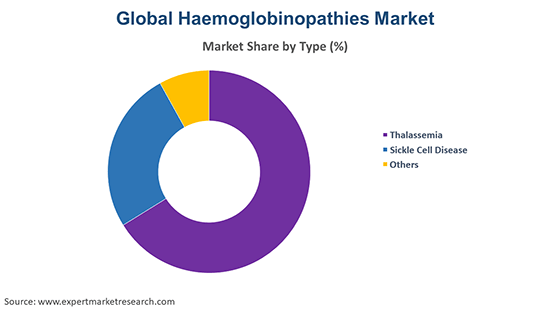

Market Breakup by Hemoglobinopathy Type

The report offers an insight into types of hemoglobinopathies. It majorly constitutes sickle cell disease, and thalassemia among others.

Market Breakup by Diagnosis Type

Based on types of diagnostics, the report is segmented into DNA testing, hemoglobin electrophoresis, complete blood count (CBC), prenatal testing, newborn screening, and others.

Market Breakup by Treatment Type

The hemoglobinopathies market growth is driven by the development of advanced treatments. The report provides a detailed breakup of treatment types, which includes blood transfusion, blood marrow transplantation, gene therapy, iron chelation therapy and others. Each treatment type is deployed based on the condition and severity of the condition in patients.

Market Breakup by End User

The report offers an analysis on the basis of end users as well. Hospitals, diagnostic laboratories, research institutions, blood banks among others are amongst key end users. Each section holds significant value, owing to rising expenditures in the healthcare domain.

Market Breakup by Region

Geographically, the market is divided into North America, Europe, Asia Pacific, Latin America, Middle East, and Africa. North America is expected to dominate the hemoglobinopathies market share. The market size can be attributed to the presence of major healthcare providers in the region, undergoing significant collaborations and acquisitions to devise the best treatment solutions. With high investments to improve the healthcare and research infrastructure, Asia Pacific is poised to experience rapid market growth.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The key features of the market report include patent analysis, grants analysis, clinical trials analysis, funding and investment analysis, partnerships, and collaborations analysis by the leading key players. The major companies in the market are as follows:

Kindly note that this only represents a partial list of companies, and the complete list has been provided in the report.

Upto 15% Off

USD

$3299 $2969

$5499 $4949

$6999 $5949

$8199 $6969

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Hemoglobinopathy Type |

|

| Breakup by Diagnosis Type |

|

| Breakup by Treatment Type |

|

| Breakup by End User |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Supplier Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 3,299

USD 2,969

tax inclusive*

Single User License

One User

USD 5,499

USD 4,949

tax inclusive*

Five User License

Five User

USD 6,999

USD 5,949

tax inclusive*

Corporate License

Unlimited Users

USD 8,199

USD 6,969

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.