Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

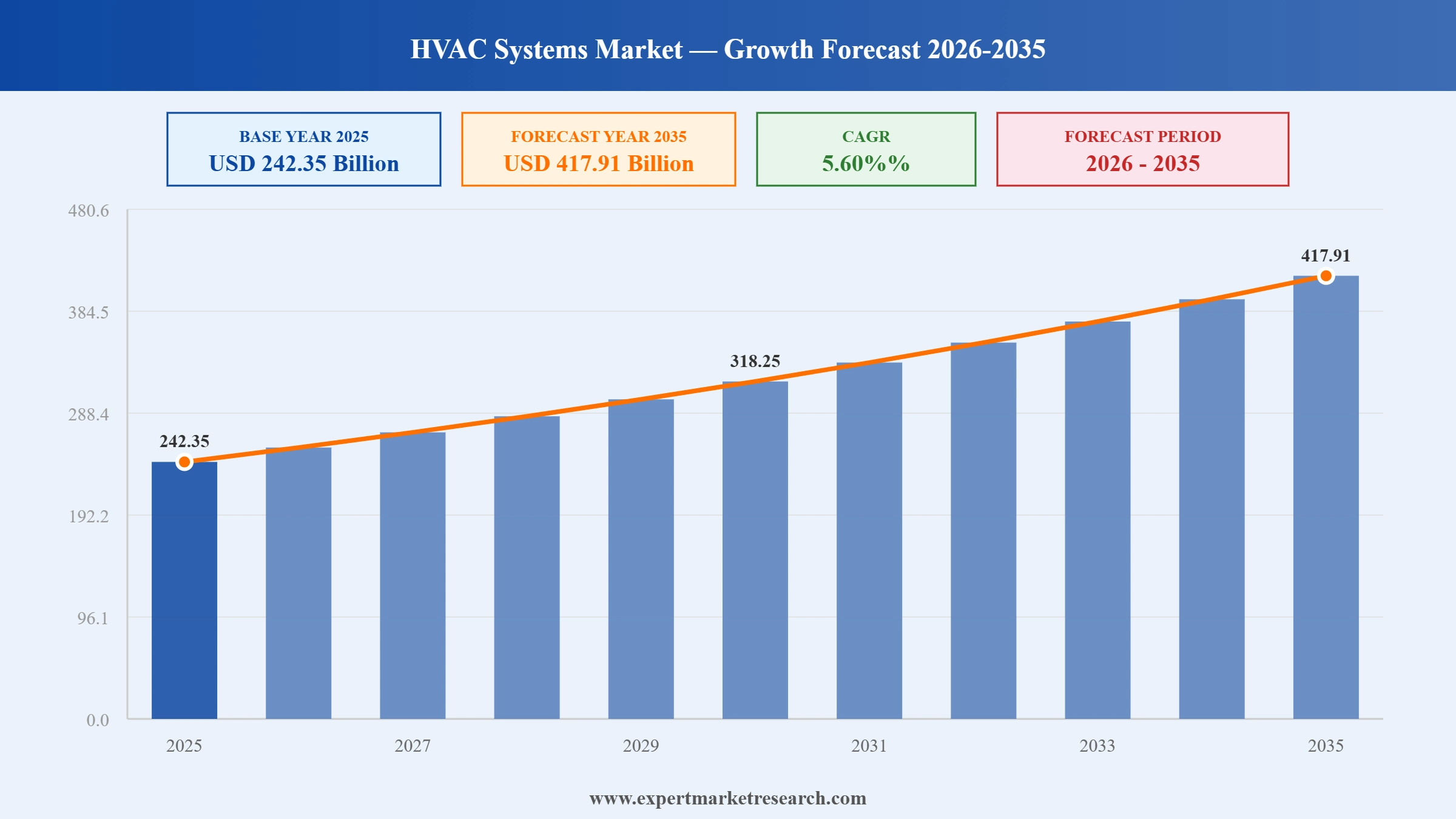

The global HVAC systems market size USD 242.35 Billion in 2025. The industry is expected to grow at a CAGR of 5.60% during the forecast period of 2026-2035. By 2035, the market is expected to reach USD 417.91 Billion.The HVAC systems market share is increasing with governments worldwide implementing stricter energy efficiency standards. In January 2024, the U.S. Department of Energy finalized new energy efficiency standards for residential cooking products to limit household utility costs and improve appliance reliability and performance. These policies are helping to lower carbon emissions and operational costs by promoting high-efficiency HVAC units that use advanced technologies, such as inverter compressors and smart thermostats. As a result, the demand is rising for these systems to meet compliance while offering long-term sustainability and savings.

According to Bloomberg, Chicago-based HVAC firm Madison Air Solutions raised USD 2.23 billion in its April 15, 2026, IPO, valuing the company at roughly USD 15.5 billion after shares surged 18% on debut. The largest US industrial IPO since 1999 signals strong investor appetite for HVAC manufacturers tied to data center and AI-driven cooling demand, reinforcing growth momentum across the global HVAC systems market.

As reported by CNBC, The Home Depot's SRS Distribution announced on March 24, 2026, an agreement to acquire Mingledorff's, a wholesale HVAC distributor operating 42 locations across five southeastern US states. The deal opens a USD 100 billion HVAC distribution vertical for Home Depot, intensifying consolidation in the sector and expanding professional contractor access to HVAC equipment, replacement parts, and aftermarket supplies.

The HVAC-as-a-Service (HVACaaS) model is emerging as a customer value proposition in the HVAC systems industry for offering flexible payment options and reducing upfront costs. This model allows businesses and homeowners to access HVAC systems without significant capital investment, promoting the adoption of energy-efficient technologies. With the tightening energy efficiency mandates and operational flexibility becoming vital, HVACaaS is gaining popularity as a cost-effective, scalable solution. The HVAC systems market is further witnessing increasing integration with building automation systems (BAS) to enhance energy efficiency and occupant comfort. In May 2025, Johnson Controls launched the NSW8000 Series Wireless Sensor to enable real-time temperature, humidity, occupancy, and optional CO2 monitoring for Metasys BAS and FX controllers. This integration allows for centralized control and monitoring of HVAC systems, lighting, and other building systems, leading to optimized performance and reduced energy consumption.

Read more about this report - Request a Free Sample

| HVAC Systems Market Report Summary | Description | Value |

| Base Year | USD Billion | 2025 |

| Historical Period | USD Billion | 2019-2025 |

| Forecast Period | USD Billion | 2026-2035 |

| Market Size 2025 | USD Billion | 242.35 |

| Market Size 2035 | USD Billion | 417.91 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 5.60% |

| CAGR 2026-2035 - Market by Region | Asia Pacific | 5.6% |

| CAGR 2026-2035 - Market by Country | China | 6.1% |

| CAGR 2026-2035 - Market by Country | USA | 4.7% |

| CAGR 2026-2035 - Market by Equipment | Cooling | 5.3% |

| CAGR 2026-2035 - Market by End Use | Residential | 5.4% |

| Market Share by Country 2025 | USA | 21.3% |

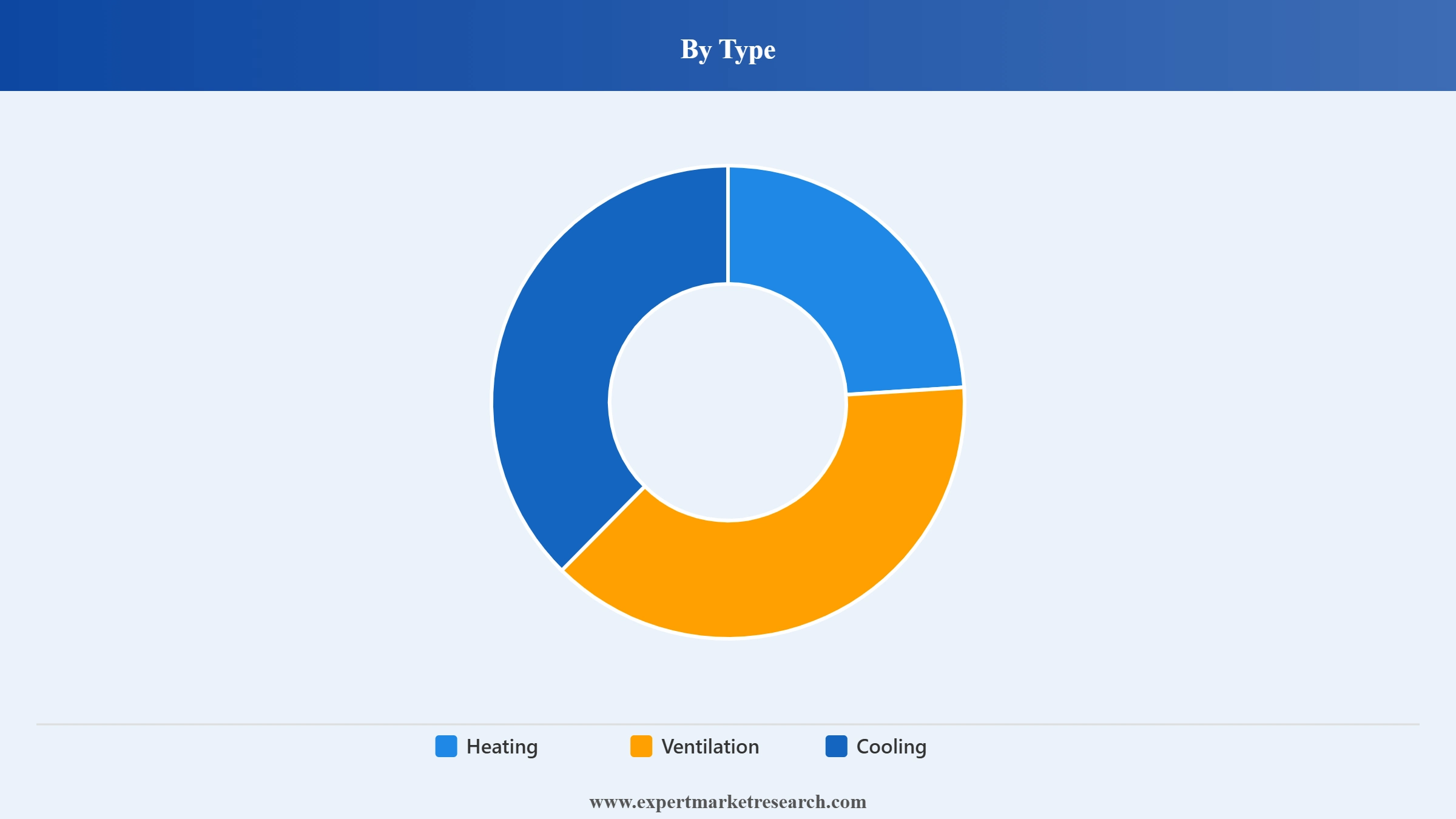

Intensifying Need for Ventilation and Cooling Systems

The ventilation segment of the HVAC systems market includes air-handling units, air filters, purifiers, ventilation fans, and humidity control devices, all essential for maintaining indoor air quality. Air-handling units regulate and circulate air in large buildings, while filters and purifiers remove allergens and pollutants, especially in polluted cities. Centrifugal fans are widely used in industrial and commercial spaces for high-efficiency air movement. Dehumidifiers and humidifiers help to control indoor moisture while improving comfort and preventing dryness. Rising health concerns, stricter air quality regulations, and smart building integration are also driving the demand for advanced, energy-efficient ventilation solutions across global markets.

The cooling segment of the HVAC systems market includes split and packaged systems, chillers, coolers, and evaporative cooling towers, each serving distinct needs across sectors. Split systems are ideal for residential use, while packaged units suit small commercial buildings due to their compact, all-in-one design. Chillers, used in large facilities to offer centralised cooling with high energy efficiency, are further driving innovations. In April 2024, Carrier introduced its new AquaForce 30XF chiller range to cater to data centres. Meanwhile, coolers, especially evaporative types, are cost-effective for dry regions. Evaporative cooling towers are essential in industrial and commercial settings for managing heat loads efficiently. This growing demand for energy-efficient, sustainable cooling solutions is adding to the segment's growth.

Read more about this report - Request a Free Sample

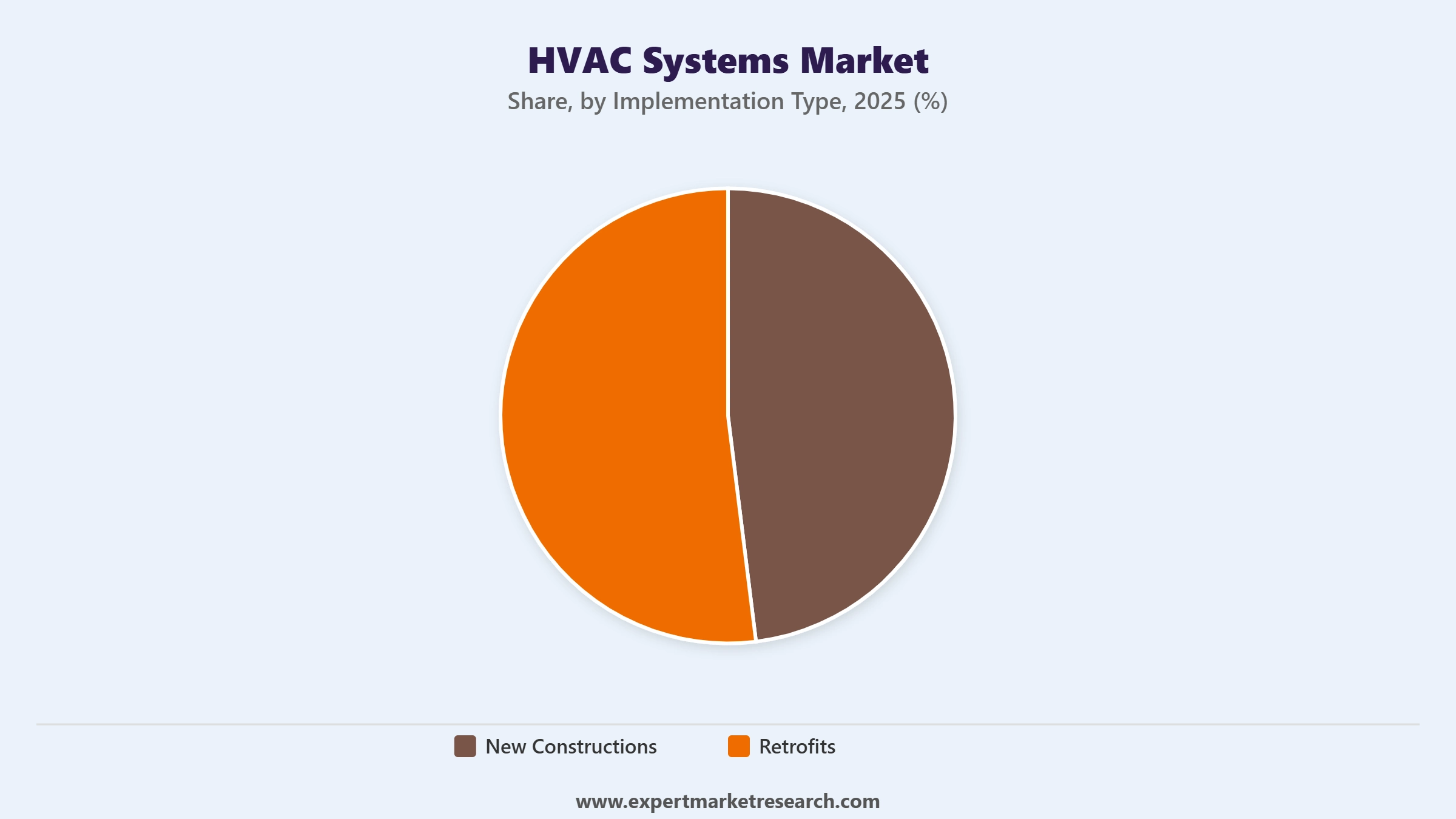

Rising Demand for Retrofits of HVAC Systems

The retrofit segment is rapidly expanding in the HVAC systems market due to ageing building infrastructure and rising energy efficiency standards. Many older structures, especially in North America and Europe, are increasingly upgraded with modern HVAC technologies to reduce energy consumption and comply with environmental regulations. For instance, in September 2023, Belimo’s RetroFIT+ program was launched for easy HVAC replacements while enhancing system efficiency, reducing emissions and improving comfort. Retrofit projects are also common in historical or commercial buildings where full reconstruction is not feasible. This segment is further crucial for sustainability and long-term HVAC industry growth.

Read more about this report - Request a Free Sample

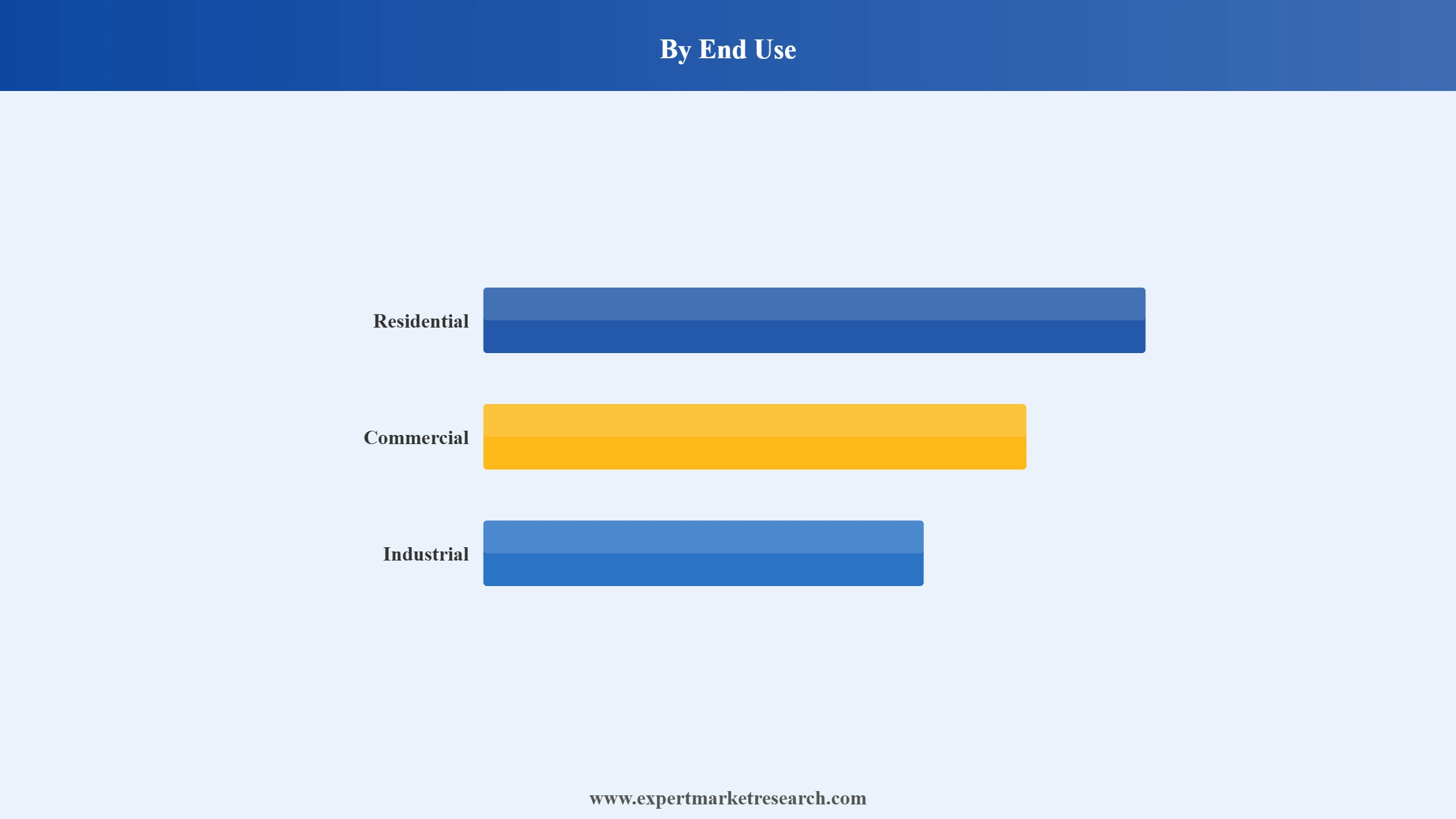

Thriving HVAC Systems Adoption in Commercial & Industrial Sectors

The commercial segment records a significant share of the HVAC systems market, led by increasing construction of office spaces, malls, hospitals, and educational institutions. These facilities require large-scale HVAC systems to ensure optimal comfort and energy efficiency. Supporting with an instance, in October 2024, Johnson Controls-Hitachi introduced sustainable solutions to cater to commercial HVAC customers across Singapore. Commercial buildings largely deploy advanced systems integrated with automation. The shift toward sustainable and intelligent infrastructure in cities is also making commercial HVAC systems a priority.

The industrial segment in the HVAC systems market is gaining importance for maintaining environmental conditions in factories, warehouses, and specialised facilities. These environments require precise climate control for operational efficiency and regulatory compliance. Demand in this segment is typically driven by the need for ventilation, temperature stability, and pollution control. The industrial HVAC sector also involves higher-value, customised systems, making it strategically significant for players focusing on performance-intensive and mission-critical applications.

Read more about this report - Request a Free Sample

SPX Technologies, Inc. (NYSE: SPXC) completed the acquisition of Thermolec Ltd., a Montreal-based manufacturer of electric duct heating equipment, modulating controls, and steam humidifiers for the HVAC industry, for total cash consideration of CA$195 million (approximately US$140 million) on January 20, 2026.

Hajoca Corp. acquired American Refrigeration Supplies (ARS), an HVACR distributor operating 34 branches and two distribution centers across seven U.S. states, from Kitchell on February 2, 2026, marking Hajoca's sixth major HVAC sector acquisition and expanding its network to more than 175 HVAC-focused locations across North America.

Ecolab announced on March 20, 2026, a definitive agreement to acquire CoolIT Systems, a provider of liquid cooling technology for AI data centers, from KKR-managed funds for approximately $4.75 billion in cash, with the transaction expected to close in the third quarter of 2026.

Carrier Global Corporation (NYSE: CARR) reported Q1 2026 net sales of $5.3 billion on April 30, 2026, with global Commercial HVAC orders up 35% year-over-year, driven by data center orders increasing over 500%, and reaffirmed its full-year financial outlook.

Urbanization is driving the HVAC systems market, as the population is rapidly shifting to urban areas, creating higher demand for residential, commercial, and industrial infrastructure. With the expansion of cities, the construction of apartment complexes, office buildings, shopping malls, hospitals, and data centers is accelerating, each requiring reliable, energy-efficient climate control systems. According to industry reports, about 68% of the global population is expected to live in urban areas by 2050, adding immense pressure on infrastructure development.

The integration of smart technology is complimenting the HVAC systems market for revolutionizing indoor climate management. Smart HVAC systems equipped with IoT sensors, AI algorithms, and automated controls offer real-time monitoring and precise regulation of temperature, humidity, and air quality. In December 2024, Meross unveiled its first Matter-certified smart thermostat for North American HVAC systems, featuring a Wi-Fi-connected white glass panel with a touch screen, smart scheduling, and system usage tracking. This tech-forward shift is appealing to both residential and commercial users seeking convenience, energy efficiency, and sustainability, driving market growth globally.

The HVAC systems market expansion is driven by the increasing shift towards decarbonisation and electrification to reduce carbon emissions and reliance on fossil fuels. According to industry reports, the rate of power generation across the globe rose by 2.6% in 2023. Heat pumps and other electric-based systems are becoming popular alternatives to traditional heating and cooling methods, promoting sustainability and energy efficiency.

Government incentives and rebates are influencing the HVAC systems industry for encouraging the adoption of energy-efficient systems across residential, commercial, and industrial sectors. In January 2025, the government of Ontario introduced new energy efficiency programs offering rebates on renovations to help reduce energy bills. These financial benefits are reducing the initial cost barrier, making advanced, eco-friendly technologies more accessible to consumers and businesses.

The integration of renewable energy sources, such as solar and geothermal is gaining traction in the HVAC systems market. These systems not only reduce dependence on fossil fuels but also lower operating costs. As per industry reports, the global installation of solar energy touched 600 GW in 2024, and is expected to reach an installation of 1 TW per year by 2030. This rise in consumption is making solar a viable option for HVAC integration.

The Expert Market Research's report titled “HVAC Systems Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

Market Breakup by Type

Key Insight: The heating segment of the HVAC systems market includes heat pumps, furnaces, and boilers, all essential for maintaining indoor comfort in colder climates. Air-to-air heat pumps offer energy-efficient heating and cooling, making them ideal for moderate climates and further driving innovations. For instance, in January 2025, Carrier introduced its new 4-14 kW line of heat pumps for residential and commercial applications. Oil furnaces deliver strong heat output but face declining demand due to environmental concerns. Boilers remain common for offering efficient radiant heating through gas, oil, and electricity. As regulations tighten and energy efficiency becomes crucial, the market is shifting toward greener and high-efficiency systems across all heating technologies.

Market Breakup by Implementation Type

Key Insight: The new construction segment leads the HVAC systems market due to the rapid growth of residential and commercial real estate worldwide. Urbanization, government infrastructure initiatives, and green building codes are accelerating the demand for integrated, energy-efficient HVAC installations in newly built structures. As per industry reports, 68% of the global population is projected to reside in urban areas by 2050. Mega projects, such as Saudi Arabia’s NEOM and India's Smart Cities Mission are also heavily relying on advanced HVAC setups designed during the construction phase, adding to the segment growth.

Market Breakup by End Use

Key Insight: The residential segment is the largest segment of the HVAC systems market, driven by rapid urbanization, rising disposable incomes, and growing awareness of indoor air quality. Demand for energy-efficient and smart HVAC solutions is increasing, especially in developing economies, such as India, China, and Brazil. Additionally, climate change and rising global temperatures are continuing to fuel the need for residential cooling systems across all regions. In March 2024, Trane Technologies unveiled a comprehensive overhaul of its residential HVAC product lineup for introducing enhancements to improve energy efficiency and sustainability, adding to the segment's growth.

Market Breakup by Region

Key Insight: North America dominates the global HVAC systems market, primarily due to its highly developed infrastructure, stringent energy regulations, and climate variability. The United States and Canada are major contributors, with strong demand for energy-efficient systems in both residential and commercial sectors. Government initiatives and retrofitting of ageing infrastructure are further boosting market growth. Highlighting this trend, in May 2024, the Canada Infrastructure Bank offered USD 70 million in financing to CAPREIT to retrofit 60 multi-residential buildings across Canada. Additionally, extreme weather patterns necessitate reliable HVAC systems, reinforcing consistent market demand.

Read more about this report - Request a Free Sample

The HVAC systems market is growing as the focus on energy-efficient heating, ventilation, and air conditioning solutions intensifies across residential, commercial, and industrial applications. Ongoing urbanisation, large-scale infrastructure development, and evolving building energy standards continue to shape market progress. Advancements such as smart HVAC systems, automated climate control, and IoT integration are enhancing operational efficiency and system reliability. Manufacturers are prioritising innovative technologies that optimise energy use while improving indoor air quality and thermal comfort.

Regional trends indicate strong market momentum in areas experiencing active construction and changing climate conditions. The emphasis on sustainable construction practices and green building certifications is encouraging the adoption of advanced HVAC solutions with reduced environmental impact. Supportive government policies, modernisation of older systems, and growing awareness of indoor air quality are contributing to long-term market expansion. This analysis highlights a market environment focused on technological innovation, regulatory alignment, and dependable climate control solutions.

Read more about this report - Request a Free Sample

Europe & Asia Pacific to Boost HVAC Systems Market

Europe HVAC systems market share is propelled by robust environmental policies and increasing emphasis on sustainability. The European Union’s strict regulations on carbon emissions and building energy efficiency are driving the adoption of eco-friendly HVAC technologies. Germany, France, and the United Kingdom are major players due to government incentives and retrofitting programs targeting older buildings. The growing trend of smart homes and the integration of IoT in HVAC units is also supporting the market.

Asia Pacific is contributing to the HVAC systems market, fuelled by rapid urbanisation, population expansion, and rising disposable income, particularly in China, India, and Southeast Asian nations. According to industry reports, 68% of the global population is estimated to live in urban areas by 2050. Increasing construction of commercial buildings and residential complexes is spurring the demand for HVAC systems. The surging adoption of advanced HVAC technology, mainly in Japan and South Korea, is also driving the regional market growth.

Read more about this report - Request a Free Sample

Prominent players operating in the HVAC systems market are adopting a range of strategic initiatives to strengthen their global presence and meet evolving consumer needs. One primary focus is the development of energy-efficient and environmentally friendly technologies. With tightening regulatory standards and growing demand for sustainability, companies are investing in research & development to produce smart HVAC systems that utilize IoT, AI, and automation for better performance and lower emissions. Strategic mergers, acquisitions, and partnerships are commonly pursued to expand market share, enter new regions, and diversify offerings.

Meanwhile product diversification and customization are enabling companies to serve distinct market segments, including residential, commercial, and industrial sectors. Many brands are tailoring their solutions to climate-specific and region-specific needs, enhancing customer relevance. Digital transformation is playing a growing role, with cloud connectivity, remote monitoring, and predictive maintenance becoming standard features. These innovations improve system reliability and end-user experience. Lastly, companies focus on marketing and branding, often highlighting smart features and sustainability to differentiate their products.

Lennox International, Inc., founded in 1895 and headquartered in Texas, the United States, specializes in climate control solutions, providing heating, ventilation, air conditioning (HVAC), and refrigeration systems. The company’s product portfolio serves both residential and commercial markets, emphasizing energy efficiency and innovation in indoor air quality and temperature regulation.

Founded in 1958, LG Electronics, Inc. is based in Seoul, South Korea and offers a diverse range of consumer electronics, home appliances, and HVAC solutions. LG's product lineup includes televisions, mobile devices, refrigerators, and air conditioners, with a strong focus on smart technology and sustainability across both residential and commercial applications.

Carrier Global Corporation, headquartered in Florida, the United States and founded in 2020, provides HVAC systems, refrigeration, and building automation solutions. The company serves residential, commercial, and industrial clients, focusing on energy efficiency, environmental stewardship, and advanced technology for climate and safety solutions.

Established in 1969 and headquartered in Suwon, South Korea, Samsung Electronics Co. Ltd. is a global leader in technology and consumer electronics. The company manufactures smartphones, semiconductors, televisions, and home appliances. Samsung also provides digital and HVAC solutions for offering advanced innovations that integrate smart technologies across diverse product categories.

Other players in the HVAC systems market are Haier Smart Home Co., Ltd., Daikin Industries, Ltd, Emerson Electric Co., Honeywell International Inc, Johnson Controls International plc, Hitachi Ltd., Havells India Ltd., Fujitsu, Mitsubishi Electric Corporation, Rheem Manufacturing Company, and Trane, among others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Download a free sample of the HVAC Systems Market Report today to explore detailed forecasts, emerging technologies, and competitive insights. Stay ahead with expert analysis of the HVAC systems market trends 2026, government policies, and innovations shaping the future of climate control solutions. Empower your decisions with trusted, data-driven intelligence.

North America HVAC Market

Saudi Arabia HVAC Market

Chile HVAC Market

UAE HVAC Market

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market reached an approximate value of USD 242.35 Billion.

The market is projected to grow at a CAGR of 5.60% between 2026 and 2035.

The market is estimated to witness a healthy growth during 2026-2035 to reach around USD 417.91 Billion by 2035.

Key strategies driving the market include adoption of energy-efficient and smart technologies, government incentives promoting sustainable solutions, and rising urbanization increasing demand for climate control systems. Additionally, manufacturers are expanding through strategic partnerships, product innovations, and service-based models like HVAC-as-a-Service to meet evolving customer and regulatory expectations.

The key trends aiding the market include a growing preference for condensing boilers; popularity of ductless HVAC; growing demand for sustainable HVAC systems; and the rise of smart HVACs.

The major regions in the industry are North America, Latin America, the Middle East and Africa, Europe, and the Asia Pacific.

The leading equipment types in the industry are heating, ventilation, and cooling.

The major implementation types of HVAC systems in the market are new constructions and retrofits.

The significant end use segments in the industry are residential, commercial, and industrial sectors.

The key players in the market report include Lennox International, Inc., LG Electronics, Inc., Carrier Global Corporation, Samsung Electronics Co. Ltd., Haier Smart Home Co., Ltd., Daikin Industries, Ltd, Emerson Electric Co., Honeywell International Inc, Johnson Controls International plc, Hitachi Ltd., Havells India Ltd., Fujitsu, Mitsubishi Electric Corporation, Rheem Manufacturing Company, and Trane, among others.

The residential segment is the largest segment of the market, driven by rapid urbanization, rising disposable incomes, and growing awareness of indoor air quality.

Asia Pacific led the market owing to improving economic conditions, rapid industrialization, and commercialization are anticipated to have a positive impact on the HVAC systems market growth.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Type |

|

| Breakup by Implementation Type |

|

| Breakup by End Use |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.