Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

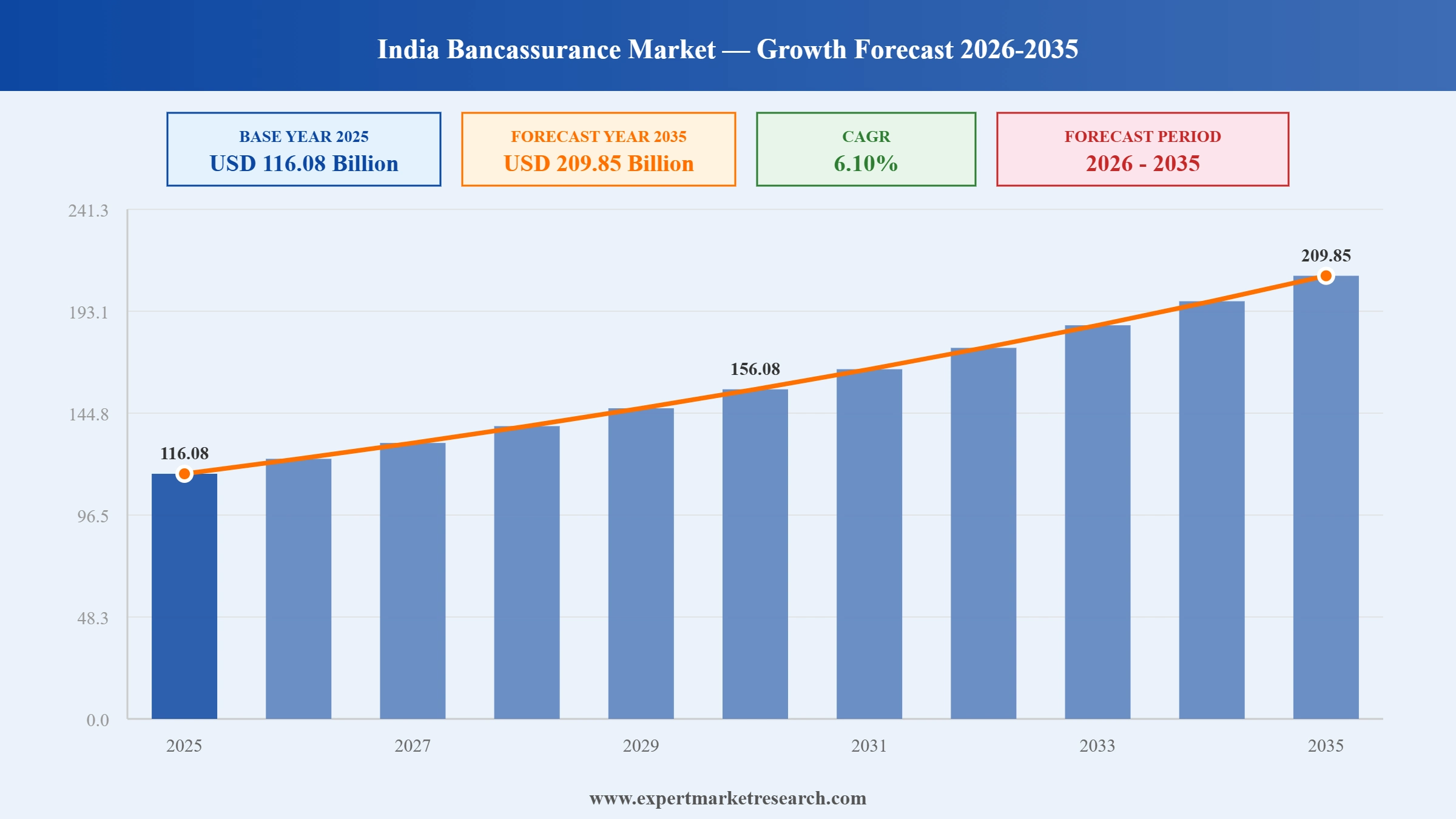

The India Bancassurance Market reached a value of USD 116.08 Billion at 2025 and is projected to expand at a CAGR of around 6.10% during the forecast period of 2026-2035. With surging government support for insurance penetration, expanding InsurTech-bank collaborations, deepening mobile banking integration, and growing financial awareness among rural and semi-urban consumers, the market is expected to reach USD 209.85 Billion by 2035.

Department of Financial Services Secretary M. Nagaraju on April 21 directed banks to abandon exclusive bancassurance partnerships and adopt a neutral, multi-insurer distribution stance to widen consumer choice. The push triggered a sharp sell-off in life insurer stocks including SBI Life and Canara HSBC Life, as reported by The Economic Times, signalling a likely shift toward open architecture in India's bancassurance market and renewed scrutiny on parent-bank distribution economics.

Public consultation on the Reserve Bank of India's draft Responsible Business Conduct Amendment Directions closed in early March, with the rules barring compulsory bundling of insurance with bank loans and mandating explicit customer consent before policy issuance. Bancassurance income, estimated at INR 25,000 crore annually, faces meaningful pressure in the credit life segment ahead of the July rollout, according to Business Standard.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

|

India Bancassurance Market Report Summary |

Description |

Value |

|

Base Year |

USD Billion |

2025 |

|

Historical Period |

USD Billion |

2019-2025 |

|

Forecast Period |

USD Billion |

2026-2035 |

|

Market Size 2025 |

USD Billion |

116.08 |

|

Market Size 2035 |

USD Billion |

209.85 |

|

CAGR 2019-2025 |

Percentage |

XX% |

|

CAGR 2026-2035 |

Percentage |

6.10% |

|

CAGR 2026-2035 - Market by Region |

East India |

6.5% |

|

CAGR 2026-2035 - Market by Region |

West India |

6.3% |

|

CAGR 2026-2035 - Market by Product Type |

Life Bancassurance |

6.6% |

|

CAGR 2026-2035 - Market by Model Type |

Exclusive Partnership |

7.2% |

|

2025 Market Share by Region |

West India |

27.2% |

India's bancassurance market is shaped by regulatory modernization, InsurTech adoption, expanding rural distribution networks, and evolving partnership models that are deepening integration between banking and insurance ecosystems.

In October 2025, RBL Bank announced a bancassurance partnership with the Life Insurance Corporation of India, India's largest state-owned life insurer. The agreement allows RBL Bank customers to access LIC's comprehensive suite of life insurance products through the bank's branch network and digital platforms. The partnership is structured to deepen LIC's distribution reach among urban and semi-urban banking customers while enabling RBL Bank to generate non-interest income through insurance sales commissions. This tie-up reflects a broader industry trend of banks pursuing bancassurance partnerships to diversify revenue streams as the traditional lending margin environment remains under pressure.

In October 2025, Ageas Federal Life Insurance announced a strategic bancassurance partnership with CSB Bank to expand life insurance access specifically for small and medium enterprises and individual entrepreneurs. The partnership integrates protection-oriented financial products into CSB Bank's branch network, providing business owners and self-employed customers with tailored insurance coverage suited to their financial planning needs. The tie-up marks one of the early initiatives targeting SME bancassurance as a distinct segment, recognising the unique risk and protection requirements of small business owners who often lack access to group insurance schemes available to corporate employees.

In June 2025, AU Small Finance Bank announced a bancassurance partnership with the Life Insurance Corporation of India, giving AU SFB's customers access to LIC's life insurance, term, endowment, and pension products across over 2,456 banking touchpoints nationwide. The partnership is significant because small finance banks primarily serve underbanked and semi-urban customer segments, broadening LIC's reach beyond its traditional urban-focused distribution. For AU SFB, the tie-up strengthens its financial services product portfolio and reinforces its positioning as a full-service bank for underserved markets, contributing to India's goal of achieving universal insurance coverage by 2047.

In April 2025, the Indian government granted conditional approval to insurers to expand their bancassurance distribution networks, clearing the way for broader bank-insurer collaboration across the country. The move follows years of regulatory discussion around diversifying insurance distribution beyond traditional agent channels. By conditionally greenlighting expanded bancassurance networks, the government signaled its intent to accelerate insurance penetration in underserved regions. Industry participants, including Star Health and Allied Insurance, responded by announcing plans to add 29 to 30 new bancassurance partners by the first half of 2026, illustrating the immediate commercial response to the policy shift.

In February 2025, India Post Payments Bank entered a bancassurance partnership with PNB MetLife India Insurance Company, utilizing IPPB's vast network of 650+ branches and 1.36 lakh access points to make life insurance available to millions of Indians in remote and underserved areas. The collaboration specifically targets communities that have historically been excluded from formal insurance due to the absence of private bank branches and insurance distribution infrastructure. By leveraging the postal network for insurance distribution, the partnership represents a meaningful step toward the IRDAI's ambitious goal of achieving universal insurance coverage across India by 2047.

Government support for bancassurance has become one of the most powerful structural growth drivers in India's insurance sector. The IRDAI's vision of achieving universal insurance coverage by 2047 has created a clear policy mandate for expanding bancassurance as a primary distribution channel. In April 2025, the Indian government granted conditional approval for insurers to expand their bancassurance networks, prompting companies like Star Health and Allied Insurance to announce plans for adding 29 to 30 new bank partners by the first half of 2026. Private sector life insurers have rapidly increased their market share from 56% in FY2018 to 68% by Q2 FY2025, and bancassurance is the distribution channel most responsible for this structural shift in the India bancassurance market growth trajectory.

Access to insurance in rural and semi-urban India remains significantly below urban levels, and bancassurance through public sector banks, postal networks, and small finance banks is increasingly recognized as the most viable solution. Banks with broad rural reach are now central to the government's financial inclusion agenda, and partnering with insurers has become a natural extension of their mandate. In February 2025, India Post Payments Bank teamed up with PNB MetLife India Insurance to deliver life insurance products through its 1.36 lakh access points, primarily serving customers in regions with little or no private insurance agent presence. This approach pairs IPPB's physical reach with PNB MetLife's insurance product expertise, creating a scalable model for rural insurance distribution that others are likely to replicate.

The rapid expansion of InsurTech in India is reshaping how insurance products are distributed and serviced through bank channels, making bancassurance more personalized, faster, and digitally seamless. AI-powered recommendation engines, paperless digital KYC, and mobile banking-embedded insurance journeys are reducing friction at every stage of the customer lifecycle. The Indian InsurTech sector is reported to have grown twelvefold in revenue over five years, reaching USD 750 million in 2023. In July 2024, ICICI Lombard launched Elevate, a new health insurance plan built with AI technology designed to offer tailored solutions for diverse healthcare needs and unforeseen medical emergencies, representing the type of technology-driven product innovation now driving growth across bancassurance channels in India.

India's bancassurance regulatory environment is undergoing active reform aimed at improving distribution transparency, curbing mis-selling, and promoting multi-insurer model diversity. IRDAI has been deliberating regulations to cap the share a parent bank can hold in a life insurance subsidiary's bancassurance business, intended to reduce conflicts of interest and encourage more open distribution practices. These reforms are pushing banks and insurers toward the pure distributor and open architecture models, which accounted for approximately 39% and a significant portion of model-type market share respectively in 2025. In December 2024, IRDAI was formally considering new cap regulations for bancassurance business concentration, signaling a structural regulatory shift that will influence how partnerships are structured across the India bancassurance market over the forecast period.

The Expert Market Research's report titled "India Bancassurance Market Report and Forecast 2026 to 2035" offers a detailed analysis of the market based on the following segments:

Market Breakup by Product Type

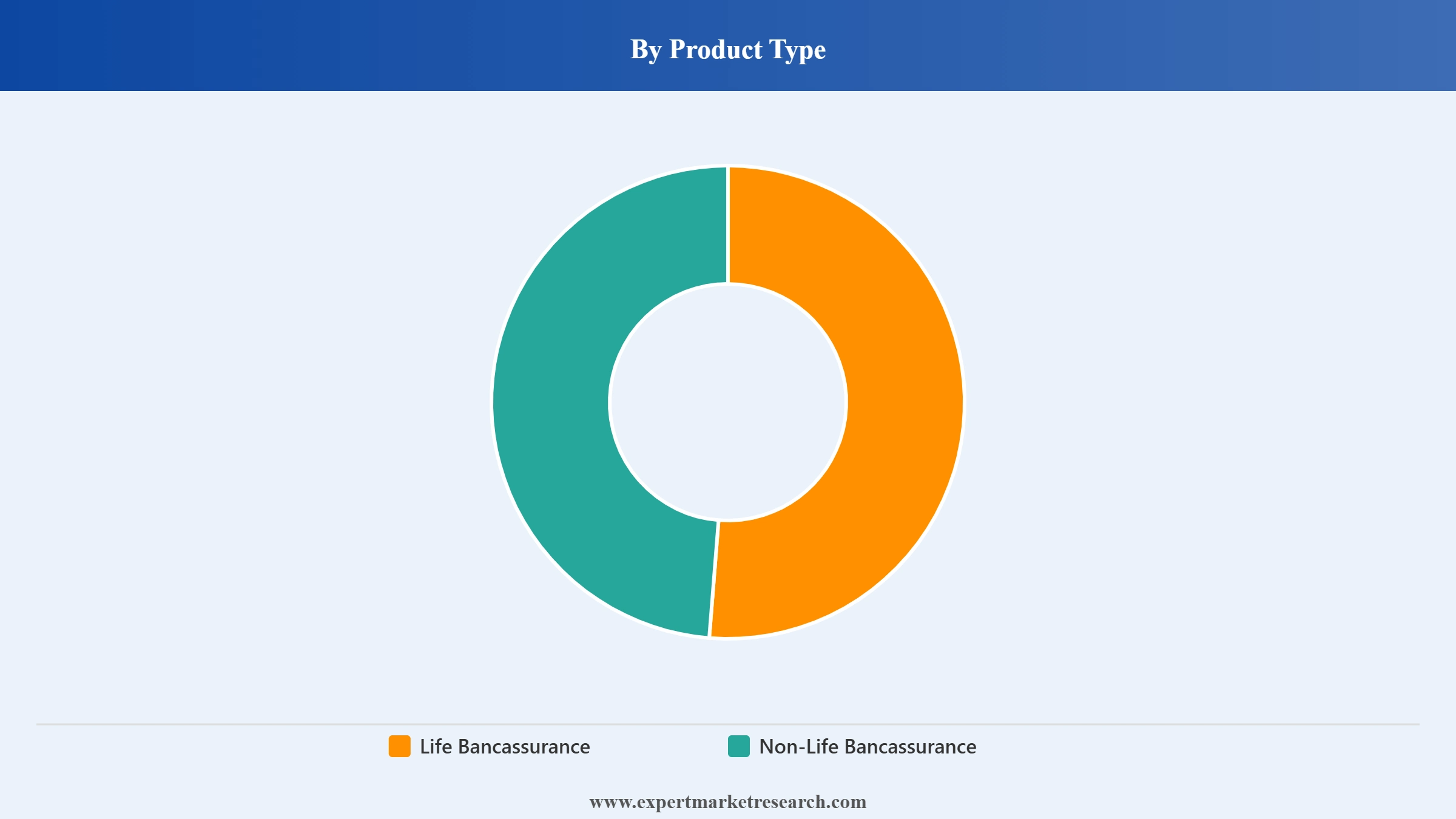

Key Insight: Life Bancassurance dominates the India Bancassurance Market, accounting for approximately 60% of total market revenue in 2025. Its leadership reflects persistent consumer demand for long-term financial protection instruments, retirement planning, and tax-saving investment-linked insurance products sold through bank channels. Banks have deeply integrated life insurance products into their wealth management and loan disbursement workflows, cross-selling term and endowment policies to existing customers at key financial decision points. HDFC Life, for example, generated over 60% of its individual new business through bancassurance in FY2024, with premiums sourced through corporate bank agents having grown at a CAGR of approximately 15.3% between FY2019-20 and FY2023-24. Non-Life Bancassurance is the faster-growing segment, driven by rising demand for health, vehicle, and general insurance, aided by regulatory changes and new embedded insurance models at digital platforms.

Market Breakup by Model Type

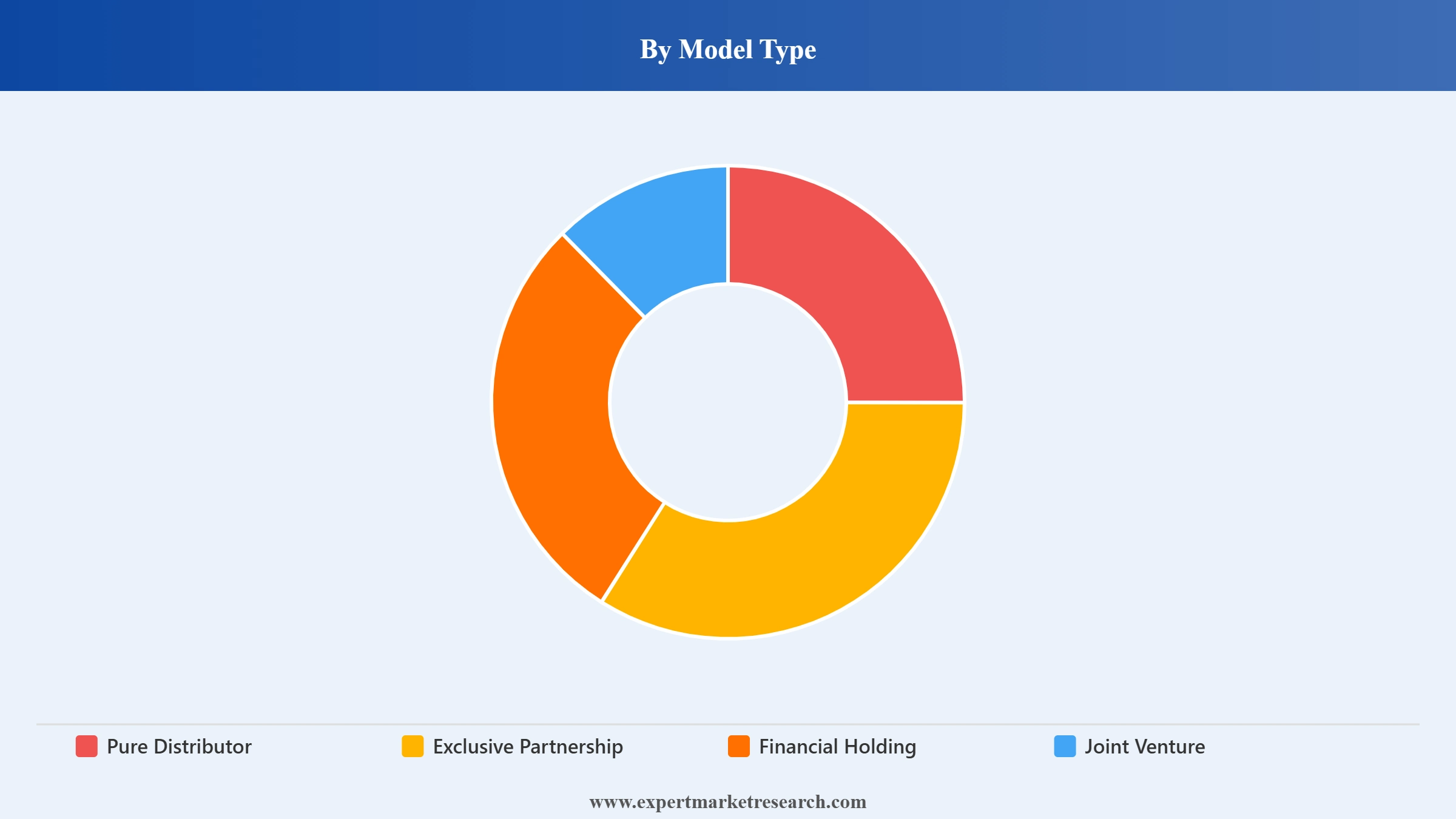

Key Insight: The Pure Distributor model leads the India Bancassurance Market by model type, holding approximately 39% of the market share in 2025. This model is preferred because it allows banks to distribute insurance products through commission-based arrangements without requiring capital investment, equity ownership, or complex regulatory compliance typically associated with deeper structural models. It is especially favored by mid-size and smaller banks entering insurance distribution for the first time. The Exclusive Partnership model represents a mature, high-performing segment where a bank partners deeply with one insurer per category, allowing for more tailored product offerings and stronger co-branding. Financial Holding and Joint Venture models are more prevalent among large private sector banks, enabling tighter data integration, shared customer analytics, and co-developed insurance products.

Market Breakup by Region

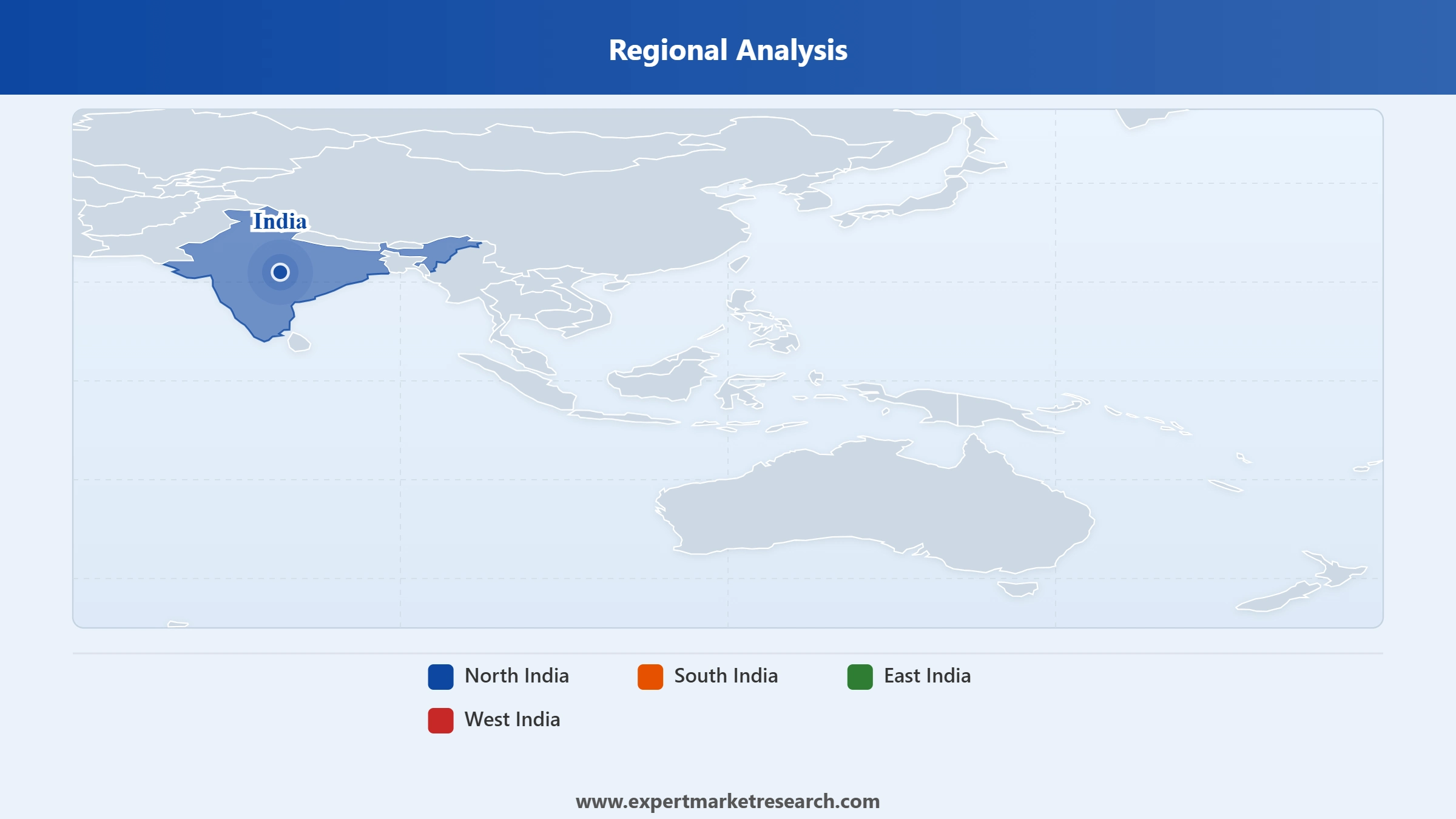

Key Insight: West and Central India leads the India Bancassurance Market with approximately 32% of total market share in 2025, anchored by the concentration of leading insurers, private sector banks, and BFSI institutions in Mumbai and Maharashtra. South India is the market's fastest-growing region, with a strong private banking ecosystem across Karnataka, Tamil Nadu, and Telangana driving bancassurance adoption. North India contributes significantly through the national capital region's large salaried population and strong penetration of public sector banks with bancassurance mandates. East India, while currently the smallest regional segment, is an emerging growth area driven by expanding banking access in West Bengal, Odisha, and the northeastern states, supported by Jan Dhan account expansion and regional financial inclusion programs.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Product Type

Life Bancassurance is the dominant segment, accounting for approximately 60% of total India Bancassurance Market revenue in 2025. Its dominance is rooted in India's cultural emphasis on financial security for families and the structural advantage of life insurance as a tax-saving instrument under Section 80C of the Income Tax Act. Banks have made life insurance a standard component of their financial planning conversations with customers, particularly at loan origination, salary account opening, and retirement planning touchpoints. The HDFC Life and ICICI Prudential bancassurance businesses exemplify this integration, together generating thousands of crores in annual premium through bank-led distribution. Non-Life Bancassurance, while smaller in absolute share, is growing faster as consumers become increasingly aware of health, vehicle, and property insurance requirements, and as embedded insurance models on digital platforms create new purchase occasions for non-life products.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Model Type

The Pure Distributor model commands the largest share of India's bancassurance market by model type, driven by its operational simplicity and the wide range of banks that can participate without the need for significant structural commitments. The model's 39% share in 2025 reflects how broadly it has been adopted across public and private sector banks of varying sizes. However, the Exclusive Partnership model remains strategically important for the largest banks and insurers, enabling deeper product integration and joint marketing campaigns that generate higher premium yields per customer. Research from Magi Research and Consultants highlights that bancassurance channels reduce customer acquisition costs by 40 to 50% compared to traditional distribution, creating compelling economics for banks that commit to more integrated partnership structures.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

West and Central India holds the largest share of the India Bancassurance Market, with Maharashtra standing as the undisputed commercial center. Mumbai is home to the headquarters of LIC, HDFC Life, ICICI Prudential, SBI Life, and several major private sector banks whose bancassurance operations collectively set the benchmark for market performance. The density of financial institutions and their established corporate agency networks creates a volume base that is difficult for other regions to match in the near term. According to available research, West and Central India accounted for approximately 32% of total bancassurance market share in 2025. The region benefits from higher average income levels, greater financial literacy, and a consumer base already accustomed to purchasing complex financial products through bank relationships.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

South India is the most dynamic growth market within India's bancassurance sector, driven by the strong presence of private sector banks, a highly educated workforce, and deep smartphone penetration that supports digital insurance distribution. Karnataka, Tamil Nadu, and Telangana have all invested heavily in fintech and financial services infrastructure, and South India's urban population shows higher willingness to adopt new financial products compared to national averages. Bancassurance partnerships in this region increasingly involve digital-first product journeys embedded within mobile banking apps, reducing agent dependency and enabling insurers to serve a younger demographic effectively. The IndiaFirst Life CEO's observation that South India leads in first-time insurance buyer engagement through bancassurance channels underscores the region's role as the market's primary growth frontier over the forecast period.

The India Bancassurance Market is structured around deep partnerships between major banks and established life and general insurance companies. The market is moderately concentrated, with HDFC Life, LIC, SBI Life, and ICICI Prudential collectively dominating the life bancassurance segment through their relationships with India's largest banking institutions. Competition is increasingly fought on the dimensions of digital platform integration, product diversity, and rural distribution reach rather than pure commission economics.

Emerging InsurTech players and API-led insurance infrastructure platforms are entering the value chain as technology enablers, helping both banks and insurers deliver faster, more personalized products without overhauling legacy systems. Regulatory evolution by IRDAI, including proposals to cap parent bank shareholding in insurance subsidiaries, is pushing the competitive landscape toward a more open-architecture distribution model, which is expected to benefit well-positioned mid-tier insurance companies looking to access bank distribution channels on competitive terms.

Founded in 2000 and headquartered in Mumbai, India, HDFC Life Insurance Company Limited is a joint venture between HDFC Ltd and abrdn plc and one of India's most prominent private sector life insurers. The company distributed over 60% of its individual new business through bancassurance in FY2024, generating over Rs. 10,435 crore in bancassurance Annual Premium Equivalent. HDFC Life maintains 265 bancassurance partnerships spanning NBFCs, micro-finance institutions, small finance banks, and commercial banks, in addition to 39 non-traditional ecosystem partnerships. Its strong persistency rates, often reaching 90% at the 13-month mark, reflect the quality of its bancassurance-driven customer relationships. HDFC Life was one of the first private insurers to receive an IRDAI license in 2001.

Founded in 1911 and headquartered in Mumbai, India, Central Bank of India is one of India's oldest and largest public sector commercial banks. The bank distributes life and non-life insurance products through its extensive branch network spanning thousands of locations across India, with a strong presence in rural and semi-urban regions. As a public sector entity, Central Bank of India plays a significant role in furthering the government's financial inclusion agenda, channeling insurance products to customer segments typically underserved by private sector distribution. Its bancassurance operations support LIC and several other insurance partners through corporate agency arrangements, contributing to premium mobilization in geographies where private insurers have limited direct reach.

Founded in 1956 and headquartered in Mumbai, India, the Life Insurance Corporation of India is the country's largest state-owned life insurer and the dominant force in India's insurance sector. LIC commands approximately 32% of the private and public insurance market and has been steadily expanding its bancassurance footprint through corporate agency agreements with both public and private sector banks. In 2024, LIC signed a bancassurance partnership with IDFC First Bank, enabling access to over one crore bank customers. In October 2025, it formalized a similar agreement with RBL Bank. LIC's brand recognition, sovereign backing, and widespread trust among rural and semi-urban customers make it the preferred insurance partner for banks targeting financial inclusion-oriented customer segments.

Founded in 1956 and headquartered in Mumbai, India, the Life Insurance Corporation of India is the country's largest state-owned life insurer and the dominant force in India's insurance sector. LIC commands approximately 32% of the private and public insurance market and has been steadily expanding its bancassurance footprint through corporate agency agreements with both public and private sector banks. In 2024, LIC signed a bancassurance partnership with IDFC First Bank, enabling access to over one crore bank customers. In October 2025, it formalized a similar agreement with RBL Bank. LIC's brand recognition, sovereign backing, and widespread trust among rural and semi-urban customers make it the preferred insurance partner for banks targeting financial inclusion-oriented customer segments.

Other key players in the market are Aditya Birla Capital Ltd., Briisk Limited, The New India Assurance Co. Ltd., Bank of Maharashtra, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Discover the latest insights on the India Bancassurance Market 2026 with our comprehensive report. Stay informed on distribution model shifts, InsurTech-driven disruption, regulatory developments, and the regions recording the strongest insurance penetration growth. Whether you are a bank exploring new revenue channels, an insurer optimizing your distribution strategy, or an investor evaluating India's BFSI opportunity, this report equips you with the data you need. Download your free sample today and explore the key opportunities within India's rapidly expanding bancassurance sector.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market reached an approximate value of USD 116.08 Billion.

The market is projected to grow at a CAGR of 6.10% between 2026 and 2035.

The key strategies of the market are the surging government support, rise in Insurtech and bank partnerships, increased integration of mobile banking, rising digitalisation and focus on cybersecurity.

The pure distributor model will gain ground with the rising scope for insurance companies to pay commissions to the bank in the form of management fees.

The major players in the market are HDFC Life Insurance Company Limited, Central Bank of India, PNB MetLife India Insurance Company Limited, Life Insurance Corporation of India, Aditya Birla Capital Ltd., Briisk Limited, The New India Assurance Co. Ltd., Bank of Maharashtra, and others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Product Type |

|

| Breakup by Model Type |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.