Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

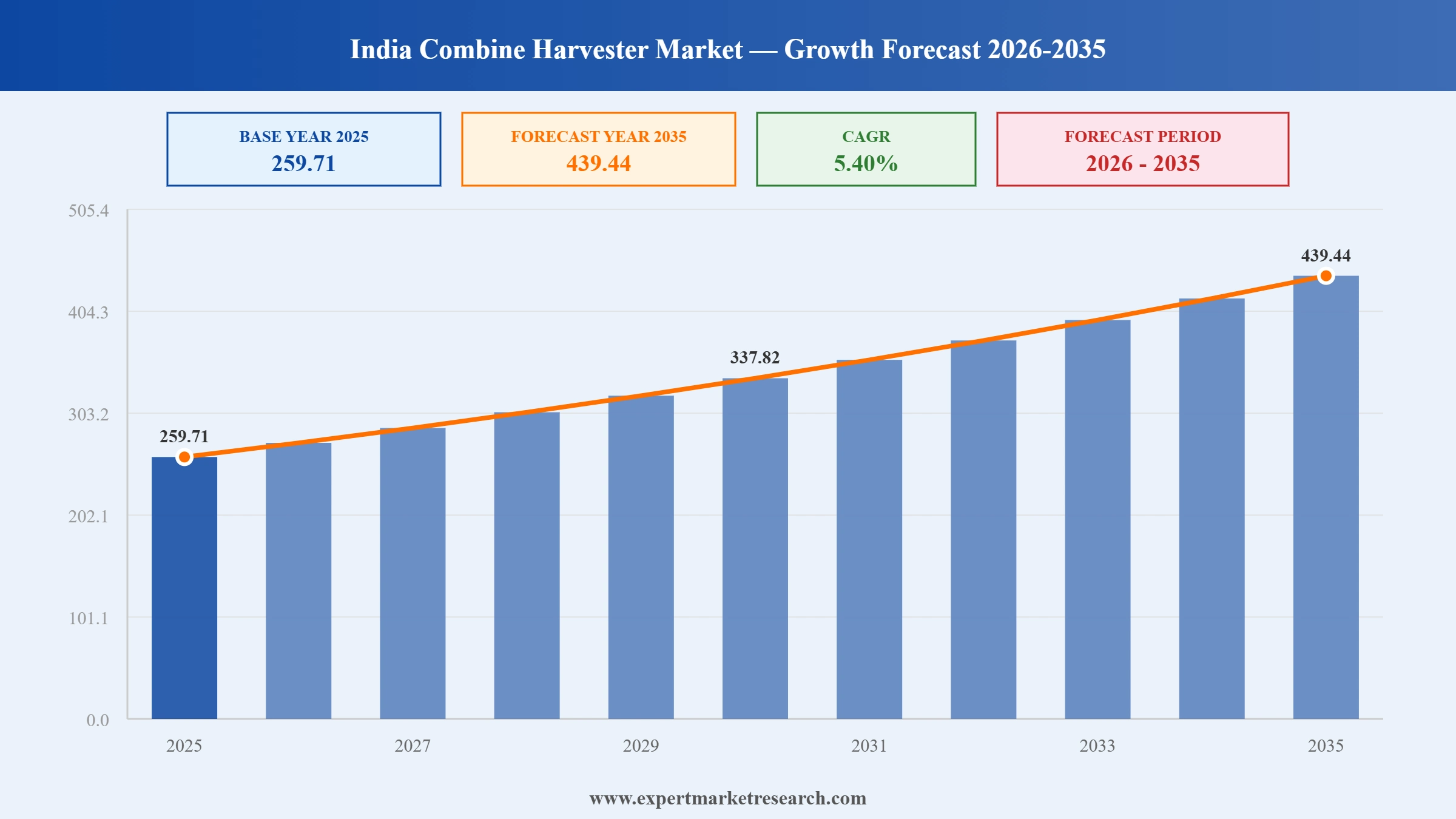

The India Combine Harvester Market reached a value of USD 259.71 Million at 2025 and is projected to expand at a CAGR of around 5.40% during the forecast period of 2026-2035. With rising agricultural labor costs driving mechanisation demand across India's grain-producing states, strong government support through SMAM subsidies and state mechanisation schemes accelerating equipment adoption, expanding custom hiring center networks broadening access among small landholders, and technological advancements embedding precision agriculture and telematics capabilities into new combine models, the market is expected to reach USD 439.44 Million by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

|

India Combine Harvester Market Report Summary |

Description |

Value |

|

Base Year |

USD Million |

2025 |

|

Historical Period |

USD Million |

2019-2025 |

|

Forecast Period |

USD Million |

2026-2035 |

|

Market Size 2025 |

USD Million |

259.71 |

|

Market Size 2035 |

USD Million |

439.44 |

|

CAGR 2019-2025 |

Percentage |

XX% |

|

CAGR 2026-2035 |

Percentage |

5.40% |

|

CAGR 2026-2035 - Market by Region |

North India |

5.8% |

|

CAGR 2026-2035 - Market by Region |

South India |

5.4% |

|

CAGR 2026-2035 - Market by Type |

Self-Propelled |

6.9% |

|

2025 Market Share by Region |

North India |

32.4% |

India's combine harvester market is being reshaped by four concurrent forces: government-driven mechanization at an accelerating pace, the proliferation of custom hiring centers democratising equipment access, the integration of precision agriculture and smart telematics into mainstream combine products, and the growing adoption of multi-crop capable designs addressing the diverse harvesting requirements of India's geographically varied agricultural landscape.

Escorts Kubota Limited announced a major capital investment of INR 4,500 crore (approximately USD 540 million) to establish a new agricultural and construction machinery manufacturing facility near Jewar Airport, Uttar Pradesh in February 2025, with land acquisition actively in progress. The company additionally allocated INR 400 crore for capital expenditure in FY 2025-26, with 75% of that amount designated for product development and 25% for improvements at existing manufacturing facilities. The Jewar facility investment signals Escorts Kubota's strategic intent to expand domestic production capacity for both tractors and agricultural equipment including combine harvesters, aligning with the broader government and industry push to increase local manufacturing of farm machinery under the Make in India initiative.

Yanmar Holdings Co., Ltd. completed the acquisition of CLAAS India Private Limited through its group business, Yanmar Coromandel Agrisolutions Private Limited, in January 2025, renaming the entity Yanmar Agricultural Machinery India Private Limited (YAMIN), effective November 20, 2024. The Morinda, Punjab facility acquired through this transaction specialises in manufacturing combine harvesters and associated attachments for both domestic distribution and international markets. The acquisition represents a significant structural shift in India's combine harvester competitive landscape, as CLAAS was one of the most recognised brands in the Indian market. Yanmar's entry into combine harvester manufacturing in India through this transaction strengthens its position in the agricultural machinery segment and expands its India market presence beyond its existing tractor and transplanter operations.

Kubota Corporation unveiled its latest combine harvester model, the Pro 588i-G, at the Krishi Darshan Expo 2025 held in Hisar, showcasing the machine as a purpose-built solution for simplifying and improving the harvesting process for Indian farmers. The Pro 588i-G is specifically designed for wheat and paddy crop harvesting, making it well suited to the dominant crop calendar of India's northern grain belt, particularly Punjab, Haryana, and Uttar Pradesh. The launch reflects Kubota's continued investment in India-specific combine harvester development, where product localisation around crop type, terrain conditions, and operator accessibility is a critical commercial requirement. The Krishi Darshan Expo platform provided Kubota with direct engagement with agricultural contractors, custom hiring operators, and progressive farmers who represent the primary purchasing channels for combine harvesters in India.

Mahindra and Mahindra Ltd increased its equity holding in Sampo Rosenlew Oy, its Finland-based agricultural machinery affiliate, to 100% by exercising a call option and acquiring residual shares for more than INR 35 crore. The acquisition of complete ownership of Sampo Rosenlew, which is a recognised European combine harvester manufacturer, strengthens Mahindra's access to advanced harvester technology, engineering capabilities, and export market positioning in the combine harvester segment. Sampo's product expertise in high-performance combine harvester design is expected to enhance Mahindra's India product development pipeline for combine harvesters, supporting the company's competitive positioning as the India combine harvester market growth narrative increasingly rewards manufacturers with proven precision agriculture and harvesting technology credentials.

The Bureau of Indian Standards implemented its 2024 safety order for agricultural machinery, including combine harvesters, in 2025, raising the compliance requirements for both domestic manufacturers and importers operating in India's combine harvester segment. The new standards favour manufacturers with certified production facilities and established quality management systems, effectively raising entry barriers for smaller assemblers and unorganised players who lack the capital and process infrastructure to meet the updated certification criteria. The compliance requirements are expected to accelerate market consolidation as larger and more technologically capable players, including Mahindra, Escorts Kubota, John Deere, and Preet Group, maintain and potentially strengthen their market share by leveraging their certified manufacturing credentials as a competitive differentiator in both OEM and custom hiring supply channels.

India's agricultural mechanization rate climbed from 40% in 2022 to 47% in 2024 and is targeting over 60% by 2025 under Ministry of Agriculture estimates, a trajectory directly supported by the Sub-Mission on Agricultural Mechanisation (SMAM) that provides subsidies and financial assistance for combine harvester purchases by individual farmers, farmer producer organizations, and custom hiring centers. State governments have amplified these efforts through complementary schemes, with states including Andhra Pradesh and Uttar Pradesh deploying combine harvesters through mechanization flagship programmes. Punjab and Haryana, already at 75% mechanization, continue to upgrade their fleets toward higher-horsepower and smarter models, while emerging states including Madhya Pradesh, Chhattisgarh, and Odisha are at the fastest growth stage of mechanization adoption, making them priority deployment targets for both government programmes and India combine harvester market growth strategies of manufacturers.

The expansion of the custom hiring center (CHC) model across India is fundamentally democratising access to combine harvesters by allowing small and marginal farmers, who constitute the majority of India's farm operator base, to access mechanised harvesting on a per-acre charge basis without the capital commitment of machine ownership. Custom hiring operators now represent a major and rapidly growing buyer segment for new combine harvesters, and their fleet procurement decisions are driving meaningful volume into the market in states where individual farmer purchasing power is limited. Manufacturers including Mahindra and Escorts Kubota are actively bundling financing, telematics subscriptions, and extended warranty packages with CHC fleet contracts, creating recurring revenue relationships and ensuring after-sales service engagement. The government's CHC establishment programme under SMAM includes capital subsidy support for CHC formation, directly accelerating the CHC model's reach into India's combine harvester market trends landscape across previously underserved eastern and central agricultural states.

Technology integration is rapidly moving from a premium differentiator to a baseline commercial requirement in India's combine harvester market, as buyers increasingly evaluate machines on the strength of their telematics, remote diagnostics, yield monitoring, and precision agriculture capabilities alongside traditional mechanical performance metrics. John Deere's JDLink ecosystem, which enables remote monitoring, predictive maintenance, and yield mapping, has established a high-technology benchmark that domestic manufacturers are progressively responding to through their own digital platform investments. Mahindra's mobile service vans now preload parts based on telematics alerts, reducing harvesting season downtime for custom hiring operators who depend on maximum machine uptime during tight harvest windows. Escorts Kubota is pursuing autonomous agricultural robotics platforms that could integrate harvester attachments within five years, reflecting the longer-term direction of the India combine harvester market forecast toward precision and connected equipment.

India's combine harvester market has historically been concentrated in wheat and paddy cultivation zones of Punjab, Haryana, and Uttar Pradesh, but the growing availability of multi-crop combine harvesters is expanding the addressable market into soybean, mustard, chickpea, sorghum, and finger millet growing regions across Madhya Pradesh, Rajasthan, Maharashtra, and Karnataka. Manufacturers including Preet Group and Kartar Agro have developed multi-crop header designs and combine platforms that can be reconfigured across crop types within a single season, allowing custom hiring operators to maximise asset utilisation beyond the narrow wheat and paddy harvest windows. The ICAR has confirmed that harvesting and threshing mechanisation for crops excluding rice and wheat stands at only 32%, indicating the significant untapped demand available as India combine harvester market outlook models account for multi-crop penetration accelerating through the forecast period across the country's diverse agro-ecological zones.

The Expert Market Research's report titled "India Combine Harvester Market Report and Forecast 2026 to 2035" offers a detailed analysis of the market based on the following segments:

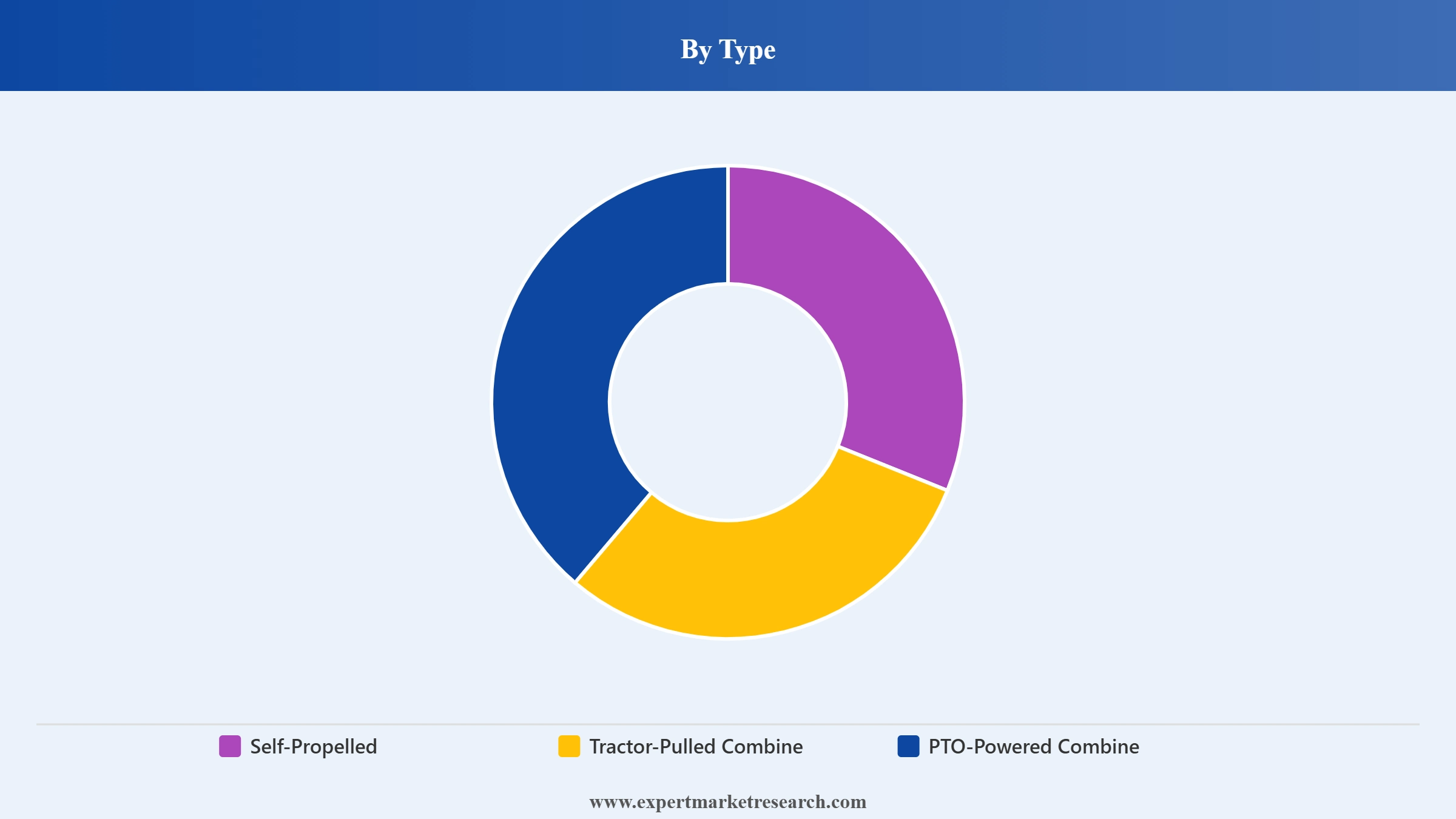

Market Breakup by Type

Key Insight: Self-Propelled combine harvesters represent the dominant product category in the India Combine Harvester Market, commanding a leading position anchored by their superior operational efficiency, high harvesting throughput, and suitability for large-scale wheat and paddy cultivation across the northern grain belt states of Punjab, Haryana, and Uttar Pradesh where farm mechanization already exceeds 75%. Their independence from tractor power requirements makes them the preferred choice for large commercial farmers and professional custom hiring contractors who prioritise maximum field capacity per machine hour. Tractor-Pulled Combines hold a meaningful and growing market share, driven by their significantly lower acquisition cost compared to self-propelled alternatives, which makes them accessible to smaller farm operators and custom hiring centers in states with more fragmented landholding structures. This category directly benefits from India's large installed tractor base and the government's tractor financing and subsidy programmes, which create a companion demand for tractor-compatible combine attachments. PTO-Powered Combine Harvesters are gaining momentum in hilly, remote, and geographically constrained regions, including the Northeastern states and certain Himalayan foothills districts, where their compact form factor and lightweight configuration allow harvesting operations on smaller and more irregular field geometries that larger self-propelled platforms cannot effectively serve.

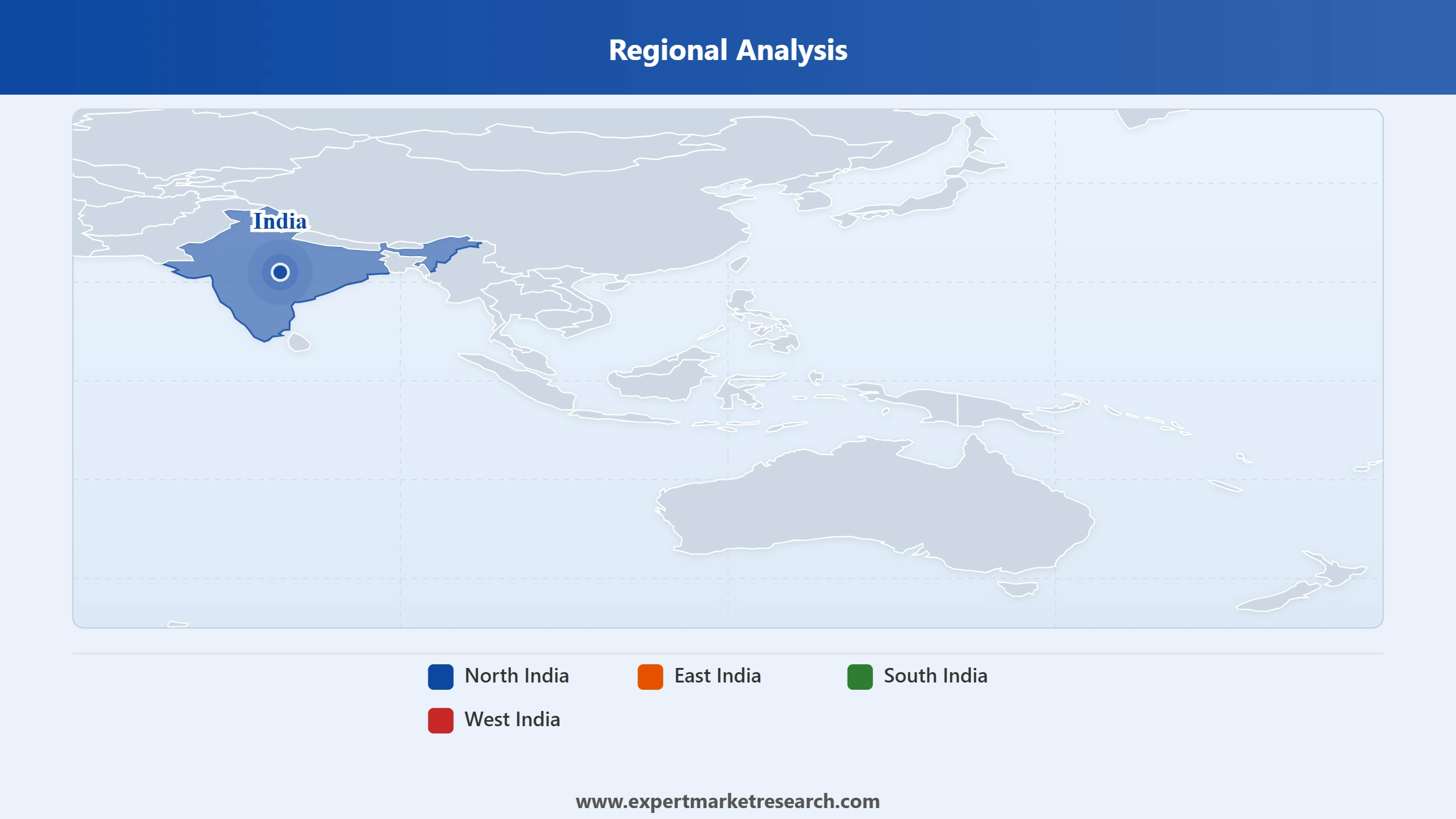

Market Breakup by Region

Key Insight: North India is the dominant regional market for combine harvesters, anchored by Punjab and Haryana, which together constitute the epicentre of India's mechanised grain harvesting activity. With mechanization rates exceeding 75% in these two states and an established culture of commercial custom hiring that migrates harvesting teams and machines southward through the wheat-paddy harvest season, North India generates a disproportionate share of both new equipment purchases and replacement demand. Uttar Pradesh is also a major and expanding contributor to the regional market, with its enormous cultivation area for wheat, paddy, and sugar crops creating sustained demand for both self-propelled and tractor-pulled combine types. East India is an emerging market undergoing rapid mechanization acceleration in states including West Bengal, Odisha, Bihar, and Assam, where rising paddy cultivation areas and improving rural infrastructure are creating growing deployment opportunities for PTO-powered and tractor-pulled combines suited to smaller and more fragmented field conditions. South India is the fastest-growing regional market, supported by favorable paddy and commercial crop cultivation conditions in Karnataka, Tamil Nadu, Andhra Pradesh, and Telangana, state-level mechanisation investment, and the increasing participation of progressive farmers in formal equipment purchase and leasing channels. West India is growing through Maharashtra and Gujarat, where commercial farming of soybean, wheat, and oilseeds generates meaningful demand for multi-crop capable harvesting equipment.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Self-Propelled combine harvesters hold a commanding share of the India Combine Harvester Market, reflecting their dominant adoption across the commercially critical wheat and paddy harvesting markets of Punjab, Haryana, and Uttar Pradesh. The category's leadership is reinforced by the custom hiring center model, through which professional operators deploy self-propelled machines across multiple farms and states during each harvest season, driving asset utilisation and justifying the higher capital outlay compared to tractor-pulled alternatives. Self-propelled machines are also the primary beneficiary of technological upgrades toward telematics, precision agriculture, and smart yield monitoring, as their larger scale and professional operator base support investment in digital value-added services.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Tractor-Pulled Combines represent the second-largest type segment, serving the price-sensitive mass-market tier where tractor compatibility reduces the effective incremental cost of mechanised harvesting for smaller and mid-size operators. This category is strategically important for market volume expansion into states outside the Punjab-Haryana-UP belt, where farm structures are more fragmented and individual farmer purchasing power requires more affordable equipment solutions. North India dominates the regional landscape, but South India is the fastest-growing region, generating accelerating demand driven by expanding paddy cultivation and state government mechanization investments that are bringing combine harvester adoption into states where manual harvesting still prevails. East India represents the most significant volume growth opportunity on the horizon as mechanisation penetration in West Bengal, Odisha, and Bihar remains low relative to their agricultural scale.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

North India is the most commercially developed regional market in India's combine harvester industry, with Punjab and Haryana functioning as the country's primary hub of mechanised grain harvesting activity. These states, with mechanization rates above 75%, have a mature and sophisticated combine harvester ecosystem characterised by well-established custom hiring networks, experienced operators, and strong after-sales service infrastructure from all major manufacturers. Uttar Pradesh provides the region with additional volume through its vast wheat and paddy cultivation acreage, and the state's improving road connectivity and cold storage infrastructure are supporting the commercial expansion of custom hiring operations into previously underserved districts. North India's established mechanization culture also creates a secondary market effect: custom hiring teams migrate from Punjab and Haryana toward central and eastern states during the inter-season period, carrying harvesting capacity to regions that have not yet developed a comparable local CHC base.

South India is the fastest-growing regional market, where paddy and commercial crop cultivation across Karnataka, Tamil Nadu, Andhra Pradesh, and Telangana provides a growing demand base for combine harvesters as state governments increase mechanization subsidies and awareness campaigns. The region's agro-climatic diversity, including lowland paddy zones in the Cauvery and Krishna deltas and upland commercial crop regions across the Deccan Plateau, creates demand for both self-propelled combines suited to lowland operations and tractor-pulled configurations suited to more varied terrain. Progressive farmer adoption of multi-crop combines in South India is expanding the harvesting season beyond the primary paddy harvest, improving asset utilisation for CHC operators and making equipment investment economics more favourable. South India's growing agricultural technology adoption, supported by digital connectivity and exposure to precision farming practices through agri-tech startups, is also creating a receptive environment for smart telematics-equipped combine models from manufacturers including John Deere and Escorts Kubota.

The India Combine Harvester Market features a moderately concentrated competitive structure, with international manufacturers including Claas (through Yanmar's YAMIN entity), John Deere, Kubota, and CNH Industrial competing alongside strong domestic and domestically anchored players such as Mahindra, Preet Group, and SAME Deutz-Fahr. Market leaders leverage economies of scale, certified manufacturing credentials under the Bureau of Indian Standards 2024 safety order, extensive dealer and service networks, and government program relationships to maintain competitive advantages. Technology differentiation through telematics, precision agriculture integration, and multi-crop capability is rapidly reshaping competitive positioning beyond pure price competition.

Domestic challengers including Preet Group and Iseki compete through cost-effective platforms, strong regional dealer relationships, and competitive financing options that serve the price-sensitive mass-market segment, particularly in states outside the established Punjab-Haryana belt. The CHC model has added a new competitive dimension, with manufacturers bundling financing, warranties, and telematics packages to secure long-term fleet supply relationships with professional custom hiring operators who now represent a material share of annual combine harvester demand.

Founded in 1913 and headquartered in Harsewinkel, Germany, Claas is one of the world's leading agricultural machinery manufacturers with particular strength in combine harvesters. In India, Claas operated through Claas India Private Limited until January 2025, when the entity was acquired by Yanmar Holdings Co., Ltd. and renamed Yanmar Agricultural Machinery India Private Limited (YAMIN). The Morinda, Punjab manufacturing facility continues to produce combine harvesters and attachments for domestic and international markets under the new ownership. Claas's legacy product portfolio in India includes the Crop Tiger series, which holds a recognised position for its performance in multi-crop and difficult tangled crop conditions, and is widely used by custom hiring operators across North and Central India.

Founded in 1945 and headquartered in Mumbai, Mahindra is India's largest agricultural machinery conglomerate and operates in the combine harvester segment through its Swaraj Division. The company increased its ownership in Sampo Rosenlew Oy, a Finnish combine harvester manufacturer, to 100% in 2025 through the exercise of a call option, securing full access to European harvester technology and engineering capabilities. Mahindra's competitive advantage in combine harvesters is built on the country's densest agricultural equipment service network, which ensures minimal downtime during critical harvest periods. Its mobile service vans equipped with predictive maintenance capabilities further strengthen its service proposition to professional custom hiring operators who prioritise machine uptime over acquisition price.

Founded in 1890 and headquartered in Osaka, Japan, Kubota operates in the Indian combine harvester market through Escorts Kubota Limited, formed through the merger of Escorts Limited and Kubota's Indian operations. In February 2025, Escorts Kubota committed INR 4,500 crore to a new manufacturing facility near Jewar Airport, Uttar Pradesh, signalling a major capacity expansion intent for agricultural machinery including combine harvesters. The company unveiled its Pro 588i-G combine harvester at the Krishi Darshan Expo 2025 in Hisar, targeting wheat and paddy harvesting applications in the northern grain belt. Escorts Kubota is also investing in autonomous agricultural robotics platforms that could integrate modular harvester attachments within a five-year horizon.

Founded in 1837 and headquartered in Moline, Illinois, Deere and Company operates in India through John Deere India Pvt. Ltd., headquartered in Pune, manufacturing tractors, harvesters, and implements since 1998. John Deere is recognised as the technology leader in India's combine harvester market through its JDLink ecosystem, which provides remote monitoring, predictive maintenance alerts, yield mapping, and cloud-based performance analytics. The company commands a leading position in the high-technology premium segment, where its AI-based in-field optimisation and precision agriculture capabilities justify premium pricing among large-acreage commercial farms and well-capitalised custom hiring operators. John Deere's Right-to-Repair restriction model, while commercially effective, has generated some friction among independent repair operators in India's aftermarket.

Other key players in the market are Yanmar Co. Ltd, AGCO Corporation, Iseki & Co. Ltd, CNH Industrial NV, Preet Group, and SAME Deutz-Fahr S.p.A., and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

The India Combine Harvester Market is entering a new phase of growth, shaped by India's accelerating mechanisation agenda, a technology-driven competitive transformation, and the emergence of the custom hiring model as the dominant go-to-market channel for the next phase of adoption. Our comprehensive analysis of the India Combine Harvester Market 2026 equips you with the intelligence to navigate government policy changes, identify the highest-growth type and regional sub-markets, assess the competitive strategies of Claas, Mahindra, Kubota, and John Deere, and build a data-driven strategy for this expanding agricultural machinery opportunity. Download your free sample now.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the India combine harvester market reached an approximate value of USD 259.71 Million.

The market is projected to grow at a CAGR of 5.40% between 2026 and 2035.

The market is estimated to witness healthy growth in the forecast period of 2026-2035 to reach a value of around USD 439.44 Million by 2035.

The major drivers of the market are the increased awareness of climate-resilient farming, adoption of efficient management practices, and the rising accessibility to rural credit.

The key trends of the market include the evolution of multi-crop combine harvesters, expansion of Custom Hiring Centers (CHCs), integration of smart and precision technology, and the local components and indigenous manufacturing.

The major regions in the market are North India, East India, South India, and West India.

The various types considered in the market report are self-propelled, tractor-pulled combine, and PTO-powered combine.

The major players in the market are Claas KGaA GmbH, Mahindra & Mahindra Ltd, Kubota Corporation, Deere & Company, Yanmar Co. Ltd, AGCO Corporation, Iseki & Co. Ltd, CNH Industrial NV, Preet Group, and SAME Deutz-Fahr S.p.A., among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Type |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.