Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

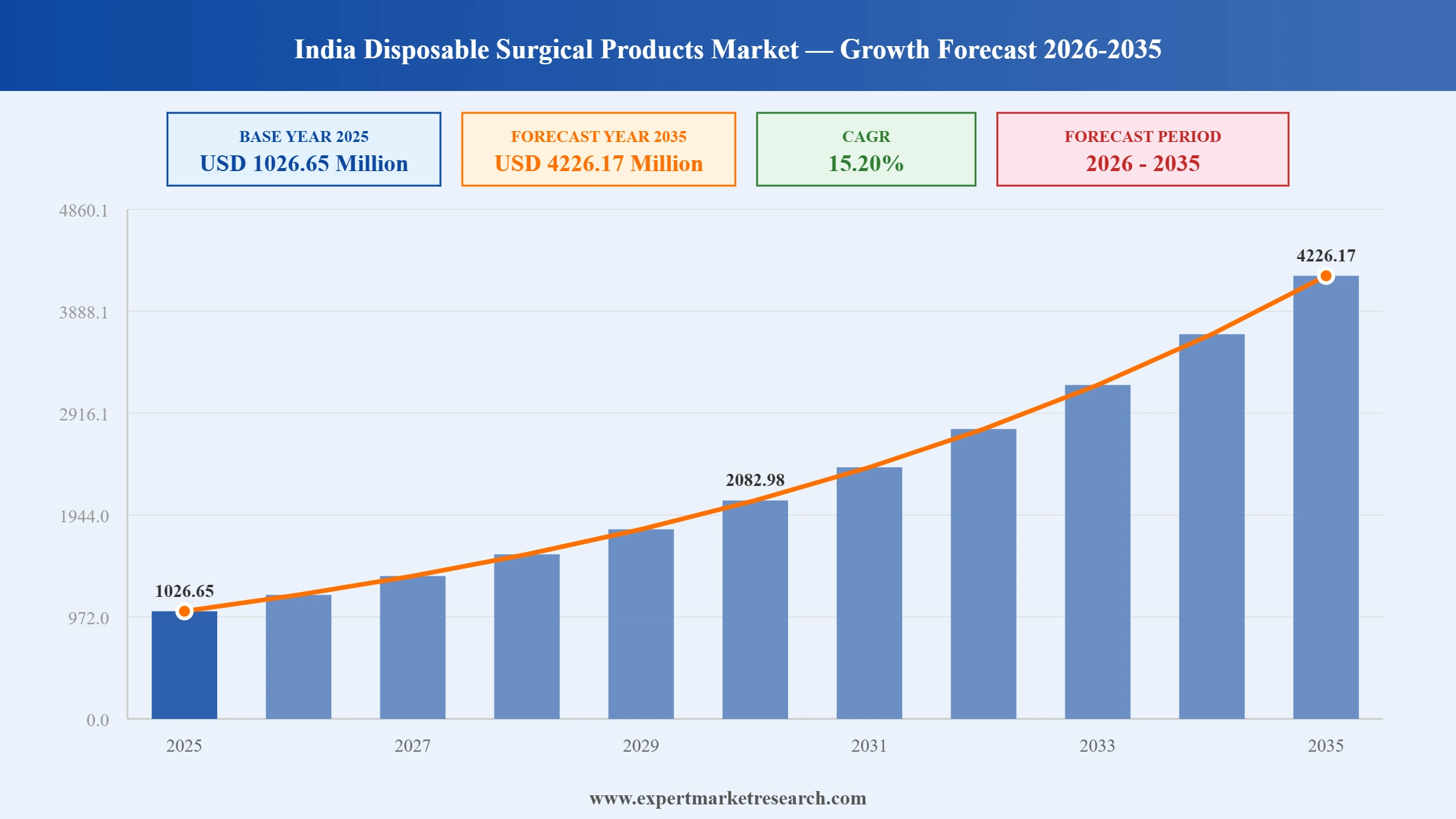

The India disposable surgical products market reached a value of USD 1026.65 Million at 2025 and is projected to expand at a CAGR of around 15.20% during the forecast period of 2026-2035. Lifted by the April 2024 Ministry of Health mandate on reuse-prevention syringes, accelerating Ayushman Bharat coverage, a building wave of private hospital construction across secondary cities, and a domestic manufacturing sector scaling fast under PLI scheme incentives, the market is expected to reach USD 4226.17 Million by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

India's disposable surgical products market is going through a regulatory-led inflection. Government policy is converting previously discretionary purchasing into mandated specifications, multinational and domestic manufacturers are racing to scale local production, and the mix shift toward safety-engineered products is rewriting unit economics across the entire category. The pace of change over the past 18 months is faster than at any point in the segment's recent history.

In January 2025, Becton Dickinson announced investments exceeding USD 10 million in its broader manufacturing network for critical medical devices including disposable syringes, needles, and IV catheters, with an additional USD 30 million planned across 2025. The capacity buildout directly affects how quickly BD can serve high-growth markets like India, where its premium positioning depends on supply reliability alongside clinical performance differentiation.

Nipro Corporation, one of Japan's largest medical device companies, opened a new manufacturing unit in India in January 2025 through its Nipro India Corporation subsidiary. India's syringe market is one of the highest-volume markets in Asia Pacific, and producing locally rather than importing from Japan reduces landed cost, improves supply chain responsiveness, and positions Nipro for high-volume immunisation tenders that increasingly specify domestic manufacturing.

In April 2024, India's Ministry of Health issued a national regulation requiring the use of reuse-prevention syringes across all government hospitals. The mandate eliminated the lower-cost conventional syringe from government procurement and raised the average unit value of public tenders significantly. The policy is the single most consequential regulatory event for the India disposable surgical products market in this decade.

In March 2024, Hindustan Syringes and Medical Devices launched Dispojekt, an indigenous single-use safety syringe with an integrated needle designed to retract automatically after use. HMD invested approximately Rs 70 crore in Phase 1 manufacturing, with a stated target of 200 million syringes annually and an explicit ambition for a 60 to 70% share of India's safety syringe segment over the following three years.

The 15.20% CAGR is largely a story of regulatory architecture converting discretionary procurement into mandated procurement. The April 2024 safety syringe mandate is the clearest case, but it sits within a broader policy arc covering Bio-Medical Waste Management Rules, infection control guidelines, and Ayushman Bharat accreditation requirements that all push hospitals toward higher disposable product adoption.

Safety syringes captured the dominant share of global disposable syringe revenue by 2024, and India is catching up rapidly. With safety syringes selling at 2 to 3 times the price of conventional equivalents, the mix shift is driving revenue growth meaningfully faster than volume growth alone would suggest across the India disposable surgical products market.

Blood banks and diagnostic labs are an often-overlooked driver of disposable consumable demand. India's blood banking infrastructure has expanded under National Blood Policy guidelines that mandate single-use equipment, and chains like Thyrocare, Dr Lal PathLabs, and Metropolis are scaling their collection networks aggressively, with each new collection point lifting glove, syringe, and cannula consumption.

India's medical tourism sector, recovering strongly since 2022, is raising the specification floor at hospitals catering to international patients. JCI accreditation and equivalent international standards require premium-grade single-use products, non-powdered surgical gloves with biocompatibility testing, and sterilised packaging, creating a profitable premium segment for global suppliers operating across the India disposable surgical products market.

India's Production Linked Incentive scheme for medical devices has supported capacity additions across syringe, glove, PPE, and cannula manufacturers. The export angle matters: manufacturing to export-quality standards forces producers to upgrade quality management systems and regulatory compliance infrastructure, which then improves the reliability of products sold to domestic hospitals as well.

The report by Expert Market Research titled "India Disposable Surgical Products Market Report and Forecast 2026-2035" offers a detailed analysis of the market based on the following segments:

Market Breakup by Type

Key Insight: Syringes are the volume anchor of the India disposable surgical products market. The country's immunisation programme alone, one of the world's largest by coverage ambition, consumes billions of syringe units a year before counting hospital therapeutic injections, blood draws, and diagnostic procedures. The safety versus conventional split within syringes is where the most commercially significant shift is happening, with safety syringes now having regulatory backing in the government channel and credible domestic manufacturing through HMD's Dispojekt. Surgical gloves are the second-largest category, with non-powdered gradually displacing powdered as international accreditation standards spread across the Indian hospital base. PPE kits, surgeon caps, nebuliser masks, and cannulas each serve distinct clinical functions and continue to grow alongside surgical volumes and respiratory disease burden.

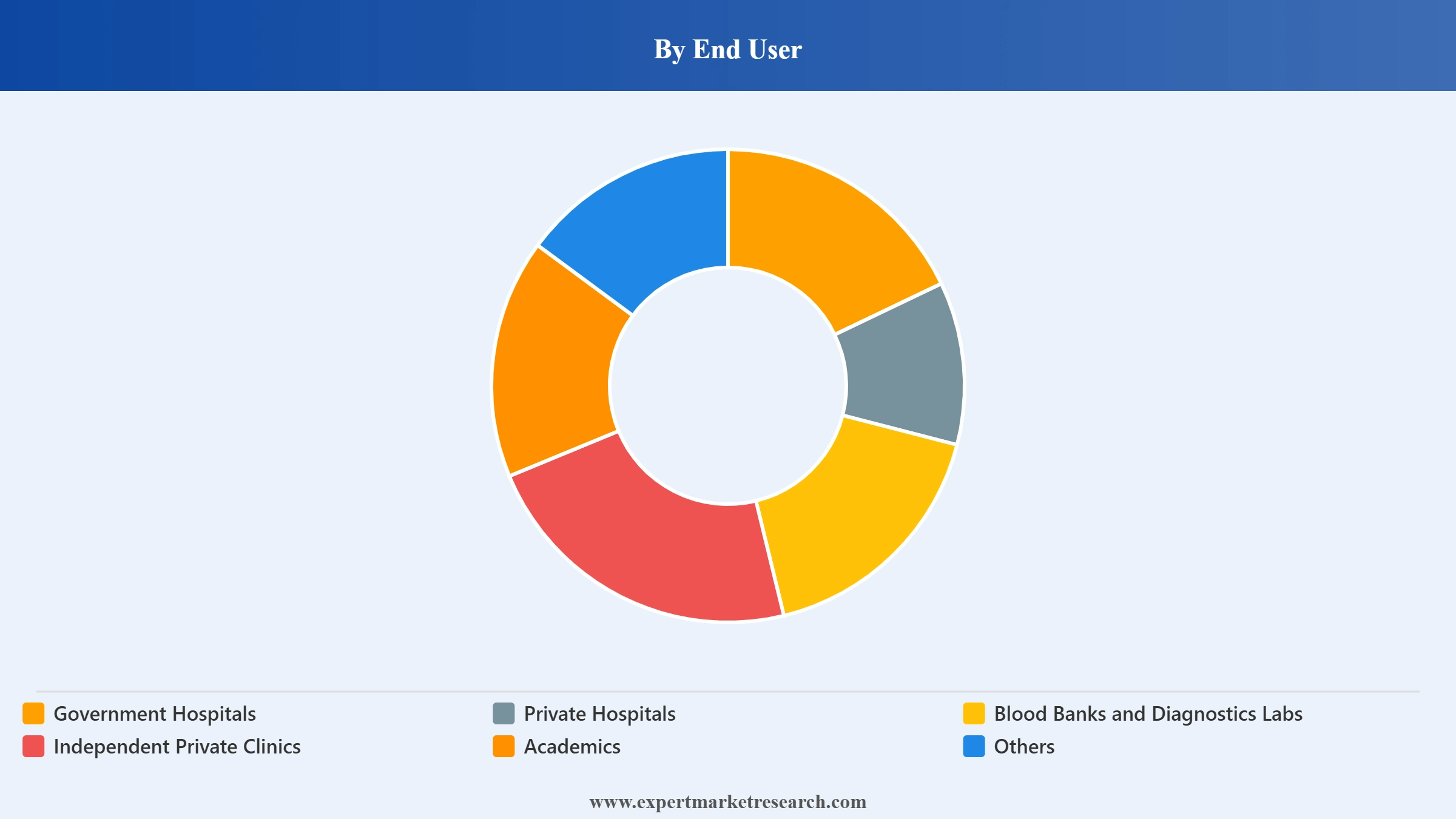

Market Breakup by End User

Key Insight: Government hospitals account for the largest procurement volume by a considerable margin, reflecting the scale of India's public healthcare system. Procurement is tender-driven, price-sensitive, and specification-determined by centrally issued guidelines, and the April 2024 safety syringe mandate transformed those tenders overnight. Private hospitals buy at higher unit prices but in more fragmented patterns. Blood banks and diagnostic labs together represent the fastest-growing end-user cluster proportionally, lifted by national chain expansion and consumable intensity per collection. Independent private clinics are numerous and geographically spread, making distributors rather than direct sales forces the economic way to serve them effectively across the India disposable surgical products market.

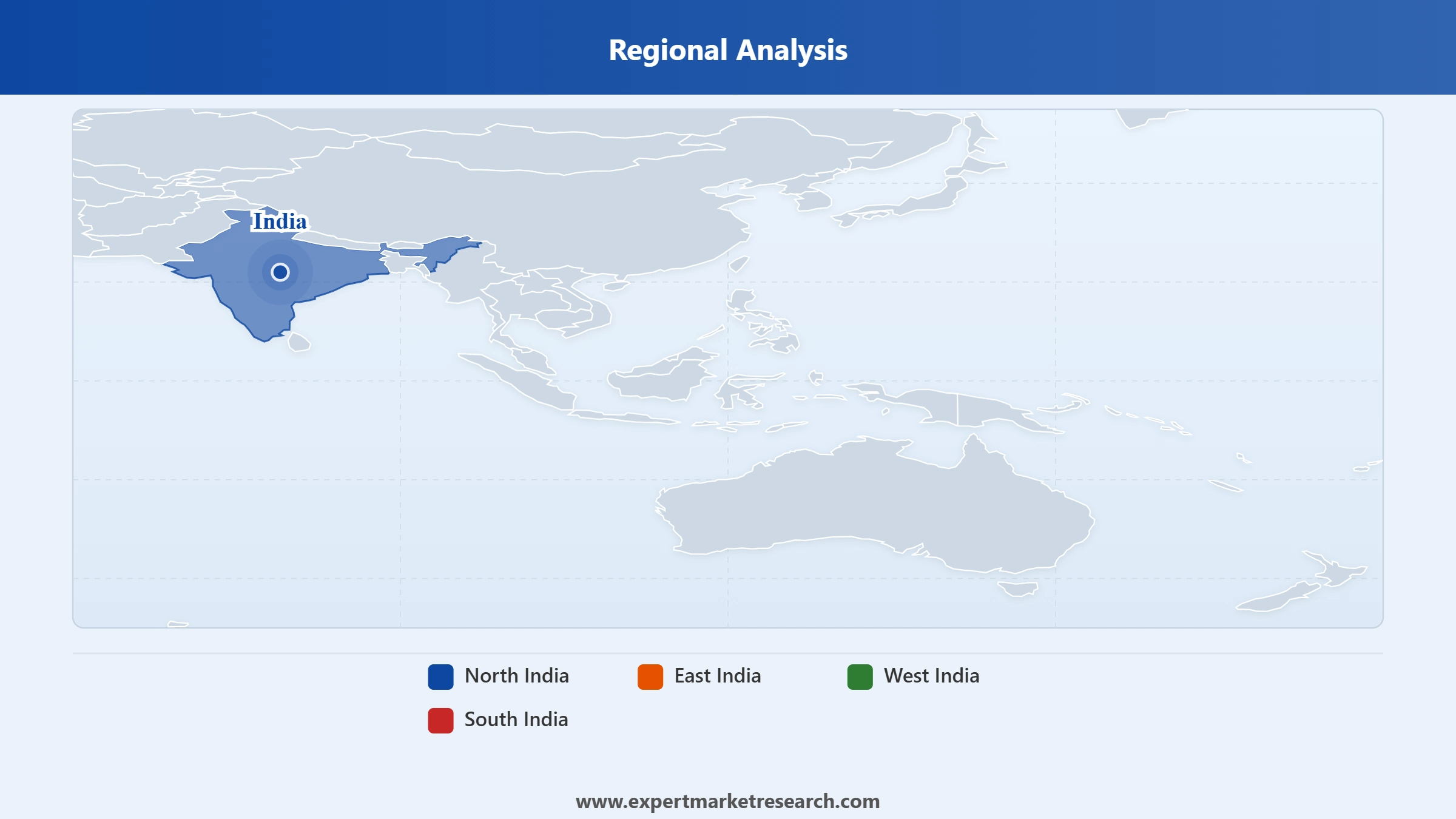

Market Breakup by Region

Key Insight: South India leads on private hospital quality and medical tourism intensity, making it the premium-product market within the country. Chennai's medical corridor, Hyderabad's growing hospital chains, and Bangalore's corporate healthcare infrastructure create a buyer base that specifies and pays for higher-grade disposables. North India, anchored by Delhi and the NCR's hospital density, combines large government procurement volumes with a significant private hospital base. West India, led by Maharashtra and Mumbai, is the commercial and manufacturing centre for several domestic disposable producers. East India historically lagged in healthcare infrastructure but is receiving disproportionate government investment to close regional disparities, making it the fastest-growing volume-grade market across the India disposable surgical products industry.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Type, Syringes dominate the market, with safety syringes lifting average revenue per unit across the category

Syringes account for the largest share of the India disposable surgical products market by revenue, and the mix shift toward safety syringes within that dominant category is raising average revenue per unit faster than volume growth alone would suggest. The April 2024 Ministry of Health mandate has effectively repriced the entire government channel, where a safety syringe retails at 2 to 3 times the price of a conventional equivalent. Hindustan Syringes' Dispojekt launch demonstrated that domestic manufacturers can produce safety syringes at competitive unit costs, removing the import dependency argument that previously slowed adoption.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Surgical gloves hold the second-largest share, with non-powdered gradually growing relative to powdered as clinical evidence against powder use strengthens and international accreditation requirements push procurement specifications in that direction. PPE kits remain a meaningful category post-pandemic as standard infection control rather than emergency response. Cannulas grow consistently alongside surgical volumes, while surgeon caps, pads, and nebuliser masks each track their respective clinical demand drivers across the broader India disposable surgical products industry.

By End User, Government Hospitals command the largest volume share, driven by public health system scale and Ayushman Bharat coverage

Government hospitals command the dominant volume share of the India disposable surgical products market, which reflects the scale of India's public healthcare system rather than any premium positioning. Procurement is centralised, tender-driven, and specification-led, and Ayushman Bharat's coverage of surgical procedures for over 500 million beneficiaries is steadily lifting the procedure volumes that drive disposable consumable demand. The April 2024 safety syringe mandate raised the average unit value of government purchases significantly, even at unchanged volume levels.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Private hospitals generate the highest revenue per procedure for suppliers because procurement is less price-compressed and specifications allow for premium product grades. Blood banks and diagnostic labs are the fastest-growing end-user segment proportionally, lifted by the expansion of national diagnostic chains and the consumable intensity of blood collection and processing. Independent private clinics serve the long tail of demand, particularly in tier-2 and tier-3 cities where the multinational and national distributor footprint is thinner but where the India disposable surgical products market still finds steady incremental volumes.

South India dominates the market due to premium private hospital infrastructure, JCI-accredited facilities, and medical tourism intensity

South India leads the India disposable surgical products market on the basis of premium product specifications, hospital quality, and medical tourism volumes. Chennai's medical corridor along Old Mahabalipuram Road, Hyderabad's growing hospital chains including Apollo and KIMS, and Bangalore's corporate healthcare infrastructure together create the country's most demanding buyer base for clinical disposables. Hospitals competing for medical tourists from the Middle East, Africa, and Southeast Asia require JCI-accredited or equivalent quality standards, which translates directly into premium-grade single-use product demand. International patients and their insurance carriers expect biocompatibility-tested non-powdered gloves, safety-engineered syringes, and sterilised packaging that meets international standards, and South Indian hospitals are willing to pay the price premium that comes with those specifications.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

East India is the fastest-growing region of the India disposable surgical products market, lifted by disproportionate government investment in closing regional healthcare disparities. New medical college hospitals, expanded district hospital capacity, and Ayushman Bharat empanelment rollouts across Bihar, Odisha, West Bengal, Jharkhand, and the northeastern states are creating fresh demand pipelines for volume-grade disposable consumables. The growth profile differs from South India: where the south anchors premium revenue, the east drives unit volume, and the combination of the two represents one of the more diversified country-level demand stories in Asia Pacific's medical consumables space.

The India disposable surgical products market has a bifurcated competitive structure that is more nuanced than a simple multinational versus local narrative would suggest. Multinationals like Becton Dickinson, B.Braun, Terumo, and Ansell compete primarily on product quality, clinical evidence, and relationships with premium private hospitals and medical tourism facilities. Domestic manufacturers like Hindustan Syringes and Pharmatrex compete on price, supply chain reliability, and government procurement relationships. A middle tier of mid-sized multinational subsidiaries operates across both customer segments depending on product category.

The April 2024 safety syringe mandate and the PLI scheme together are gradually shifting the competitive dynamics, particularly in syringes. Domestic manufacturers that can deliver safety syringes at government specification and unit cost are now competing for tender business that was previously import-dependent. The next three years will determine whether domestic players can maintain quality alongside the operational scale that India's public health system tenders require, with significant share implications across the India disposable surgical products industry.

Becton Dickinson is the global market leader in syringes and one of the most established multinational medical device companies in India. Its India portfolio spans conventional and safety syringes, IV catheters, needles, and diagnostic systems. The company competes at the premium end of the market with technologies like SafetyGlide, the BD Plastipak syringe range, and BD Neopak prefillable systems, and its January 2025 investment announcement reinforced its long-term commitment to manufacturing quality and supply reliability across high-growth markets.

B.Braun is a German multinational whose India operations cover infusion therapy, IV access, wound management, and surgical disposables. The company holds one of the broader product portfolios of any foreign player in the Indian hospital disposables space, which lets it serve hospitals as a partial or full-line supplier rather than a single-category vendor. Its cannula and infusion product range is particularly well-established in private hospitals, where European manufacturing standards and international accreditation credentials are valued.

Terumo is a Japanese company with strong positions in blood management and transfusion medicine alongside its syringe and IV catheter portfolio. In India, this dual positioning is strategically valuable: blood banks and transfusion centres are among the faster-growing end-user segments, and Terumo's blood bag and transfusion equipment expertise gives it natural access to those buyers alongside its hospital syringe business. The company competes at the quality-differentiated end of the market with India-specific product adaptations.

Teleflex operates in India primarily through vascular access, anaesthesia, and specialty surgical product lines, including cannulas and related vascular access devices. It is less of a broad hospital consumables player and more of a specialty company with deep expertise in clinical categories where its devices are specified by name in surgical protocols. This gives Teleflex a different competitive dynamic from volume-commodity players, with clinical adoption by anaesthesiologists, intensivists, and interventional specialists driving sales.

Other key players in the India disposable surgical products market include Nipro India Corporation Pvt. Ltd., Novo Nordisk India Pvt Ltd., Cardinal Health India Pvt. Ltd., Hindustan Syringes & Medical Devices Ltd., Baxter Pharmaceuticals India Pvt Limited (BPIPL), Ansell India Protective Products Pvt Ltd, Sempertrans India Pvt Ltd, Pharmatrex Healthcare Pvt Ltd, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Get the latest perspective on the India disposable surgical products market with our 2026 report. Track the rise of safety-engineered products, the regulatory tailwinds reshaping government procurement, and the segment-level shifts redefining demand across government and private hospitals, blood banks, and diagnostic labs. Whether you are a medical device manufacturer planning India entry, a domestic producer scaling under PLI incentives, or a healthcare investor evaluating consumables exposure, the report delivers the clarity you need. Download your free sample now and explore the opportunities reshaping the thriving India disposable surgical products industry.

Upto 15% Off

USD

$1999 $1799

$3099 $2789

$4599 $3909

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

The market is expected to grow at a CAGR of 15.20% between 2026-2035.

The market is driven by the growing rate in surgeries due to multiple medical conditions, the awareness of hygiene and safety amongst the masses, and improvements in healthcare infrastructure.

The key trends of the market include are the growing prevalence of wearing disposable surgical masks, increase in medical tourism, local production of disposable surgical products, and rising use of disposable products by blood banks and diagnostic labs.

Disposable surgical products are healthcare items that are typically used in surgeries and can only be used once in order to provide protection.

The various types of disposable surgical products in the market are syringes, surgical gloves, surgeon cap and pads, PPE kits, nebuliser mask, cannula, among others.

In blood banks, the use of gloves is critical because it acts like a shield protecting against direct contact with pathogens that might get transferred through blood.

The major end uses in the market are government hospitals, private hospitals, blood banks and diagnostics labs, independent private clinics, and academics, among others.

Surgical disposables are recommended to be thrown away after being used once as they can spread infections among patients and staff.

The major regions in the market for disposable surgical products in India are North India, East India, West India, and South India.

The key players in the market include Becton Dickinson Pvt. Ltd., B.Braun Medical India Pvt. Ltd., Terumo India Pvt Limited, Teleflex Medical Pvt Limited, Nipro India Corporation Pvt. Ltd., Novo Nordisk India Pvt Ltd., Cardinal Health India Pvt. Ltd., Hindustan Syringes & Medical Devices Ltd., Baxter Pharmaceuticals India Pvt Limited (BPIPL), Ansell India Protective Products Pvt Ltd, Sempertrans India Pvt Ltd, and Pharmatrex Healthcare Pvt Ltd.

At 2025, the market reached an approximate value of USD 1026.65 Million.

The market reaches USD 4226.17 Million by 2035, supported by mandatory safety syringe adoption across government hospitals, the Ayushman Bharat insurance coverage expansion pulling more patients into formal surgical settings, rapid growth in diagnostic and blood bank infrastructure, and a domestic manufacturing sector scaling up under PLI incentives.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Type |

|

| Breakup by End User |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 1,999

USD 1,799

tax inclusive*

Single User License

One User

USD 3,099

USD 2,789

tax inclusive*

Five User License

Five User

USD 4,599

USD 3,909

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.