Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

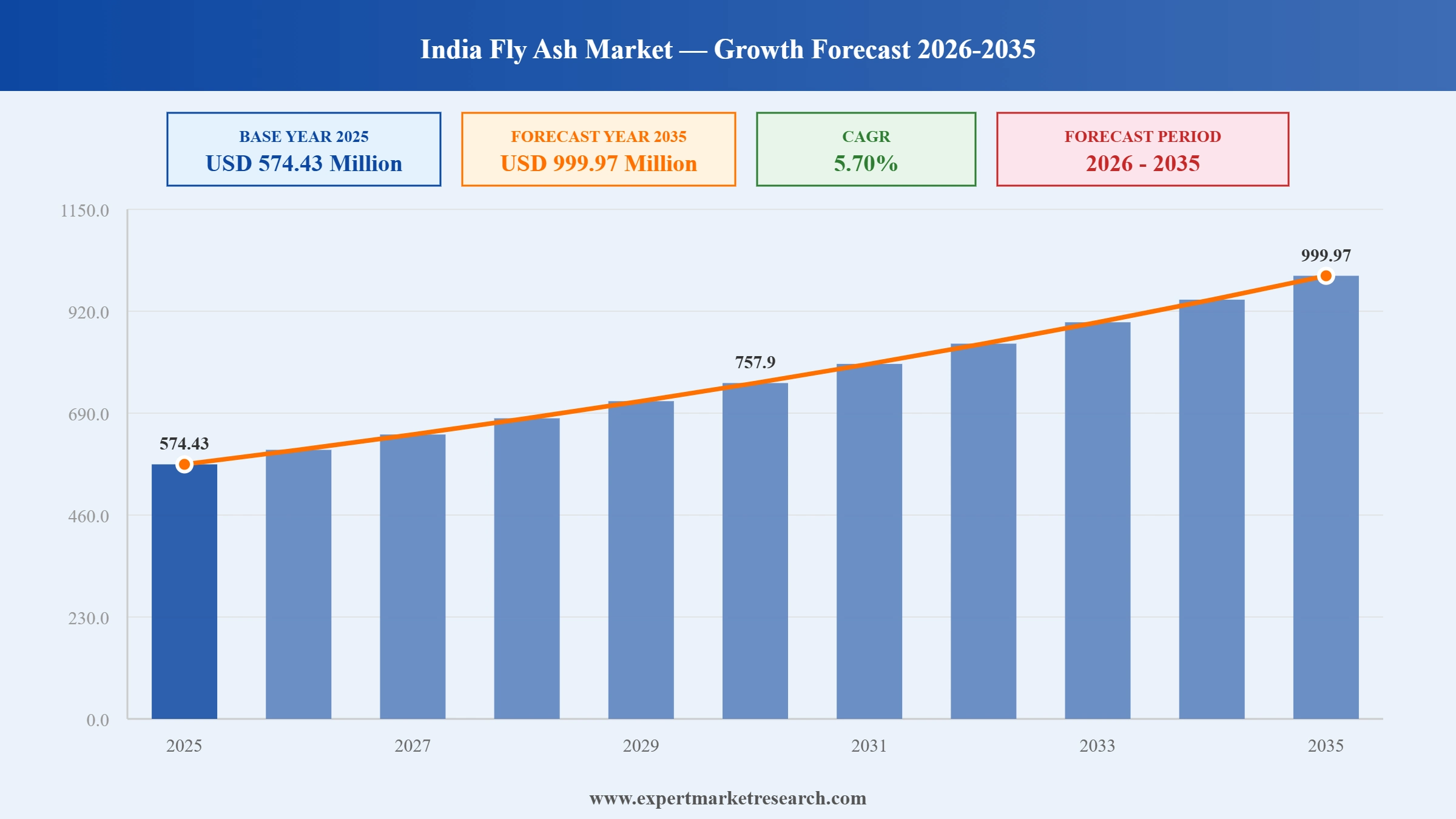

The India Fly Ash Market reached a value of USD 574.43 Million at 2025 and is projected to expand at a CAGR of around 5.70% during the forecast period of 2026-2035. With a booming construction sector, government mandates for fly ash utilisation, growing sustainable construction practices, and increasing adoption across agriculture, mining, and water treatment, the market is expected to reach USD 999.97 Million by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

|

India Fly Ash Market Report Summary |

Description |

Value |

|

Base Year |

USD Million |

2025 |

|

Historical Period |

USD Million |

2019-2025 |

|

Forecast Period |

USD Million |

2026-2035 |

|

Market Size 2025 |

USD Million |

574.43 |

|

Market Size 2035 |

USD Million |

999.97 |

|

CAGR 2019-2025 |

Percentage |

XX% |

|

CAGR 2026-2035 |

Percentage |

5.70% |

|

CAGR 2026-2035 - Market by Region |

South India |

6.5% |

|

CAGR 2026-2035 - Market by Region |

East India |

6.1% |

|

CAGR 2026-2035 - Market by Type |

Class F |

6.0% |

|

CAGR 2026-2035 - Market by Application |

Construction |

6.6% |

|

2025 Market Share by Region |

West India |

26.7% |

The India Fly Ash Market is being shaped by the intersection of regulatory mandates, infrastructure investment cycles, sustainability commitments by the cement industry, and expanding non-construction applications that are collectively elevating fly ash from an industrial by-product to a strategically valued circular economy material.

JK Lakshmi Cement launched Green Pro LC3, a sustainable blended cement product with approximately 40% lower CO2 emissions than Ordinary Portland Cement, commencing commercial shipments in February 2026. The product is designed for high-durability applications in marine environments and high-temperature construction projects. LC3, which combines calcined clay and limestone with clinker, typically incorporates fly ash as a supplementary cementitious component to enhance workability and reduce embodied carbon further. The launch reflects the broader industry shift toward decarbonised cement formulations and the central role that fly ash plays as a low-carbon ingredient in India's evolving blended cement portfolio.

NTPC Limited strengthened its fly ash distribution strategy in 2025 by deepening partnerships with cement manufacturers and leveraging Indian Railways for bulk fly ash transport, as part of its goal to achieve 100% fly ash utilisation across all its thermal power stations. NTPC's fly ash marketing model increasingly relies on long-distance rail logistics to bridge the geographic gap between eastern coal belt power plants - where the bulk of India's fly ash is generated - and cement plants concentrated in western and southern India. This logistics strategy is central to resolving the demand-supply mismatch that has historically left significant fly ash volumes unutilised in proximity-constrained markets.

In March 2024, NTPC Limited inaugurated a Fly Ash Based Light Weight Aggregate Plant at the Sipat Super Thermal Power Station in Bilaspur, Chhattisgarh, as part of a broader set of power projects worth over INR 30,000 crore dedicated by the Prime Minister. The facility, built at an investment of INR 51 crore, converts fly ash into lightweight aggregates through pelletizing and sintering technology. This high-value application for fly ash reduces landfill burden at one of India's largest thermal power stations while creating a building material with superior insulation and load-bearing properties compared to conventional aggregates. The plant directly advances India's 100% fly ash utilisation target.

Ambuja Cements paid Rs 413.75 crore to acquire a 1.5 MTPA cement grinding mill in Tuticorin, Tamil Nadu in 2024. Spanning 61 acres, the facility benefits from a long-term fly ash supply agreement that secures a consistent, cost-advantaged feedstock. The acquisition expands Ambuja's coastal footprint in southern Indian markets and bolsters its capacity to produce blended cement products incorporating fly ash as a partial clinker substitute. The deal reflects the strategic priority that major Indian cement companies place on securing reliable fly ash supply as they scale production of Portland Pozzolana Cement and other fly ash-blended variants to meet growing green construction demand.

Bharat Aluminium Company Limited (BALCO) signed a Memorandum of Understanding with Shree Cement Limited in 2024 to supply 90,000 metric tonnes of fly ash for use in low-carbon cement production. The agreement facilitates the responsible bulk utilisation of fly ash generated at BALCO's power operations, diverting the material from disposal to productive industrial use. For Shree Cement, the partnership provides a secured low-cost input for manufacturing Portland Pozzolana Cement and reduces its reliance on conventional clinker-intensive formulations. The collaboration is cited as a tangible example of circular economy principles being operationalised within India's industrial materials supply chain.

India's government-enforced fly ash utilisation directives - which require construction projects within a 100-kilometre radius of thermal power stations to use fly ash-based materials - have created a structural and regulatory floor for demand in the construction segment. This policy backbone is amplified by the government's massive infrastructure investment programme, encompassing metro rail expansion, national highway development, affordable housing schemes, and dam construction. The India Fly Ash Market growth is particularly visible in metro cities where fly ash concrete is standard specification in substructure and pavement works. In March 2024, NTPC inaugurated a Fly Ash Based Light Weight Aggregate Plant at Sipat, Chhattisgarh, converting fly ash into construction-grade aggregates and demonstrating the value creation potential of government-backed investment in fly ash processing infrastructure.

India's cement industry is the single largest consumer of fly ash, and its accelerating shift toward blended cement products - Portland Pozzolana Cement and Portland Slag Cement - is a primary demand driver for the market. As cement manufacturers work toward reducing their Scope 1 carbon emissions, replacing clinker with fly ash offers an immediate, cost-effective route to lower embodied carbon per tonne of cement. Leading companies including UltraTech, Ambuja, and Shree Cement are actively securing long-term fly ash supply agreements to underpin their green cement strategies. In 2024, Ambuja Cements acquired a 1.5 MTPA cement grinding mill in Tuticorin with a long-term fly ash supply deal embedded in the transaction, illustrating the degree to which fly ash procurement has become a strategic priority alongside production capacity.

Beyond cement and construction, India is building an expanding ecosystem of circular economy partnerships that divert fly ash from disposal into productive industrial applications. Power generators including NTPC, Adani Power, and BALCO are entering structured supply agreements with cement companies, brick manufacturers, and road developers that guarantee minimum offtake volumes and establish logistics frameworks for bulk distribution. The agricultural application of fly ash for soil amendment is also gaining research backing and farmer-level adoption, particularly for acidic soils in eastern states. In 2024, BALCO signed an MoU with Shree Cement for 90,000 metric tonnes of fly ash, a transaction that exemplifies the institutionalisation of circular economy supply chains within India's industrial materials sector.

The emergence of next-generation low-carbon cement products in India - including LC3 (Limestone Calcined Clay Cement), geopolymer cements, and high-fly-ash-content blends - is opening a premium demand segment for high-quality, consistently specified fly ash. Cement companies are investing in quality assurance infrastructure to pre-process and certify fly ash to IS: 3812 standards, enabling its use in structural-grade concrete applications that would otherwise require tighter material specifications. This quality-focus trend supports pricing improvements and encourages power companies to invest in beneficiation. In February 2026, JK Lakshmi Cement launched Green Pro LC3 with 40% lower CO2 emissions, signaling the mainstreaming of sustainable cement formulations that rely on fly ash as a core ingredient.

The Expert Market Research's report titled "India Fly Ash Market Report and Forecast 2026-2035" offers a detailed analysis of the market based on the following segments:

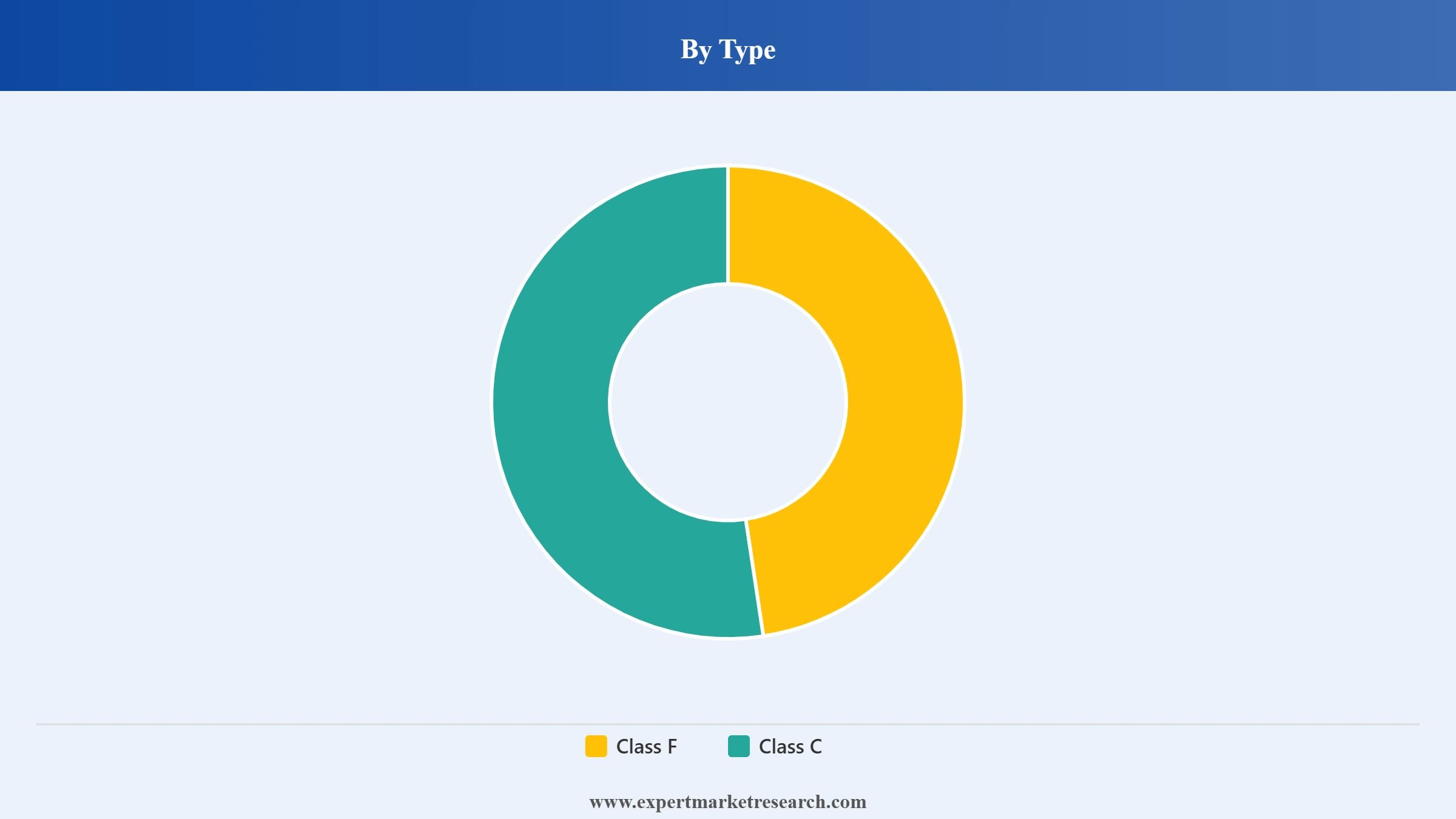

Market Breakup by Type

Key Insight: Class F fly ash dominates the India market given its prevalence as the by-product of burning high-carbon bituminous and anthracite coals, which make up the bulk of fuel used by Indian thermal power stations including NTPC's fleet. Class F is characterised by lower calcium oxide content and pozzolanic properties, making it the standard input for PPC cement, concrete, and fly ash bricks. Class C fly ash, derived from lignite and sub-bituminous coal, has self-cementing properties and is growing in preference among ready-mix concrete operators for early-strength applications. Global data shows Class C posting the faster CAGR trajectory, a trend that is beginning to reflect in India as coal quality diversifies and international best practices in fly ash classification gain traction.

Market Breakup by Application

Key Insight: Construction is the commanding application segment, accounting for the majority of fly ash demand and projected to grow at a CAGR of 6.6% through the forecast period. The sub-segment breakdown covers fly ash bricks and blocks - which offer a 30% lower carbon footprint than conventional fired clay bricks - road base construction, and Portland cement and concrete production where fly ash partially substitutes clinker. The agriculture application is gaining meaningful traction as agronomists confirm fly ash's benefits for improving soil structure, adjusting pH levels in acidic soils, and providing trace micronutrients. The mining application covers fly ash use in mine backfilling, particularly at coal mines in eastern India, while the water treatment application benefits from fly ash's adsorptive properties for heavy metal removal.

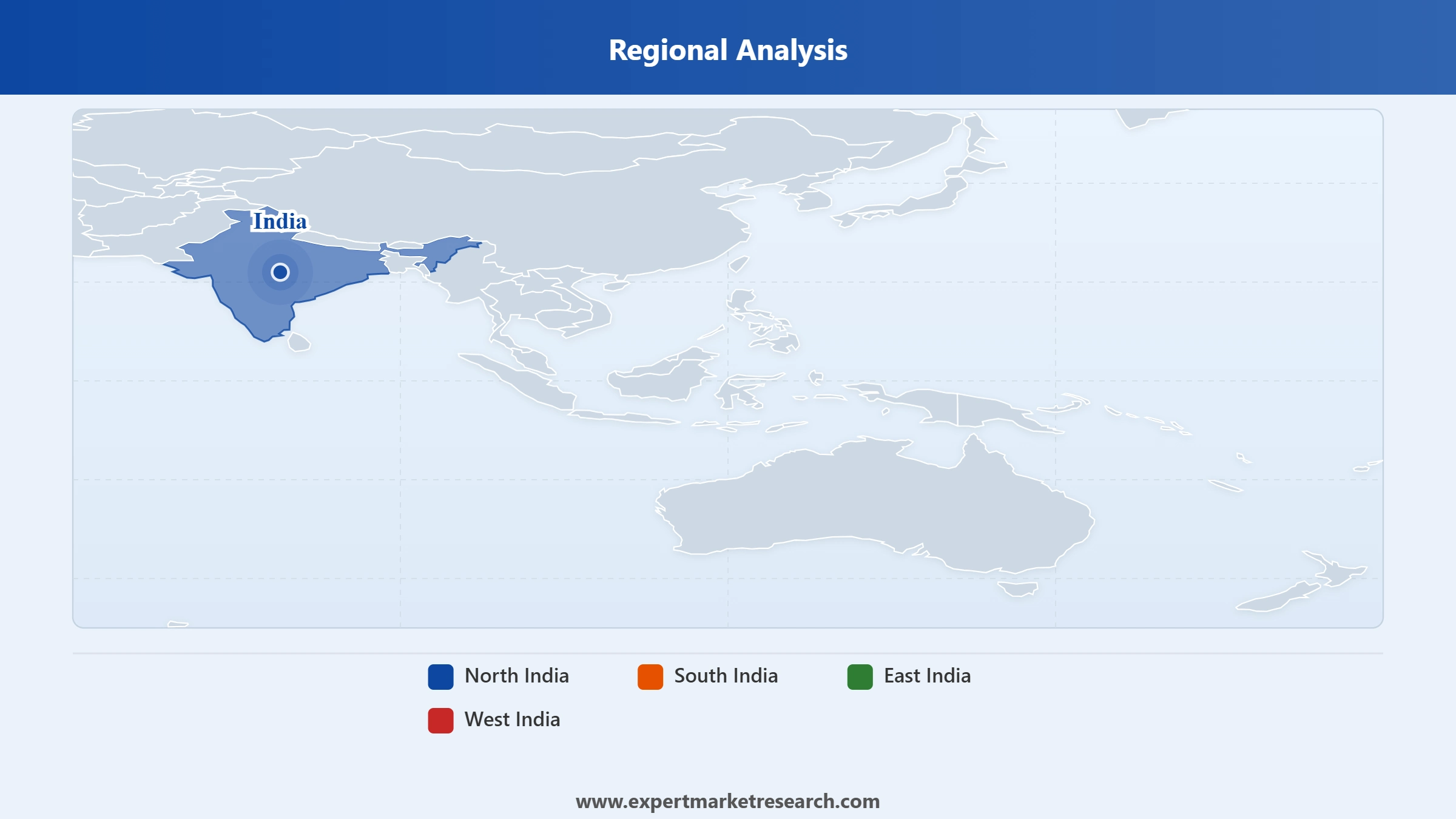

Market Breakdown by Region

Key Insight: East India holds the largest share of fly ash generation given the concentration of India's thermal power capacity in states such as Jharkhand, West Bengal, Odisha, and Chhattisgarh. However, the demand centre for fly ash is distributed more widely, with West India holding approximately 26.7% market share in 2025, driven by the cement industry clusters in Gujarat and Rajasthan. South India is a significant consumption zone anchored by Andhra Pradesh and Tamil Nadu cement plants, while North India benefits from the proximity of large power generators in Uttar Pradesh, Punjab, and Haryana to major construction activity in the Delhi-NCR belt. The ongoing expansion of the East-West logistics corridor through Indian Railways is steadily improving inter-regional fly ash distribution economics.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Class F fly ash holds the dominant market share within the type segmentation, reflecting the fact that most Indian thermal power stations burn high-carbon bituminous coal from the Gondwana coal belt of eastern and central India. NTPC, as the country's largest power generator, produces Class F fly ash predominantly and its marketing policies set the benchmark for supply pricing and contractual terms across the industry. The construction application accounts for the dominant share of total fly ash consumption by volume and value, with cement manufacturing being the single largest end-use given India's status as the world's second-largest cement producer. Fly ash bricks represent the fastest-growing sub-application as housing programme mandates and builders' sustainability commitments converge on demanding low-carbon wall materials.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Within the region segmentation, West India commands the largest share of market revenue in 2025, supported by the Gujarat and Rajasthan cement belts that absorb large fly ash volumes for PPC production. East India, while the dominant supply region, still sells a portion of its output to western markets via rail logistics as local demand - primarily from brick manufacturers and construction projects - has not fully kept pace with generation. The Water Treatment application holds a small but growing share as municipal corporations in water-stressed states explore fly ash-based adsorption technologies for groundwater remediation and industrial effluent treatment.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

East India is the structural backbone of India's fly ash supply chain, housing the country's largest thermal power station clusters across Jharkhand (Bokaro, Patratu), West Bengal (Farakka, Bakreswar), Odisha (Talcher, Sterlite), and Chhattisgarh (Sipat, Korba). These installations collectively generate tens of millions of tonnes of fly ash annually, and NTPC - with its massive integrated generation capacity across eastern India - is the most influential single supplier in the country. Historically, demand absorption in the east has lagged generation due to limited local cement and construction activity relative to output volumes, driving the necessity of long-distance rail-based distribution. The NTPC Sipat lightweight aggregate plant inaugurated in 2024 represents a strategic effort to add on-site processing capacity that creates higher-value products from fly ash before transport, improving logistics economics.

West India, anchored by Gujarat's cement manufacturing corridors in Kutch and Saurashtra and Rajasthan's large-scale integrated cement plants, is the dominant fly ash consuming region by value. UltraTech Cement, Ambuja, ACC, and Shree Cement all operate major facilities in this zone, and fly ash arrives primarily via unit trains from eastern power stations. The expansion of blended cement production mandated by BIS standards and consumer preference for PPC is driving a steady increase in fly ash procurement by West Indian cement plants. South India's consumption is growing in line with accelerating construction activity in Andhra Pradesh, Telangana, Tamil Nadu, and Karnataka, where metro rail projects, highway development, and industrial infrastructure are collectively consuming increasing volumes of fly ash-based concrete and road base materials.

The India Fly Ash Market operates as a multi-tier value chain spanning power generators who supply fly ash as a by-product, intermediary processors who beneficiate and bag it, and end-user industries including cement, construction, and agriculture that consume it. The upstream supply tier is dominated by thermal power companies, with NTPC setting de facto industry norms through its scale and marketing policies. The downstream demand tier is led by large integrated cement manufacturers whose long-term supply agreements shape pricing and logistics structures across the industry.

The competitive environment is fragmented below the top tier, with hundreds of small brick manufacturers, road contractors, and agricultural input suppliers creating a long tail of fly ash consumers. Consolidation is visible in the cement segment where acquisitions such as Ambuja's Tuticorin grinding mill purchase and Shree Cement's BALCO supply MoU reflect strategic moves to secure fly ash supply at scale. Companies that develop proprietary beneficiation technologies, establish reliable rail logistics, and build quality certification systems are gaining sustainable competitive advantages.

Ashtech (India) Pvt. Ltd., founded in 2002 and headquartered in Mumbai, specializes in supplying fly ash of the highest quality through a well-developed logistics network for timely delivery anywhere in India. The company has set up meaningful partnerships with major power utilities to ensure consistent supply.

Established in 1994 and located in Tamil Nadu, Kumaraswamy Industries provides fly ash-based bricks and blocks to the construction industry. The company has focused on offering sustainable alternatives for the housing sector and makes investments in low-carbon building solutions and automated manufacturing units.

Hi-Tech Flyash (India) Private Limited, formed in 2019, offers extensive fly ash and admixture solutions. The company also emphasizes quality control techniques along with associations with universities for the advancement of future products in the field of fly ash.

JAYCEE BUILDCORP LLP was established in 2016, is known for exporting fly ash and slag-based products to over 15 countries in the world. The company specializes in developing compliance as per environmental legislation, product certification, and rigorous quality assurance for clients all over the world.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Unlock the full depth of opportunity in India's rapidly expanding fly ash sector with our comprehensive 2026 market report. Whether you are a power company optimising fly ash utilisation strategy, a cement manufacturer securing long-term supply, a construction materials investor evaluating new product lines, or a policy analyst assessing circular economy outcomes, this report delivers the data and strategic intelligence you need. Download your free sample today and explore the key value chains driving growth in India's thriving fly ash market.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the India fly ash market reached an approximate value of USD 574.43 Million.

The market is projected to grow at a CAGR of 5.70% between 2026 and 2035.

Key strategies driving the market include investing in regional logistics, diversifying product applications, and engaging in policy advocacy for circular economy incentives.

The major types considered in the market report are Class F and Class C.

The regions considered in the market report are North India, East India, South India, and West India. The West India market held 26.7% of the market share in 2025.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Type |

|

| Breakup by Application |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.