Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

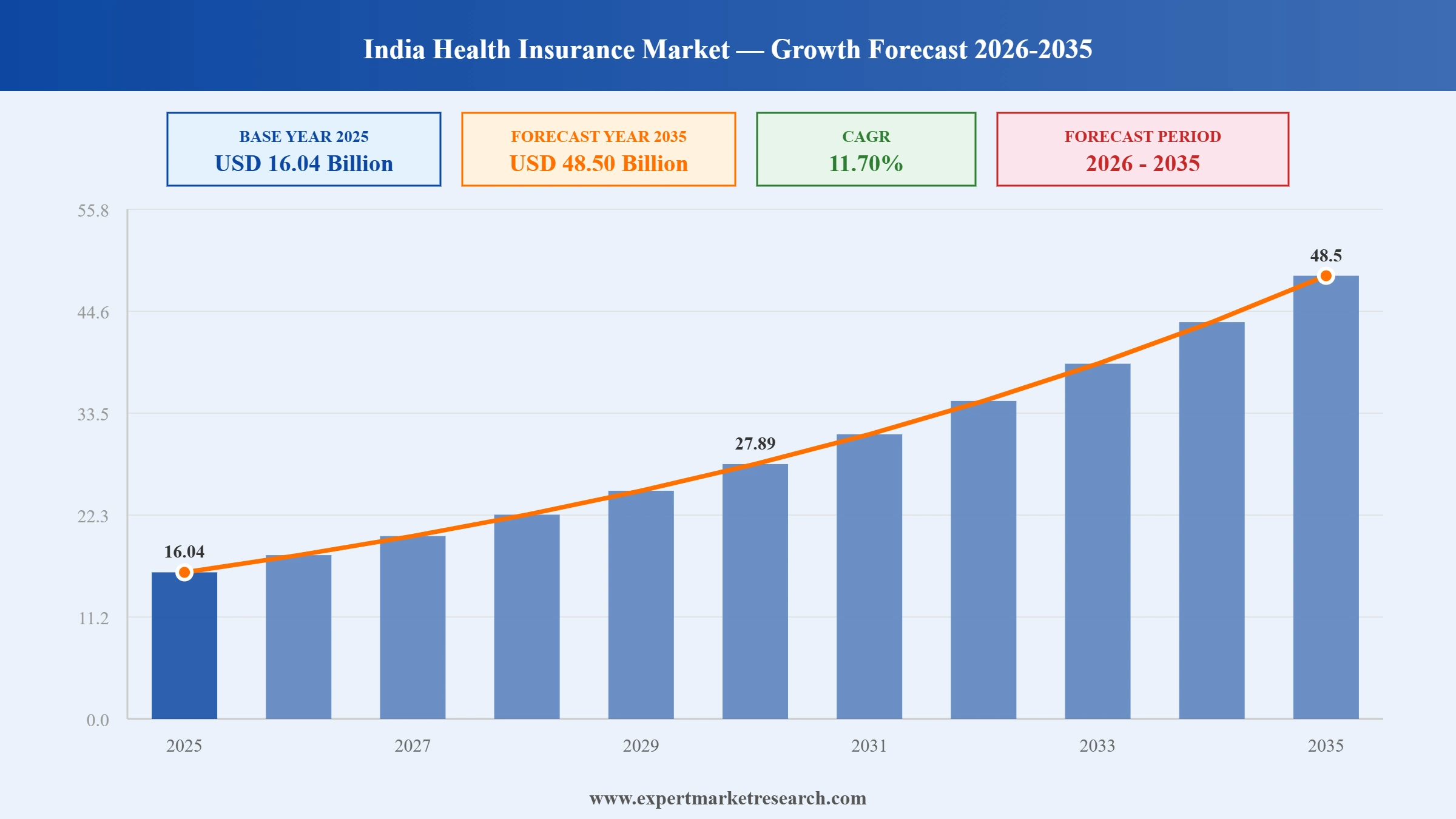

The India Health Insurance Market reached a value of USD 16.04 Billion at 2025 and is projected to expand at a CAGR of around 11.70% during the forecast period of 2026-2035. With escalating medical inflation driving insurance demand, strong government commitment to universal health coverage through Ayushman Bharat, rapid digital adoption by private insurers reducing policy purchase friction, and increasing penetration of standalone health insurance among self-employed and senior citizen segments, the market is expected to reach USD 48.50 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Introduction of specialised products; shift towards cashless reimbursement; use of big data technology; and adoption of cloud-based data storage solutions are the major factors favouring the India health insurance market expansion.

In February 2025, Bajaj Allianz Life Insurance Co. Ltd. launched HERizon Care, described as India's first comprehensive health insurance plan specifically engineered for women's healthcare needs. Structured around two primary covers, Vita Shield and Cradle Care, the plan integrated multiple specialised benefits including maternity care, critical illness protection, and wellness provisions within a single policy. The product launch reflected Bajaj Allianz's strategic intent to capture the underserved female health insurance segment, which represents a significant growth opportunity as women's financial independence and health awareness continue to rise across urban and semi-urban India.

In September 2025, the Insurance Regulatory and Development Authority of India launched the Bima Sugam digital insurance marketplace, a one-stop platform enabling policyholders, insurers, intermediaries, and agents to compare, purchase, manage, and potentially settle claims for life, health, motor, and other insurance products. The platform, with phased rollout of full transaction capabilities planned by December 2025, directly benefited major insurers in the India health insurance ecosystem including HDFC Life, SBI Life, ICICI Prudential Life, and others in the TOC, by reducing customer acquisition costs and streamlining policy servicing at scale through a government-backed digital infrastructure.

In March 2025, the Competition Commission of India approved Bajaj Group's acquisition of Allianz SE's 26% stake in Bajaj Allianz Life Insurance Co. Ltd. for INR 24,180 crore, a landmark transaction that brought the joint venture under full Bajaj Group ownership. The deal marked a significant shift in the competitive dynamics of India's private insurance sector, granting Bajaj Allianz complete strategic autonomy to expand its product range, distribution networks, and geographic penetration without requiring approval from a foreign joint venture partner. The company enters this new phase with one of the widest insurance product ranges among private sector players in India.

In February 2025, nine insurance companies, including HDFC Ergo General Insurance and SBI General Insurance, subsidiaries of two of India's largest financial institutions, submitted IPO plans to the Insurance Regulatory and Development Authority of India (IRDAI) as part of a broad push to raise capital and strengthen corporate governance across the sector. The filings signalled the insurance industry's growing confidence in public market financing and reflected investor appetite for insurance sector exposure. The planned listings were expected to increase transparency, expand capital availability for product innovation, and accelerate distribution network growth among the applicant companies.

In 2024, Zurich Insurance Group announced plans to acquire a 70% stake in Kotak General Insurance, a subsidiary of the broader Kotak Mahindra Group, reflecting strong foreign investor confidence in India's expanding insurance market. The transaction, once completed, would give Zurich Insurance a substantial and direct presence in India's fast-growing general and health insurance segments and would provide Kotak's insurance operations with access to Zurich's global underwriting expertise, technology platforms, and reinsurance relationships, collectively strengthening the competitive position of the Kotak Mahindra Group in the Indian insurance landscape.

The Government of India's extension of Ayushman Bharat PMJAY health coverage to all citizens aged 70 and above, announced in September 2024, significantly expanded the programme's reach and cemented its role as the foundation of India's universal health coverage push. With over 41 crore Ayushman Cards issued and the programme covering secondary and tertiary hospitalisation for over 550 million beneficiaries, the scheme is generating indirect India Health Insurance Market growth by creating awareness of health insurance as a concept among demographics that had no prior exposure to formal financial protection products. Private insurers are capitalising on this awareness by targeting adjacent consumer segments with complementary commercial products.

India's Union Budget 2025 announcement raising the Foreign Direct Investment limit in the insurance sector from 74% to 100% for companies investing all collected premiums domestically represented a landmark policy shift. The change eliminated the joint venture structure previously required for foreign insurers, lowering barriers to entry and enabling global insurance giants to pursue majority-owned or fully-owned India operations. In March 2025, Prudential plc announced a joint venture with HCL Group's Vama Sundari Investments to launch a standalone health insurance business, reflecting how quickly foreign capital and expertise are responding to the reform. This wave of incoming investment is strengthening product innovation, underwriting technology, and distribution infrastructure across the market.

India's health expenditure has risen from INR 3.2 lakh crore in 2020 to 2021 to INR 6.1 lakh crore in 2024 to 2025, representing a compound annual growth rate of 18%. Out-of-pocket healthcare spending, which still accounts for approximately 39% of total health expenditure, is creating significant financial stress for middle-income households facing hospitalisation, surgeries, or chronic disease management costs. This convergence of rising medical costs and inadequate savings buffers is the single most powerful driver of retail health insurance adoption in India, particularly among first-time policyholders in Tier 2 and Tier 3 cities who are newly exposed to formal insurance products through bancassurance and mobile platforms.

The digitisation of India's health insurance distribution is fundamentally changing how policies are sold, managed, and renewed. InsurTech platforms, bancassurance digital channels, and app-based direct-to-consumer tools are compressing the time from consideration to policy issuance from days to minutes. In September 2025, the launch of Bima Sugam, IRDAI's one-stop digital insurance marketplace, added a government-backed digital layer that enables consumers to compare plans, purchase policies, and process claims through a single portal. Additionally, Future Generali India introduced an AI-powered tool to help consumers assess optimal health coverage levels, reflecting how technology is addressing the information gap that historically depressed insurance penetration in semi-urban and rural markets.

"India Health Insurance Market Report and Forecast 2026-2035" offers a detailed analysis of the market based on the following segments:

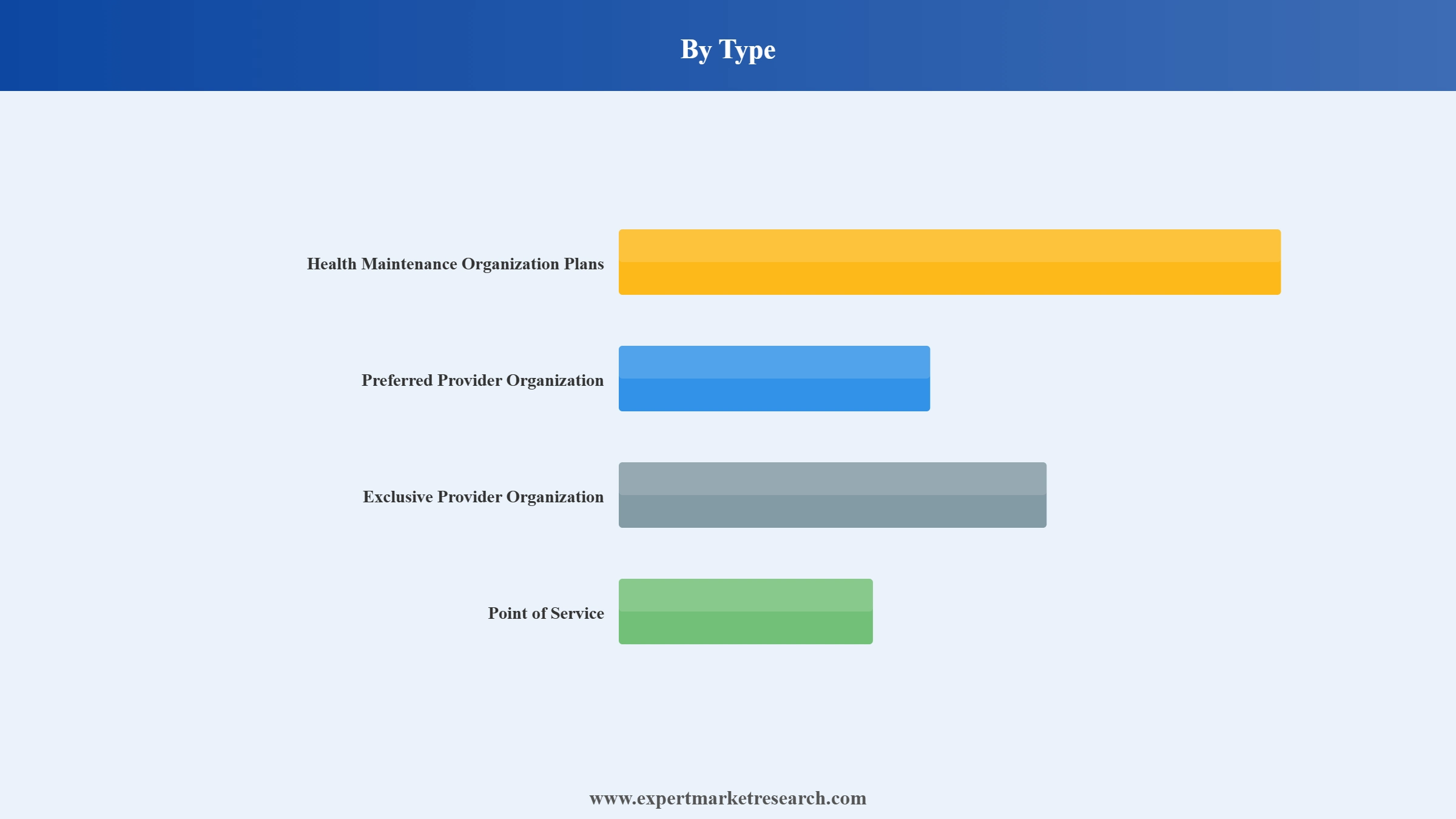

Market Breakup by Type

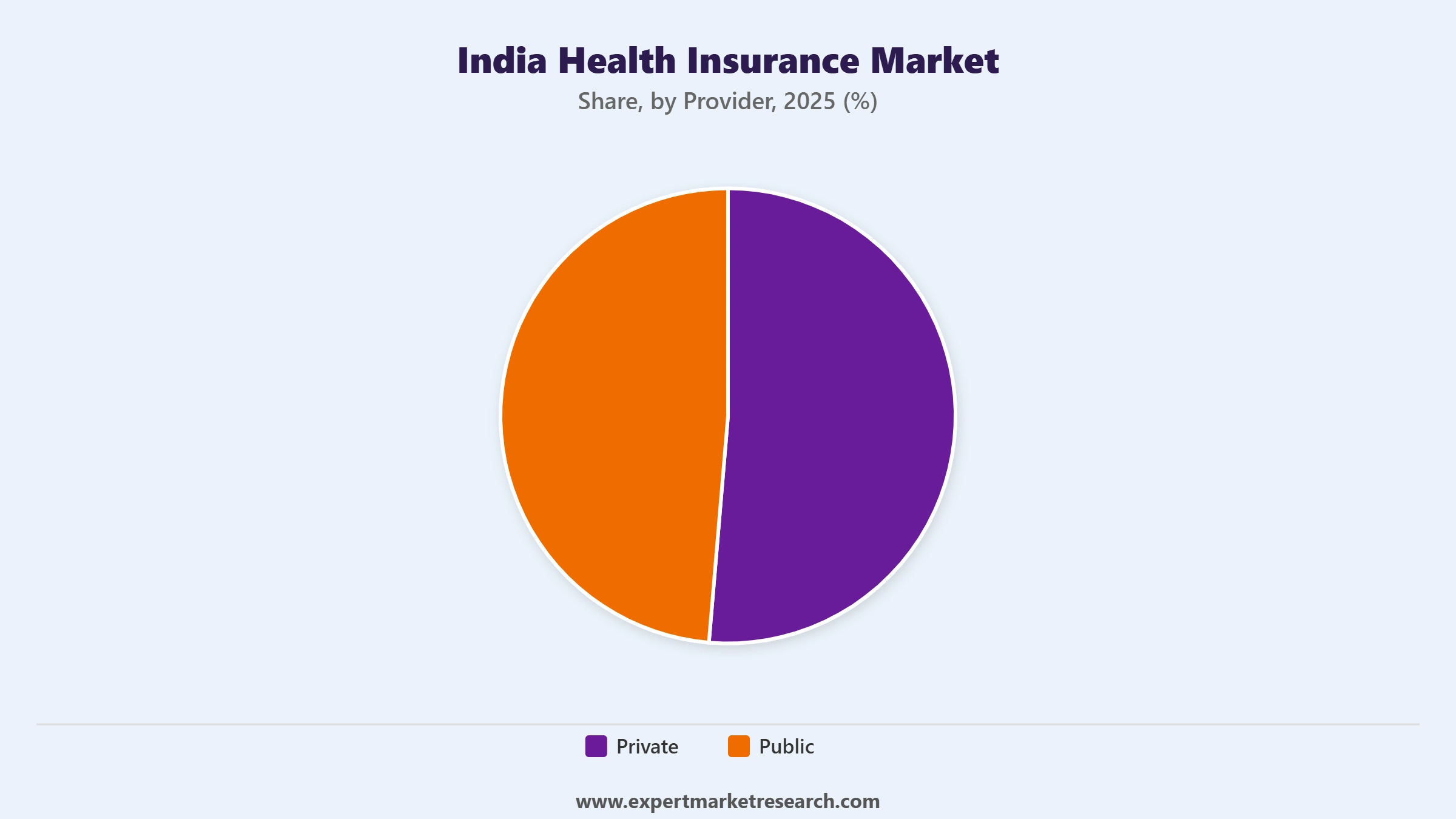

Market Breakup by Provider

Market Breakup by Coverage

Market Breakup by Demographics

Market Breakup by Mode

Market Breakup by End User

Market Breakup by Distribution Channel

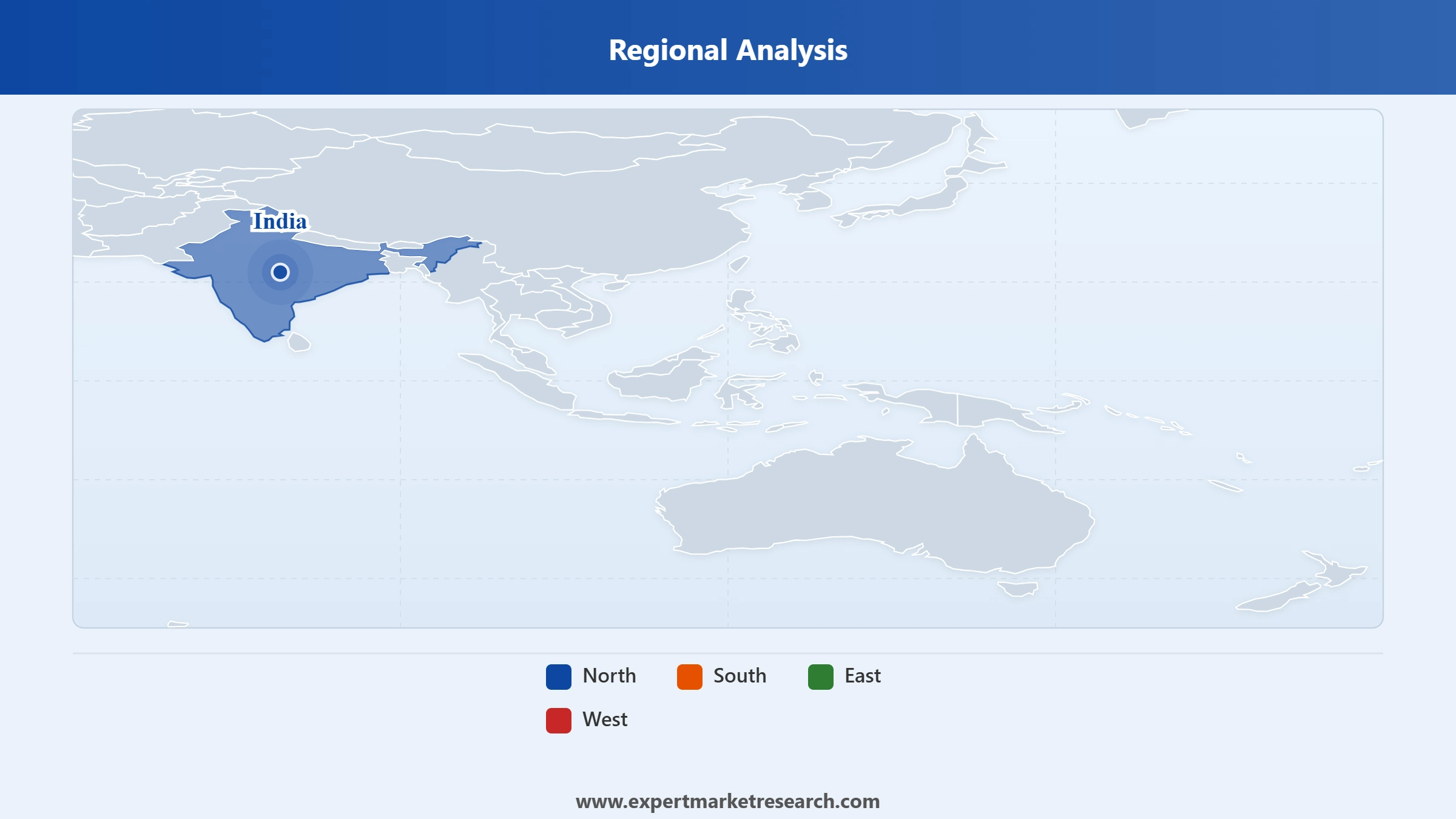

Market Breakup by Region

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Within the Type segmentation, Point of Service plans command the largest revenue share at approximately 45% in 2025, reflecting their structural advantage in India's urban healthcare market where consumers demand both in-network cost efficiency and the ability to see specialists outside the network when needed. This flexibility is particularly valued by urban dual-income households managing chronic conditions for which specialist continuity of care matters. HMO plans hold a significant share in the corporate group health insurance segment, where employers prioritise cost predictability and managed care networks over individual policyholder flexibility.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Private providers hold a dominant 65 to 66% revenue share in India's health insurance market, a position reinforced by consistent advantages in product speed-to-market, claim settlement efficiency, and customer experience. Private insurers' claim settlement ratios, with HDFC Life reporting 99.7% and ICICI Prudential Life at 99.29%, have become a primary trust-building metric that is converting first-time buyers who were previously reluctant to engage with the insurance sector. The public sector's market share, while substantial through LIC of India and government-run general insurers, is eroding as private players deepen their penetration in semi-urban markets through InsurTech partnerships.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Within the regional dimension, South India accounts for the largest share of India's health insurance market and is expected to sustain this position through the forecast period. West India, particularly Maharashtra, follows closely as a high-revenue region given Mumbai's large base of corporate policyholders and the state's relatively higher penetration of retail health insurance.

South India leads the India Health Insurance Market across all major metrics, combining higher consumer awareness, a dense private hospital network, and stronger financial literacy than most other regions. Tamil Nadu, Karnataka, Telangana, and Kerala collectively drive South India's insurance demand through a combination of urban middle-class retail policyholders, large employer group health plans in IT and manufacturing sectors, and government-linked schemes that are effectively expanding the insurance concept into rural communities. Southern India is projected to record the highest regional CAGR over the 2026 to 2035 forecast period, as standalone health insurers concentrate distribution expansion efforts in this region due to its proven consumer receptiveness.

West India, anchored by Maharashtra and growing rapidly in Gujarat, is the second-most significant regional market for health insurance. Mumbai's position as India's financial capital generates a large base of corporate group health policyholders employed in banking, financial services, and insurance sectors, creating consistent and high-value premium flows. Maharashtra also hosts a significant concentration of private hospital chains, reinforcing insurance utility and accelerating repeat renewals. Gujarat's industrial base and high entrepreneurial density translate into above-average small and medium enterprise group health plan adoption. West and Central India is expected to record a CAGR of 13.3% over the forecast period.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

India's health insurance market is moderately concentrated at the top, with a cluster of large private life and health insurers competing intensely on product innovation, digital distribution, and claim settlement efficiency. The public sector anchor, Life Insurance Corporation of India, retains the largest single market share by premium volume but is increasingly facing competition from nimble private players who are investing heavily in technology and customer experience. Standalone health insurers are carving out specialised market positions by focusing exclusively on health products, developing superior medical underwriting capabilities and insurer-hospital network relationships.

Competitive priorities are shifting from distribution breadth toward product depth and digital experience. Bancassurance remains the dominant distribution channel, but InsurTech platforms, corporate broker networks, and direct digital acquisition are rapidly gaining share. Key competitive levers include claim settlement ratios, hospital network size and cashless facility availability, and the ability to offer wellness-linked premium discounts that reduce long-term claims exposure while building policyholder loyalty

Founded in 2000 and headquartered in Mumbai, India, HDFC Life Insurance Company Ltd. is a joint venture between HDFC Ltd. and Standard Life Group. The company operates across 535 branches and maintains bancassurance partnerships with 265 institutions. HDFC Life's industry-leading claim settlement ratio of up to 99.7% and its 2025 Superbrand recognition reflect its strong consumer trust. The company's product range spans term plans, unit-linked insurance products, cancer-specific policies, critical illness covers, and retirement plans, offering broad coverage across India's insurance needs.

Established in 2006 as a joint venture between Bharti Enterprises and AXA Group, Bharti AXA is one of India's established private health and life insurance players. The company serves individual, family floater, and corporate policyholders with a product portfolio spanning health, life, and general insurance. Bharti AXA leverages the distribution strength of the Bharti Enterprises group alongside AXA's global insurance expertise to serve urban and semi-urban markets. Its focus on accessible, mid-market insurance products and digital policy management positions it well within India's rapidly expanding middle-class policyholder base.

Founded in 2001 as a joint venture between the State Bank of India and BNP Paribas Cardif, SBI Life Insurance Company Ltd. is India's largest private-sector life insurer by new business premium. In FY25, SBI Life collected INR 35,577 crore (approximately USD 4.16 billion) in premium, maintaining its top position among private players. The company's unparalleled distribution advantage through SBI's 22,000-plus branches and extensive rural banking network gives it a reach that no purely private sector insurer can replicate.

Founded in 2001 as a joint venture between ICICI Bank and Prudential plc, ICICI Prudential Life Insurance Company Ltd. was the first insurance company in India to be publicly listed on domestic stock exchanges, achieving this milestone in 2016. The company's particular strength lies in unit-linked insurance products and retirement solutions. With a claim settlement ratio of 99.29% and a solvency ratio of 5.16, highest in the industry, ICICI Prudential's financial robustness is a key competitive asset in a market where consumer trust is built primarily on claims reliability.

Other key players in the market are Max Life Insurance Company, Bajaj Allianz Life Insurance Co. Ltd., Tata AIA Life Insurance Company Limited, Kotak Mahindra Group, Aditya Birla Capital Ltd., Life Insurance Corporation of India, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

India's health insurance market is one of the most compelling growth stories in the global financial services sector, combining a vast underinsured population, a government committed to universal coverage, rising medical costs creating genuine consumer urgency, and a technology environment that is rapidly reducing the friction in buying and managing insurance. Our 2026-2035 report provides the data, context, and competitive intelligence you need to identify your opportunity within this market. Download your free sample today and take the first step toward building a strategy grounded in the realities of India's health insurance landscape.

Vietnam Health Insurance Market

Saudi Arabia Health Insurance Market

Upto 15% Off

USD

$1999 $1799

$3099 $2789

$4599 $3909

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market reached an approximate value of USD 16.04 Billion.

The market is projected to grow at a CAGR of 11.70% between 2026 and 2035.

The market is estimated to witness healthy growth in the forecast period of 2026-2035 to reach a value of around USD 48.50 Billion by 2035.

The different regions considered in the market report include East India, West and Central India, North India, and South India.

The different types of health insurance include disease health insurance and medical health insurance.

The different end users of insurance in the market include individuals, and corporates, among others.

The different types of health insurance coverage include disease insurance and medical insurance, among others.

Key players in the market are Life Insurance Corporation of India, HDFC Life Insurance Company Ltd., SBI Life Insurance Company Ltd., ICICI Prudential Life Insurance Company Ltd., Max Life Insurance Company, Bajaj Allianz Life Insurance Co. Ltd., Tata AIA Life Insurance Company Limited, Kotak Mahindra Group, Aditya Birla Capital Ltd., and The New India Assurance Co. Ltd., among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Type |

|

| Breakup by Provider |

|

| Breakup by Coverage |

|

| Breakup by Demographics |

|

| Breakup by Mode |

|

| Breakup by End User |

|

| Breakup by Distribution Channel |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Supplier Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 1,999

USD 1,799

tax inclusive*

Single User License

One User

USD 3,099

USD 2,789

tax inclusive*

Five User License

Five User

USD 4,599

USD 3,909

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.