Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

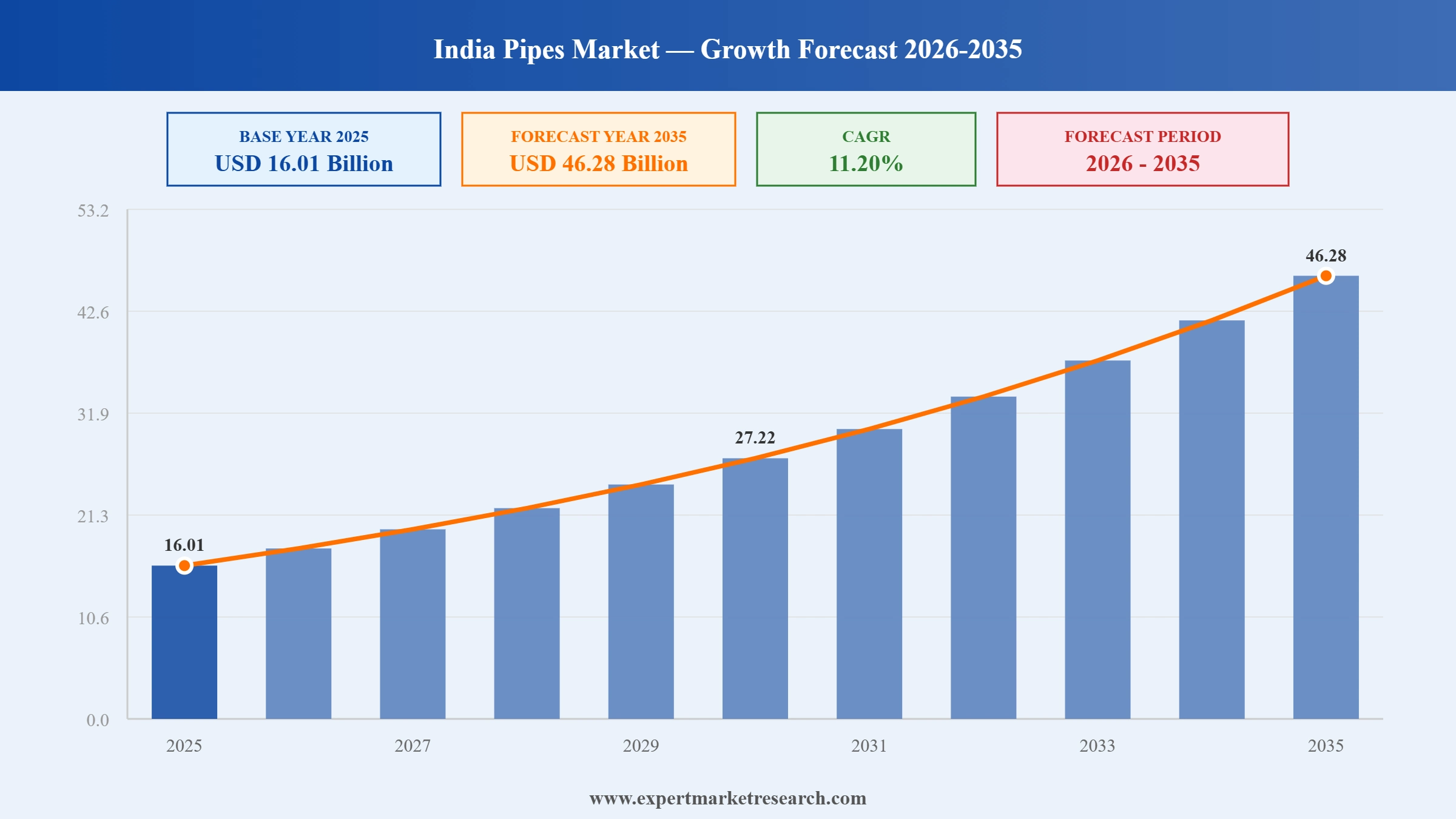

The India Pipes Market reached a value of USD 16.01 Billion at 2025 and is projected to expand at a CAGR of around 11.20% during the forecast period of 2026-2035. With the Jal Jeevan Mission and AMRUT 2.0 creating large-scale national demand for water supply and sewerage pipes, rapid urbanisation and real estate development expanding demand across residential and commercial construction, rising agricultural irrigation investment requiring extensive HDPE and plastic pipe networks, and growing industrial and renewable energy sector infrastructure creating new applications for piping systems, the market is expected to reach USD 46.28 Billion by 2035.

The India market for pipes is experiencing robust traction from the city gas distribution (CGD) segment on account of the "One Nation, One Gas Grid" scheme that is aimed at linking more than 70% of the population with piped natural gas. India is looking to achieve over 35,000 km of gas pipeline network by 2030, as per PNGRB. High-performance PE pipes are favoured because of their corrosion resistance, flexibility, and safety. The India pipe demand forecast is particularly strong in Tier II and III cities, where pipeline deployment is growing very fast.

Telecom infrastructure expansion, spurred by BharatNet and 5G rollout, is also contributing considerably to demand for duct pipes in India. India is going to lay more than 10 million km of optical fibre by 2025. HDPE duct pipes are essential to safeguard fibre optic networks in urban areas as well as rural areas. Telecom operators prefer companies that provide UV-resistant, crush-resistant, and easy-to-install ducting systems to achieve low-maintenance high-speed internet delivery in data-intensive settings.

The pipes market in India is slated for robust growth due to rapid urbanization, government infrastructure programmes, such as the Jal Jeevan Mission, and increasing agricultural and industrial demands. The most prominent trends are increased adoption of CPVC and HDPE pipes as they offer better durability and corrosion resistance to soil and earth chemicals. The market is expected to expand with increased demand for automation and emerging technologies for manufacturing. Major players such as Supreme Industries, Finolex Industries, and Astral Limited are increasing product offerings and distribution channels to position themselves strategically for tapping into rural and urban infrastructure expansion in domestic and international markets.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

| India Pipes Market Report Summary |

Description |

Value |

|

Base Year |

USD Billion |

2025 |

|

Historical Period |

USD Billion |

2019-2025 |

|

Forecast Period |

USD Billion |

2026-2035 |

|

Market Size 2025 |

USD Billion |

16.01 |

|

Market Size 2035 |

USD Billion |

46.28 |

|

CAGR 2019-2025 |

Percentage |

XX% |

|

CAGR 2026-2035 |

Percentage |

11.20% |

|

CAGR 2026-2035- Market by Region |

North India |

12.8% |

|

CAGR 2026-2035 - Market by Region |

South India |

12.0% |

|

CAGR 2026-2035 - Market by Material Type |

Plastic |

13.2% |

|

CAGR 2026-2035 - Market by Application |

Offices and Housing |

13.4% |

| 2025 Market Share by Region | North India |

32.7% |

In July 2025, Hindware inaugurated its third Truflo-brand plastic pipe manufacturing facility at Roorkee, Uttarakhand, backed by an investment of approximately INR 170 crore. The new plant commenced trial production with an initial annual capacity of 12,500 tonnes, producing a comprehensive range of CPVC, UPVC, SWR, and PVC pipes and fittings along with overhead water storage tanks. The Roorkee location was selected for its strategic advantage in serving North and West India more efficiently, reducing logistics costs and improving distribution reach. With this addition, Hindware's total Truflo piping production capacity rose to 80,500 tonnes per annum. The facility is also expected to generate approximately 200 direct and indirect jobs in the region.

In July 2025, Adani Enterprises Ltd announced plans to build a 1 million tonnes per annum PVC manufacturing plant at its Mundra, Gujarat complex, targeted for commissioning in FY2028. The facility will be integrated within a larger petrochemical complex incorporating chlor-alkali, calcium carbide, and acetylene units, employing a regulator-approved production process. The scale of this investment reflects a strategic commitment by one of India's largest industrial conglomerates to reducing the country's PVC import dependency and to competing in the domestic PVC pipe and construction material supply chain at significant scale. The plant, when operational, will materially add to India's domestic PVC resin supply, improving raw material availability and likely easing input costs for downstream pipe manufacturers.

In March 2025, Ashirvad Pipes Private Limited, one of India's major PVC, UPVC, and CPVC pipe manufacturers, announced plans to invest approximately USD 47 million in two new greenfield manufacturing facilities in South India, with sites in Chennai and Hyderabad targeted for commissioning by FY2027. The investment is designed to expand the company's total production capacity from 3 lakh tonnes to 4 lakh tonnes per annum, enabling Ashirvad to better serve the strong and growing demand for plastic pipes in residential construction, water supply networks, and industrial applications across South India and neighbouring states. The move reflects the broader trend of leading Indian pipe manufacturers making major capacity commitments to capture rising demand.

In February 2025, JTL Industries Limited secured a USD 3 million order from the Public Health Engineering Department of Jammu for the supply of 3,000 metric tons of galvanised iron (GI) pipes to support India's Jal Jeevan Mission (JJM). JTL Industries is an established supplier in India's government infrastructure projects and has built a strong track record in delivering high-quality pipe products under national water access schemes. The order came shortly after the Indian government extended the Jal Jeevan Mission timeline to 2028 with an additional budget allocation of approximately USD 4.8 billion announced by the Jal Shakti Ministry, signalling long-duration committed demand for pipe products across rural water connectivity projects.

In February 2025, Malpani Pipes and Fittings Limited announced a capital investment of approximately INR 3.8 crore to expand its manufacturing operations, introducing a new range of PVC pipes alongside an upgrade to its production machinery. The expansion added 5,400 MTPA of additional capacity across PVC, HDPE, and MDPE pipe types. The investment reflects the broader trend of small and mid-sized Indian pipe manufacturers scaling up operations in response to the demand uplift created by government programmes including the Jal Jeevan Mission and state-level irrigation and water supply projects. Malpani's product portfolio expansion into HDPE and MDPE pipes also positions the company to participate in agricultural irrigation and rural water supply procurement, two of the fastest-growing demand channels in the India pipes market.

India's real estate expansion beyond its major metros is creating a growing and geographically distributed demand base for residential pipes. Tier 2 and Tier 3 cities are experiencing accelerated housing project activity as developers follow migrating middle-class populations, supported by government schemes promoting affordable housing and urban infrastructure improvement. Each new housing development creates demand for PVC, CPVC, and HDPE pipes across plumbing, drainage, water supply, and sewage applications. India's urban population is projected to reach 600 million by 2031, and the construction of new housing and commercial developments to accommodate this shift is sustaining long-term demand for plastic pipes across a widening geography. In the first half of 2024, real estate transactions across India surged meaningfully, with developers in Tier 2 cities reporting stronger-than-expected pre-sales for newly launched residential projects.

India's agricultural sector is undergoing a significant shift toward drip and sprinkler irrigation systems, which require extensive HDPE and LDPE pipe networks to distribute water efficiently to fields. Government programmes including the Pradhan Mantri Krishi Sinchai Yojana (PMKSY) are promoting precision irrigation adoption among farmers, creating structured and subsidised demand for plastic pipes in rural areas. Agricultural applications represent a distinct and growing segment of the India pipes market that runs in parallel to the urban infrastructure demand driven by the Jal Jeevan Mission and AMRUT 2.0. In 2024, government allocations under PMKSY continued supporting farmers' transition to micro-irrigation systems, with HDPE pipes forming the backbone of the distribution networks for drip and sprinkler installations across key agricultural states including Maharashtra, Gujarat, Madhya Pradesh, and Rajasthan.

The Indian government's Jal Jeevan Mission, which targets providing functional tap water connections to every rural household in India, has become the single most powerful demand driver in the India Pipes Market. With over 11.8 crore homes connected as of August 2024, representing approximately 78% of rural household coverage, the programme has generated vast and recurring demand for water supply pipes across all states. AMRUT 2.0 has compounded this by approving 3,571 urban water supply projects worth INR 1,18,421.92 crore through the Ministry of Housing and Urban Affairs. These schemes guarantee a multi-year pipeline of government-funded pipe procurement, providing manufacturers with revenue visibility and incentivising capacity expansion. In August 2024, Jal Jeevan Mission coverage surpassed 78% of rural households, a milestone that simultaneously highlighted the continued demand ahead for closing the remaining coverage gap.

Across water supply, sewerage, agriculture, and construction applications, HDPE and CPVC pipes are steadily displacing traditional metal and lower-specification plastic pipe types. HDPE is the preferred choice for long-distance rural water supply networks and irrigation systems due to its flexibility, weld-joint integrity, and resistance to corrosion, soil movement, and temperature fluctuation. CPVC is gaining rapid traction in residential and commercial plumbing, HVAC, and fire-sprinkler systems for its ability to handle hot water and chemical resistance without the brittleness of standard PVC. India's PVC pipes market reached 3.1 million tonnes in 2025 and is projected to grow at a CAGR of 6.59% through 2034, underlining the momentum of advanced plastic pipe types in the India Pipes Market growth trajectory. In March 2025, Ashirvad Pipes committed USD 47 million to two South India facilities specifically for PVC, UPVC, and CPVC production, reflecting manufacturer confidence in sustained demand for these advanced materials.

The EMR’s report titled “India Pipes Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

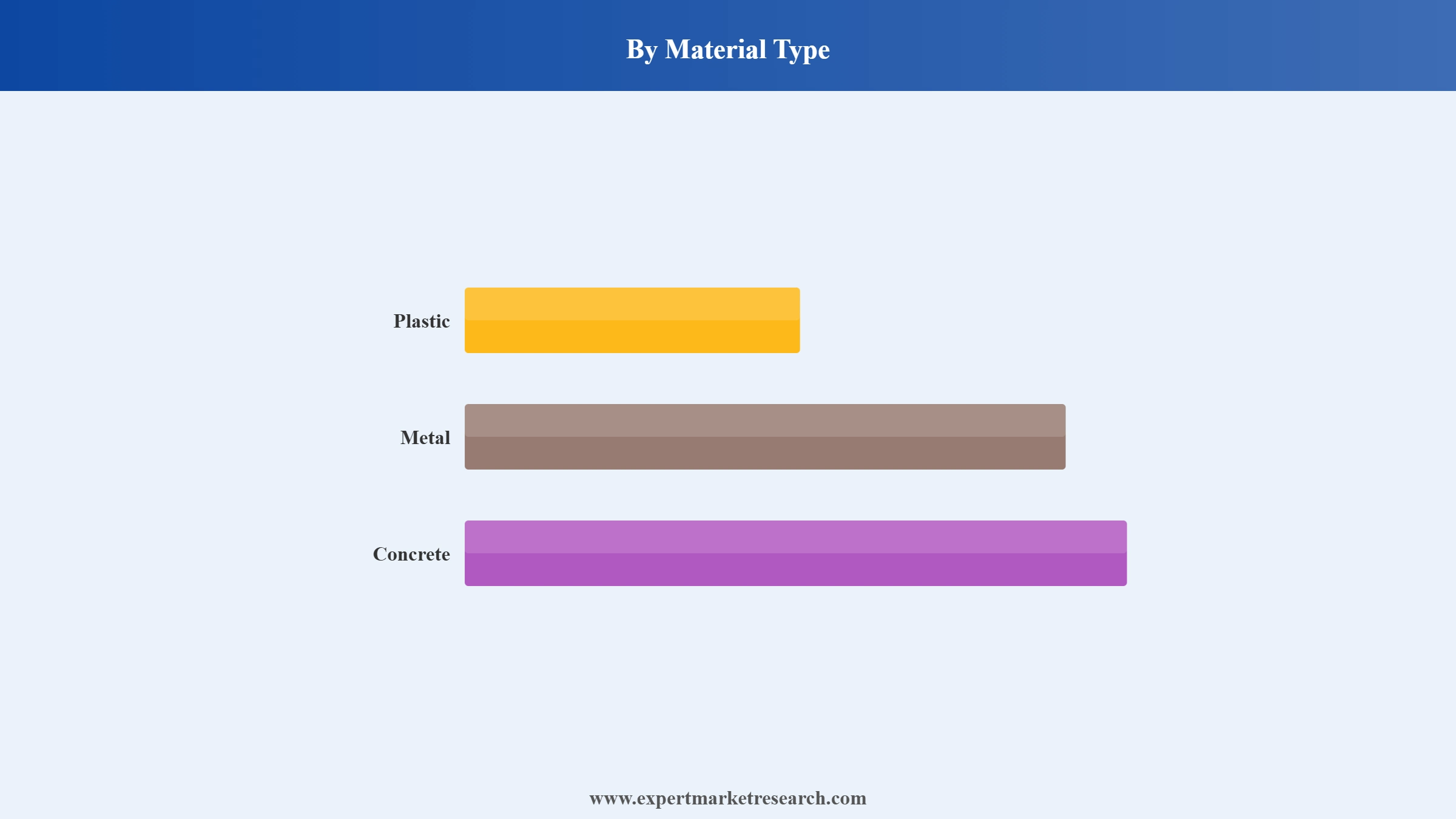

Market Breakup by Material Type

Key Insight: Plastic pipes dominate the India pipes market with the largest share and the fastest growth rate among all material categories. PVC is the highest-volume plastic pipe type, used extensively in water supply, sewerage, agricultural irrigation, and residential construction. HDPE is the preferred material for long-distance rural water networks and agricultural irrigation due to its flexibility and weld-joint integrity. CPVC is gaining momentum in potable water plumbing and industrial applications for its high-temperature and chemical resistance. The PVC pipes segment in India reached 3.1 million tonnes in 2025 and is projected to grow at a CAGR of 6.59% through 2034. Metal pipes, particularly ductile iron, serve critical water transmission mains and sewage force main applications where structural strength and pressure performance are non-negotiable. ERW pipes serve oil and gas and industrial applications. Concrete pipes continue to be used in large-diameter stormwater and drainage projects in urban infrastructure.

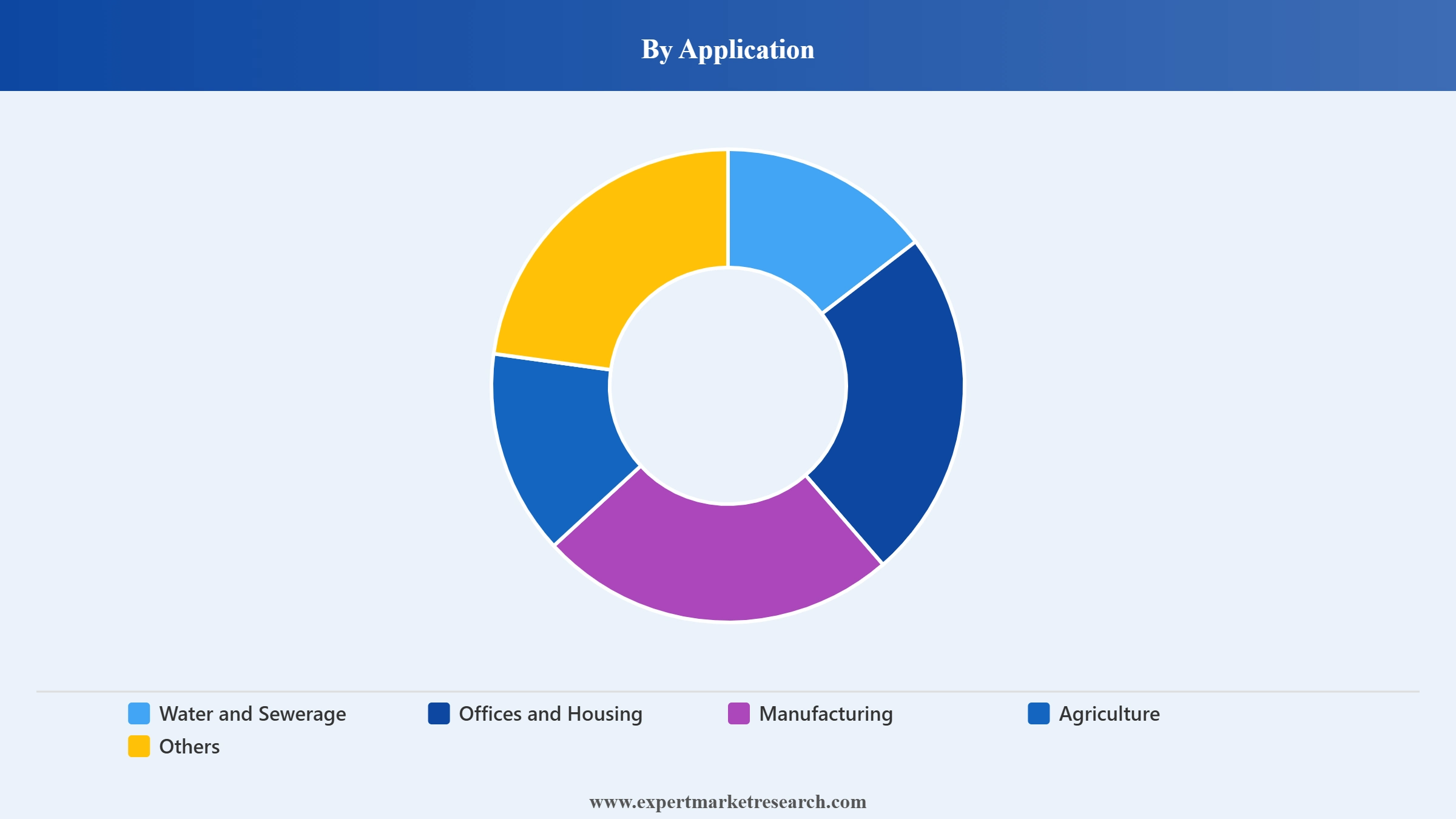

Market Breakup by Application

Key Insight: Water and sewerage is the dominant application in the India pipes market, backed by the Jal Jeevan Mission and AMRUT 2.0's combined investment in rural and urban water infrastructure across the country. As of August 2024, the Jal Jeevan Mission had connected over 11.8 crore homes, and AMRUT 2.0 had approved water supply projects worth INR 1,18,421.92 crore, generating sustained multi-year demand. Offices and housing represent the second-largest application, driven by rapid urbanisation and residential construction in Tier 2 and Tier 3 cities. Agriculture is the fastest-growing application segment, as government irrigation schemes including PMKSY expand precision irrigation adoption, creating large-scale rural demand for HDPE and LDPE pipes. Manufacturing applications are growing in parallel with industrial zone expansion under Make in India.

Market Breakup by Diameter

Key Insight: Small-diameter pipes in the up to 50 mm and 50 to 100 mm ranges are the highest-volume categories in the India pipes market, driven primarily by residential and agricultural applications where large numbers of individual connections require distribution pipe of small diameter. Medium-diameter pipes in the 100 to 200 mm and 200 to 400 mm ranges serve municipal water distribution mains and sewage collection networks, representing the highest combined value segment given the extensive government-funded network expansion underway across India. Large-diameter pipes above 400 mm are used for major water transmission mains, industrial process lines, and sewage trunk mains, with demand concentrated in large infrastructure projects funded through AMRUT 2.0 and state government programmes.

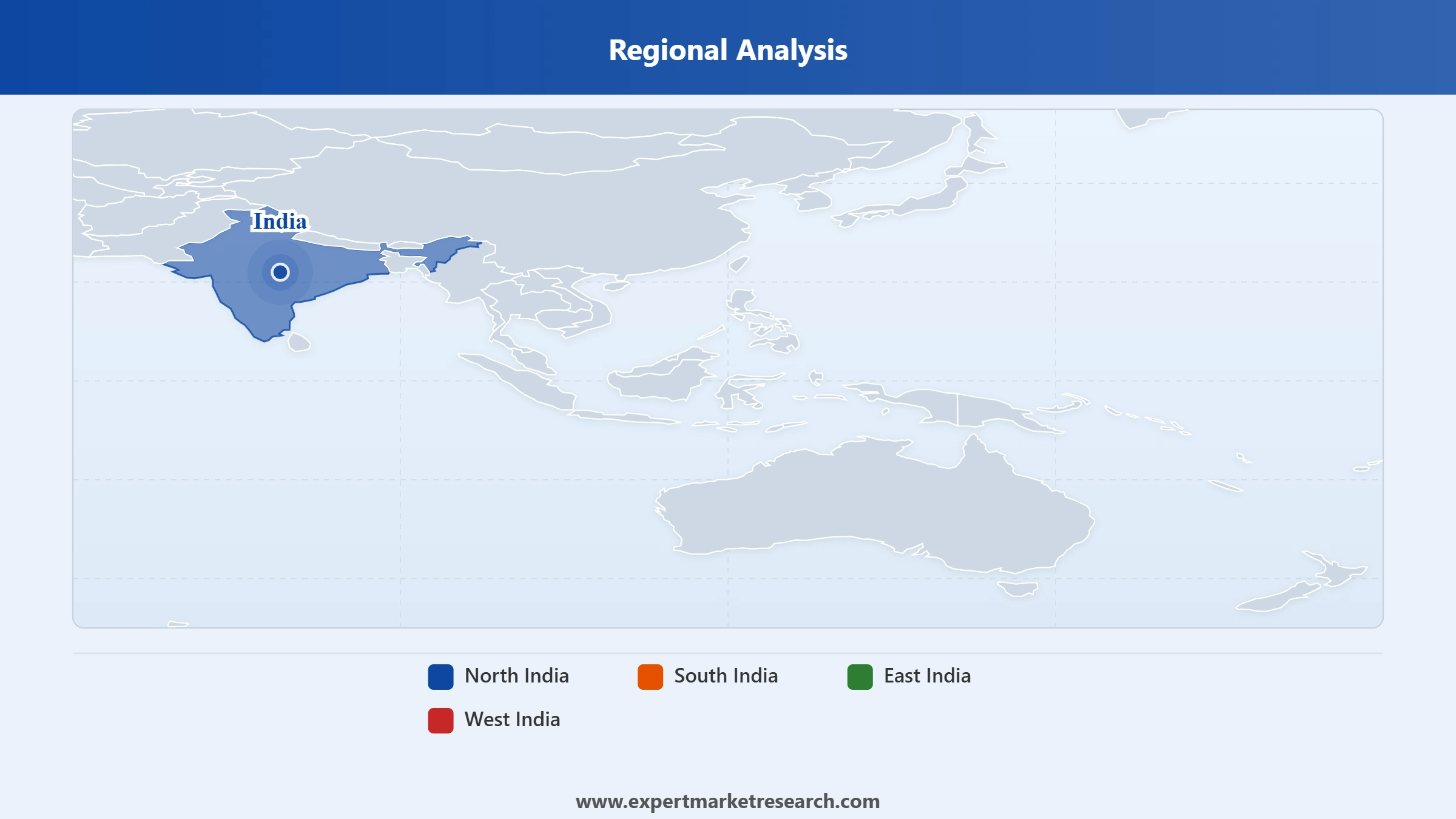

Market Breakup by Region

Key Insight: North India is the dominant region in the India pipes market by volume, driven by the large population base of Uttar Pradesh, Punjab, Haryana, and Delhi's urban agglomeration, extensive agricultural irrigation demand, and the concentration of major government water and sewage infrastructure projects. West India, centred on Maharashtra and Gujarat, is a key market given the strong industrial base, active real estate development, and agricultural irrigation investment in these states. South India is the fastest-growing region, with significant manufacturing investment, real estate expansion across Bengaluru, Chennai, and Hyderabad, and major pipe manufacturing capacity additions including Ashirvad Pipes' planned greenfield facilities in Chennai and Hyderabad.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Material Type, plastic pipes hold the dominant market share in India across both volume and value, a reflection of the country's government-driven water infrastructure programmes and construction growth, both of which heavily favour plastic pipe solutions for their cost efficiency and ease of installation. PVC commands the highest share within the plastic sub-segment given its applicability across water supply, sewerage, agricultural irrigation, and residential plumbing. HDPE is gaining its share of the plastic market as Jal Jeevan Mission rural water network projects increasingly specify weld-jointed HDPE networks for their long-term reliability and leak resistance. Companies such as Finolex Pipes and Astral Poly Technik have built strong national market positions in PVC and CPVC pipes, serving both retail and institutional procurement channels. Metal pipes, while smaller in overall share, maintain critical roles in high-pressure transmission applications, with Jindal SAW Ltd. and Welspun Corp. Ltd. among the leading suppliers in the metal pipe segment.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Application, water and sewerage commands the leading share of the India pipes market, sustained by the multibillion-dollar government infrastructure programmes delivering functional water connections to rural and urban households. The JJM's achievement of 78% rural household coverage as of August 2024 represents a significant volume of past pipe consumption but also signals continued demand to close the remaining coverage gap. Simultaneously, AMRUT 2.0's urban water projects are creating urban demand that runs in parallel to the rural JJM procurement. Agriculture is growing its share within the total market as precision irrigation adoption expands, with PMKSY subsidies lowering the cost of drip and sprinkler systems for farmers and creating demand for HDPE and LDPE pipes that did not previously exist in these rural markets.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

North India is the largest and highest-volume region in the India pipes market. States including Uttar Pradesh, Rajasthan, Punjab, Haryana, and the National Capital Territory of Delhi collectively generate the highest demand for water supply, sewerage, and agricultural pipes in the country. Uttar Pradesh is a critical market for Jal Jeevan Mission pipe procurement given its large rural population and the scale of water connection targets within the state. In February 2025, JTL Industries secured a USD 3 million order from the Public Health Engineering Department of Jammu for GI pipes under Jal Jeevan Mission, illustrating the breadth of government procurement activity across North India. Agricultural states including Punjab, Haryana, and Rajasthan also generate significant demand for irrigation pipes under PMKSY, particularly for HDPE drip and sprinkler system supply networks. The presence of major plastic pipe manufacturers in Gujarat, situated on the border of West and North India, further supports supply-chain efficiency for Northern markets.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

South India is emerging as the fastest-growing regional market for pipes in India, driven by a combination of industrial investment, real estate development in major cities, and government infrastructure spending. The Bengaluru and Hyderabad technology corridors are experiencing sustained residential and commercial construction activity that requires extensive plumbing and drainage pipe installation. Chennai is a growing industrial hub with manufacturing zones that create process and utility pipe demand. In March 2025, Ashirvad Pipes announced plans to invest approximately USD 47 million in greenfield manufacturing facilities in Chennai and Hyderabad, targeting production capacity of 4 lakh tonnes per annum by FY2027. This investment reflects manufacturer confidence in the long-term demand growth of South India's pipes market and will simultaneously improve local supply availability and reduce logistics costs for South Indian construction and infrastructure projects.

The India pipes market features a diverse and competitive landscape, with a large number of domestic manufacturers serving distinct material niches, regional markets, and application segments. Market leaders have built national brands through scale, product quality, and distribution reach, while smaller regional players compete on price and proximity to project sites. Government infrastructure programmes like the Jal Jeevan Mission have introduced a parallel institutional procurement channel alongside traditional trade distribution, which is reshaping competitive dynamics as manufacturers build capabilities to win large government tenders.

The competitive environment is intensifying as demand growth attracts new entrants and prompts existing leaders to expand capacity aggressively. Companies with strong certifications, large dealer networks, and the technical capability to supply high-specification products across PVC, HDPE, CPVC, ductile iron, and ERW pipe types are securing stronger competitive positions. The shift toward premium materials such as CPVC and HDPE is creating differentiation opportunities for manufacturers investing in product quality and brand equity.

Jain Irrigation Systems Ltd. is one of India's most prominent irrigation and water management companies, with a strong presence in the agricultural pipe segment through its extensive portfolio of HDPE, PVC, and drip irrigation pipes and systems. Founded in 1963 and headquartered in Jalgaon, Maharashtra, the company has built a vertically integrated business spanning piping, micro-irrigation, and agri-technology. Jain Irrigation's scale of operations, its broad geographic reach across Indian agricultural states, and its established relationships with government irrigation programmes make it a key player in the agricultural pipe segment and a significant supplier to PMKSY-linked procurement.

Founded in 1942 and headquartered in Mumbai, Supreme Industries Ltd. is one of India's largest plastic products manufacturers, with a significant pipe business covering PVC, CPVC, HDPE, and composite pipe products. The company operates a network of manufacturing plants across India and has built an extensive dealer and distributor network that gives it national reach across residential construction, agricultural, and municipal applications. Supreme Industries has consistently invested in new product development and capacity expansion, positioning itself as a premium supplier to both retail and institutional pipe markets.

Astral Poly Technik is a leading Indian manufacturer of CPVC and PVC piping systems, known particularly for its pioneering introduction of CPVC technology in India through a technical collaboration with Lubrizol Corporation of the US. Headquartered in Ahmedabad, Gujarat, Astral has built a strong brand identity around quality and technical credibility in the residential and commercial plumbing segment, where CPVC pipes for hot and cold water distribution are its core market. The company has expanded its product range to include drainage and industrial piping systems and has grown through both organic capacity additions and strategic acquisitions.

Welspun Corp. Ltd. is one of India's leading manufacturers of large-diameter metal pipes, including ERW and helical submerged arc welded (HSAW) steel pipes, serving oil and gas, water transmission, and industrial applications. Headquartered in Mumbai and with manufacturing facilities in Gujarat and Rajasthan, Welspun Corp. has a strong export business alongside its domestic market presence and has participated in major government and private sector pipeline infrastructure projects across India and internationally. The company's technical capability in producing high-specification, large-diameter pipes for critical infrastructure distinguishes it in the metal pipe segment.

Other key players in the market are Jain Irrigation Systems Ltd., Dutron Ltd., Prince Pipes and Fittings Ltd., Ashirvad Pipes Private Limited, Apollo Pipes Limited, APL Apollo Tubes Limited, Kisan Irrigations and Infrastructure Ltd., Jindal SAW Ltd., Finolex Pipes, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Unlock strategic intelligence in India’s expanding pipes market with our detailed 2026-2035 forecast report. Gain clarity on trends, regional demand shifts, and key player strategies. Download a free sample or consult our analysts to explore high-growth segments and upcoming infrastructure-driven opportunities across India.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the India pipes market reached an approximate value of USD 16.01 Billion.

The market is projected to grow at a CAGR of 11.20% between 2026 and 2035.

The market is estimated to witness healthy growth in the forecast period of 2026-2035 to reach a value of around USD 46.28 Billion by 2035.

Key strategies driving the India pipes market include capacity expansion, localization of manufacturing, product innovation in CPVC/HDPE segments, government project partnerships, and targeting export growth to emerging markets.

The key trends of the market include the use of CPVC and HDPE, smart technologies, trenchless installations, and green solutions, due to increasing urbanization, with even more emphasis on agriculture and infrastructure development.

The major regions in the market are North India, South India, West India, and East India.

The various material types considered in the market report are plastic, metal, and concrete.

The various applications considered in the market report are water and sewerage, offices and housing, manufacturing, agriculture, and others.

The diameters considered in the India pipes market report are upto 50mm, 50-100 mm, 100 – 200 mm, 200-400 mm, and above 400 mm.

The key players in the market include Jain Irrigation Systems Ltd., Dutron Ltd., Prince Pipes & Fittings Ltd., Supreme Industries Ltd., Astral Poly Technik, Ashirvad Pipes Private Limited, Apollo Pipes Limited, Welspun Corp. Ltd., APL Apollo Tubes Limited, Kisan Irrigations & Infrastructure Ltd., Jindal SAW Ltd., and Finolex Pipes, among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Material Type |

|

| Breakup by Application |

|

| Breakup by Diameter |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.