Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

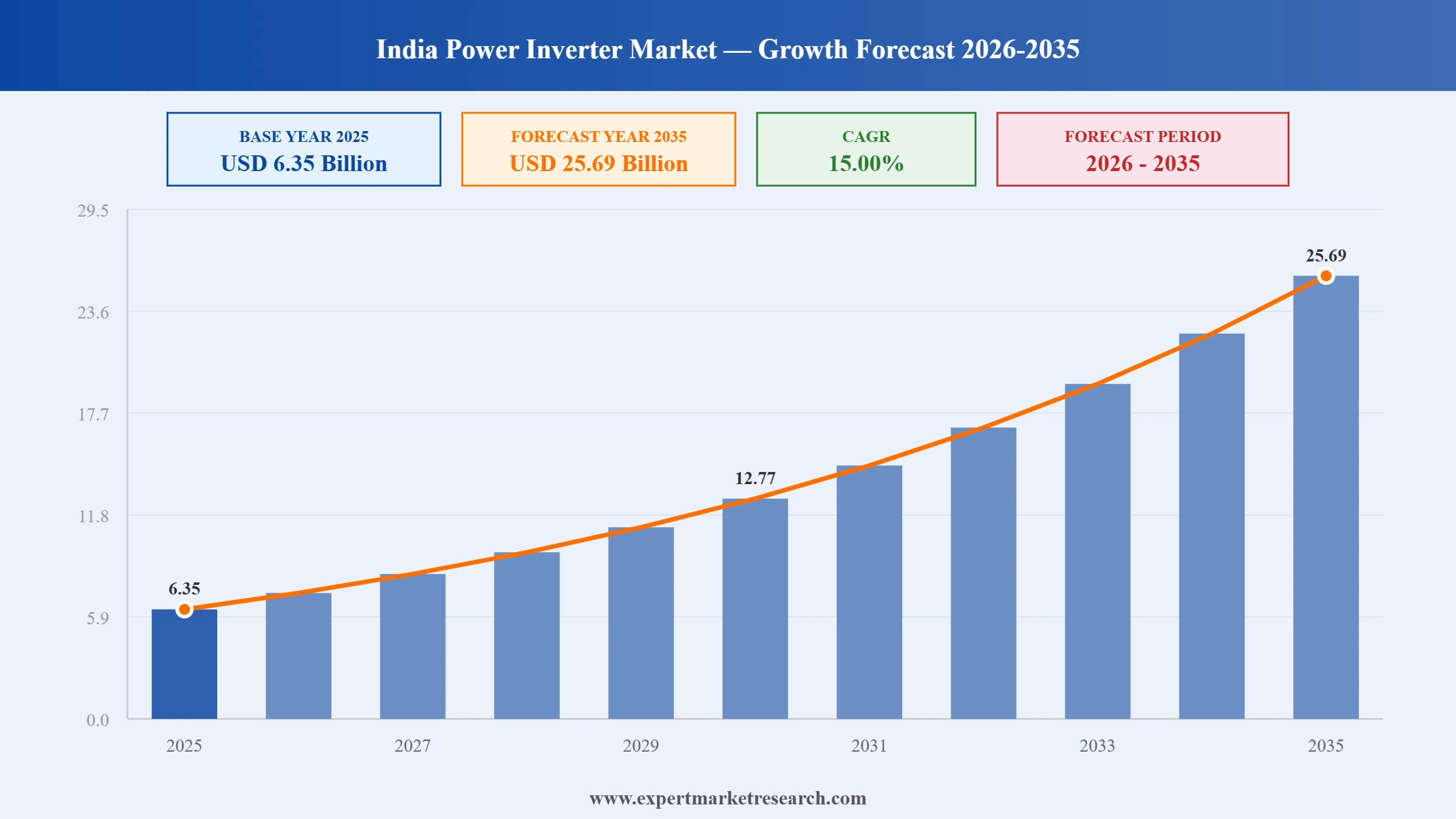

The India power inverter market reached a value of USD 6.35 Billion at 2025 and is projected to expand at a CAGR of around 15.00% during the forecast period of 2026-2035. With accelerating solar PV installations, expanding EV and HEV adoption, government-led rural electrification drives, and growing industrial motor drive applications, the market is expected to reach USD 25.69 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

India's power inverter market is undergoing rapid transformation as renewable energy investment scales up and electric mobility gains ground. Government policy continuity under the Production-Linked Incentive scheme, aggressive solar capacity additions, and expanding EV infrastructure are drawing global technology leaders and domestic specialists to deepen their India-specific product and service commitments.

India's Ministry of New and Renewable Energy paused its annual renewable energy tender targets after the unexecuted project pipeline reached 43 GW, raising concerns about project execution timelines and near-term inverter procurement schedules.

TBEA launched its TS500KTL-HV-C1 500 kW string inverter for utility-scale solar and solar-plus-storage projects, featuring third-generation silicon carbide semiconductors, a 1,600 Vdc high-voltage architecture, and grid-forming capabilities for weak-grid environments including India's large-scale ground-mounted solar plants.

India recorded its highest-ever quarterly solar installation figure of 15.3 GW in January-March 2026, a 143% year-on-year increase, with rooftop solar contributing 2.7 GW and the residential segment accounting for 82% of rooftop capacity driven by PM Surya Ghar subsidies.

India's cumulative renewable energy capacity reached 275 GW by the end of March 2026 as the country added 44.6 GW of solar and 6 GW of wind in FY 2025-26, with non-fossil fuel sources now accounting for 42.2% of total installed electricity generation capacity.

India's accelerating solar capacity additions directly translate into inverter demand. With the country targeting 500 GW of renewable capacity by 2030 and more than 110 GW already commissioned, the India power inverter market continues to scale through utility and rooftop deployments at an unprecedented pace.

Rising EV adoption is opening a significant new demand vector across the India power inverter market. India recorded approximately 1.7 million EV sales in FY2024, with each vehicle requiring onboard traction inverters and contributing to charging infrastructure demand across automotive and transportation end uses.

Smart inverters with real-time monitoring and grid-support capabilities are replacing legacy DC-AC converters in India. Companies including ABB, SMA Solar, and SolarEdge are deploying IoT-integrated inverter platforms in the C&I sector, improving fleet management, uptime, and regulatory compliance in the India power inverter market.

Motor drives remain the most established inverter application in Indian manufacturing, covering pumps, compressors, conveyors, and HVAC systems. Expansion of factory capacity under the Production-Linked Incentive program continues to generate steady baseline demand for variable frequency drives and motor drive inverters across industrial verticals.

Schemes including PM Kusum and the Deen Dayal Upadhyaya Gram Jyoti Yojana have extended power inverter deployment to rural households and agricultural users. Policy-backed off-grid solar adoption is broadening the India power inverter market beyond urban and industrial centres to include underserved rural communities.

“India Power Inverter Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

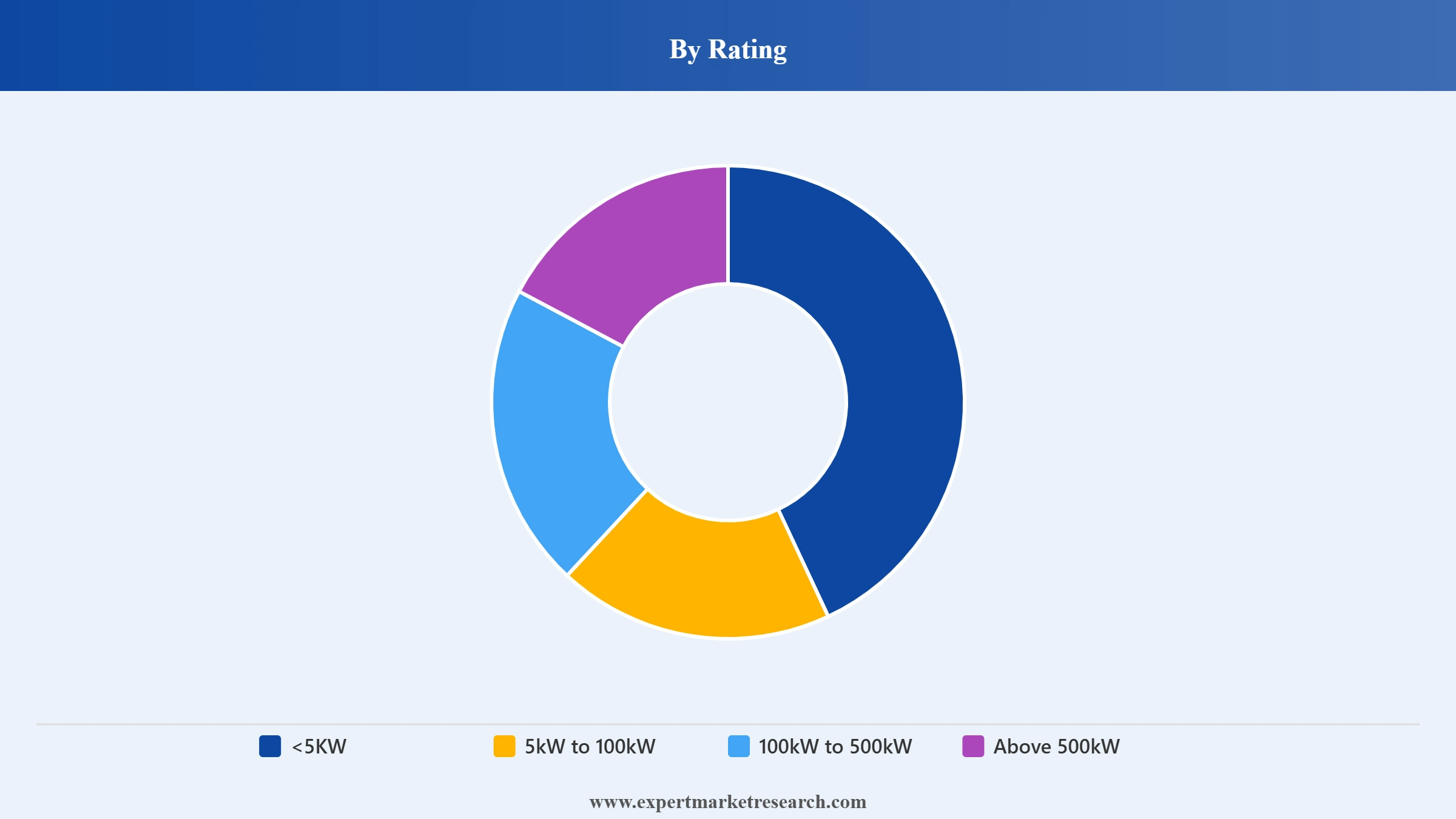

Breakup by Rating

Key Insight: The sub-5kW rating segment leads by unit volume, serving millions of residential rooftop solar users and households seeking backup power during outages. The 5kW to 100kW band covers the growing C&I solar and industrial automation segment, where PLI-backed manufacturing expansion sustains consistent demand. Utility-scale ratings above 500kW are the fastest-growing power band, anchored by India's large-scale solar parks and ISTS-connected projects that procure high-power string and central inverters in bulk across the India power inverter market.

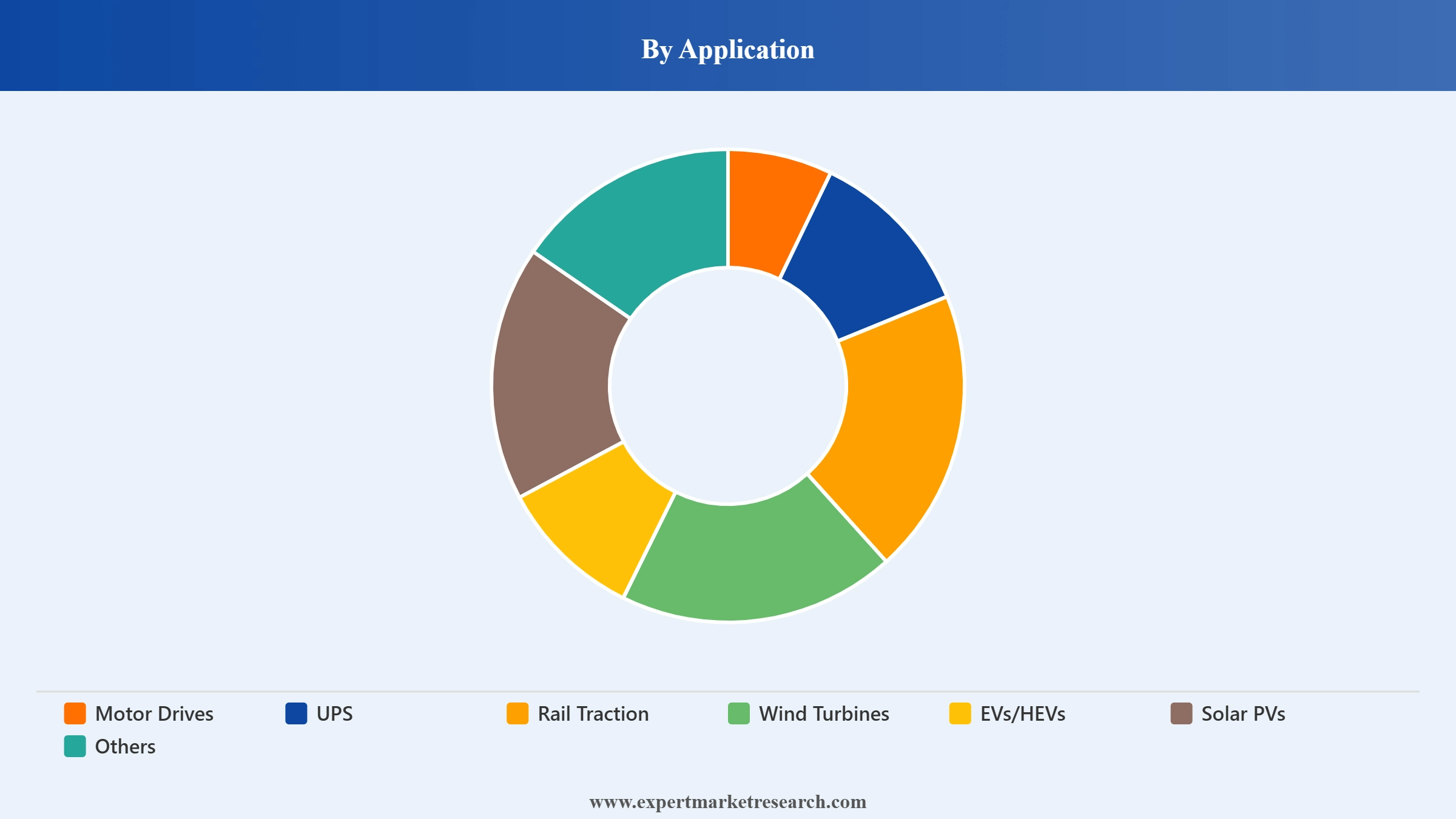

Breakup by Application

Key Insight: Solar PVs command the largest application share, driven by surging grid-scale and rooftop solar capacity additions under India's ambitious renewable targets. Motor drives remain the foundational industrial application, supporting manufacturing automation at scale. EVs/HEVs represent the fastest-growing application, propelled by India's national electric mobility mission and rising EV penetration. Rail traction is a structurally growing niche as Indian Railways electrifies its broad-gauge network, generating long-term demand for high-power traction inverters across the India power inverter market.

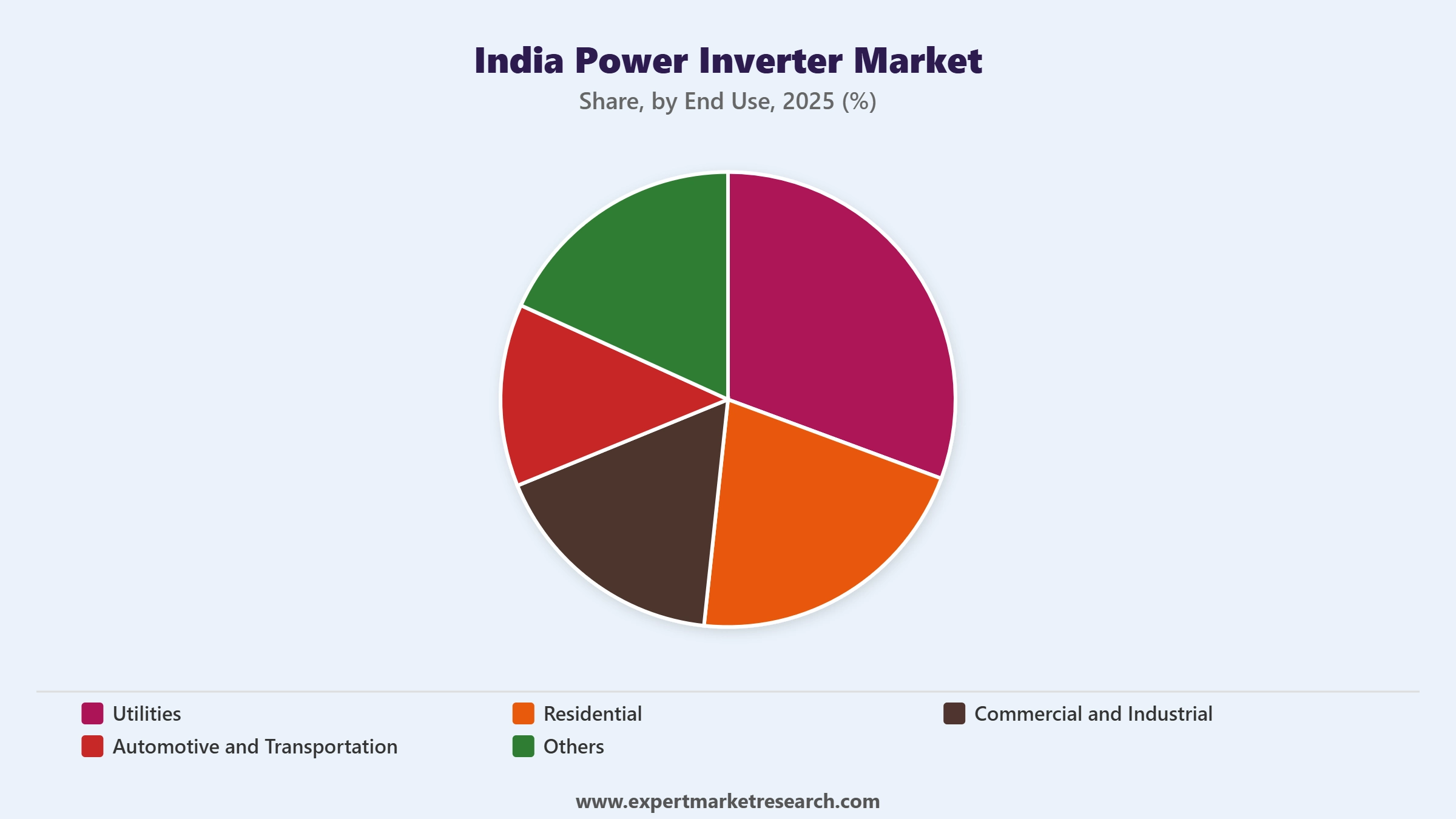

Breakup by End Use

Key Insight: Utilities hold the dominant end-use share because large-scale solar parks and wind farms require central and string inverters procured in high volumes by power developers and state electricity boards. Residential is the fastest-growing end use, fuelled by subsidised rooftop solar schemes and rising consumer demand for energy autonomy. Commercial and industrial benefits from PLI-driven manufacturing expansion. Automotive and transportation is an emerging, fast-scaling end use tied directly to India's accelerating EV deployment and supporting charging infrastructure rollout.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By rating, the sub-5kW segment dominates the market due to high residential and small rooftop solar volumes

The sub-5kW power rating segment leads the India power inverter market by unit volume, primarily serving the large number of residential households deploying rooftop solar systems and seeking reliable backup during grid outages. India's high solar irradiance, declining module prices, and government subsidy schemes have made small-scale solar a standard household investment, generating consistent demand for compact, affordable inverters in this power band across urban and semi-urban areas.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Higher-wattage inverters in the 5kW to 100kW band are capturing increasing commercial share as enterprises replace diesel generators with solar-plus-storage systems. In December 2025, Sungrow's newly launched 75 kW inverter for India's C&I segment directly addressed this growing demand, with features tailored for bifacial panel compatibility and shade-tolerant, high-efficiency operation, reinforcing the shift towards clean energy alternatives in the India power inverter market.

By application, solar PVs account for the dominant share of the market due to India's rapid renewable capacity expansion

Solar PV applications drive the largest share within the India power inverter market because the country is deploying utility-scale solar parks and rooftop systems at an accelerating pace to meet its 500 GW non-fossil energy target. Grid-tied string and central inverters are standard components of these installations, and every megawatt of commissioned solar capacity generates a corresponding inverter procurement requirement across utilities, C&I, and residential segments.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

EVs and HEVs represent the fastest-growing application, as electric passenger cars, two-wheelers, and three-wheelers enter the market in rising numbers. In September 2025, Huawei deepened its Indian presence through expanded local distributor partnerships, enabling faster deployment of its power electronics and enabling it to serve the growing traction inverter and EV charging demand emerging across the India power inverter market.

By end use, utilities dominate the market due to bulk procurement for large-scale solar and wind installations

The utilities segment commands the largest end-use share of the India power inverter market because large-scale solar parks and wind farms require high-capacity inverters procured in bulk by power developers and state electricity boards. India's ongoing capacity addition programmes and competitive renewable energy tariff auctions have created a reliable and growing procurement pipeline, making utilities the most consistent and highest-volume demand channel for inverter suppliers.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The residential segment is the fastest-growing end use, fuelled by rising rooftop solar adoption, falling system costs, and government programmes promoting energy self-sufficiency. In November 2025, Sungrow's new residential PV and ESS system featuring the MG5/6RL inverter and paired battery module reflected how leading manufacturers are developing integrated home energy platforms to capture the residential segment's expanding base within the India power inverter market.

The India power inverter market is moderately concentrated at the top tier, with global technology leaders competing alongside domestic manufacturers on inverter efficiency, smart grid compatibility, service network reach, and ALMM compliance. Chinese manufacturers including Huawei and Sungrow dominate utility-scale solar installations, while European players such as ABB and SMA hold strong positions in industrial and commercial segments. Indian companies like Genus Power serve the residential and small-commercial backup power segment through extensive distribution.

Competition increasingly centres on smart inverter features, IoT integration, after-sales support, and localisation of manufacturing and servicing under India's regulatory requirements for approved product lists.

Swiss multinational founded in 1988, headquartered in Zurich, with a broad power electronics and automation portfolio. ABB supplies string and central inverters for solar plants and drive systems for industrial applications in India, backed by an extensive local service network. Its focus on grid-connected inverter solutions and industrial motor drives positions it as a preferred supplier for large C&I and utility-scale projects.

Chinese technology conglomerate founded in 1987, headquartered in Shenzhen, with a leading Digital Power division supplying string inverters for utility-scale solar in India. Huawei's Smart PV inverter range integrates AI-driven diagnostics and remote monitoring, and the company has expanded its Indian distribution network to support its growing installed base across major solar parks and C&I installations.

Taiwanese power management company founded in 1971, headquartered in New Taipei City. Delta offers a comprehensive inverter range covering solar PV, UPS, and motor drive applications. Its India operations benefit from a manufacturing presence and a wide distribution network serving residential, commercial, and industrial customers across the country.

Indian subsidiary of German solar technology company SMA Solar Technology AG, founded in 1981. SMA's Sunny Tripower and Sunny Central product families serve residential, C&I, and utility-scale solar installations in India. Its reputation for product reliability and grid compliance makes it a preferred choice in commercial and industrial deployments where quality assurance is a primary purchase criterion.

Other key players in the market are Genus Power Infrastructures Ltd, SolarEdge Technologies Inc., and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

The India power inverter market faces significant operational challenges driven by import dependence and grid integration complexity. A substantial share of inverter bill-of-material value including high-voltage silicon carbide modules and advanced power semiconductors is sourced from China, Taiwan, and Southeast Asia, creating supply chain vulnerability to geopolitical disruption and currency depreciation. Grid integration challenges around inverter stability, reactive power management, and curtailment further strain operational performance across utility-scale solar installations.

Structural restraints moderate the pace of market formalisation and technology upgrade cycles. The Bureau of Energy Efficiency's Standards and Labelling Programme for grid-connected solar inverters creates compliance cost burdens that disproportionately affect smaller domestic manufacturers with limited R&D capacity. A large unexecuted project pipeline driven by land acquisition delays, transmission readiness gaps, and offtake agreement bottlenecks continues to delay inverter procurement cycles and create near-term revenue uncertainty for manufacturers.

Despite these headwinds, the market presents compelling growth opportunities across residential, commercial, and utility segments. The PM Surya Ghar subsidy scheme is driving residential rooftop solar adoption at scale, sustaining demand for string and micro-inverters in the household segment. The repowering and retrofit of ageing solar plants is creating a structural secondary demand stream for higher-efficiency replacement inverters, while India's commitment to expanding non-fossil fuel electricity capacity provides a durable long-term demand foundation for manufacturers investing in domestic production and technology localisation.

Stay ahead in India's rapidly expanding energy landscape with our latest report on the India power inverter market 2026. Gain clarity on where solar PV growth, electric mobility, and industrial automation are creating the highest-value demand pockets. Whether you are a technology supplier, EPC contractor, utility, or investor, this report gives you the intelligence to act with confidence. Download your free sample today and explore the key opportunities shaping India's power electronics landscape.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market reached an approximate value of USD 6.35 Billion.

The market is projected to grow at a CAGR of 15.00% between 2026 and 2035.

The market is estimated to witness healthy growth in the forecast period of 2026-2035 to reach a value of around USD 25.69 Billion by 2035.

The market is being aided by the growing use of power inverters in the residential sector, rapid urbanisation, and the rising adoption of power inverters in utility operations.

The market is expected to be bolstered by the rising penetration of smart power inverters, the rising exploration of solar energy, and the growing manufacturing of power inverters in the country.

The power ratings for inverters in the market are <5KW, 5kW to 100kW, 100kW to 500kW, and above 500kW.

The various applications of power inverter are motor drives, UPS, rail traction, wind turbines, EVs/HEVs, and solar PVs, among others.

The significant end uses in the market are utilities, residential, commercial and industrial, and automotive and transportation, among others.

The major players in the market are ABB Ltd., Huawei Technologies Co., Ltd., Delta Electronics, Inc., SMA Solar India Private Limited, Genus Power Infrastructures Ltd, and SolarEdge Technologies Inc., among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Rating |

|

| Breakup by Application |

|

| Breakup by End Use |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

| Report Price and Purchase Option | Explore our purchase options that are best suited to your resources and industry needs. |

| Delivery Format | Delivered as an attached PDF and Excel through email, with an option of receiving an editable PPT, according to the purchase option. |

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.