Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

The India pre-school/childcare market reached a value of USD 5.59 Billion at 2025 and is projected to expand at a CAGR of around 10.50% during the forecast period of 2026-2035. With rising women's workforce participation, NEP 2020-aligned curricula, rapid franchise-led Tier 2 and Tier 3 expansion, and growing parent-tech integration, the market is expected to reach USD 15.17 Billion by 2035.

Compound Annual Growth Rate

10.5%

Value in USD Billion

2026-2035

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

India's preschool/childcare market is being reshaped by four converging forces - private-equity-led network consolidation, NEP 2020-aligned curriculum modernisation, rapid Tier 2 and Tier 3 franchise expansion, and integration of parent-tech and digital tools across early childhood education.

Coverage of the Indian preschool sector through late 2025 highlighted Lighthouse Learning's 34% revenue jump to Rs 881 crore in FY25, alongside ongoing Tier 2/Tier 3 franchise expansion across the EuroKids and EuroSchool networks. The financial performance validates the franchise-led, K-12-anchored business model and provides a benchmark for premium private preschool operators. Industry coverage also flags Kidzee's 1,900+ centre footprint and Bachpan's continued franchise growth across Tier 2 and Tier 3 cities.

The Insights on India review on child care in India highlighted the operational restructuring of the National Crèche Scheme into the Palna Scheme under Mission Shakti, alongside complementary initiatives Mission Saksham Anganwadi and Poshan 2.0. These programmes create a public-sector funnel for working mothers, expanding India's overall childcare access. They also create demand for private operators in metro and Tier 2 cities, where Anganwadi and Palna alone are unable to meet rising demand for premium and bilingual preschool/daycare services.

EuroKids' network expanded to over 2,200 preschool and early-learning centres across more than 500 cities and towns, serving 300,000+ enrolled children and employing over 25,000 qualified educators. The brand is actively encouraging franchise partnerships in Tier 2 and Tier 3 cities, where demand for quality early childhood education is growing rapidly. Total investment to start a EuroKids franchise stands at ₹15–20 lakhs, covering setup, furniture, teaching aids, curriculum materials, and initial operational support.

KKR, alongside Canada's PSP Investments, made a fresh investment in Lighthouse Learning Group - the parent of EuroKids, Kangaroo Kids, EuroSchool, Billabong High International, Centre Point Group, and Heritage International Xperiential School - to support the next phase of growth. Lighthouse Learning reported revenue of Rs 881 crore in FY25, a 34% jump year-on-year, and operates over 1,850 preschools and 60 K-12 schools serving 190,000+ students daily. The capital injection signals continued investor conviction in India's premium preschool franchise model.

The Ministry of Women and Child Development launched the National Curriculum for Early Childhood Care and Education for children three to six years and the National Framework for Early Childhood Stimulation for children from birth to three. Both frameworks align with the National Curriculum Framework for Foundational Stage 2022 under NEP 2020 and cover physical/motor, cognitive, language, socioemotional, and cultural domains. While slightly older than the 24-month freshness window, this is a foundational regulatory development that frames every preschool/childcare offering through 2035.

Global private-equity firms continue to back Indian preschool networks. KKR's November 2025 fresh investment in Lighthouse Learning, alongside PSP Investments, signals that India's preschool franchise model now sits among Asia's most fundable consumer-services categories. Lighthouse's FY25 revenue of Rs 881 crore (+34% YoY) anchors the investment thesis. Consolidation is also broadening: networks now span preschool, K-12, experiential learning, and curriculum partnerships, raising entry barriers for stand-alone players. The India pre-school/childcare market growth is tightly linked to private-capital deployment.

Foundational learning has been formally embedded into the preschool experience. The National Curriculum for ECCE (3–6 years) and the National Framework for Early Childhood Stimulation (birth to 3 years) - both launched in April 2024 - operationalise NEP 2020's foundational stage and require preschools to offer multilingual instruction, structured learning outcomes, and developmentally appropriate domains. Preschools now compete on curriculum credibility and documented learning outcomes, advantaging branded operators with central R&D and teacher-training capability over unbranded local operators.

EuroKids' December 2025 milestone of 2,200+ centres across 500+ cities, alongside Kidzee's 1,900+ centre network, confirms that growth is now concentrated in Tier 2 and Tier 3 cities rather than metros. Drivers include rising disposable incomes, growing nuclear families, and parental aspiration for early-stage English-medium and structured-learning environments. Franchise investments of ₹15–20 lakhs offer reasonable payback periods for local entrepreneurs, supporting sustained network expansion through 2035.

The restructuring of the National Crèche Scheme into the Palna Scheme under Mission Shakti, alongside Mission Saksham Anganwadi and Poshan 2.0, expands public-sector childcare access for working mothers. While these programmes serve lower-income segments, they also widen the broader demand funnel for early childhood services and create policy tailwinds. Premium private operators (EuroKids, Kidzee, Bachpan, Shemrock, Hello Kids, Little Millennium) capture metro and Tier 2 demand that public schemes cannot fully address.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The Expert Market Research’s report titled “India Pre-School/Childcare Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

Market Breakup by Facility

Key Insight: Full Day Care is the dominant facility type because it directly serves working parents in nuclear-family households across metros and Tier 2 cities, and its higher fee structure supports network economics. After School Care is smaller but growing, especially in Tier 2 cities, where dual-income families increasingly demand structured care for school-age children. Both categories benefit from NEP 2020-aligned foundational learning and from KKR-backed Lighthouse Learning's ongoing premium-tier expansion.

Market Breakup by Ownership

Key Insight: Private ownership dominates by both revenue and unit count. Branded private networks - EuroKids/Lighthouse, Kidzee, Bachpan, Shemrock, Hello Kids, Little Millennium - anchor Tier 1, Tier 2, and Tier 3 demand. Public ownership (Anganwadi-linked centres, Palna Scheme) expands access for lower-income segments through Mission Shakti, but the bulk of premium and mid-market demand sits in private operators. Standalone independent preschools remain the long-tail cohort in non-metro markets.

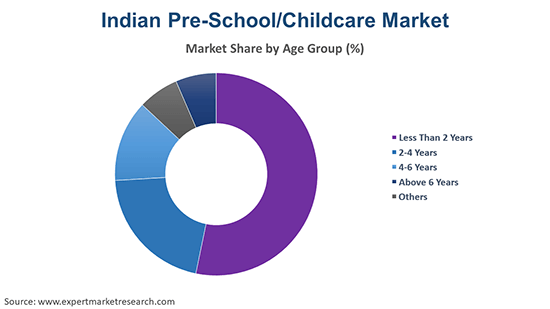

Market Breakup by Age Group

Key Insight: The 2–4 years age band remains the largest revenue contributor because it captures the foundational stage that NEP 2020 emphasises. The under-2 segment is fastest-growing in metros, supported by working mothers needing infant daycare. The 4–6 years cohort is the Junior KG–Senior KG bridge, often co-located with K-12 schools. Above 6 years (after-school) is smaller but growing in dual-income Tier 2 households.

Market Breakup by Location

Key Insight: Standalone facilities are the largest sub-segment by unit count, anchored by franchise networks. School-premises preschools are a strategic asset for K-12-anchored groups (Lighthouse Learning) because they create natural progression into Junior KG and beyond. Office-premises daycare is fastest-growing - corporates partner with operators to offer infant and toddler care as an employee benefit, particularly in Bengaluru, Hyderabad, Mumbai and Delhi NCR.

Market Breakup by Major Cities

Key Insight: Delhi-NCR and Bengaluru alternate as the largest urban markets - Delhi-NCR by school density, Bengaluru by working-mother concentration. Hyderabad's IT cluster and Chennai's manufacturing/IT base drive premium demand. Mumbai and Kolkata anchor regional networks. Rest of India captures the rapidly expanding Tier 2/Tier 3 base where EuroKids and Kidzee are scaling.

Market Breakup by Region

Key Insight: South India and West/Central India lead market value, anchored by Bengaluru, Hyderabad, Chennai, Mumbai, and Pune - cities with high working-women density and dense corporate clusters. North India (Delhi-NCR) follows closely, while East India (Kolkata) is a smaller but growing market.

By Facility: Full Day Care holds the dominant share of the facility split because it aligns with the structural rise in nuclear families and dual-income households across metros and Tier 2 cities. EuroKids and Kidzee both lead through Full Day Care offerings. The supporting evidence is Lighthouse Learning's 34% YoY revenue growth in FY25 to Rs 881 crore - driven by Full Day Care expansion across the EuroKids network - and confirmed in November 2025 KKR investor disclosures, validating Full Day Care as the primary growth engine.

By Ownership: Private ownership commands the dominant share of the market because branded networks have built scale, brand equity, and franchise economics that public schemes (Palna, Anganwadi) do not replicate at premium price points. The supporting evidence is the December 2025 milestone of EuroKids' 2,200+ centres across 500+ cities, alongside Kidzee's 1,900+ centre footprint - both private - and the absence of comparable scale among public-sector operators in premium and mid-market segments.

By Age Group: The 2–4 years age band holds the largest share, capturing the foundational early childhood stage that the NEP 2020-aligned 2024 ECCE National Curriculum formalised. Parents increasingly enrol children at the earliest age of 2 to access structured English-medium environments and developmental tracking. The supporting evidence is the 2024 PIB launch of the National Curriculum for ECCE 3–6 Years, which explicitly positions this band as the foundational stage and underwrites the segment's leadership in industry revenue.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

South India: South India is the largest regional cluster, anchored by Bengaluru, Hyderabad, and Chennai. Drivers include high female labour-force participation, dense IT and IT-services clusters supporting dual-income families, and a strong franchise penetration of EuroKids, Kidzee, Hello Kids, and Little Millennium. Investment is flowing into office-premises daycare partnerships with tech corporates, alongside Tier 2 expansion to Coimbatore, Mysuru, Visakhapatnam, and Madurai. Statistics show Lighthouse Learning's premium EuroSchool and EuroKids networks are particularly active in South India, with the region accounting for a meaningful share of total enrolment.

West and Central India: The West and Central India region - anchored by Mumbai, Pune, Ahmedabad, Hyderabad-adjacent zones, and Indore - is the second-largest market by value. Drivers include high disposable incomes, large corporate clusters, and dense mid-market and premium private school ecosystems. Mumbai and Pune lead in office-premises daycare partnerships with banking, FMCG, and IT corporates. Investment is also flowing into Tier 2 cities (Nashik, Aurangabad, Surat, Vadodara) where franchise costs are lower and parental willingness to pay for English-medium preschool remains strong. Lighthouse Learning's K-12 schools (Billabong, EuroSchool, Centre Point) are also concentrated here.

The India pre-school/childcare market is fragmented at the long tail and moderately consolidated at the top, with branded franchise networks (EuroKids/Lighthouse, Kidzee, Bachpan, Shemrock, Hello Kids, Little Millennium) capturing the majority of mid-market and premium demand. Competitive priorities have shifted from raw network expansion toward NEP 2020-aligned curriculum credibility, parent-tech integration, multilingual instruction, and corporate B2B partnerships.

The next layer is dynamic: regional networks, edu-tech-enabled standalones, and corporate-backed operators continue to expand in Tier 2 and Tier 3 cities. Multinationals respond through private-equity-led consolidation (KKR's repeat investment in Lighthouse) and through K-12 integration that turns preschool customers into long-cycle K-12 enrolments - making the second tier a meaningful competitive battleground.

Founded in 2003 and headquartered in Mumbai, India, Kidzee is one of Asia's largest preschool chains, operating 1,900+ centres in India. Capabilities span proprietary curriculum (Mi+ programme), franchise training, and a scalable delivery model. Strengths include a Tier 2 and Tier 3 city footprint, parent-tech integration, and recognition as a leading brand for structured early-childhood learning.

Founded in 2004 and headquartered in Delhi, India, Bachpan is a major franchise-led preschool network with strong Tier 2 and Tier 3 presence across North and Central India. Capabilities include curriculum design, teacher training, and franchise support across hundreds of centres. Strengths sit in pricing accessibility, regional distribution depth, and a long-standing presence in non-metro markets.

Founded in 2001 and headquartered in Mumbai, India, EuroKids is the flagship preschool brand of Lighthouse Learning Group (KKR-backed) with 2,200+ centres across 500+ cities, 300,000+ enrolled children, and 25,000+ qualified educators. Capabilities span proprietary curriculum, parent-tech tools, K-12 integration via EuroSchool and Billabong, and a deep franchise-support engine. Strengths include scale, K-12 progression, and access to PE-backed capital.

Founded in 1989 and headquartered in Delhi, India, Shemrock is one of India's earliest preschool networks, with hundreds of centres across the country. Capabilities include play-based curriculum, franchise training, and steady expansion across North, West, and Central India. Strengths include heritage credibility, strong parent loyalty in metros, and long-tenured centre managers across the network.

Other key players in the market are Hello Kids Education India Pvt., Little Millennium, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Discover the latest insights on the India pre-school/childcare market 2026 with our comprehensive report. Stay ahead of the curve with verified data on franchise expansion, NEP 2020 alignment, working-women workforce dynamics, and the strategies of EuroKids, Kidzee, Bachpan, Shemrock, Hello Kids, and Little Millennium. Whether you are launching a new centre, investing in a franchise network, or designing a corporate daycare benefit, this report gives you the clarity you need. Download your free sample now and discover the key opportunities in the thriving India Pre-School/Childcare space.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

At 2025, the market reached an approximate value of USD 5.59 Billion.

The market is projected to grow at a CAGR of 10.50% between 2026 and 2035.

The market is projected to grow significantly during the forecast period 2026 - 2035. to reach USD 15.17 Billion by 2035.

Growth is driven by the rising number of nuclear families, increasing women's labour-force participation, NEP 2020-aligned ECCE foundational curriculum, rapid Tier 2 and Tier 3 franchise expansion (EuroKids, Kidzee), private-equity-backed consolidation (KKR's repeat investment in Lighthouse Learning), and corporate-sponsored office daycare partnerships.

The market is segmented into Full Day Care and After School Care. Full Day Care is the dominant facility type, supported by working parents in nuclear-family households across metros and Tier 2 cities; After School Care is smaller but growing in dual-income Tier 2 cities.

Private-equity-led network consolidation; NEP 2020-aligned foundational curriculum rollout; rapid Tier 2 and Tier 3 city franchise expansion; expansion of public childcare programmes (Palna Scheme); and corporate-led office daycare partnerships.

The key players in the market include Kidzee, Bachpan, EuroKids (Lighthouse Learning), Shemrock, Hello Kids Education India Pvt., Little Millennium and Others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Facility |

|

| Breakup by Ownership |

|

| Breakup by Age Group |

|

| Breakup by Location |

|

| Breakup by Major cities |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

| Report Price and Purchase Option | Explore our purchase options that are best suited to your resources and industry needs. |

| Delivery Format | Delivered as an attached PDF and Excel through email, with an option of receiving an editable PPT, according to the purchase option. |

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.