Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

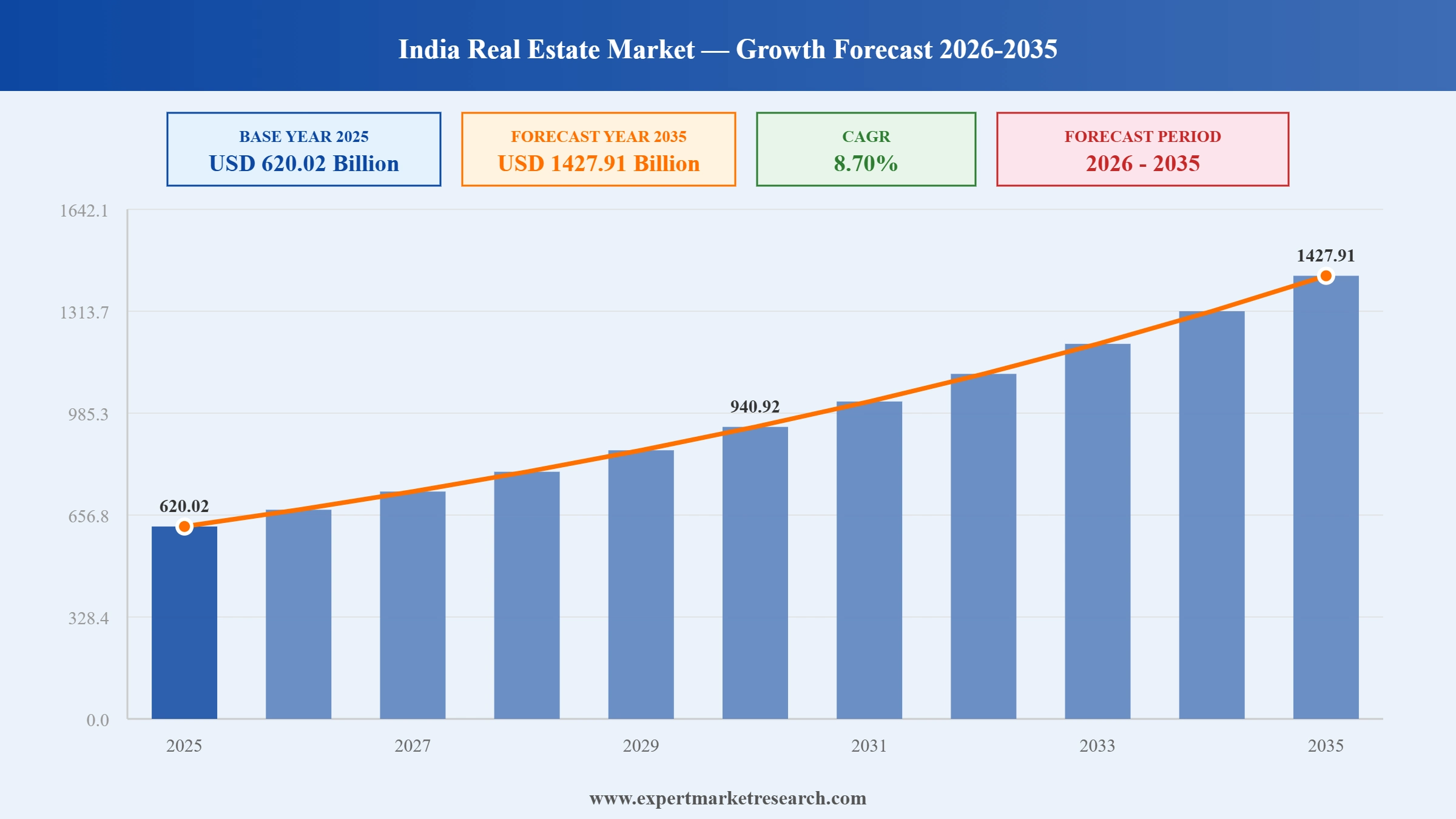

The India real estate market attained a value of USD 620.02 Billion in 2025 and is projected to expand at a CAGR of 8.70% through 2035. The market is further expected to achieve USD 1427.91 Billion by 2035. The rapid growth in the number of global capability centers, data center campuses, and logistics infrastructure is fueling the need for large-scale commercial real estate properties, prompting developers to adopt technology-driven, high-value real estate concepts.

According to Business Standard, capital inflows into India's real estate sector reached a historic USD 5.1 billion in the first quarter of 2026, marking a 72% year-on-year rise from USD 2.9 billion in Q1 2025. Domestic investors dominated with a 96% share, led by developers and REITs. The surge, driven by strong demand for premium office and residential assets, signals deepening institutional confidence in the India real estate market.

According to Outlook Money, India's residential real estate market recorded housing sales exceeding 6 lakh units in 2025, with an estimated total value of Rs 8.4 lakh crore. Homes priced above Rs 1 crore accounted for 78% of total sales, underlining a decisive shift toward premiumisation. Rising incomes, RBI rate cuts, and urbanisation are fuelling sustained demand across major metro markets, further strengthening the India real estate market outlook.

One of the important growth factors in the India real estate market is the active involvement of institutional investors in commercial and mixed-use real estate developments, allowing developers to execute bigger and more advanced projects with improved governance frameworks. Another important factor is the growing demand for Grade A offices by multinationals for expanding their engineering, technology, and business service operations across the country. This is inspiring top developers to focus on premium asset development, improving efficiency, and creating recurring income streams through diversified real estate investments.

The India real estate market is witnessing a substantial amount of change as the leading developers are increasingly adopting modern technology-driven infrastructure, mixed-use assets, and institutional quality investment platform. One of the key trends was made evident by the expansion by DLF Limited in its premium commercial and luxury residential assets across major Indian cities in May 2025. According to estimates by DLF, the 2027 outlook of the company maintains record levels of sales bookings amounting to over INR 20,000 crore driven by high end residential projects and premium urban assets.

Moreover, another key trend in the India real estate market is the adoption of an integrated approach by leading real estate companies to develop residential, retail, hospitality, and office spaces within the same project. Some of the prominent companies including Godrej Properties, Prestige group, Lodha and Oberoi Realty, are increasing investment in township developments backed by digital property management, green buildings, and smart mobility infrastructure. On the other hand, in June 2026, Harmony Infra Ventures acquired full ownership of Horizon Residences, strengthening luxury housing development in Ghaziabad. At the same time, investments by institutional investors are making developers opt for an asset-light business model with improved execution capabilities.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

| India Real Estate Market Report Summary |

Description |

Value |

|

Base Year |

USD Billion |

2025 |

|

Historical Period |

USD Billion |

2019-2025 |

|

Forecast Period |

USD Billion |

2026-2035 |

|

Market Size 2025 |

USD Billion |

620.02 |

|

Market Size 2035 |

USD Billion |

1427.91 |

|

CAGR 2019-2025 |

Percentage |

XX% |

|

CAGR 2026-2035 |

Percentage |

8.70% |

|

CAGR 2026-2035 - Market by Region |

North India |

9.6% |

|

CAGR 2026-2035 - Market by Region |

West India |

8.4% |

|

CAGR 2026-2035 - Market by Property |

Residential |

10.8% |

|

CAGR 2026-2035 - Market by Type |

Sales |

12.1% |

| 2025 Market Share by Region | North India | 31.0% |

Tulip Infratech launched the luxury project called Tulip Melrose located in Southern Peripheral Road, Gurugram. This launch demonstrates the increase in the need for luxurious homes in highly connected urban areas, which motivates developers to launch landmarks in residential real estate projects for the upper-class sector, thereby boosting the India real estate market growth.

Mahindra Lifespaces announced the launch of a project called Codename Sanctum. It is situated in Mahindra Citadel and consists of limited 2 and 3 BHK residences. These homes have efficient layouts along with nature-inspired designs. The launch of such an integrated township signifies the continuous need for premium homes within an integrated community. Builders can focus on launching their mid-sized luxury apartments in urban locations.

Significant growth initiatives and luxury residential development were achieved by Prestige Group. This indicates high investor confidence and increased demand for branded residential complexes. Thus, India real estate market companies can benefit from the increase in the demand for branded residential properties by focusing on their pipeline of premium projects in metropolitan areas.

Marubeni invested in the residential project of Kolte-Patil’s township in Pune. This is the fifth residential investment by Marubeni in India, which will help develop about 900 residential units. This shows the growing interest of international investors in the development of residential property in India. Developers can therefore bring foreign investment into their residential projects via their township development projects.

Prominent developers are shifting their attention towards integrated township projects that encompass all residential, retail, commercial, health care, and education infrastructure into one ecosystem. This trend in the India real estate market is aiding developers in creating diversified income sources and making projects more attractive for institutional investors. For example, Godrej Properties, Prestige Group, and DLF are scaling up their mixed-use development portfolio in key metropolitan areas taking advantage of the growth in urbanization. In addition, government policies like Smart Cities Mission are enabling upgrades of infrastructural projects in urban agglomerations. In June 2026, Bhartiya Urban launched Nikoo Homes 8 in North Bengaluru, investing INR 1,000 crore across 1,000 premium residences.

Data centers are becoming an extremely important real estate vertical due to increased cloud computing, artificial intelligence workloads, and digitalization in India. Developers are collaborating with technologically-driven companies and global investors to create a large campus-like structure of data centers in business locations, boosting the India real estate market opportunities. For example, in October 2025, Adani ConneX announced plans to invest significantly in Chennai, Noida, Hyderabad, and Navi Mumbai with a view to establishing data centers by 2035.

The rise of GCCs is expected to fuel the increasing need for high-end office spaces in key business hubs of India. Corporates are setting up their engineering, research, analytics, and business services departments in cities like Bengaluru, Hyderabad, Pune, and Chennai. Real estate developers like Embassy Office Parks, DLF, and RMZ are meeting their demands through the development of Grade A office spaces with smart technology and sustainability measures. As international businesses continue to favor efficiency and talent availability, premium office investments are expected to be an important growth sector in the country. In April 2026, Pi Data Centers partnered with JLL to accelerate a 23MW AI-ready data center expansion, creating new opportunities in the India real estate market.

Environmental sustainability is becoming a significant point of differentiation for many real estate firms looking to attract institutional investment and multinationals as tenants. Many real estate developers are undertaking projects certified by LEED and IGBC, including renewable energy solutions, energy efficiency, water management techniques, and sustainable construction materials. This includes Lodha and Mahindra Lifespaces which are expanding their portfolio of green buildings. Green initiatives by the government are further promoting such practices in the India real estate market. In March 2026, IFC, GBPN, and Smarter Dharma launched MGEM, enabling access to verified green materials and sustainable construction financing.

Fast-moving developments in e-commerce, manufacturing investments, and modernizing the supply chain are driving increased demand for bulk logistics and industrial space, accelerating demand in the India real estate market. Real estate developers are busy building their logistics space portfolio close to transport routes and industrial estates. Several logistics companies such as ESR, IndoSpace, and Blackstone logistics are continuously setting up logistics parks that incorporate state-of-the-art infrastructure for automated systems and effective inventory management. Government efforts such as the PM Gati Shakti National Master Plan and industrial corridor projects are enhancing connectivity in the country. In November 2025, IndoSpace Core acquired six logistics parks worth INR 3,000 crore, strengthening India's industrial real estate footprint.

The Expert Market Research's report titled “India Real Estate Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

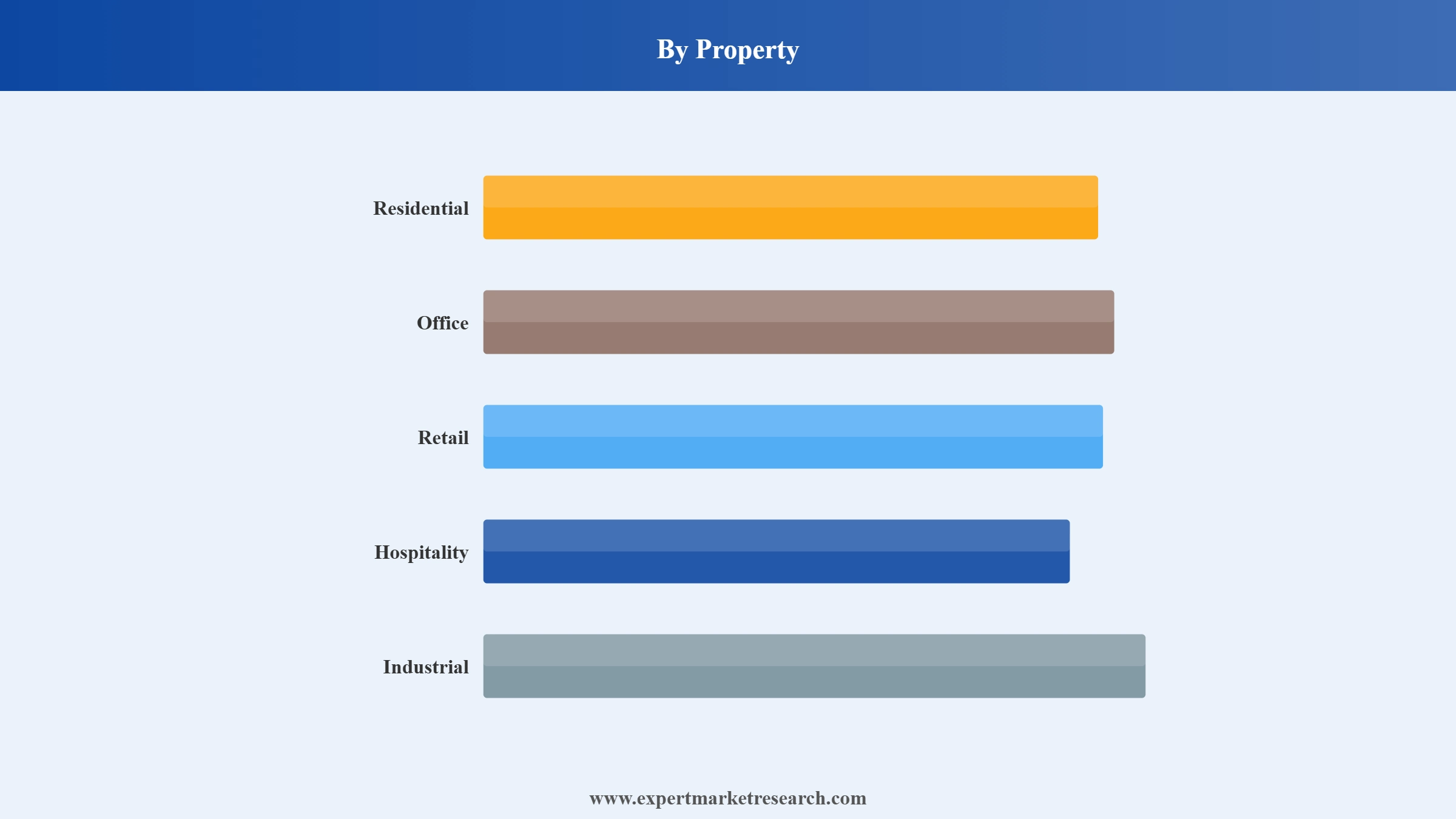

Market Breakup by Property

Key Insight: The residential sector maintains its dominance because of the high demand from end-users, upscale launches, and holistic communities, largely contributing to the India real estate market revenue. The office sector remains relevant for multinational firms looking for state-of-the-art offices where they can recruit talented people and operate efficiently. The retail sector is evolving with the emergence of the experiential model along with mixed-use integration. The hospitality sector is also witnessing growth because of the increased business travel and events hosted by corporate firms. In June 2026, DS Group announced a INR 1,000 crore hospitality expansion, including a INR 400 crore W Hotels project in Delhi NCR, addressing luxury hotel supply shortages and rising premium travel demand.

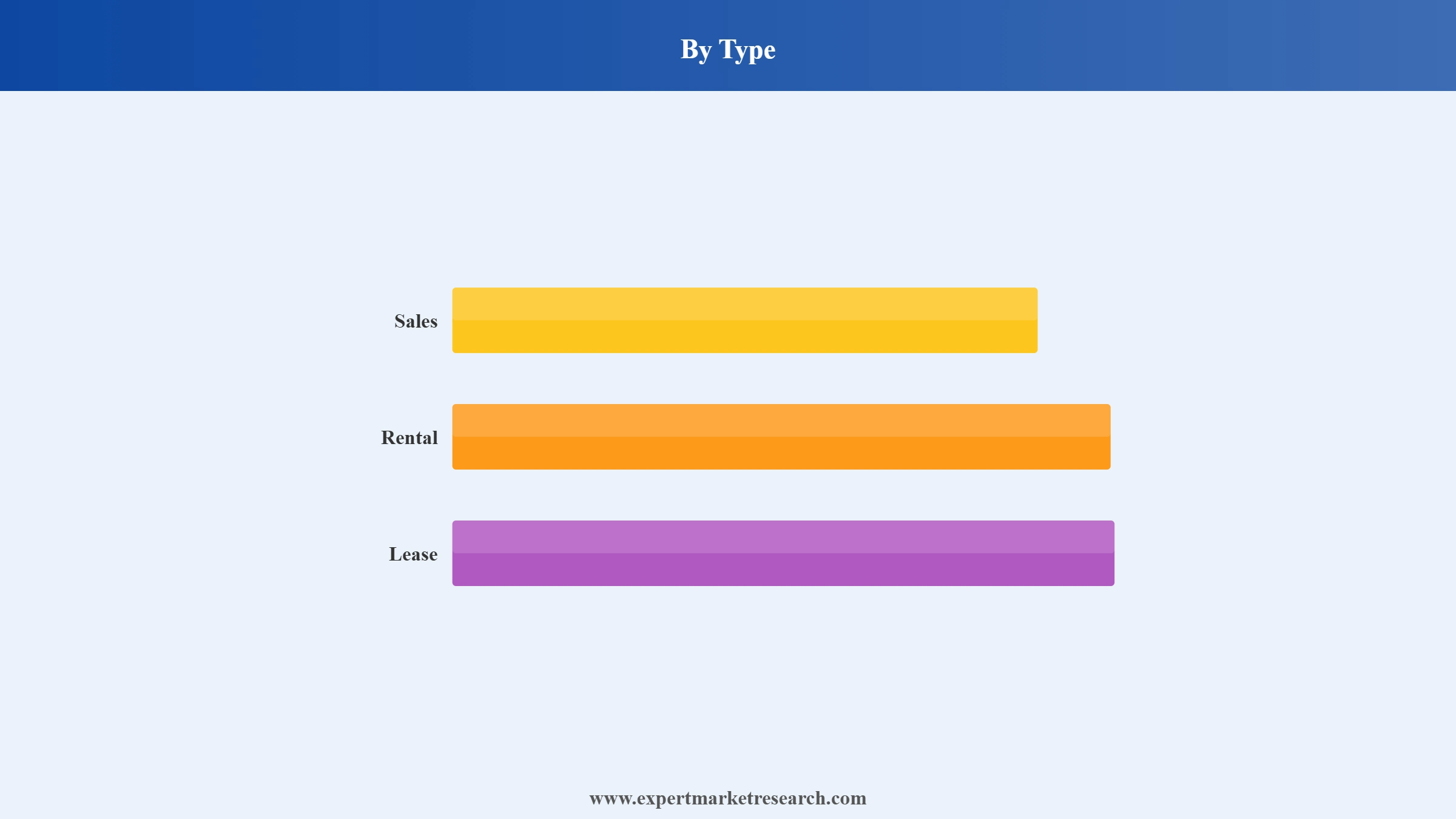

Market Breakup by Type

Key Insight: Transactions of a sales nature remain dominant in the India real estate market since ownership is considered to be the most optimal approach to investors and end users looking to create value over a period of time. Rentals offer the convenience of mobility and affordable occupation within the residential and commercial property markets. Leases are becoming popular as companies focus on creating operational efficiency, flexible infrastructural arrangements, and prudent use of capital. Property owners are also becoming flexible enough to provide custom-tailored occupancy solutions and enhanced service provision through advanced technologies in asset management.

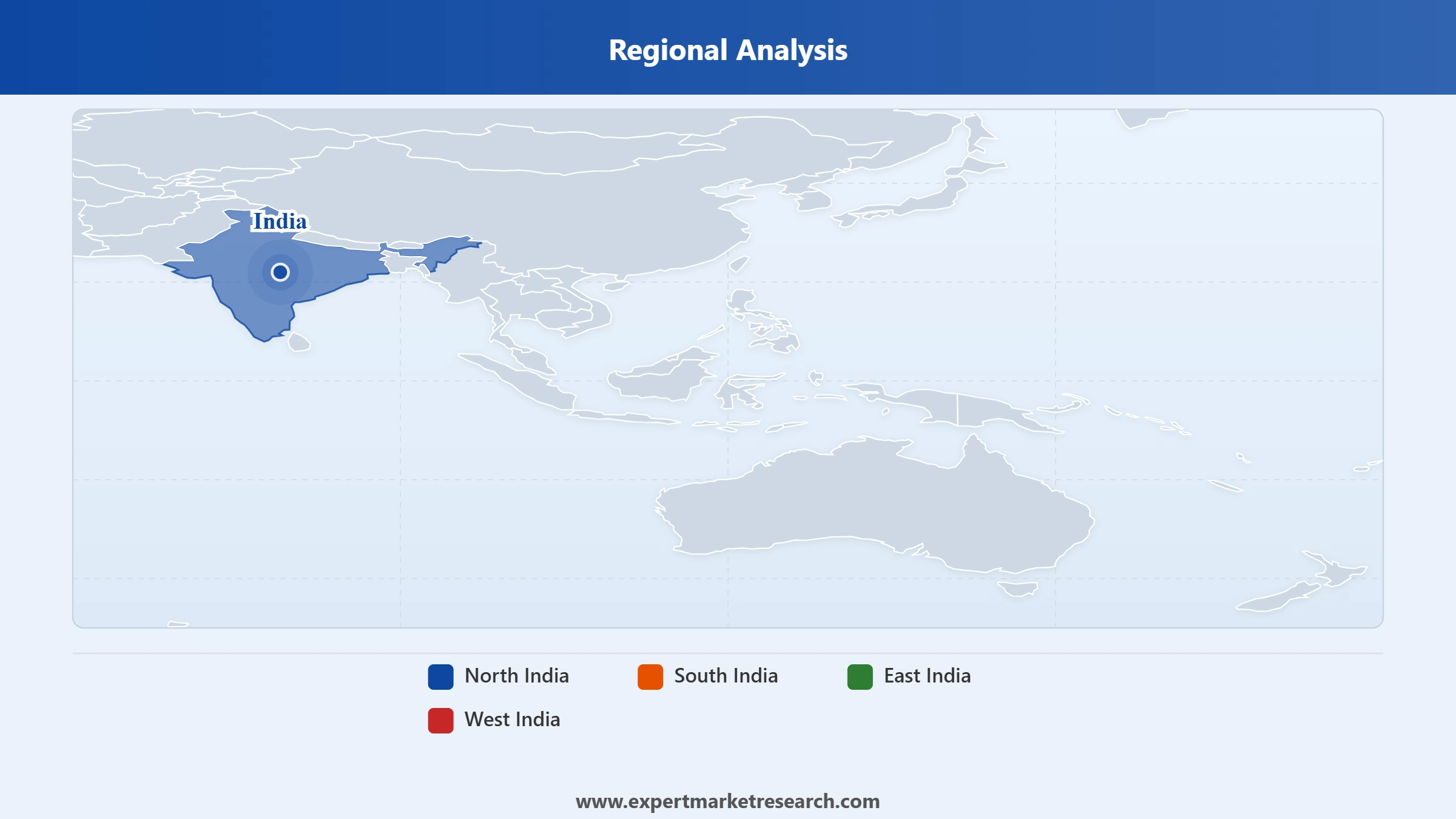

Market Breakup by Region

Key Insight: The North India real estate market has an advantage because of its government institutions, infrastructural investments, and residential demands within major cities. Eastern India fuels growth through its industrial expansion, logistics development, and urban infrastructural investments. Southern India continues to see success due to economic growth driven by technology, increased demand for office spaces, and innovative investments. Western India remains dominant due to its concentration of the financial services industry, high-end development projects, and robust institutional participation. Every region exhibits unique demand patterns that affect investment strategies and project planning. Collectively, these regions ensure balanced growth for developers looking to invest in India.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Residential properties account for the largest market share due to sustained urban housing demand and premium township developments

The residential real estate market in India continues to lead as prominent property developers continue to prioritize luxury housing, townships, and brand name residential properties. Firms like DLF, Godrej Properties, Lodha, and Prestige Group are investing significantly in developing their large-scale residential portfolios to meet changing consumer tastes regarding lifestyle-based projects. The demand is also expected to be bolstered by increasing migration into cities, mortgage lending, and greater uptake of smart home technologies. Retailing, healthcare, and recreational components are also being introduced as developers look to enhance property value and customer retention. In June 2026, Union Living expanded its managed housing portfolio, strengthening presence through new student and co-living accommodations.

The industrial real estate segment is identified as the fastest-growing sector in the India real estate market with developers investing in industrial parks and facilities linked to manufacturing as well as logistics hubs. Factors such as improved supply chain management, the growth of the e-commerce industry, and increased industrial production activity are contributing to the growth of this real estate segment. Significant investment is being made in developing high-grade industrial buildings close to transport routes as well as logistics centers. Modern occupiers require state-of-the-art infrastructure characterized by automation, energy efficiency, and ample storage space.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Property sales generate maximum revenue due to strong ownership demand

Sales transactions continue dominating the India real estate market as home buyers, institutional investors, and corporations prefer the acquisition of assets for asset management and capital accumulation purposes. Developers are investing in high-end, branded properties and mixed-use properties to give property owners an opportunity to gain from future property growth. Other driving factors include favorable financing options and improved investor confidence in professionally managed projects. The real estate companies are developing their sales processes through technological advancements and customer-oriented initiatives to support conversion and transaction volume. In June 2025, Godrej Properties sold 1,450 homes worth INR 2,000 crore at Bengaluru's Godrej MSR City launch.

The lease transactions represent the fastest-growing category in the India real estate market as a result of corporate real estate development strategy changes as well as the need for operational efficiency. Corporations are shifting focus to lease contracts, which give them an opportunity to allocate capital effectively while accessing the best commercial facilities. Developers and property owners are also investing in custom lease solutions, professional managed spaces, and loyalty schemes to encourage tenants to remain committed. The growth is particularly notable in the office, logistics, and industrial property markets.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

West India clocks in the leading position of the market due to financial hubs and investment concentration

The western region is established as the leader in the India real estate market because of the presence of financial hubs, business hubs, and luxurious residential projects in the area. Some of the key cities in West India, including Mumbai, Pune, and Ahmedabad, are receiving significant investment from both domestic and foreign players in commercial, residential, and industrial real estate segments. Developers are looking at premium properties, redevelopment projects, and mixed-use developments, making the most out of available space. Strong financial activity, infrastructure upgrades, and institutional participation are driving successful project development across the region. According to industry reports, Mumbai's redevelopment pipeline may unlock 59,000 homes worth INR 1.5 trillion by 2031.

The South India real estate market observes rapid growth owing to the expansion of the tech industry, Global Capability Centers, and rising demand for premium office spaces. Cities like Bengaluru, Hyderabad, Chennai, and Kochi are receiving interest from multinationals because of skilled manpower. There is development taking place in terms of large-scale office campuses, integrated townships, and logistics parks. The startup ecosystem, rise in the digital economy, and infrastructural upgrades are adding to the development process in South India.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The market is becoming increasingly competitive, as India real estate market players are now not only investing in residential and commercial properties but also in technology-driven ecosystems. Premium housing, mixed-use developments, logistics parks, data centers, and sustainable assets are becoming a priority for developers who wish to boost their recurring revenue. The use of smart buildings technologies, digital real estate property management systems, and certification in eco-friendly properties are among the key competitive advantages in the near future.

Moreover, India real estate companies are increasingly partnering with international investment funds to enhance operational efficiency, strengthen financing capabilities, and accelerate project execution. More options have appeared in the area of Global Capability Centers, life science facilities, warehouses, and luxury homes. Artificial intelligence can become an integral part of property management, preventive maintenance, and communication with customers.

Founded in 1898 and based in Mumbai, Maharashtra, Godrej Properties Ltd. combines innovative designs with extensive residential and mixed-use developments. The firm’s areas of interest include sustainable construction, digital sales channels, and township developments. These factors contribute to an effective strategy that centers around land-light growth, joint ventures, and premium housing developments in high-growth urban locations.

Founded in 1980 and based in Mumbai, Maharashtra, Oberoi Realty Ltd. concentrates on premium housing, commercial, retail, and hospitality properties. The company is known for the creation of luxury integrated ecosystems with top-notch facilities and cutting-edge buildings. Premium asset quality, customer experience improvement, and effective execution have helped the firm stay strong in the India real estate market.

DLF Ltd., founded in 1946 and based in Gurugram, Haryana, continues to be among India’s top real estate developers. DLF concentrates on luxury residential developments, Grade A offices, and huge metropolitan complexes. The organization is increasingly turning its attention towards developing infrastructure that supports sustainability, digitization of operations, and smart solutions. DLF’s commercial properties have ensured stable revenue through long-term lease agreements.

Founded in 1980 and based in Mumbai, Maharashtra, Lodha Developers Ltd. deals mainly in premium residential enclaves, integrated townships, and upscale metropolitan projects. The company is keen on promoting green building practices, incorporating smart home features, and implementing wellness designs in its developments. With its approach based on large scale land acquisition, innovations in customer services, and luxury offerings, Lodha is able to attract both private and institutional clients.

Other key players in the market include Jaypee Infratech Limited, Prestige Estates Projects Limited, Sobha Ltd., Merlin Group, Brigade Enterprises Limited, and Sunteck Realty Ltd., among others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Unlock the latest insights with our India real estate market trends 2026 report. Discover regional growth patterns, consumer preferences, and key industry players. Stay ahead of competition with trusted data and expert analysis. Download your free sample report today and drive informed decisions in the market.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market reached an approximate value of USD 620.02 Billion.

The market is projected to grow at a CAGR of 8.70% between 2026 and 2035.

The key players in the market include Godrej Properties Ltd., Oberoi Realty Ltd., DLF Ltd., Lodha Developers Ltd., Jaypee Infratech Limited, Prestige Estates Projects Limited, Sobha Ltd., Merlin Group, Brigade Enterprises Limited, Sunteck Realty Ltd. and others.

The sales segment is expected to grow at 12.1% CAGR through 2035.

Key strategies driving the market include affordable housing initiatives, smart city development, increased FDI inflows, infrastructure upgrades, REIT expansion, digital adoption, regulatory reforms like RERA, sustainable construction, co-living/co-working trends, and government incentives. These collectively enhance transparency, investor confidence, and urban growth, fueling long-term market momentum.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Property |

|

| Breakup by Type |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.