Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

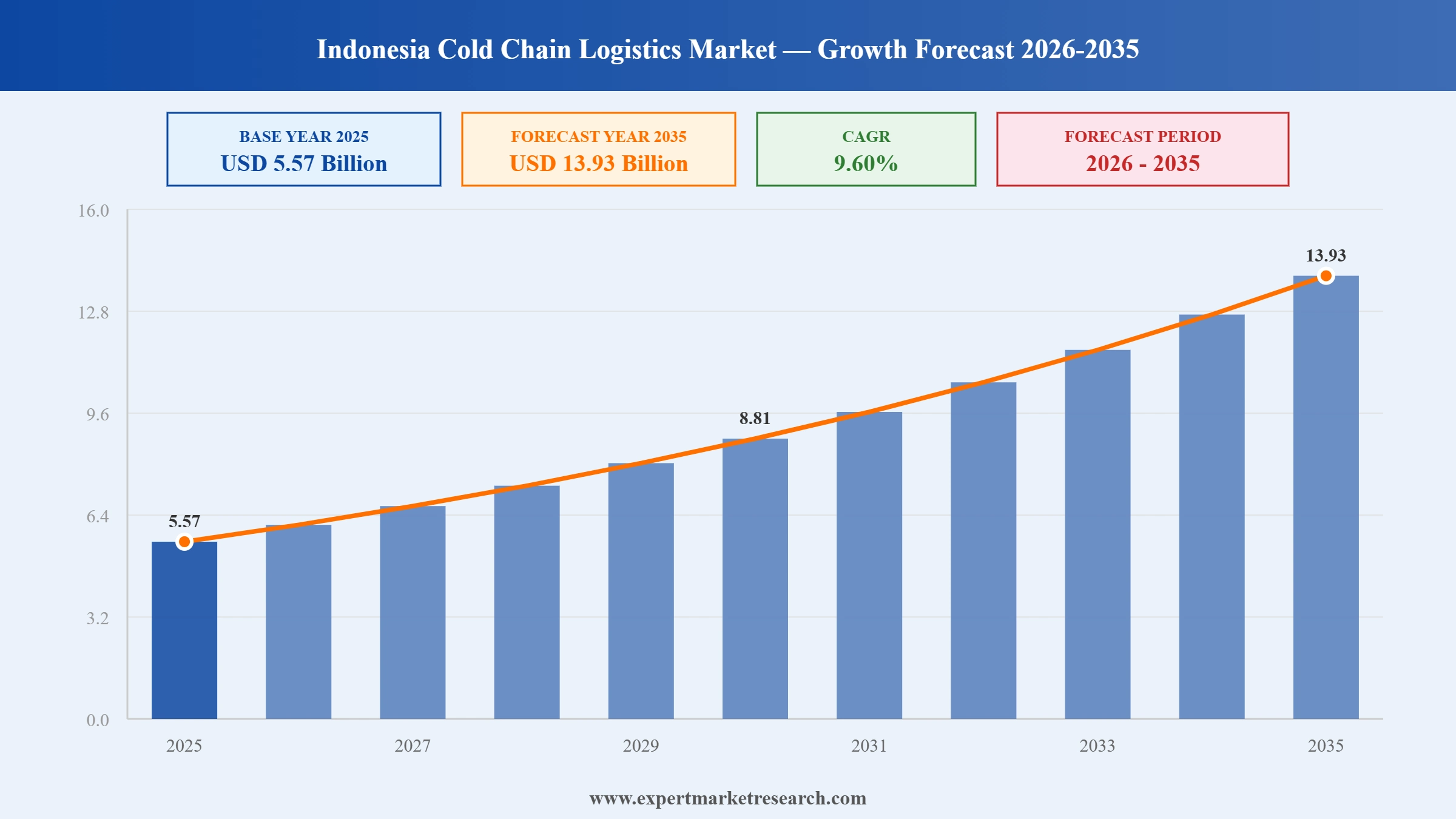

The Indonesia cold chain logistics market reached a value of USD 5.57 Billion at 2025 and is projected to expand at a CAGR of around 9.60% during the forecast period of 2026-2035. With rising demand for processed food and seafood products, rapid expansion of pharmaceutical logistics, growing e-commerce penetration, and accelerating cold storage infrastructure investment, the market is expected to reach USD 13.93 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The Indonesia cold chain logistics sector is undergoing meaningful structural shifts, driven by the convergence of rising consumer demand for perishable goods, pharmaceutical distribution modernisation, and digital commerce growth. Logistics operators are investing in technology-enabled temperature monitoring, automated warehousing, and energy-efficient refrigeration to stay competitive and meet increasingly stringent food safety and pharmaceutical compliance requirements.

The Indonesian Ministry of Industry hosted the Indonesia Cold Chain Infrastructure Summit in August 2025, bringing together regulators, investors, and industry leaders to coordinate fiscal incentives, standardise cold chain practices, and integrate the sector with the National Logistics Ecosystem. The summit reinforced the government's commitment to making cold chain logistics a strategic pillar of food security and public health distribution.

DHL Group deepened its commitment to Indonesia's cold chain market in June 2025, expanding its Life Science and Healthcare Competency Centre in Jakarta with specialised 2 to 8 degrees Celsius and 15 to 25 degrees Celsius storage facilities. The move supports pharmaceutical sector growth projected to reach USD 11 billion in market value, directly strengthening Indonesia's cold chain logistics infrastructure.

In April 2025, DHL Group announced a EUR 500 million investment in Asia Pacific healthcare logistics as part of its new DHL Health Logistics brand, with Jakarta identified as a key regional hub. The investment targets GDP-certified pharma hubs, expanded cold chain capacity, and ultra-low temperature storage capabilities across the region, benefiting Indonesia's pharmaceutical cold chain sector.

MGM Bosco Logistics implemented the Blue Yonder Warehouse Management Solution in July 2024, with support from SGV Consulting, Blue Yonder's Indonesia partner. The deployment enhanced warehouse efficiency and customer-oriented supply chain operations, positioning MGM Bosco as a technology-forward cold chain operator in Indonesia's evolving logistics landscape.

Growing pharmaceutical distribution requirements are reshaping Indonesia's cold chain logistics market, as operators expand GDP-compliant storage and transport capabilities. DHL's Jakarta Life Science centre exemplifies this trend, handling temperature-sensitive drugs, vaccines, and biologics to meet Indonesia's rising healthcare cold chain logistics market demand.

Rapid e-commerce growth, with Indonesia projected to exceed 50 million online buyers, is fuelling cold chain logistics market growth across urban and peri-urban zones. Platforms like Tokopedia and GrabMart are expanding micro-fulfilment cold hubs, driving demand for distributed refrigerated warehousing and last-mile temperature-controlled delivery solutions.

Indonesia's National Logistics Ecosystem initiative is reshaping the cold chain sector by standardising port-to-warehouse temperature management protocols. Integration at Tanjung Priok Port reduced cargo clearance times by approximately 27%, directly benefiting time-sensitive perishable goods movement and boosting Indonesia cold chain logistics market efficiency.

In February 2026, Indonesia's Ministry of Marine Affairs and Fisheries secured market access for fishery products to Turkey and China, with 57 fish processing units meeting HACCP and cold chain standards. This cold chain logistics market expansion directly supports demand for frozen warehousing, reefer transport, and traceability-enabled distribution networks.

Indonesia confirmed compatibility of its national seafood traceability system with the GDST Standard in November 2025, enabling interoperable data exchange with international trading partners. This development strengthens export market access for Indonesian seafood, reinforcing cold chain logistics demand across coastal fisheries hubs and national distribution corridors.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The report of Expert Market Research's titled "Indonesia cold chain logistics market report and forecast 2026-2035 offers a detailed analysis of the market based on the following segments:

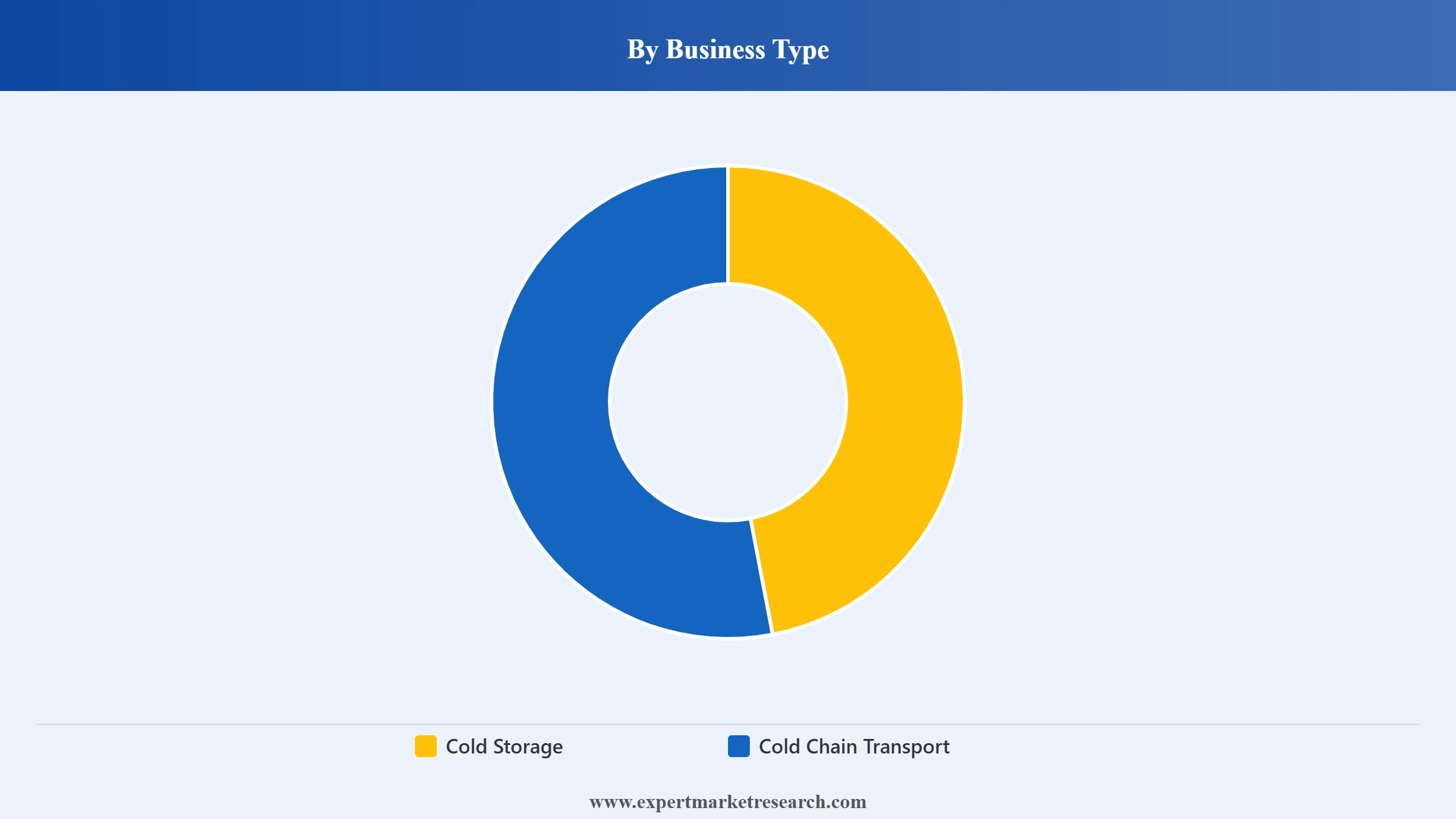

Market Breakup by Business Type

Key Insight: Cold storage holds the dominant share of the Indonesia cold chain logistics market, supported by the country's vast fisheries sector, growing pharmaceutical storage needs, and increasing online grocery demand. Indonesia's fishing sector contributes approximately 2.77% of national GDP, with fish consumption per capita at 35.26 kg in 2021, making reliable cold storage essential for extending the shelf life of seafood across domestic and export markets. Cold chain transport is expanding rapidly as perishable goods require seamless connectivity between production zones, ports, and distribution centres across the archipelago.

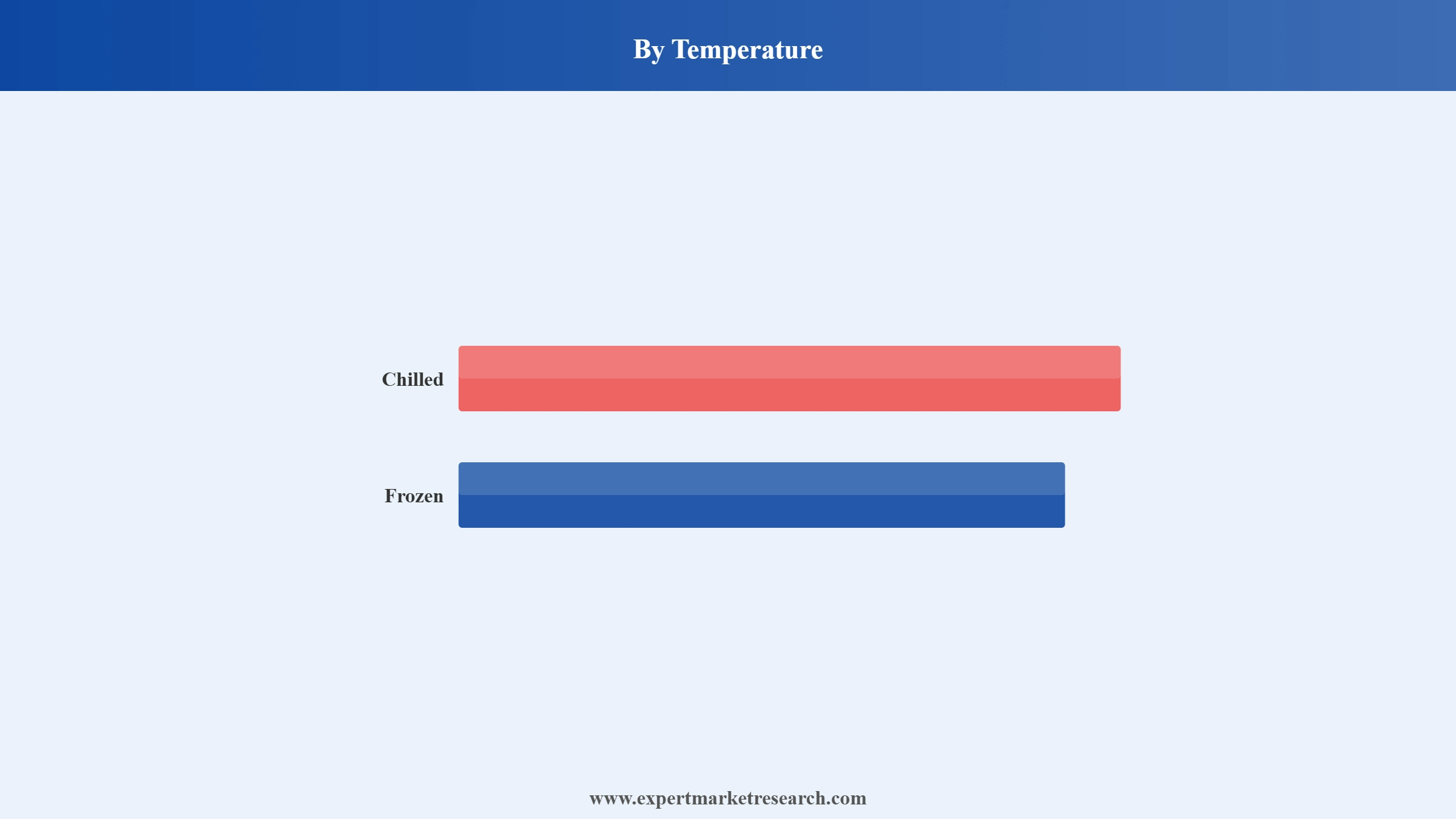

Market Breakup by Temperature

Key Insight: The frozen temperature segment commands the largest share of the Indonesia cold chain logistics market, driven by the country's position as a top global seafood exporter and growing consumption of frozen processed foods in modern retail and foodservice channels. The chilled segment is growing steadily as organised retail expands and demand for fresh dairy, ready-to-eat meals, and pharmaceuticals requiring 2 to 8 degrees Celsius storage conditions increases, broadening service scope across both temperature bands.

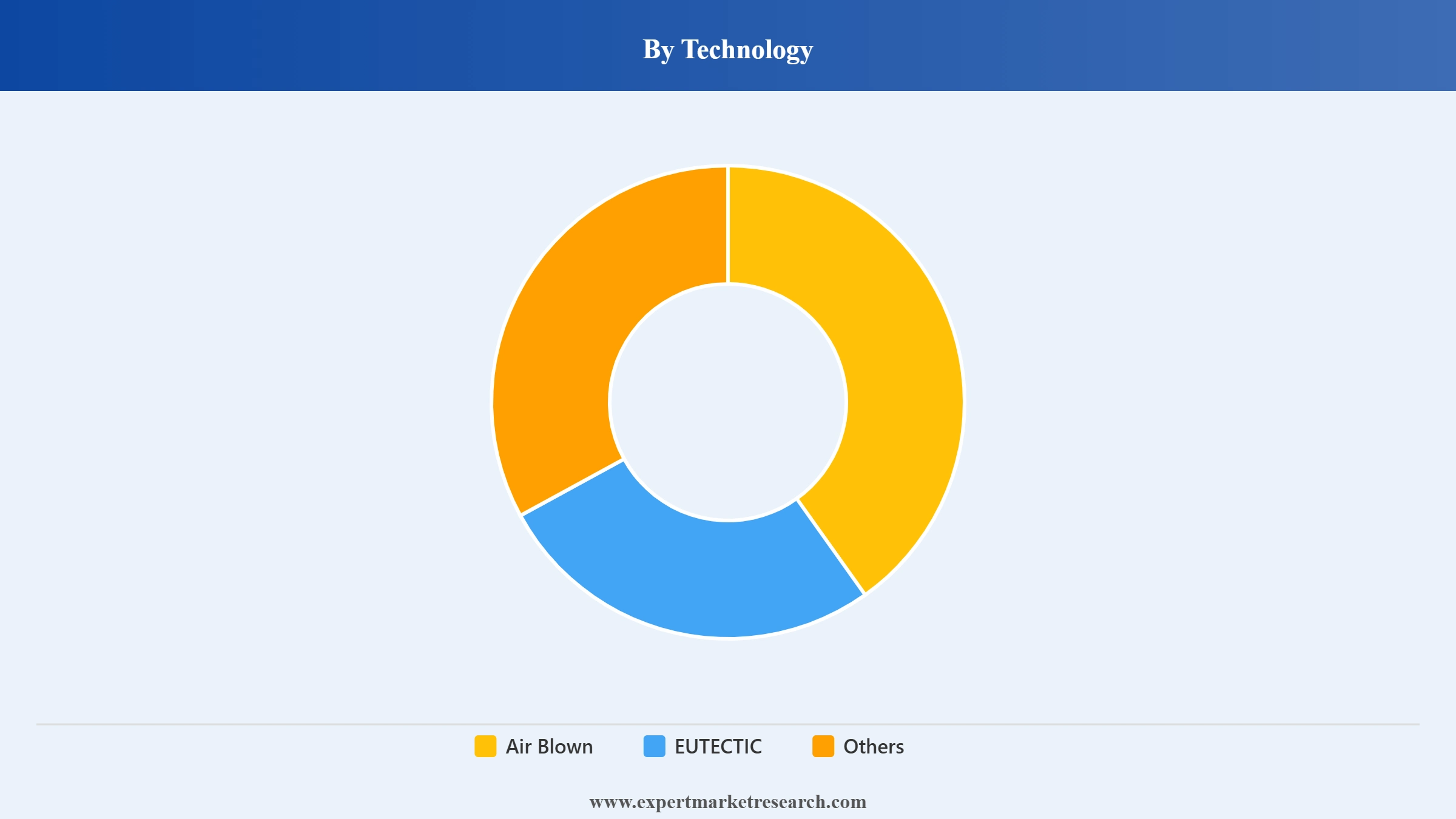

Market Breakup by Technology

Key Insight: Air blown refrigeration technology leads the Indonesia cold chain logistics market due to its versatility, cost efficiency, and compatibility with a wide range of perishable product categories including seafood, dairy, and pharmaceuticals. EUTECTIC systems are gaining traction in last-mile cold chain delivery, particularly for urban food delivery applications where passive cooling during short transit windows reduces energy costs and supports green logistics compliance requirements.

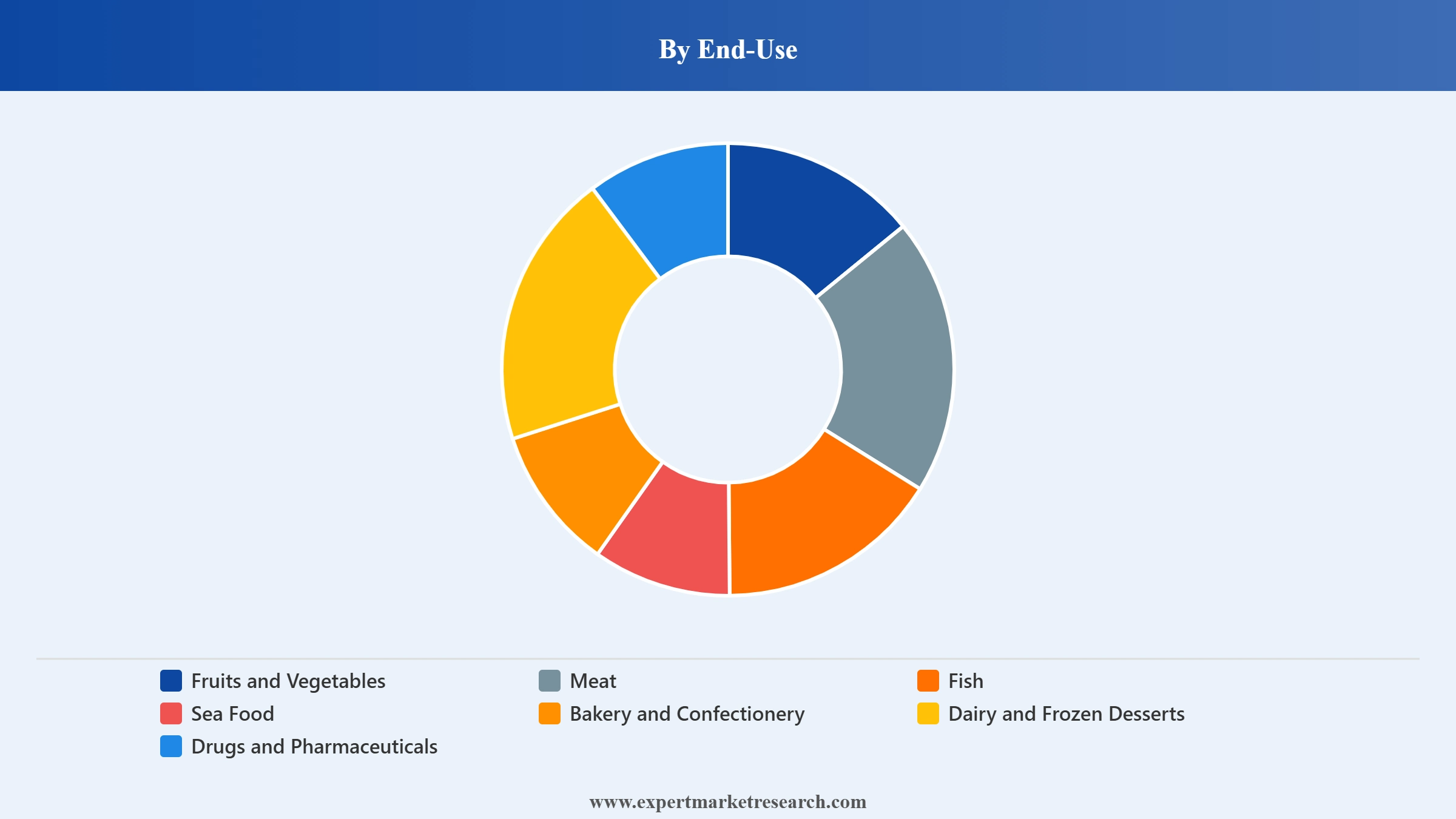

Market Breakup by End-Use

Key Insight: Meat, fish, and seafood represent the dominant end-use segment in the Indonesia cold chain logistics market, reflecting the country's status as one of the largest seafood producers globally with over 8,500 fish varieties. Annual fish and seafood consumption exceeds 7 million metric tons, creating structural demand for pre-cooling, frozen storage, and reefer transport. Drugs and pharmaceuticals are the fastest-growing end-use segment, driven by healthcare sector expansion and rising access to temperature-sensitive medications.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Business Type, Cold Storage Dominates the Market Due to Expanding Fisheries Sector and Pharmaceutical Storage Needs

Cold storage accounts for the largest share of the Indonesia cold chain logistics market, anchored by the country's robust fisheries sector and rising pharmaceutical distribution requirements. Indonesia's archipelagic geography, with over 17,000 islands, means seafood products require extended cold storage at origin ports before reaching domestic consumers or export destinations. Growing numbers of organised food retailers and quick service restaurants across Java and Sumatra further reinforce consistent demand for cold storage facilities.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Cold chain transport is the faster-growing sub-segment within the Indonesia cold chain logistics market, driven by last-mile delivery demands from online grocery platforms and food delivery services. The Ministry of Marine Affairs' seafood export approvals in early 2026, covering 57 HACCP-compliant processing units, are expected to intensify inter-island reefer transport activity. Operators are investing in GPS-enabled reefer trucks and IoT temperature monitoring to maintain product integrity across multi-modal routes.

By Temperature, Frozen Accounts for the Dominant Share of the Market Due to Indonesia's Position as a Global Seafood Leader

The frozen temperature segment holds the commanding share of the Indonesia cold chain logistics market, driven by deep integration with global seafood trade and growing consumption of frozen processed foods. Categories like shrimp, tuna, and cephalopods require continuous sub-zero temperature control from coastal harvest points through processing facilities to export ports. Modern retail chains and foodservice operators reinforce demand for blast freezers, frozen warehousing, and reliable reefer transport documentation.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The chilled temperature segment is gaining momentum in the Indonesia cold chain logistics market as pharmaceutical distribution, fresh dairy, and ready-to-eat meal categories expand. Healthcare logistics operators including DHL are establishing 2 to 8 degrees Celsius compliant facilities in Jakarta to handle vaccines and biologics. Fresh produce exporters are also increasing chilled storage use to meet retailer-specific shelf life requirements and reduce post-harvest losses across the supply chain.

By Technology, Air Blown Dominates the Market Due to Versatility, Cost Effectiveness, and Wide Applicability Across Product Categories

Air blown refrigeration technology holds the largest share of the Indonesia cold chain logistics market, valued for its operational flexibility across bulk cold storage applications ranging from seafood and meat to pharmaceutical products. Large-scale facilities across Java and Sumatra predominantly rely on air blown systems to handle diverse product mixes at consistent temperatures. The technology is deeply embedded in Indonesia's refrigerated truck fleet serving inter-city distribution routes nationwide.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

EUTECTIC refrigeration technology is emerging as a practical alternative for last-mile cold delivery within the Indonesia cold chain logistics market. Its ability to maintain temperatures without active refrigeration during short delivery windows makes it cost-effective for urban food delivery and small-batch pharmaceutical distribution. Indonesia's participation in the I-NCAP initiative is accelerating interest in EUTECTIC and natural refrigerant systems, helping operators reduce operating costs and meet green logistics standards.

The Indonesia cold chain logistics market features a moderately fragmented competitive landscape, with a mix of established domestic operators and multinational logistics providers competing across cold storage, reefer transport, and value-added services. Leading domestic players such as PT Dua Putra Perkasa Pratama, MGM Bosco Logistics, and PT Sukanda Djaya maintain competitive advantages through their deep regional networks, longstanding relationships with food processors and seafood exporters, and expanding cold storage capacities across Java and Sumatra.

Multinational operators including DHL Supply Chain and YCH Group are competing aggressively in the pharmaceutical cold chain and e-commerce logistics segments, leveraging global compliance standards, advanced technology platforms, and significant capital to build GDP-certified facilities and IoT-enabled monitoring capabilities. The market is witnessing increasing technology adoption, with companies deploying warehouse management systems, real-time temperature tracking, and automated cold storage operations to differentiate their service offerings and capture growing demand from pharmaceutical, foodservice, and online grocery clients.

Founded in 1997 and headquartered in Jakarta, PT Dua Putra Perkasa Pratama (DPPP) is one of Indonesia's leading integrated cold chain logistics companies. The company specialises in cold storage, reefer transport, and fisheries logistics, with extensive operations across Java and Sulawesi. DPPP operates large-scale cold storage facilities and a refrigerated vehicle fleet, serving seafood processors, food manufacturers, and retail distributors. Its strong compliance record and broad network of temperature-controlled facilities make it a preferred partner for export-oriented fisheries clients.

Established in 1994 and headquartered in Jakarta, MGM Bosco Logistics is a prominent integrated cold chain service provider operating across Indonesia. The company offers cold storage, refrigerated transport, and distribution services, serving food processors, pharmaceutical companies, and retail clients. In July 2024, MGM Bosco deployed the Blue Yonder Warehouse Management Solution to enhance operational efficiency and customer service quality. With facilities in Sidoarjo, East Java, and Jakarta, the company has a strong footprint in both Western and Eastern Indonesian markets.

Founded in 1975 and based in Jakarta, PT Sukanda Djaya is a well-established food distribution and cold chain logistics company serving the hospitality, retail, and food processing sectors across Indonesia. The company operates a comprehensive cold chain network encompassing frozen and chilled storage facilities and a dedicated reefer transport fleet. PT Sukanda Djaya is particularly strong in serving hotels, restaurants, and catering operators, positioning it at the intersection of cold chain logistics and foodservice distribution. Its established relationships with international food brands and domestic processors underpin its market position.

The Kiat Ananda Group is one of Indonesia's pioneering cold storage operators, with decades of experience in temperature-controlled warehousing and logistics. Headquartered in Indonesia, the group operates cold storage facilities designed to handle diverse product categories including seafood, frozen food, dairy, and pharmaceuticals. Its strategic facility locations near major industrial and port zones enable efficient handling of large-volume fisheries and food processing clients. The group's long operational history and sector expertise have earned it a strong reputation among seafood exporters and large food manufacturers.

Other key players in the Indonesia cold chain logistics market are CKL Indonesia Raya (CKL Cargo), YCH Group, TITAN Containers A/S, PT Perintis Sempurna Bersama (Coldspace), and others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Gain a competitive advantage with the latest insights on the Indonesia cold chain logistics market 2026. Explore in-depth data on cold storage infrastructure trends, pharmaceutical logistics developments, seafood export dynamics, and regional growth opportunities across Indonesia's expanding cold chain ecosystem. Whether you are planning market entry, scaling existing operations, or evaluating investment potential, this report gives you the clarity and confidence you need. Download your free sample today and unlock key opportunities in Indonesia's thriving cold chain logistics sector.

Cell and Gene Therapy Cold Chain Logistics Market

United Kingdom Cold Chain Logistics Market

Saudi Arabia Cold Chain Logistics Market

Australia Cold Chain Logistics Market

Peru Cold Chain Logistics Market

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market value was approximately USD 5.57 Billion.

The market is projected to grow at a CAGR of 9.60% between 2026 and 2035.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach around USD 13.93 Billion by 2035.

The major drivers include the expansion of retail and restaurant chains, increasing demand for processed food, and technological advancements.

The key trends include the expansion of multinational fast-food brands in the foodservice sector and the rising adoption of online grocery and food delivery.

The different business types include cold storage and cold chain transport.

The major end users of cold chain logistics include fruits and vegetables, meat, fish, and sea food, bakery and confectionery, dairy and frozen desserts, and drugs and pharmaceuticals, among others.

The key players in the market include PT Dua Putra Perkasa Pratama, PT Mulia Bosco Logistik (MGM Bosco Logistics), PT Sukanda Djaya, Kiat Ananda Group, CKL Indonesia Raya (CKL Cargo), YCH Group, TITAN Containers A/S, and PT Perintis Sempurna Bersama (Coldspace), among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Business Type |

|

| Breakup by Temperature |

|

| Breakup by Technology |

|

| Breakup by End-Use |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.