Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

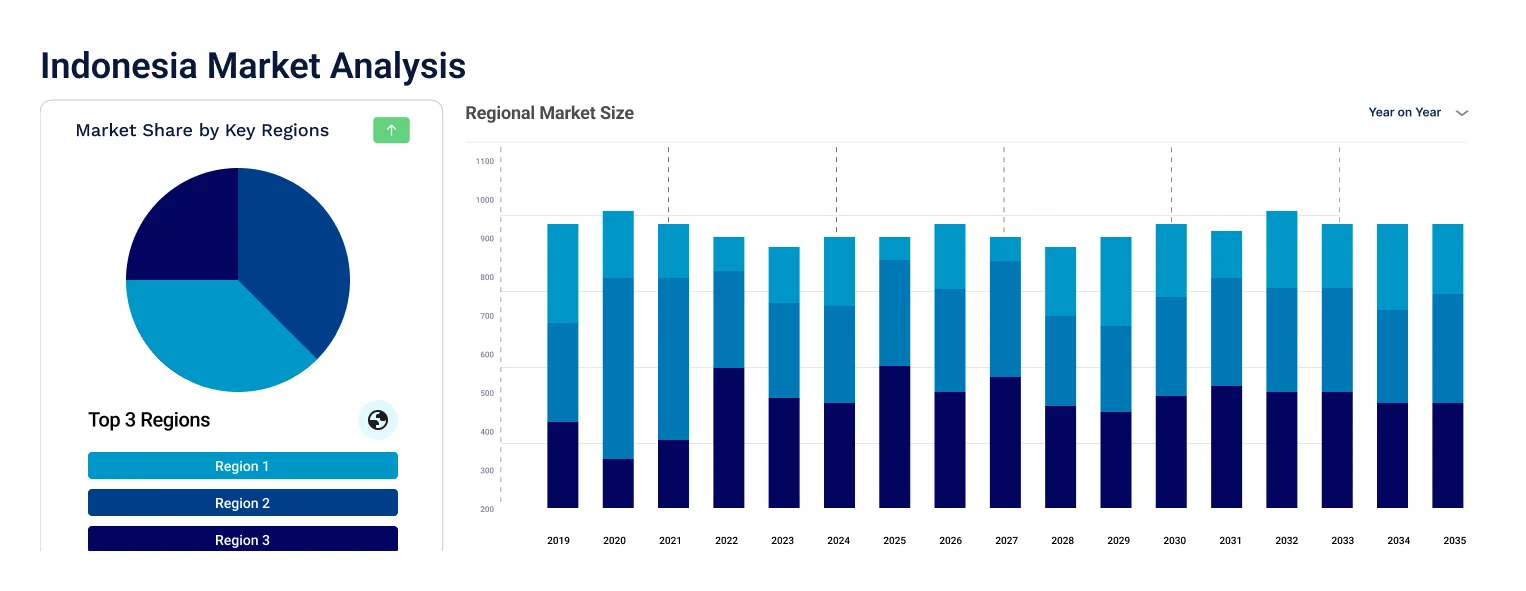

The Indonesia Shampoo Market reached a value of USD 550.00 Million at 2025 and is projected to expand at a CAGR of around 3.70% during the forecast period of 2026-2035. With the growing demand for halal-certified and naturally formulated shampoo products across Indonesia's large Muslim consumer base, rising household incomes enabling a shift toward premium and specialized hair care, rapid expansion of e-commerce platforms providing nationwide product access, and increasing consumer adoption of gender-specific and dermatologist-endorsed formulations, the market is expected to reach USD 790.95 Million by 2035.

Compound Annual Growth Rate

3.7%

Value in USD Million

2026-2035

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

| Indonesia Shampoo Market Report Summary |

Description |

Value |

|

Base Year |

USD Million |

2025 |

|

Historical Period |

USD Million |

2019-2025 |

|

Forecast Period |

USD Million |

2026-2035 |

|

Market Size 2025 |

USD Million |

550.00 |

|

Market Size 2035 |

USD Million |

790.95 |

|

CAGR 2019-2025 |

Percentage |

XX% |

|

CAGR 2026-2035 |

Percentage |

3.70% |

|

CAGR 2026-2035- Market by Price Category |

Premium |

4.2% |

|

CAGR 2026-2035 - Market by End User |

Kids |

4.4% |

|

CAGR 2026-2035 - Market by Distribution Channel |

Online |

13.2% |

Indonesia's shampoo market is being shaped by strong halal consumption values, a deepening cultural preference for botanical ingredients, the structural growth of e-commerce as a distribution channel, and a gradual but clear premiumization trend that is transforming the product mix available to Indonesian consumers.

In January 2026, Unilever launched a landmark reinvention of its Sunsilk brand, the world's most-chosen hair care brand and the number one shampoo in Indonesia. The transformation includes the launch of Sunsilk Wondermist, a hybrid hair mist combining conditioning performance with scientifically validated mood-boosting fragrance technology. The launch is anchored in a social-first marketing strategy aimed specifically at Gen Z consumers and is designed to shift Sunsilk from a functional daily-use brand to a culturally resonant beauty product. For Indonesia, where Sunsilk holds the number one position, this reinvention carries significant implications for premium segment growth and consumer engagement across digital channels.

In 2025, Unilever Indonesia undertook a significant brand revitalization initiative, relaunching or launching over 85% of its core brands including flagship hair care lines Sunsilk and Clear. The initiative was accompanied by investments in process automation, operational simplification, and supply chain transformation to improve efficiency and cost discipline. The brand relaunch program was supported by a strengthened innovation pipeline and reduced product development lead times, enabling the company to respond more quickly to evolving consumer preferences in Indonesia's competitive shampoo market. The program reflects Unilever's strategy to drive volume-led recovery following a period of performance pressure in the Indonesian market.

In 2024, students from Universitas Negeri Gorontalo developed Armosa Paper, an eco-friendly, rinse-free paper shampoo formulated using jackfruit leaf extract and pineapple skin waste. Supported by Indonesia's Ministry of Education, Culture, Research, and Technology through the 2024 Student Entrepreneurship Creativity Program (PKM-K), the product addresses growing consumer and institutional interest in sustainable hair care solutions that conserve water and minimize plastic packaging. While still at an early commercialization stage, the innovation reflects the growing influence of sustainability values among Indonesian consumers and the emergence of local product development talent that could shape the next generation of the domestic shampoo market.

In April 2024, Kao Corporation launched its new hair care brand 'melt,' marking the first step in a broader transformation of its global Hair Care business. The melt range introduces carbonated foam shampoo, moisture repair treatments, and conditioning products formulated with hybrid repair technology and ceramide actives, targeting consumers seeking a premium salon-like experience at home. Kao, which operates two production facilities in Indonesia at Cikarang and Karawang, plans to expand its premium hair care portfolio across key Southeast Asian markets including Indonesia, where it already holds an established retail and logistics network.

In January 2024, Kundal, a South Korean luxury personal care brand recognized for its honey and macadamia formulations, launched its REFRESHING ANTI-DANDRUFF Hair Care Line in Indonesia and Malaysia, specifically targeting the growing halal personal care demand across the Muslim-majority Southeast Asian market. The product line is certified MUI Halal and vegan, aligning with Indonesian consumer expectations for religiously compliant and ethically produced hair care. The launch reflects a broader trend of international beauty brands tailoring product credentials to meet the compliance requirements of Indonesia's large and commercially influential Muslim consumer segment.

Halal compliance has moved from a regulatory consideration to a primary commercial requirement for shampoo brands operating in Indonesia, the world's largest Muslim-majority nation. Consumers increasingly seek products certified by the Majelis Ulama Indonesia (MUI), and halal labeling has become a key purchase factor alongside price and effectiveness. The Indonesian government accelerated this trend by lowering halal certification costs for domestic cosmetics manufacturers to USD 3 and reducing processing times to 15 days, making compliance more accessible for small and medium enterprises. Multinational brands have responded by reformulating products and securing halal credentials to maintain retail shelf access and consumer trust. This Indonesia shampoo market growth driver is expected to persist through the entire forecast period, structurally embedding halal compliance as a baseline product attribute rather than a differentiation claim. In January 2024, Kundal launched its REFRESHING ANTI-DANDRUFF Hair Care Line in Indonesia with full MUI Halal and vegan certification, directly targeting the segment's growing halal-compliant personal care demand.

Indonesian consumers are increasingly choosing shampoo products formulated with botanical, herbal, and traditionally derived ingredients, driven by a combination of cultural familiarity with herbal remedies, growing health consciousness, and skepticism toward synthetic chemicals. Ingredients such as coconut oil, aloe vera, ginger, and local botanical extracts carry strong cultural resonance and are seen as both safe and effective. Brands are responding by reformulating existing product lines, removing microplastics, incorporating plant-based surfactants, and adopting refillable packaging formats. Urban and coastal consumers are also showing stronger environmental awareness, seeking products that align with personal values around sustainability and responsible sourcing. International brands like Unilever and local manufacturers are actively localizing formulations to capture this growing preference, creating product innovation activity in both the medicated and non-medicated segments across mass and premium price tiers. In 2024, Unilever's Sunsilk and TRESemmé collaborated with Indonesian digital influencers to educate consumers on new herbal and functional formulations, reaching millions of viewers across social platforms.

E-commerce has emerged as a structurally important and fast-growing distribution channel for shampoo in Indonesia, driven by the country's rapidly expanding digital infrastructure, high mobile internet penetration, and the sheer logistical challenge of distributing personal care products across thousands of islands. Platforms like Tokopedia, Shopee, and Lazada have enabled brands to reach consumers in tier 2 and tier 3 cities and rural areas that traditional retail chains do not adequately serve. Online channels also enable brands to run direct-to-consumer campaigns, leverage influencer-generated content, and offer subscription or bundle pricing that is difficult to replicate through physical retail. The online channel is growing at a materially faster pace than traditional distribution channels and is expected to meaningfully increase its share of total shampoo sales over the forecast period. In 2025, Unilever Indonesia's innovation pipeline, including its core shampoo brands, increasingly prioritized digital-first campaigns and online retail partnerships as primary go-to-market routes.

While mass-market shampoos continue to dominate Indonesia's market by volume, a visible and commercially significant premiumization trend is reshaping the product mix, particularly in Java's major urban centers. Rising disposable incomes, greater exposure to global beauty trends through social media, and the influence of dermatologists and hair care professionals are all pushing consumers to trade up from basic cleansing products to specialized formulations for scalp health, damage repair, color protection, and anti-frizz. Premium product launches are commanding higher shelf space in modern retail environments and capturing growing attention in online beauty channels. International brands are driving much of this shift, with Kao's 2024 launch of its melt brand and Unilever's Sunsilk Wondermist in 2026 both targeting the premium experiential segment. In April 2024, Kao launched the melt hair care brand featuring a premium carbonated foam shampoo and ceramide-based repair treatment, targeting Indonesian and Southeast Asian consumers seeking a scalp spa-like experience at home.

The Expert Market Research's report titled "Indonesia Shampoo Market Report and Forecast 2026 to 2035" offers a detailed analysis of the market based on the following segments:

Market Breakup by Product Type

Key Insight: Non-Medicated shampoos hold the dominant share within the Indonesia shampoo market by product type, reflecting the consumer preference for everyday-use formulations designed around lifestyle benefits such as hydration, anti-frizz, fragrance, and color protection rather than therapeutic treatment. The Non-Medicated segment's strength is reinforced by digital campaigns that have shifted consumer conversations from reactive hair problem-solving toward routine wellness and hair aesthetics. Brands are investing heavily in new ingredient narratives and sensory differentiation within the non-medicated space to capture evolving consumer expectations. Medicated shampoos, led by anti-dandruff formulations such as Clear (Unilever) and Head & Shoulders (P&G), retain a stable and loyal consumer base, with dandruff remaining one of the most common hair concerns cited by Indonesian consumers due to climate-related scalp conditions.

Market Breakup by Price Category

Key Insight: The Mass price category commands the largest volume share of the Indonesia shampoo market, underpinned by Indonesia's large, cost-sensitive rural and semi-urban population that prioritizes affordability and availability. Mass-market products are distributed through a broad network of traditional warungs, convenience stores, and modern trade hypermarkets, ensuring wide geographic penetration across the archipelago. Unilever's Sunsilk and Clear brands and P&G's Pantene and Head & Shoulders are the dominant forces in this segment. The Premium category is growing at a faster rate as rising urban incomes and greater beauty awareness support a gradual trade-up. International entrants including Kao's premium lines and Korean beauty brands are fueling premiumization, particularly in Jakarta, Surabaya, and other major urban centers where younger consumers are more receptive to higher-priced specialized formulations.

Market Breakup by End User

Key Insight: Women represent the dominant end user segment in the Indonesia shampoo market, accounting for the majority of purchases across both mass and premium categories. Women in Indonesia are the primary household purchasers of personal care products and are the target demographic for the bulk of advertising investment by multinational brands. The Women's segment is also where premiumization is most pronounced, with specialized formulations for hair strengthening, hydration, and color care driving trial and repeat purchases. The Men's segment is a growing category, with gender-specific shampoo formulations gaining traction among urban male consumers who are increasingly attentive to hair and scalp health. The Kids category, while smaller in absolute volume, is a stable segment driven by the household purchase behavior of parents who prioritize gentle, mild formulations for children's daily hair care routines.

Market Breakup by Distribution Channel

Key Insight: Supermarkets and Hypermarkets have historically formed the backbone of shampoo distribution in Indonesia, serving as the primary channel for branded mass-market products in urban and suburban areas. Large-format retailers such as Alfamart's larger formats, Hypermart, and Transmart offer extensive shelf space and promotional opportunities that brands rely on to drive visibility and trial. Convenience stores are also a significant channel, particularly for smaller sachet sizes that remain popular among price-sensitive consumers in lower-income brackets. Drug stores and pharmacies are gaining importance as medicated and dermatologist-recommended shampoos grow in relevance. The Online channel is the fastest-growing distribution mode, with platforms like Tokopedia, Shopee, and Lazada enabling brands to reach consumers across Indonesia's outer islands and rural regions that traditional retail chains underserve.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Within the product type segmentation, Non-Medicated shampoos hold the dominant share of the Indonesia shampoo market, driven by the large everyday-use consumer base that purchases functional hair care products as part of daily hygiene routines. The segment is reinforced by decades of brand-building from Unilever's Sunsilk, the number one shampoo brand in the country, and Procter & Gamble's Pantene, both of which compete primarily in the non-medicated space with continuous product innovation and heavy advertising investment. Medicated shampoos represent a stable and loyal niche anchored by anti-dandruff demand, with Clear and Head & Shoulders dominating this sub-category through strong brand recognition and wide retail availability across modern and traditional trade channels.

In the price category segmentation, the Mass segment accounts for the overwhelming majority of shampoo purchases in Indonesia by volume, reflecting the country's demographic structure, where a large proportion of the population remains price-sensitive and primarily accesses products through value-driven retail formats. The dominance of Mass is sustained by Unilever's extensive distribution network, which reaches both modern supermarkets and traditional neighborhood warungs across the entire archipelago. The Premium segment, while smaller in volume, is showing faster growth rates particularly in Java's metropolitan areas, where higher-income urban consumers are trading up to specialized formulations for scalp care, damage repair, and hair aesthetics. Premium growth is being fueled by Korean beauty brands, Kao's premium portfolio, and the growing influence of social media beauty content on consumer aspirations.

In the end user segmentation, Women are the dominant purchasing demographic, accounting for the majority of shampoo sales both in terms of units and value. Women drive the most dynamic product development activity within the market, as brands compete for loyalty through product format diversity, ingredient storytelling, and aspirational marketing. The Men's segment is the fastest-growing end user category, with gender-specific formulations addressing scalp health, dandruff control, and hair strengthening gaining broader consumer acceptance among urban Indonesian males. The Kids segment remains a steady volume contributor anchored by parental purchasing decisions oriented toward mild and safe formulations.

Within the distribution channel segmentation, Supermarkets and Hypermarkets retain the dominant share of shampoo sales in Indonesia, supported by the extensive retail infrastructure of major chains and their capacity to carry full product ranges across price tiers. Convenience stores hold a meaningful secondary position, particularly through sachet and small-format packaging that serves price-sensitive consumers efficiently. The Online channel is the segment with the fastest growth trajectory, reflecting Indonesia's strong digital adoption and the proven ability of e-commerce platforms to serve consumers across the archipelago who have limited access to modern trade stores.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The Indonesia shampoo market is highly competitive, shaped by a powerful combination of established global consumer goods multinationals and a growing cohort of domestic and regional players. Unilever holds the leading market position through its Sunsilk and Clear brands, which together dominate both the women's and medicated segments respectively. Procter & Gamble's Pantene and Head & Shoulders are close challengers across premium and anti-dandruff categories. Japanese and Korean brands are actively expanding their footprint, with Kao and emerging Korean beauty entrants targeting the premium and halal-certified segments that are growing fastest within the market.

Competitive dynamics in the Indonesia shampoo market are shaped by product formulation differentiation, halal certification status, influencer marketing effectiveness, distribution depth, and e-commerce activation. Domestic players such as PT LION WINGS and PT. PILLARS COSMETIKLON INDONESIA benefit from local manufacturing capabilities, cultural alignment with consumer preferences for herbal ingredients, and competitive pricing that resonates with cost-sensitive segments. Market share is actively contested, particularly in the Non-Medicated and Mass categories, where brand switching behavior is relatively high and loyalty is earned through product experience and digital engagement rather than inertia.

PT. PILLARS COSMETIKLON INDONESIA is an Indonesian personal care manufacturing company that specializes in the production and marketing of shampoo and cosmetics products for the domestic market. As a locally rooted company, it maintains cultural and formulation alignment with Indonesian consumer preferences, including the incorporation of halal-compliant ingredients and locally sourced botanical extracts. The company competes primarily in the mass price segment, leveraging its domestic manufacturing base and distribution relationships to maintain shelf presence across traditional trade and modern retail channels throughout the archipelago. Its understanding of Indonesia-specific consumer demands positions it as a relevant competitor to multinational brands in value and mid-range shampoo categories.

Founded in 1909 and headquartered in Clichy, France, L'Oreal SA is the world's largest beauty company with a broad portfolio spanning mass, premium, and luxury personal care, including its hair care brands Elvive (sold as Elseve in some markets), Garnier, and professional hair care lines. In Indonesia, L'Oreal operates across both modern trade and digital channels, targeting urban consumers with a growing appetite for science-backed hair care claims and premium formulation stories. The company's global R&D capabilities allow it to introduce innovations including bond repair technology and color-safe shampoos that resonate with the evolving aspirations of Indonesian urban women. L'Oreal's sustainability commitments around responsible ingredient sourcing and reduced plastic packaging are increasingly relevant to Indonesia's environmentally aware urban consumer segment.

Founded in 1929 and headquartered in London, United Kingdom, Unilever Plc is the dominant force in Indonesia's shampoo market through its Sunsilk and Clear brands. Sunsilk, the number one shampoo brand in Indonesia, is also the world's most-chosen hair care brand globally, sold in 69 countries and positioned as the leading women's hair care line. Clear is the number one anti-dandruff shampoo in Indonesia. Unilever Indonesia's extensive nationwide distribution network, which penetrates both modern retail and millions of traditional warungs, gives it an unparalleled reach advantage over competitors. In 2025, Unilever Indonesia relaunched over 85% of its core brands including shampoo lines as part of a major transformation program, reinforcing its commitment to innovation and consumer-led product development.

Founded in 1886 and headquartered in New Brunswick, New Jersey, USA, Johnson & Johnson Consumer Inc. operates in Indonesia primarily through its family-oriented and dermatologically tested personal care products under the Johnson's brand. The company's positioning around gentle, clinically validated formulations resonates strongly with health-conscious and family-oriented Indonesian consumers, particularly for children's hair care products and mild adult shampoos designed for sensitive scalps. J&J's emphasis on safety credentials and dermatological endorsement provides a differentiated positioning in a market where trust in product safety is a meaningful purchase motivator, particularly for the Kids and premium adult segments.

Other key players in the market are Procter and Gamble Company, PT LION WINGS, Kao Corporation, and Mandom Corp., and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Navigate the evolving dynamics of the Indonesia Shampoo market with confidence using our detailed 2026 forecast report. From the rise of halal-certified formulations and the growing appetite for natural ingredients, to e-commerce disruption and the premiumization wave reshaping urban purchasing habits, this report arms you with the data and insight you need to compete and grow. Whether you are entering the Indonesian market for the first time, expanding your product range, or refining your distribution strategy, this report provides the intelligence to move decisively. Download your free sample today and discover the opportunities shaping the future of Shampoo in Indonesia.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

At 2025, the market reached an approximate value of USD 550.00 Million.

The market is projected to grow at a CAGR of 3.70% between 2026 and 2035.

The key players in the market include PT. PILLARS COSMETIKLON INDONESIA, L'Oréal SA, Unilever Plc, Johnson & Johnson Consumer Inc., Procter and Gamble Company, PT LION WINGS, Kao Corporation, and Mandom Corp., among others.

The key trends shaping the Indonesia shampoo market include the growing centrality of halal certification as a commercial requirement, with government policy actively reducing compliance barriers for domestic brands. Consumer preference is shifting toward natural, herbal, and botanically derived formulations that align with both cultural values and sustainability consciousness. E-commerce is structurally transforming product distribution, enabling brands to reach geographically dispersed consumers across the archipelago. Premiumization is gaining traction in urban markets as rising incomes and social media influence drive consumer willingness to invest in specialized hair care experiences beyond basic daily cleansing.

The major product types considered in the market report are medicated and non-medicated.

The market is projected to grow significantly during the forecast period 2026 to 2035 to reach USD 790.95 Million by 2035.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Product Type |

|

| Breakup by Price Category |

|

| Breakup by End User |

|

| Breakup by Distribution Channel |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.