Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

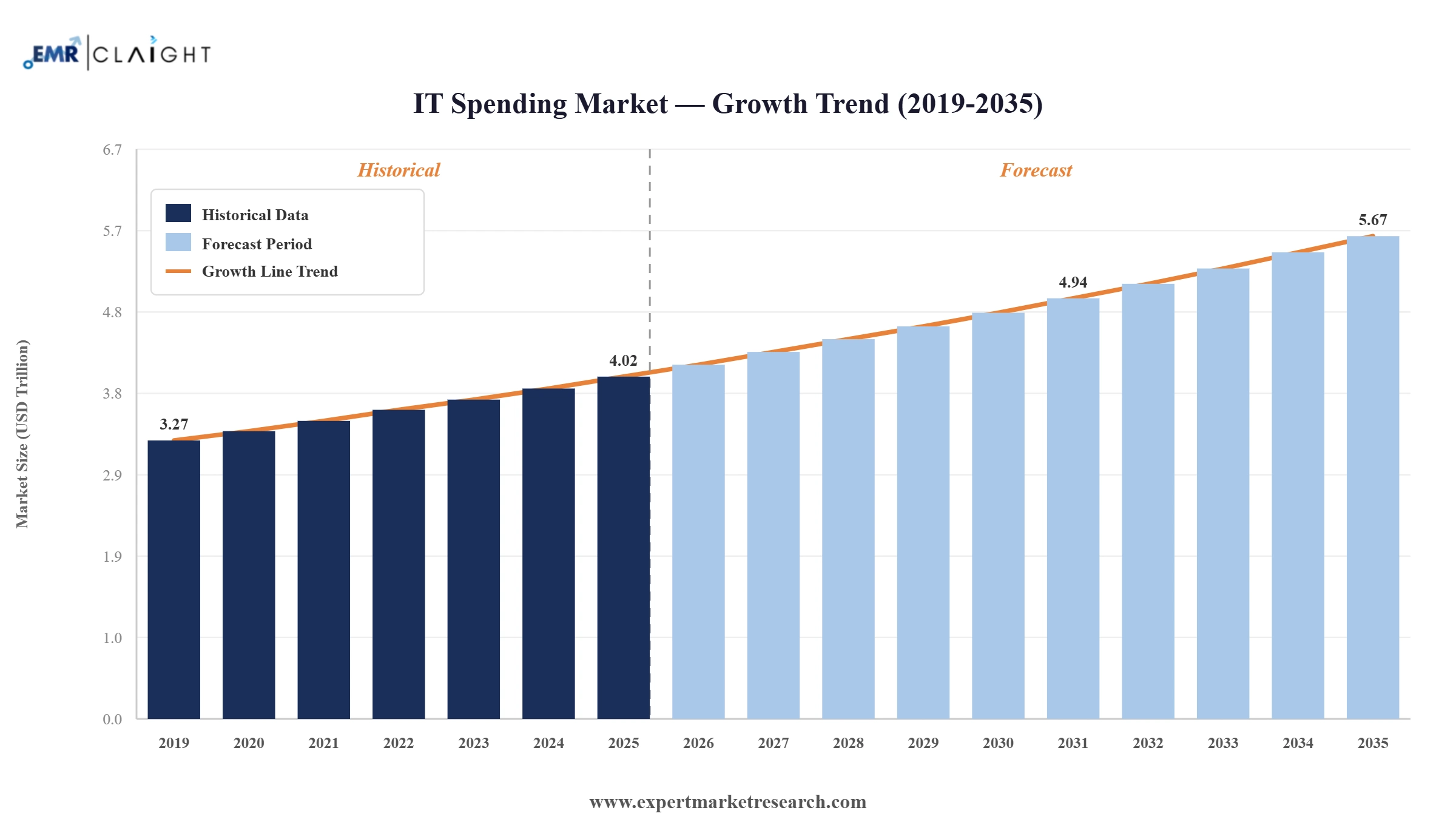

The global IT spending market attained a value of USD 4.02 Trillion in 2025 and is projected to expand at a CAGR of 3.50% through 2035. The market is further expected to achieve USD 5.67 Trillion by 2035. Growing enterprise spending on sovereign cloud infrastructure, AI-ready data center deployments, and cybersecurity resilience platforms is boosting IT investment while companies modernize critical business processes and ensure global regulatory compliance.

Companies are investing more in edge computing platforms to analyze real-time data close to consumers, which results in improved performance of applications and reduced latency. On top of that, growing popularity of pay-per-use IT purchasing models allows companies to scale their IT infrastructure and software resources based on emerging needs with limited initial capital spending. These factors are driving vendors to offer flexible subscription models, industry-specific digital solutions, and managed services.

The IT spending market observes a structural change, wherein companies are investing less in infrastructure and more in AI-based systems, cybersecurity, cloud applications, and intelligent automation solutions. For instance, in March 2026, Salesforce launched new autonomous AI agent functionalities in the enterprise environment so that companies can use Agentforce to automate their complex workflow processes. This development shows how enterprise software vendors are shifting the focus of product offerings from individual applications to generative AI.

Enterprise customers are showing increasing willingness to invest in integrated technology stacks comprising cloud infrastructure, AI models, cybersecurity solutions, analytics services, and applications for specific industries. Major technology firms such as Microsoft, Oracle, Amazon Web Services, SAP, and IBM are forming strategic partnerships to integrate AI capabilities, reshaping the IT spending market dynamics. For instance, in June 2026, OpenAI launched enhanced ChatGPT Enterprise usage analytics and spend controls, helping organizations monitor AI adoption and manage costs.

Additionally, hyperscale cloud computing providers are making significant investments in AI infrastructure, processors, and sovereign clouds to satisfy the compliance needs of enterprises. Such trends in the IT spending market are encouraging banks, manufacturing companies, hospitals, retailers, and other businesses to move away from fragmented legacy systems and adopt comprehensive digital platforms that facilitate real-time decisions and business automation. For example, in May 2026, Punjab National Bank increased cybersecurity investments to strengthen AI-driven threat detection against emerging risks from advanced AI models.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

| IT Spending Market Report Summary | Description | Value |

| Base Year | USD Trillion | 2025 |

| Historical period | USD Trillion | 2019-2025 |

| Forecast Period | USD Trillion | 2026-2035 |

| Market Size 2025 | USD Trillion | 4.02 |

| Market Size 2035 | USD Trillion | 5.67 |

| CAGR 2019-2025 | Percent | XX% |

| CAGR 2026-2035 | Percent | 3.50% |

| CAGR 2026-2035 - Market by Region | Asia Pacific | 4.5% |

| CAGR 2026-2035 - Market by Country | India | 5.2% |

| CAGR 2026-2035 - Market by Country | China | 4.6% |

| CAGR 2026-2035 - Market by Type | Enterprise IT Services | 4.1% |

| Market Share by Country | Japan | 6.4% |

AI services were introduced by ServiceNow and Accenture that can update legacy risk systems and allow agentic AI, automated governance, and increased efficiencies. This development indicates how technology vendors can provide AI governance, compliance, and migration services to help enterprises move away from legacy IT systems.

Apptio introduced an AI-powered solution that provides enterprises with real-time technology spending insights. This will aid them in making effective use of their IT budgets and cloud investments. Software vendors can introduce AI-powered solutions for FinOps and IT cost optimization, leveraging such developments in the IT spending market.

Publicis Sapient created an AI-powered IT operations platform which automates support processes, increases service reliability, and decreases operating costs within enterprises. IT service companies may grow their autonomous operations platforms to increase efficiency and decrease infrastructure and support costs.

Meta introduced paid subscriptions for Instagram, Facebook, and WhatsApp, increasing premium digital services and opening up opportunities for enterprise revenue generation. Digital platform operators can offer subscription-based services to businesses, earning regular revenue while boosting the IT spending market value.

AI infrastructure is becoming the biggest driving factor for enterprise IT expenditures as businesses go beyond pilot programs and towards full production. Businesses are investing in GPU clusters, AI data platforms, vector databases, and enterprise copilots to automate knowledge-based processes. To support this trend in the IT spending market, the United States government introduced the Stargate initiative aimed at speeding up investments into domestic AI infrastructure in January 2025. As a result, financial companies, manufacturing companies, and healthcare firms are modernizing technology stacks and enhancing operational efficiency and scalability. As an example, Palantir launched an AI engine with NVIDIA Nemotron, enabling secure sovereign AI deployments for government and critical infrastructure environments in June 2026.

To increase digital resilience, data protection, and compliance with governmental regulations, governments accelerate sovereign cloud adoption, providing opportunities for IT spending market growth. Enterprises dealing with sensitive data often need to use locally hosted clouds compliant with national rules of data governance. Oracle, Google Cloud, Microsoft, and AWS keep extending their sovereign cloud capabilities in different regions to meet this demand. The European Union's Digital Decade Program also stimulates modernizing cloud infrastructures within public institutions and enhancing their cybersecurity capabilities. Aligning with tjis trend, in June 2026, LTM partnered with OVHcloud to deliver sovereign cloud and AI solutions, enabling secure, compliant digital transformation across Europe.

Cyber threats on the rise and increased compliance regulations are compelling companies in the IT spending market to unify various disparate security systems into an integrated cyber security platform. Instead of using fragmented software tools, businesses are leveraging a unified security operations suite, artificial intelligence for threat detection, identity management systems, and expanded threat detection and response mechanisms. For instance, Palo Alto Networks continues offering Precision AI-driven security solutions aimed at automating threat protection. On the other hand, in April 2026, Microsoft announced a USD 10 billion investment in Japan, expanding AI infrastructure, cybersecurity capabilities, and workforce development through 2029.

Cloud platforms built by technology companies specifically designed for certain industries are becoming popular as opposed to enterprise-focused cloud platforms. Companies such as SAP, Salesforce, Oracle, and IBM are constantly updating cloud offerings designed for specific industries such as manufacturing, healthcare, retail, banking and financial services, and telecommunications, broadening the IT spending market scope. Such cloud platforms incorporate AI, analytics, regulatory compliance, and workflow automation all together in one environment. India's Digital Public Infrastructure and digital economy strategies are also driving digital transformation in technology spending by enterprises. In June 2026, TCS partnered with Tottenham Hotspur to deliver AI-powered digital transformation, enhancing fan engagement, cybersecurity, and club operations.

The growth in AI workloads is increasing the need for efficient data centers, hence prompting IT spending market players to re-design their data center infrastructure using sustainable goals. Hyperscale players are focusing on developing efficient cooling, renewables, liquid cooling, and better processors to cut down operating costs as well as provide efficient high-performance computing. The International Energy Agency is focusing on the improvement of energy efficiency in data centers due to rapid growth of digital infrastructure across the world. In June 2026, Solvexel Energy Technologies launched a digital energy management platform, supporting global renewable energy operations and international business expansion.

The Expert Market Research’s report titled “Global IT Spending Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

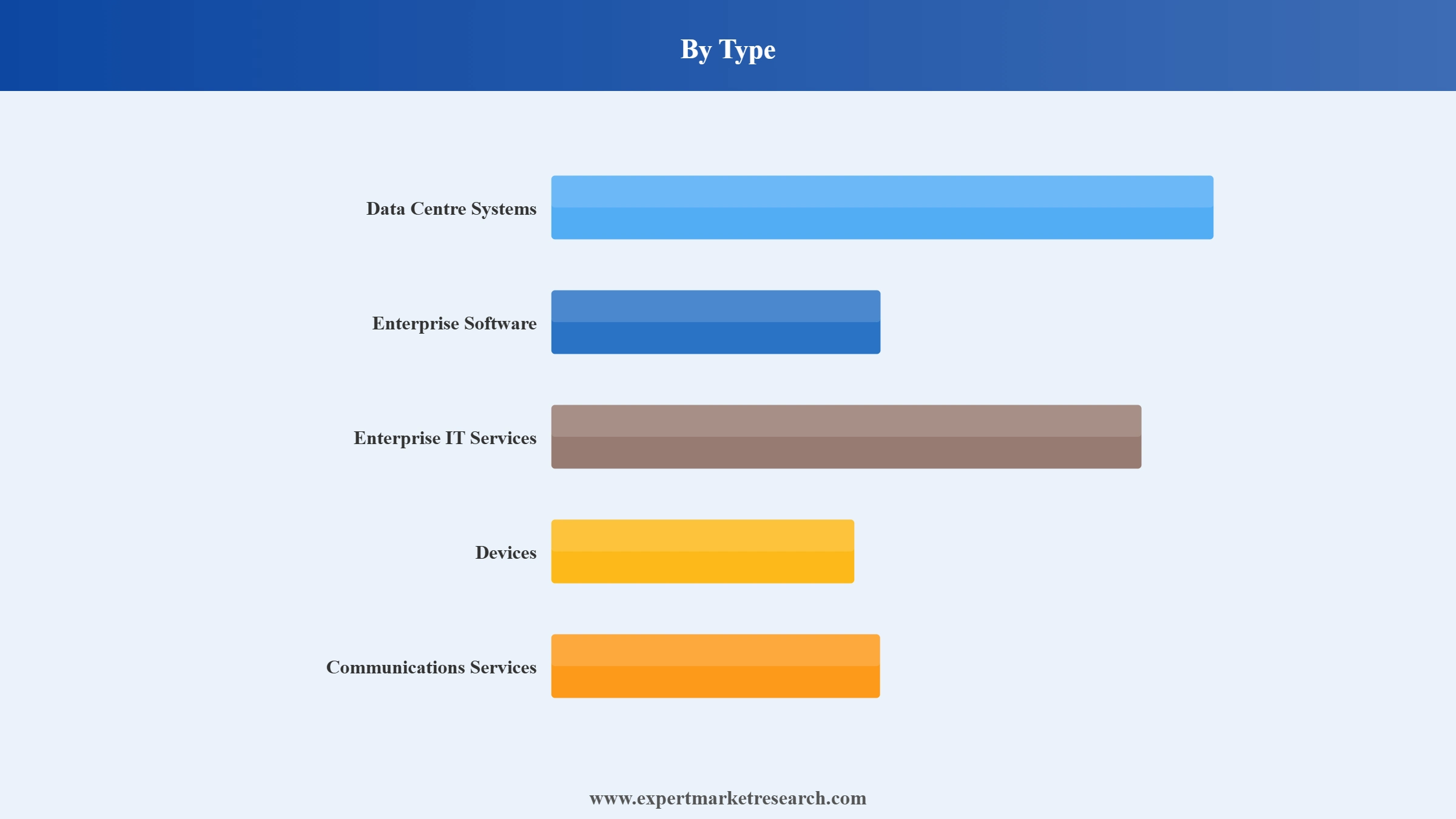

Breakup by Type

Key Insight: The global IT spending market report considers five major categories including Data Center Systems, Enterprise Software, Enterprise IT Services, Devices, and Communications Services. These five categories play roles that meet different priorities in terms of transformation within enterprises. Enterprise Software is positioned at the forefront owing to the digital business platform, Data Center Systems benefit from increased investments in AI infrastructure, whereas Enterprise IT Services keep on growing due to consulting and customized software applications. Devices have an important role to play because of hybrid working, where it is needed to be assured of endpoints and hardware productivity. In addition, Communications Services are becoming crucial as they are required to ensure cloud connection and secure digital interactions.

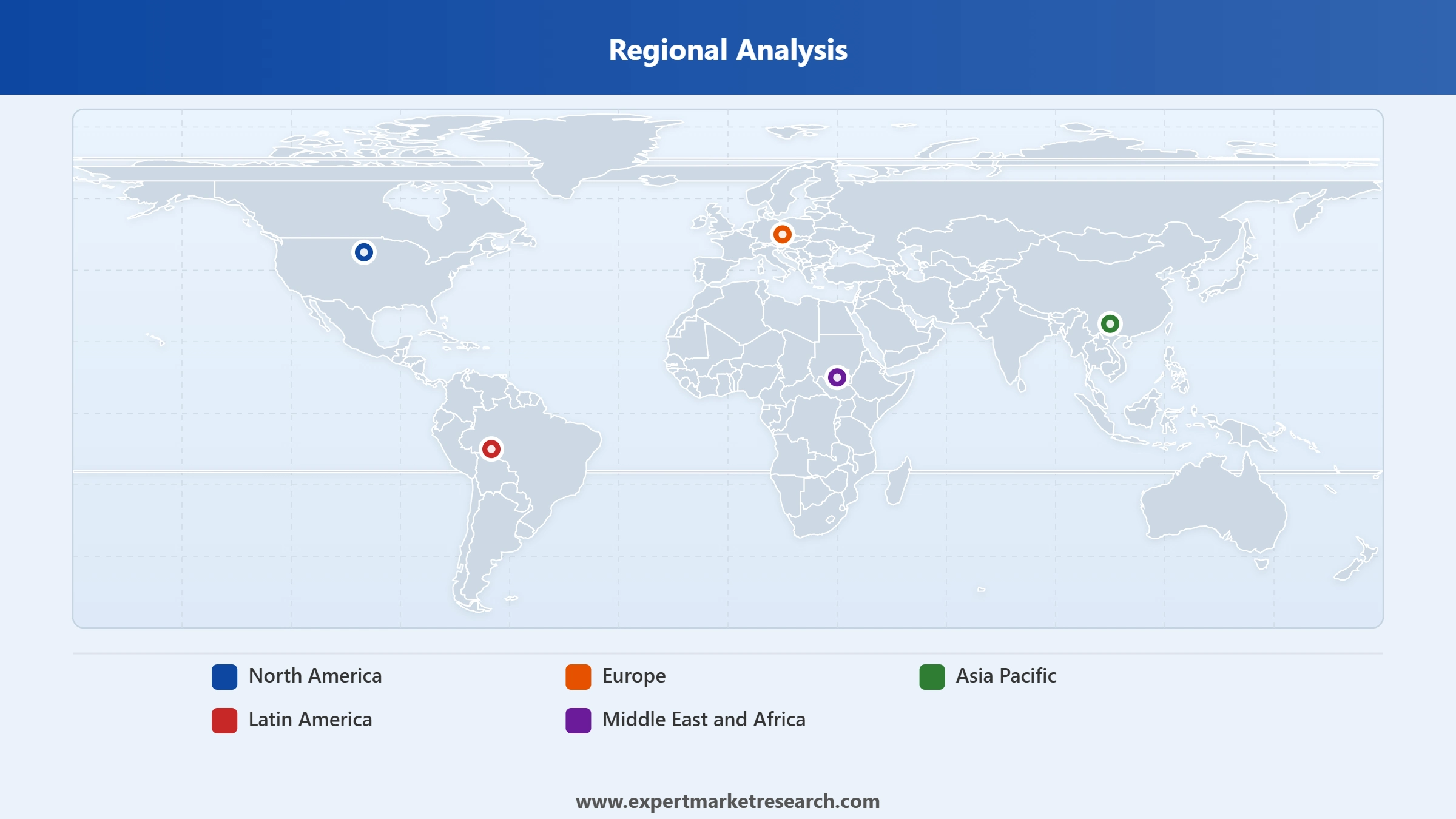

Breakup by Region

Key Insight: The North American region dominates the global IT spending market through advanced enterprise technology eco-systems and continuous investments in innovations. Europe enjoys the advantage of stringent regulatory compliance, industrial automation, and safe cloud usage in developed countries. The Asia Pacific region experiences the highest growth due to quick digitization of digital infrastructures and business operations in enterprises. The Latin American region observes the rising adoption of enterprise cloud along with digital business transformation initiatives. The Middle East and Africa market keeps growing through smart cities initiatives, digital government approach, telecommunication modernization, and enterprise cloud adoption.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By type, enterprise software dominates the market due to accelerating enterprise-wide AI integration and digital workflow modernization

Enterprise software continues to be the leading segment in the IT spending market as companies are focused on using integrated platforms that unite finance, operations, human resources, customers, and supply chains in one digital ecosystem. Companies increasingly use cloud-native applications that can support the development of analytics and automation based on artificial intelligence. Investments in enterprise resource planning, customer relationship management, business intelligence, and content management systems help companies increase their productivity, decision-making abilities, and compliance. In June 2026, Lenovo launched Hybrid AI Advantage innovations, enabling agentic AI deployment with lower inference costs and enterprise-scale AI performance.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The Data Center Systems category represents the fastest growing segment, and this is because companies and hyperscale cloud vendors make efforts to build computing infrastructures that can support growing demands. They are investing in advanced servers, clusters of GPUs, storage facilities, networking devices, and liquid cooling technologies that are needed to effectively process the heavy loads that come from the development of artificial intelligence. Adoption of hybrid cloud strategy, real-time analytics, and edge computing technologies is speeding up the infrastructure modernization process, boosting the IT spending industry growth. In May 2026, Blackstone and Google committed USD 5 billion to launch an AI cloud company delivering scalable TPU-powered compute infrastructure.

North America dominates the market through advanced enterprise digital transformation and hyperscale cloud investments

North America retains its leadership in the global IT spending market due to constant investments in the development of innovative software solutions, artificial intelligence infrastructure, cybersecurity tools, and cloud-native technologies. The region hosts numerous technology providers, hyperscale cloud computing companies, and innovators in digital services, which continually enrich enterprise software portfolios. High levels of technology adoption in the banking, healthcare, manufacturing, retail, and government segments also contribute to ongoing spending. Enterprises seek automation, predictive analytics, and intelligent business applications to remain competitive, while established venture capital communities and enterprise innovation initiatives constantly fuel technology adoption. In December 2025, Microsoft announced a CAD 19 billion AI investment in Canada, expanding cloud infrastructure, cybersecurity, and digital workforce capabilities.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The IT spending market in Asia Pacific experiences rapid growth due to ongoing migrations to the cloud, adoption of artificial intelligence, and digitization of infrastructure within fast-growing markets. Companies increase spending on enterprise software, cybersecurity, data centers, and managed IT services in order to increase agility and engage with customers better. Government-driven programs to develop a digital economy, growing ecosystem of startups, and manufacturing automation also drive enterprise technology spending. Increasing use of small and medium enterprises, along with growing adoption of digital payments and e-commerce, further strengthens regional technology spending.

The competitive environment in the market is defined by the trends associated with AI adoption in enterprises, growth of the cloud ecosystem, innovation in cybersecurity, and platform consolidation. Leading IT spending companies invest in building industry-specific AI models, sovereign clouds, intelligent automation, and comprehensive software platforms that can demonstrate real business results. Partnerships with chipmakers, cloud vendors, and systems integrators are becoming crucial for quick enterprise digital transformation.

There are opportunities in building AI-ready infrastructure, secure multi-clouds, and vertical enterprise software products in healthcare, manufacturing, finance, and retail. IT spending market players are also targeting edge computing and sustainability-related data center technologies. To succeed in the market, technology companies need to provide interoperable platforms, scalable AI tools, regulatory compliance, and innovation in their products.

Alphabet Inc. was founded in 2015 and is headquartered in Mountain View, California, United States. Alphabet Inc. supports the IT spending market through Google Cloud, AI infrastructure, cybersecurity, data analytics, collaboration capabilities, and enterprise software. The company's investment in generative AI, cloud modernization, and digital transformation helps organizations maximize their IT investments.

Microsoft Corp. was founded in 1975 and is headquartered in Redmond, Washington, United States. Microsoft Corp. supports the market growth through Azure cloud services, Microsoft 365, Dynamics 365, cybersecurity offerings, and Copilot offerings based on AI. The company's enterprise ecosystem helps businesses modernize their infrastructure, automate processes, and improve productivity.

Amazon.com, Inc. was founded in 1994 and is headquartered in Seattle, Washington, United States. Amazon.com, Inc. offers Amazon Web Services, providing cloud computing, storage, databases, AI, machine learning, analytics, and security support . The company's scalable cloud infrastructure allows enterprises to minimize their capital expenditure while digital transformation accelerates.

Dell Inc. was founded in 1984 and is headquartered in Round Rock, Texas, United States, Dell Inc. serves the market through enterprise servers, storage devices, personal computers, networking, edge computing, and infrastructure solutions. The company offers support for hybrid cloud, AI-ready infrastructure, cybersecurity, and digital workplace modernization.

Other key players in the market include Cisco Systems, Inc., Oracle Corp., IBM Corp., Lenovo Group, HP Development Company, L.P., Accenture plc, Infosys Ltd., and Capgemini SE, among others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Unlock the latest insights with our IT spending market trends 2026 report. Discover regional growth patterns, consumer preferences, and key industry players. Stay ahead of competition with trusted data and expert analysis. Download your free sample report today and drive informed decisions in the market.

Upto 15% Off

USD

$3999 $3599

$2499 $2249

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market reached an approximate value of USD 4.02 Trillion.

The market is projected to grow at a CAGR of 3.50% between 2026 and 2035.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach about USD 5.67 Trillion by 2035.

The emerging trends include the growing awareness regarding the benefits of AI audit management, the rising economic development, and the increasing investments to boost the security of IT.

North America dominates the market by its robust digital infrastructure, widespread cloud adoption, and leadership in AI and cybersecurity

The major types of IT spending in the market are data centre systems, enterprise software, enterprise IT services, devices, and communication services.

IT spending is the total money spent on IT systems and services by an organisation. IT spending is not only limited to IT organisations but is a significant aspect across diverse businesses, enabling the construction and maintenance of large-scale digital infrastructure and services.

Cloud Application Infrastructure Services (PaaS), Cloud Application Services (SaaS), and Cloud Business Process Services (BPaaS) contribute significantly to the market.

Key strategies driving the market include accelerated digital transformation, cloud migration, adoption of AI and automation, and focus on cybersecurity. Enterprises are investing in scalable infrastructure, enterprise software, and managed services to boost efficiency, enhance customer experience, and maintain competitiveness in an increasingly technology-driven global economy.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| Report Features | Details |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Type |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Report Price and Purchase Option | Explore our purchase options that are best suited to your resources and industry needs. |

| Delivery Format | Delivered as an attached PDF and Excel through email, with an option of receiving an editable PPT, according to the purchase option. |

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.