Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

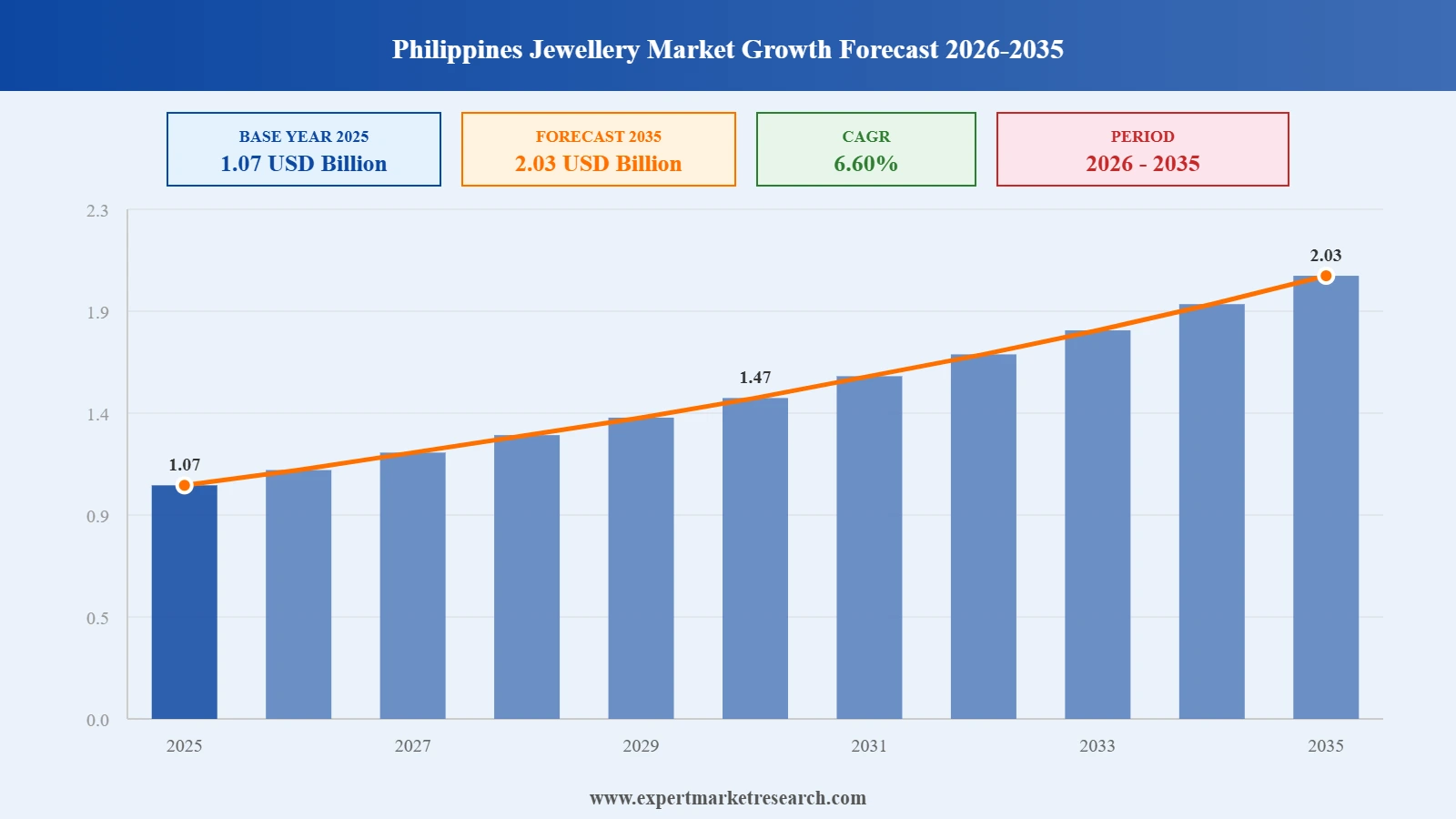

The Philippines Jewellery Market reached a value of USD 1.07 Billion at 2025 and is projected to expand at a CAGR of around 6.60% during the forecast period of 2026-2035. With rising household incomes driving demand for premium accessories, the rapid growth of online and live-selling platforms, expanding cultural significance of jewellery across milestone occasions, and the growing popularity of lab-grown and ethically sourced gemstones, the market is expected to reach USD 2.03 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

|

Philippines Jewellery Market Report Summary |

Description |

Value |

|

Base Year |

USD Billion |

2025 |

|

Historical period |

USD Billion |

2019-2025 |

|

Forecast Period |

USD Billion |

2026-2035 |

|

Market Size 2025 |

USD Billion |

1.07 |

|

Market Size 2035 |

USD Billion |

2.03 |

|

CAGR 2019-2025 |

Percentage |

XX% |

|

CAGR 2026-2035 |

Percentage |

6.60% |

|

CAGR 2026-2035 - Market by Product Type |

Ring |

7.5% |

|

CAGR 2026-2035 - Market by Material Type |

Gold |

7.3% |

The Expert Market Research report titled “Philippines Jewellery Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

Breakup by Product Type

Key Insight: Necklaces command a leading share in the Philippines jewellery market, underpinned by the deep cultural significance of necklace gifting and wearing during fiestas, weddings, and milestone occasions among Filipino women. The accessibility of stylish and affordable necklace designs through both physical retail and online channels continues to broaden the consumer base. Rings represent the fastest-growing product category, posting a CAGR of 7.5% through the forecast period, driven by surging demand for engagement rings featuring diamonds, emeralds, sapphires, and rubies. Earrings maintain steady traction as everyday accessories, with innovations in drop and stud designs, including the February 2025 Merit Beauty and Completedworks collaboration, catering to the growing millennial and Gen Z segment. Charms and bracelets benefit from the personalisation trend, with consumers seeking stackable and custom-engraved options.

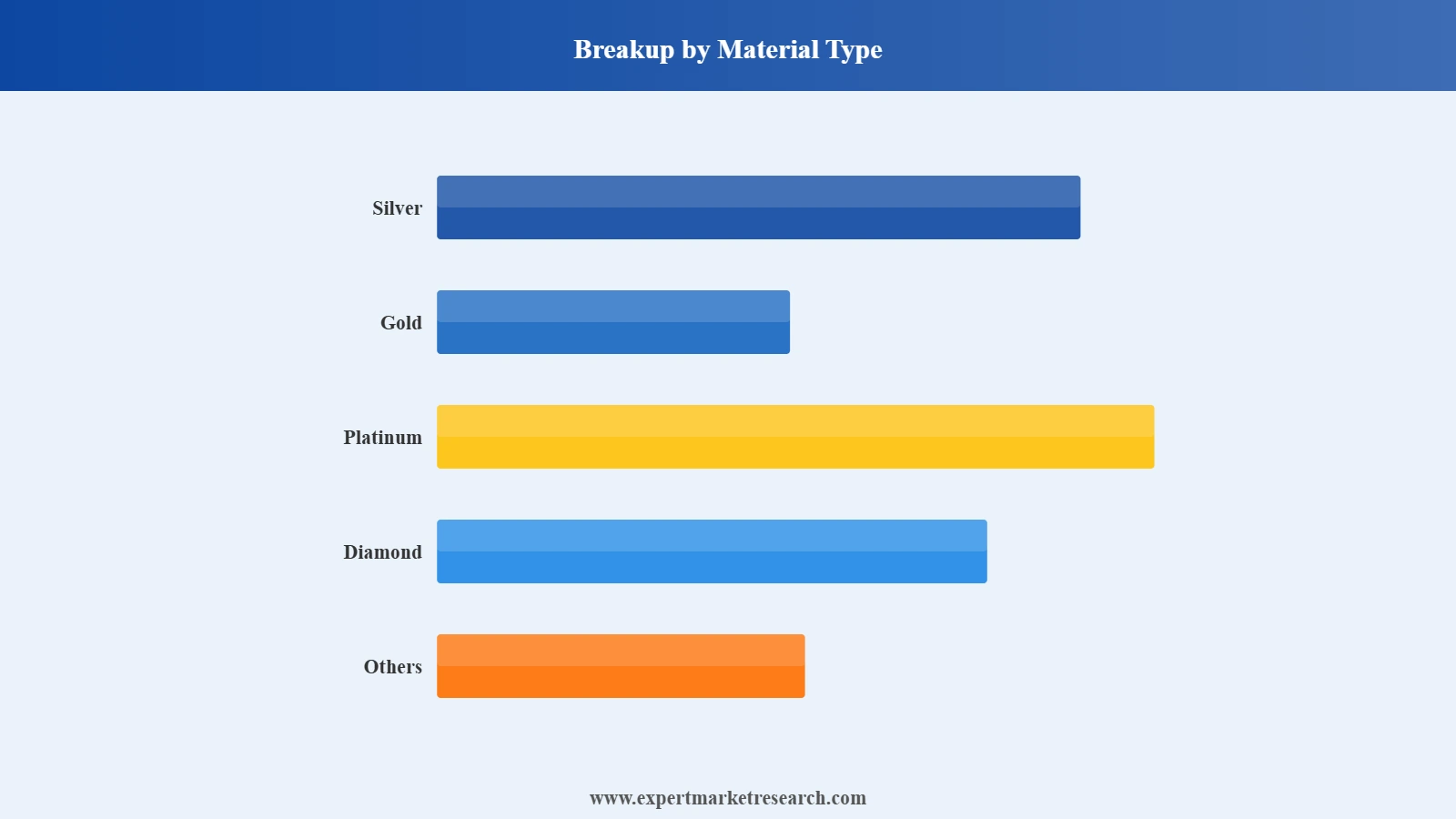

Breakup by Material Type

Key Insight: Gold remains the dominant material in the Philippine jewellery market, with a projected CAGR of 7.3% through 2035. Gold's dual function as a fashion statement and a store of value resonates strongly with Filipino consumers, particularly as artisanal and small-scale gold mining continues to expand. Silver is gaining notable ground among millennials and Gen Z shoppers who prize affordability and hypoallergenic properties, with fast fashion trends further accelerating demand. Diamond jewellery is experiencing increased traction driven by rising imports and the growing availability of lab-grown alternatives, which make diamond pieces accessible to a broader income bracket. Platinum occupies a niche premium tier, while other materials such as stainless steel and titanium serve the growing hypoallergenic and fashion jewellery sub-segments.

Breakup by Category

Key Insight: Branded jewellery holds the premium segment of the Philippine market, supported by the growing penetration of international luxury labels such as BVLGARI and the strong domestic heritage of brands like Jewelmer. Filipino consumers are increasingly associating branded jewellery with quality assurance, emotional significance, and investment value, particularly among the growing base of high-net-worth individuals. Unbranded jewellery, while commanding higher volume, is evolving in quality and design as local artisans and independent designers produce fashion-forward and culturally inspired pieces at accessible price points. The distinction between the two segments is narrowing as local independent creators build recognisable brand identities through social commerce and international exhibitions.

Breakup by End User

Key Insight: Women represent the dominant end-user segment in the Philippines jewellery market, accounting for the majority of purchases across necklaces, earrings, rings, and bracelets. The expanding female population and rising incomes among Filipino women are reinforcing this dominance. The men's segment, while smaller, is growing meaningfully as cultural attitudes toward male jewellery shift and brands create collections specifically targeting male consumers. Brands such as SilverWorks have broadened their portfolio to address hypoallergenic and fashion-forward accessories for men, capitalising on growing male grooming and styling consciousness in urban areas.

Breakup by Distribution Channel

Key Insight: Offline distribution, anchored by traditional jewellery boutiques and department store counters, retains the largest share, given the Philippine consumer's preference for physically assessing weight, shine, authenticity, and fit before purchasing high-value items. Flagship stores also function as experience centres that reinforce brand narrative and trust. Online distribution is the faster-growing channel, powered by the Philippines' 86.98 million internet users and the explosive popularity of live-selling on social commerce platforms. Digital platforms allow independent designers to bypass costly physical retail infrastructure while reaching audiences across the archipelago's dispersed island geography. Omnichannel strategies that combine online discovery with offline verification are increasingly preferred by premium jewellery buyers.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Product Type, necklaces lead the Philippines jewellery market in volume terms, sustained by the product's central role in Filipino cultural ceremonies, religious observances, and gifting traditions. The affordability of necklace options across a wide price range ensures broad consumer access. Rings are the fastest-growing product sub-segment, recording a projected CAGR of 7.5% through the forecast period. The strong social tradition of gifting rings for engagements, anniversaries, and milestones, combined with the growing availability of diverse gemstone options, is anchoring this growth. Leading brands including Jewelmer, F&C Jewelry, and SilverWorks actively develop ring collections that cater to multiple price tiers.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Material Type, gold holds the dominant share, reflecting its deep cultural meaning as a symbol of prosperity and its recognized value as a financial asset in Filipino households. The Philippines' own gold mining industry provides a degree of domestic supply, further supporting availability and consumer familiarity with gold products. Silver is the most dynamically growing alternative material, particularly among younger shoppers who seek stylish, affordable, and skin-friendly options. The millennial and Gen Z cohorts are disproportionately driving silver jewellery adoption, and brands such as SilverWorks have built their entire market proposition around this segment, producing stainless steel and titanium pieces alongside silver to serve a broad range of style preferences and budgets.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Distribution Channel, offline retail channels currently dominate sales, particularly in the fine and branded jewellery segment where physical inspection of the product is considered important by consumers before purchase. However, online channels are closing the gap rapidly. Social commerce platforms and live-selling sessions on video apps have created new, low-barrier-to-entry retail environments for independent Philippine jewellery designers, enabling them to engage directly with consumers and build communities. Cebuana Lhuillier's 2024 investment in Sparkles.ph signals financial services players moving into this digital jewellery space, adding further momentum to online channel growth.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Luzon, and Metro Manila in particular, is the undisputed centre of the Philippines jewellery market. The National Capital Region concentrates the largest share of the country's high-net-worth individuals, the densest network of branded and independent jewellery boutiques, and the most active consumer base for both fine and fashion jewellery. The November 2024 launch of BVLGARI's high jewellery line in the Philippines was targeted squarely at Manila's luxury consumer segment, underscoring the capital's standing as the market's commercial epicentre. Household incomes in Metro Manila consistently outpace the national average, enabling higher per-capita spending on accessories. Additionally, Meycauayan in Bulacan, part of the broader Central Luzon area, functions as the country's jewellery manufacturing heartland, supplying both local retail and export markets with handcrafted gold pieces.

Visayas, led by Cebu City, represents the market's most active secondary growth hub. Cebu's established reputation as a manufacturing and commercial city has facilitated the development of local jewellery retailers and craft producers. Rising household incomes across the Visayas region, combined with the Cebuano consumer's well-documented appetite for premium fashion and lifestyle products, are sustaining demand growth. Regional jewellery brands are expanding their physical presence in Cebu and surrounding provinces, while ecommerce penetration is steadily improving access to branded products for consumers in smaller Visayan cities and towns. The cultural significance of jewellery in Visayan festivals and wedding traditions adds a recurring seasonal demand driver that benefits both local artisans and branded retail channels.

The Philippines jewellery market operates across two distinct tiers: a premium branded segment dominated by established local luxury houses and international labels, and a large, fragmented unbranded segment served by thousands of independent artisans and fashion jewellery producers. Competitive intensity is moderate at the top tier, where brand heritage, design originality, and quality assurance serve as principal differentiators. The growing ecommerce and live-selling ecosystem is lowering entry barriers, allowing emerging independent brands to build national visibility without the capital expenditure of physical retail infrastructure.

The competitive landscape is shaped by a mix of century-old local jewellery houses, internationally recognised luxury brands making deeper inroads into the Philippine market, and a new generation of digitally-native jewellery startups. Leading players are prioritising product collaborations, sustainable sourcing credentials, and digital community building as core competitive strategies. The entry of BVLGARI into the Philippine high jewellery segment in late 2024 is expected to intensify premium market competition and raise consumer expectations around design and brand experience.

Founded in 1979 and headquartered in Makati, Jewelmer is the Philippines' pre-eminent luxury jewellery brand and one of the world's foremost producers of South Sea pearls. The company operates pearl farms across the Sulu Sea and has cultivated an international reputation for exceptionally high-quality golden pearls. Jewelmer's product range includes fine jewellery centred on pearls, complemented by bespoke couture collections developed through high-profile collaborations with Filipino fashion designers. The brand maintains a selective retail footprint in the Philippines and international markets, positioning itself firmly in the luxury tier.

Founded in 1973 and headquartered in Manila, F&C Jewelry has built its market position around providing fine jewellery for milestone occasions such as weddings, anniversaries, and significant celebrations. The company is known for its craftsmanship in gold and gemstone jewellery, with a portfolio tailored to Filipino cultural traditions and gifting practices. F&C Jewelry maintains physical stores across major Metro Manila retail destinations and is recognised for its personalised customer service approach, which has sustained long-term customer loyalty across multiple generations of Filipino buyers.

Sep Vergara Fine Jewelry is a prominent Philippine fine jewellery label known for its sophisticated and contemporary design language applied to precious metals and gemstones. The brand targets affluent Filipino consumers seeking distinctive, investment-grade pieces that combine international design sensibility with Philippine craftsmanship. Sep Vergara's portfolio spans rings, necklaces, and bespoke commissions, and the brand has maintained a strong presence in Metro Manila's premium retail segment. Its design-led positioning differentiates it from traditional jewellery houses and appeals to a younger, style-conscious luxury consumer.

SilverWorks is one of the Philippines' most widely recognised fashion jewellery brands, built around the proposition of delivering affordable, stylish, and hypoallergenic accessories to mainstream Filipino consumers. The brand uses tungsten, stainless steel, and titanium as primary materials, addressing the growing demand for non-tarnish, skin-friendly jewellery among millennial and Gen Z shoppers. SilverWorks operates a broad physical retail network across Philippine malls and shopping centres, supported by a growing online presence. The brand's accessible price points and trend-responsive collections make it a key player in the high-volume unbranded-to-fashion-branded transition segment.

Other key players in the market are Lily & Co., B&Co Jewelry, HansBrumann, Penny Pairs, Modern Myth, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

The Philippines jewellery industry contends with structural compliance and supply pressures that complicate scaling. Designated jewellery dealers fall within the covered-person framework of the Anti-Money Laundering Council under Republic Act 11521, requiring know-your-customer documentation and suspicious transaction reporting that strain smaller workshops in Meycauayan, Bulacan. Inconsistent enforcement of Bureau of Philippine Standards hallmark rules, persistent smuggling through informal channels documented by the Bureau of Customs, climate exposure of South Sea pearl farms monitored by PAGASA, and a thinning pipeline of master artisans further test operating resilience.

Several restraints temper near-term momentum. The 12 percent value-added tax on retail sales and the TRAIN Law excise framework on non-essential goods lift end-consumer prices, while peso depreciation against the US dollar through 2026 has raised landed costs for platinum, coloured stones, and bench equipment. Limited domestic gold refining capacity, tight working-capital access for cottage workshops, and onboarding friction within the Bangko Sentral ng Pilipinas small-scale mining gold purchase programme under Republic Act 11256 also constrain margins.

Opportunities are widening through formalisation and export-led demand. Jewelmer's Mindanao South Sea pearl franchise, the CITEM Manila FAME platform, Department of Tourism arrivals across Boracay, Cebu, and Palawan, Christmas and debut bridal cycles, OFW remittance-led purchases, and rising e-commerce traction on Lazada, Shopee, and TikTok Shop are anchoring growth.

Looking for an edge in the Philippines jewellery space? Our comprehensive 2026 report delivers the data and strategic clarity you need, from ecommerce disruption and lab-grown diamond adoption to the moves of leading brands like Jewelmer and SilverWorks. Whether you are entering the market, expanding your product range, or evaluating investment opportunities in Philippine jewellery, this report gives you a clear and current picture. Download your free sample today and start uncovering the opportunities shaping Philippine jewellery's next decade.

Latin America Jewellery Market

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, Philippines jewellery market reached an approximate value of USD 1.07 Billion.

The market is projected to grow at a CAGR of 6.60% between 2026 and 2035.

The market is estimated to witness healthy growth in the forecast period of 2026-2035 to reach a value of around USD 2.03 Billion by 2035.

The major drivers of the market are the growing female population, ease of internet access and increasing gold mining activities.

The key trends of the market include the popularity of lab grown diamonds, increasing partnerships and the abundance of pearls.

The various types considered in the market report are necklace, ring, earrings, charms and bracelets and others.

The various materials considered in the market report are silver, gold, platinum, diamond and others.

The categories considered in the market report are branded and unbranded.

The end users considered in the market report are men and women.

The major players in the market are Jewelmer, F&C Jewelry, Sep Vergara Fine Jewelry, SilverWorks, Lily & Co., B&Co Jewelry, HansBrumann, Penny Pairs, Modern Myth, and others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Product Type |

|

| Breakup by Material Type |

|

| Breakup by Category |

|

| Breakup by End User |

|

| Breakup by Distribution Channel |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.