Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

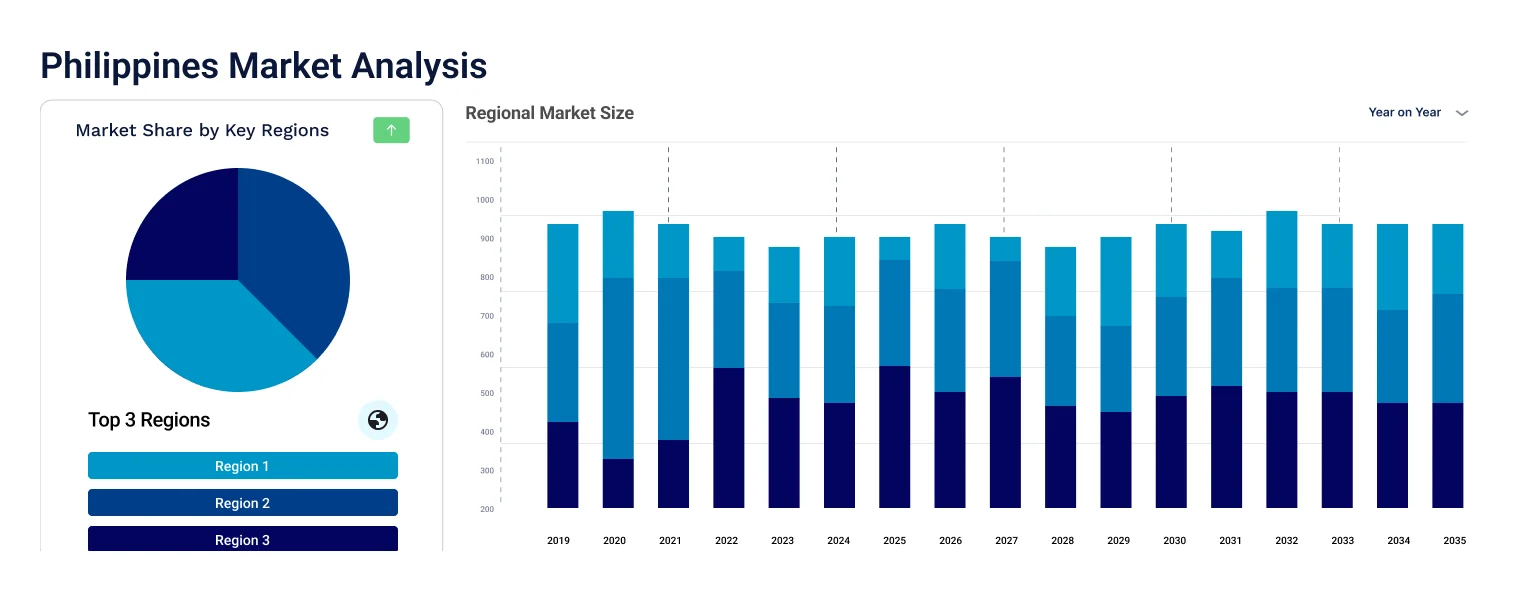

The Philippines Non-Life Insurance Market reached a value of USD 2.26 Billion at 2025 and is projected to expand at a CAGR of around 7.30% during the forecast period of 2026-2035. With high natural disaster exposure driving property and catastrophe coverage demand, rising vehicle ownership boosting motor insurance, expanding insurtech and bancassurance distribution, and microinsurance growth reaching underserved populations, the market is expected to reach USD 4.57 Billion by 2035.

Base Year

Historical Period

Forecast Period

Compound Annual Growth Rate

7.3%

Value in USD Billion

2026-2035

*this image is indicative*

| Philippines Non-Life Insurance Market Report Summary |

Description |

Value |

|

Base Year |

USD Billion |

2025 |

|

Historical Period |

USD Billion |

2019-2025 |

|

Forecast Period |

USD Billion |

2026-2035 |

|

Market Size 2025 |

USD Billion |

2.26 |

|

Market Size 2035 |

USD Billion |

4.57 |

|

CAGR 2019-2025 |

Percentage |

XX% |

|

CAGR 2026-2035 |

Percentage |

7.30% |

|

CAGR 2026-2035- Market by Insurance Type |

Travel Insurance |

8.3% |

|

CAGR 2026-2035 - Market by Insurance Type |

Property Insurance |

7.8% |

|

CAGR 2026-2035 - Market by Service Provider |

Private Insurance Providers |

7.9% |

|

CAGR 2026-2035 - Market by End User |

Individual |

7.7% |

| 2025 Market Share by Insurance Type | Motor Insurance |

XX% |

The Philippines Non-Life Insurance Market is being reshaped by the convergence of climate-driven demand for catastrophe coverage, rapid digitalization of distribution and claims processing, government-backed financial inclusion initiatives, and the expansion of bancassurance and insurtech partnerships. These factors are collectively deepening insurance penetration and broadening the product mix available to Filipino consumers and businesses.

The Philippines' position as one of the world's most disaster-prone countries continues to be a structural driver of property and catastrophe insurance demand. The country experiences an average of 20 typhoons annually, and the 2024 season was particularly severe, featuring six consecutive storms including three super typhoons within a single month. These events reinforce awareness of insurance as a financial necessity rather than a discretionary product. Property insurance accounted for 42% of general insurance premiums in 2024. The Philippine government's receipt of a USD 600 million World Bank facility in 2023 for catastrophe insurance further validates the sector's growth opportunity and underpins Philippines non-life insurance market growth over the forecast period.

Banks and digital platforms are rapidly becoming the dominant channel for non-life insurance distribution in the Philippines, displacing traditional agent-only models and dramatically expanding the reach of insurers into previously underserved customer segments. Partnerships such as BPI-AIA's InstaProtect and the TravelSmart Marketplace by Surely.Digital and PhilInsure illustrate how digital platforms can simplify the purchase and management of insurance policies. The Insurance Commission's digital agenda, combined with the fact that 82% of Filipinos now use finance apps for cashless transactions, creates fertile ground for sustained bancassurance and insurtech-led growth through the forecast period.

Microinsurance is one of the fastest-growing segments in the Philippines non-life insurance market, targeting the country's large low-income population that has historically been excluded from mainstream insurance products. Microinsurance premiums reached USD 240 million in 2023, reflecting an 84.1% year-on-year growth in Q2 2023 according to the Philippines Insurance Commission. The introduction of takaful products for Muslim Filipinos, subsidized parametric insurance for farmers, and community-based insurance schemes are all components of a broadening financial inclusion agenda. Government support through the IC's financial literacy programs and regulatory facilitation of microinsurance vehicles is expected to sustain this growth trajectory.

Parametric insurance, which triggers automatic payouts based on predefined physical parameters such as wind speed or rainfall rather than assessed losses, is gaining significant momentum in the Philippines as a faster and more efficient alternative to traditional claims-based products for natural disaster coverage. Unlike conventional policies that require lengthy loss assessment processes, parametric products provide near-immediate liquidity to government agencies, municipalities, and agribusinesses following typhoon or flood events. Leading international and domestic insurers are actively developing parametric offerings for the Philippine market, supported by satellite data, weather monitoring infrastructure, and collaboration with the Philippine government's disaster risk financing programs.

The report of the Expert Market Research Reports title"Philippines Non-Life Insurance Market Report and Forecast 2026 to 2035" offers a detailed analysis of the market based on the following segments:

Market Breakup by Insurance Type

Key Insight: Property insurance is the dominant insurance type in the Philippines, accounting for approximately 42% of general insurance premiums in 2024, underpinned by the country's extreme vulnerability to typhoons, earthquakes, and floods. Residential, commercial, and industrial property owners are increasingly incorporating catastrophe coverage as a mandatory risk management component, particularly following large-scale climate events. Motor insurance is the second-largest segment at approximately 23.5% of GWP, supported by rising vehicle ownership, regulatory compulsory third-party liability requirements, and vehicle financing mandates that require comprehensive coverage. Travel insurance is growing rapidly, driven by a post-pandemic rebound in international and domestic tourism and the needs of the country's large overseas Filipino worker population.

Market Breakup by Service Provider

Key Insight: Private insurance providers dominate the Philippines non-life insurance market, commanding the majority of premium income and offering the widest range of products across motor, property, travel, liability, and personal accident lines. Private insurers compete primarily on product breadth, digital accessibility, claims service efficiency, and bancassurance network partnerships. Public insurance providers, such as the Government Service Insurance System and Social Security System, serve specific government employee and social protection mandates but occupy a smaller and more specialized share of the overall non-life insurance market. The private sector's advantage in product innovation and distribution reach is expected to widen its lead over the forecast period.

Market Breakup by End User

Key Insight: Individual end users are the primary driver of motor insurance, travel insurance, and household property coverage, representing the largest customer base by policy count. Rising middle-class incomes, growing financial literacy, and digital accessibility are expanding individual insurance uptake across urban and suburban areas. Corporate clients are the dominant end user for commercial property, liability, engineering, marine, and specialty lines, accounting for a disproportionately high share of premium value relative to policy count. Large infrastructure projects under the Build Build Build program and related government-private partnerships have also expanded demand for commercial property and contractor's all-risk insurance among corporate buyers.

Market Breakup by Distribution Channel

Key Insights: Agents and brokers remain the most significant distribution channel in the Philippines non-life insurance market by reach, particularly in rural areas and among less tech-savvy populations, where personal relationships and community trust play a decisive role in insurance purchasing decisions. Banks, through bancassurance partnerships, are the fastest-growing distribution channel, leveraging existing customer relationships, branch networks, and digital platforms to cross-sell insurance alongside loans, mortgages, and savings products. Direct sales via digital channels are expanding as mobile and online platforms lower acquisition costs and enable faster policy issuance, particularly for travel, personal accident, and motor insurance.

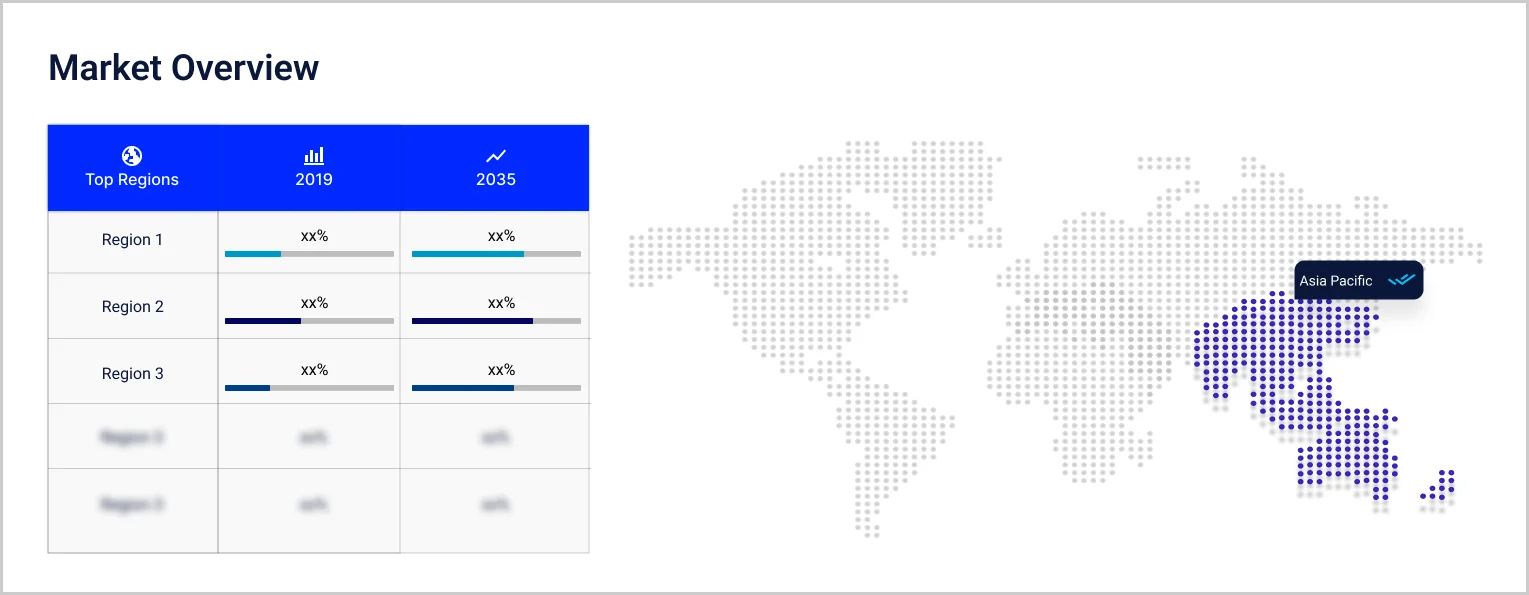

Market Breakup by Region

Key Insight: Asia-Pacific is the most significant regional context for the Philippines non-life insurance market, with the Philippines holding approximately 0.5% of the region's total non-life insurance market in 2024. Within Asia-Pacific, markets such as China, Japan, and South Korea dominate by premium volume, but Southeast Asia including the Philippines is among the fastest-growing sub-regions given lower penetration rates and stronger economic growth trajectories. Within the Philippines, Metro Manila and urban Luzon concentrate the majority of commercial and individual non-life insurance premium generation, followed by Visayas and Mindanao where microinsurance penetration and natural disaster coverage are particularly relevant.

|

CAGR 2026-2035 - Market by |

Insurance Type |

| Travel Insurance |

8.3% |

| Property Insurance |

7.8% |

| Motor Insurance |

XX% |

| Liability Insurance |

8.5% |

| Others |

XX% |

By Insurance Type

Property insurance commands the largest share of the Philippines non-life insurance market, accounting for approximately 42% of general insurance premiums in 2024. This dominance is directly linked to the Philippines' geographic location within the Pacific typhoon belt, where annual storm events, flooding, and seismic activity make property risk coverage essential for both residential and commercial property owners. Growing urbanization, infrastructure investment, and rising property values are expanding the insurable asset base. Motor insurance, as the second-largest segment at approximately 23.5% of GWP, benefits from steady growth in vehicle registrations and compulsory third-party liability requirements, ensuring a stable and growing premium base.

By Service Provider

Private insurance providers dominate the Philippines non-life insurance landscape, holding the majority of gross written premium income and offering the broadest range of products from motor and property to specialty and commercial lines. Malayan Insurance, consistently ranked as the largest non-life insurer by assets, exemplifies the competitive strength of domestic private insurers with deep market knowledge and extensive distribution networks. Global players such as Chubb and AIA complement local insurers with international underwriting expertise, multinational client coverage, and digital innovation capabilities. The public insurance sector, while important for social protection mandates, plays a secondary role in the commercial non-life space.

By Distribution Channel

Agents and brokers are the dominant distribution channel in the Philippines by reach, particularly important in rural provinces where personal relationships underpin insurance purchasing decisions. However, bancassurance is the fastest-growing channel, with major partnerships between banks and insurers reshaping how Filipinos access non-life coverage. The collaboration between BPI and AIA Philippines through InstaProtect is indicative of the broader trend of banks using their digital platforms to distribute insurance products at scale with minimal incremental cost. Digital direct sales platforms are gaining traction, particularly for travel and motor insurance, as smartphone penetration increases and consumers seek faster, more convenient policy issuance.

The Philippines non-life insurance market is characterized by a mix of dominant domestic insurers and established international players, with the top companies competing primarily on product range, distribution reach, digital capabilities, and claims processing efficiency. The market is concentrated, with leading players holding disproportionate shares of gross written premium, while a long tail of smaller domestic and regional insurers serve specialized or community-focused niches.

Competition is intensifying around digital transformation, with major insurers investing in mobile apps, AI-powered underwriting, and integrated bancassurance platforms to acquire and retain customers. Regulatory support from the Insurance Commission, which is pushing for digital adoption and financial inclusion, is accelerating the shift toward technology-enabled distribution. Climate risk is also reshaping competitive priorities, with insurers differentiating on catastrophe underwriting expertise, reinsurance relationships, and parametric product offerings.

Malayan Insurance Co., Inc. is the Philippines' largest non-life insurance company by assets, offering a comprehensive range of products including motor, fire, marine, engineering, liability, personal accident, and specialized policies such as boiler insurance and fidelity guarantee. Headquartered in Manila, Malayan has been a market leader for decades, known for its extensive agent and broker network and its ability to respond rapidly to catastrophic claims events. In 2026, the company expanded payment flexibility with zero-interest installment options, reflecting its focus on market accessibility and premium affordability.

Originally established as ACE Limited in 1985 and rebranded to Chubb following a 2016 merger, Chubb is headquartered in Zurich, Switzerland, and is one of the world's largest publicly traded property and casualty insurance companies. In the Philippines, Chubb provides property and casualty, accident and health, personal insurance, and commercial insurance products to corporate and individual clients. Its global underwriting expertise, financial strength, and international risk management capabilities make it a preferred partner for multinational corporations and large domestic enterprises operating in the Philippines.

Founded in 1919 and headquartered in Hong Kong, AIA Group is the largest independent publicly listed pan-Asian life and general insurance group, operating in 18 markets. In the Philippines, AIA (formerly Philam Life) offers life insurance, accident and health coverage, savings plans, pension products, and employee benefits through direct and bancassurance channels. AIA Philippines had total assets of PHP 257.76 billion and served nearly 1.2 million individual policyholders as of December 2024. Its partnership with BPI for InstaProtect in 2025 represents a key strategic move to expand digital insurance access across the Filipino market.

AIG Philippines is the local subsidiary of American International Group, one of the world's leading insurance organizations. The company offers a wide range of commercial and personal insurance products in the Philippines, including property, casualty, marine, liability, and specialty lines. AIG's strength lies in its global risk management expertise, international corporate client relationships, and its ability to provide large-line capacity for complex commercial risks that smaller domestic insurers may not be able to underwrite independently. Its presence in the Philippines supports both multinational operations and growing domestic corporate insurance needs.

Other key players in the market are Alliedbankers Insurance Corporation, Alpha Insurance and Surety Company Inc, Bethel General Insurance and Surety Corporation, Paramount Life and General Insurance Corporation, Metropolitan Bank and Trust Company, Fortune General Insurance Corporation, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

The Philippines non-life insurance sector is at an inflection point, shaped by climate resilience needs, digital distribution innovation, and a large underinsured population presenting compelling growth opportunities. Our comprehensive Philippines Non-Life Insurance Market Report for 2026 covers every critical dimension from property catastrophe trends and bancassurance dynamics to microinsurance expansion and insurtech adoption. Whether you are an insurer evaluating market entry, a reinsurer assessing risk concentration, or an investor identifying growth-stage opportunities, this report gives you the analytical depth and market intelligence to move with confidence. Download your free sample today.

Upto 15% Off

USD

$3999 $3599

$2499 $2249

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

Get in touch with us for a customized solution tailored to your unique requirements and save upto 35%!

At 2025, the market reached an approximate value of USD 2.26 Billion.

The market is projected to grow at a CAGR of 7.30% between 2026 and 2035.

The market is projected to grow significantly during the forecast period 2026 to 2035 to reach USD 4.57 Billion by 2035.

The Philippines Non-Life Insurance Market is driven by the country's extreme natural disaster exposure, with an average of 20 typhoons annually creating structural demand for property and catastrophe coverage. Rising vehicle ownership and regulatory compulsory insurance requirements sustain motor insurance growth. Growing middle-class incomes and urbanization are expanding the insurable population, while digital platforms and bancassurance partnerships are dramatically increasing insurance accessibility. Government financial inclusion initiatives, microinsurance expansion, and the introduction of novel products such as takaful and parametric insurance are reaching previously uninsured communities. International investor confidence, exemplified by IFC's 2024 investment in MAA General Assurance, further signals the market's long-term growth credibility.

By insurance type, the market is divided into Property Insurance, Liability Insurance, Motor Insurance, Travel Insurance, and Others. Property insurance is the dominant segment at approximately 42% of general insurance premiums in 2024, underpinned by the Philippines' high vulnerability to natural disasters. Motor insurance is the second-largest segment at approximately 23.5% of GWP, driven by rising vehicle registrations and compulsory liability requirements. Travel insurance is among the fastest-growing categories, supported by the rebound in both domestic and international tourism and the large overseas Filipino worker community.

The key trends include the intensification of property and catastrophe insurance demand driven by climate risk and rising typhoon frequency, the rapid expansion of digital distribution channels and bancassurance partnerships, microinsurance growth and financial inclusion initiatives targeting low-income Filipinos, and the emergence of parametric insurance products that offer faster payouts for natural disaster events. The introduction of takaful products in 2025 has also opened a new customer segment among Muslim Filipinos.

The key players in the market include Malayan Insurance Co. Inc., Chubb Company, AIA Group Limited, AIG Philippines Inc., Alliedbankers Insurance Corporation, Alpha Insurance and Surety Company Inc, Bethel General Insurance and Surety Corporation, Paramount Life and General Insurance Corporation, Metropolitan Bank and Trust Company, Fortune General Insurance Corporation and others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Insurance Type |

|

| Breakup by Service Provider |

|

| Breakup by End User |

|

| Breakup by Distribution Channel |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.

Share