Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

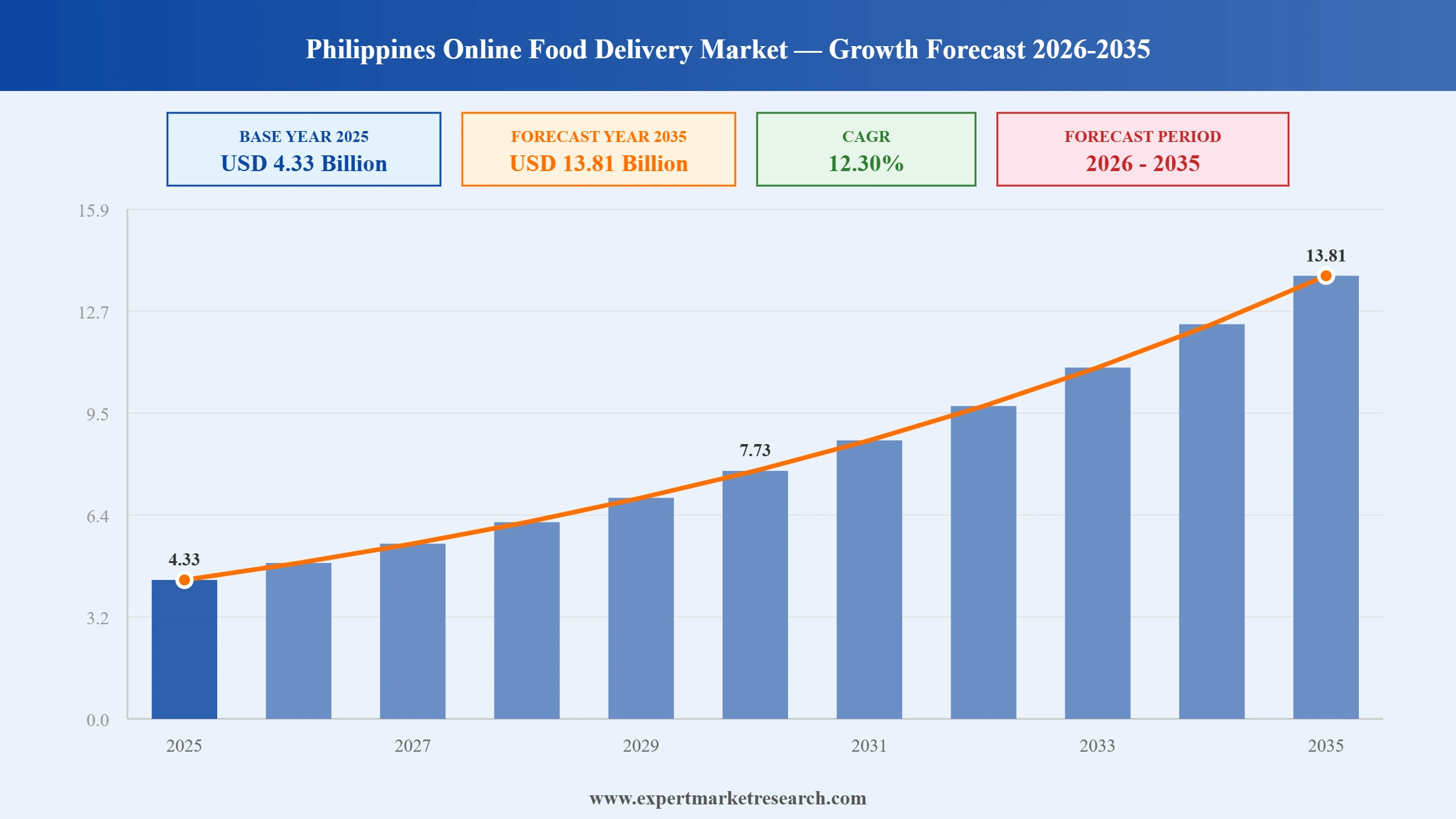

The Philippines Online Food Delivery Market reached a value of USD 4.33 Billion at 2025 and is projected to expand at a CAGR of around 12.30% during the forecast period of 2026-2035. With rising smartphone penetration, rapid cloud kitchen adoption, expanding digital payment infrastructure, and increasing urbanisation across Metro Manila and secondary cities, the market is expected to reach USD 13.81 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

|

Philippines Online Food Delivery Market Report Summary |

Description |

Value |

|

Base Year |

USD Billion |

2025 |

|

Historical Period |

USD Billion |

2019-2025 |

|

Forecast Period |

USD Billion |

2026-2035 |

|

Market Size 2025 |

USD Billion |

4.33 |

|

Market Size 2035 |

USD Billion |

13.81 |

|

CAGR 2019-2025 |

Percentage |

XX% |

|

CAGR 2026-2035 |

Percentage |

12.30% |

|

CAGR 2026-2035- Market by Region |

Visayas |

13.4% |

|

CAGR 2026-2035 - Market by Business Model |

Logistics-Based |

13.8% |

|

CAGR 2026-2035 - Market by Payment Method |

Online |

13.5% |

The Philippines Online Food Delivery Market is being shaped by the convergence of digital payment infrastructure, cloud kitchen proliferation, embedded financial services for merchants, and government-backed connectivity programs that are collectively extending delivery platform reach well beyond Metro Manila.

The Department of Information and Communications Technology (DICT) continued executing digital economy infrastructure upgrades in January 2025, with a focus on broadband connectivity improvements that directly benefit online platform services including food delivery apps. These efforts sit within the government's broader E-Commerce Philippines 2022 Roadmap and Digital Cities program, which are designed to close the connectivity gap between Metro Manila and provincial regions. Improved infrastructure in Visayas and Mindanao is directly correlated with higher delivery app registrations, greater restaurant sign-ups on aggregator platforms, and stronger order frequency in cities like Cebu, Davao, and Iloilo, all of which contribute to sustained long-term market expansion.

Grab Philippines partnered with Red Planet Hotels in December 2024 to introduce GrabFood Lockers, a contactless self-service food delivery solution for hotel guests. Customers receive a unique QR code via the Grab app to unlock a designated locker and retrieve their order, resolving persistent concerns around lost or misappropriated deliveries in hospitality settings. The rollout represents a meaningful step in integrating food delivery operations with the hospitality sector, and it opens a pathway for replicating locker-based models in office towers, residential complexes, and university campuses, potentially serving underserved delivery points in densely populated urban zones.

Foodpanda Philippines entered a multi-brand collaboration with Mobile Legends: Bang Bang, MobaPay, and Antom in October 2024, granting GCash users exclusive delivery discounts and in-game vouchers through the A+ Rewards program. Customers could claim up to 56% off on in-game items and up to PHP 100 off Foodpanda orders throughout the promotional period. The partnership taps into the Philippines' highly active mobile gaming community, using gaming as a consumer acquisition channel for food delivery. By connecting two of the country's most popular digital activities - gaming and online food ordering - the campaign drove measurable increases in app installs and new user activation.

Foodpanda Philippines introduced its curated "Meal for One" option in August 2024, consolidating individual meal choices from multiple partner restaurants into one dedicated section of the app. The service caps delivery charges at PHP 15 per order, directly targeting the large population of urban single professionals and students who rely on delivery apps for daily meals. By reducing the minimum spend and delivery cost barrier for solo diners, Foodpanda widened its addressable user base and strengthened its competitive position against GrabFood in the value-conscious segment. The initiative also provided partner cloud kitchens with a new demand channel.

Foodpanda Philippines launched the "Negosyo Like a Panda" merchant financing program in July 2024, partnering with Jia Financing Inc. to give partner restaurants direct access to business loans. The initiative is tailored for micro and small food businesses operating within the Foodpanda ecosystem, enabling them to build inventory buffers and scale their kitchen operations to meet growing delivery order volumes. By embedding financial services into its platform offering, Foodpanda deepens merchant loyalty, expands the breadth of restaurant options available to consumers, and positions itself as more than just a logistics intermediary for small food entrepreneurs.

Cloud kitchens have emerged as a defining structural shift in the Philippines online food delivery market growth, offering food entrepreneurs and established restaurant brands a cost-efficient route to market without the burden of dine-in real estate. Urban land costs and sustained post-pandemic delivery demand have accelerated adoption of this model, with over 450 delivery-only establishments now operating in Metro Manila. The lower barrier to entry also enables MSME food operators to scale rapidly, expanding restaurant variety on aggregator platforms. In August 2024, Foodpanda Philippines launched its curated "Meal for One" concept, which directly leverages cloud kitchen partners to deliver affordable single-serve meal options, reinforcing the symbiotic relationship between delivery platforms and the cloud kitchen ecosystem.

The integration of digital wallets such as GCash and PayMaya into food delivery platforms has fundamentally changed the payment landscape for Filipino consumers. Platforms now design entire promotional mechanics around cashless transactions, rewarding users with exclusive discounts, cashback, and loyalty points when they pay digitally. This shift not only reduces order abandonment at checkout but builds long-term spending habits anchored to specific platforms and wallet providers. In December 2024, Grab Philippines introduced GrabFood Lockers at Red Planet Hotels, combining contactless QR-code payment with self-serve collection in a single experience, illustrating how payment technology and delivery logistics are increasingly converging into seamless consumer journeys.

A fast-growing trend in the Philippines food delivery sector is the embedding of financial services directly into delivery platform ecosystems, transforming aggregators from mere order conduits into business enablement partners for restaurant operators. Working capital loans, micro-insurance, and inventory financing are increasingly being offered by platforms to partner merchants, helping small food businesses survive demand volatility and scale during high-growth periods. This creates stickier platform relationships and a more resilient restaurant supply base. In July 2024, Foodpanda Philippines launched the "Negosyo Like a Panda" program with Jia Financing Inc., offering partner restaurants direct access to business loans that enable them to carry more inventory and fulfill growing order volumes without capital strain.

Beyond private sector investment, government-led digital infrastructure development is proving to be a critical driver of online food delivery market expansion in the Philippines. The Department of Information and Communications Technology's active rollout of broadband upgrades under the E-Commerce Philippines 2022 Roadmap and Digital Cities initiative is systematically reducing connectivity barriers in Visayas and Mindanao. Better mobile data coverage directly translates into higher delivery app adoption in regional cities, greater restaurant participation on aggregator platforms, and broader consumer access to convenience dining options. In January 2025, the DICT continued implementing these infrastructure programs, with market observers noting a correlation between improved regional connectivity and measurable upticks in delivery app engagement metrics outside Metro Manila.

The Expert Market Research's report titled "Philippines Online Food Delivery Market Report and Forecast 2026 to 2035" offers a detailed analysis of the market based on the following segments:

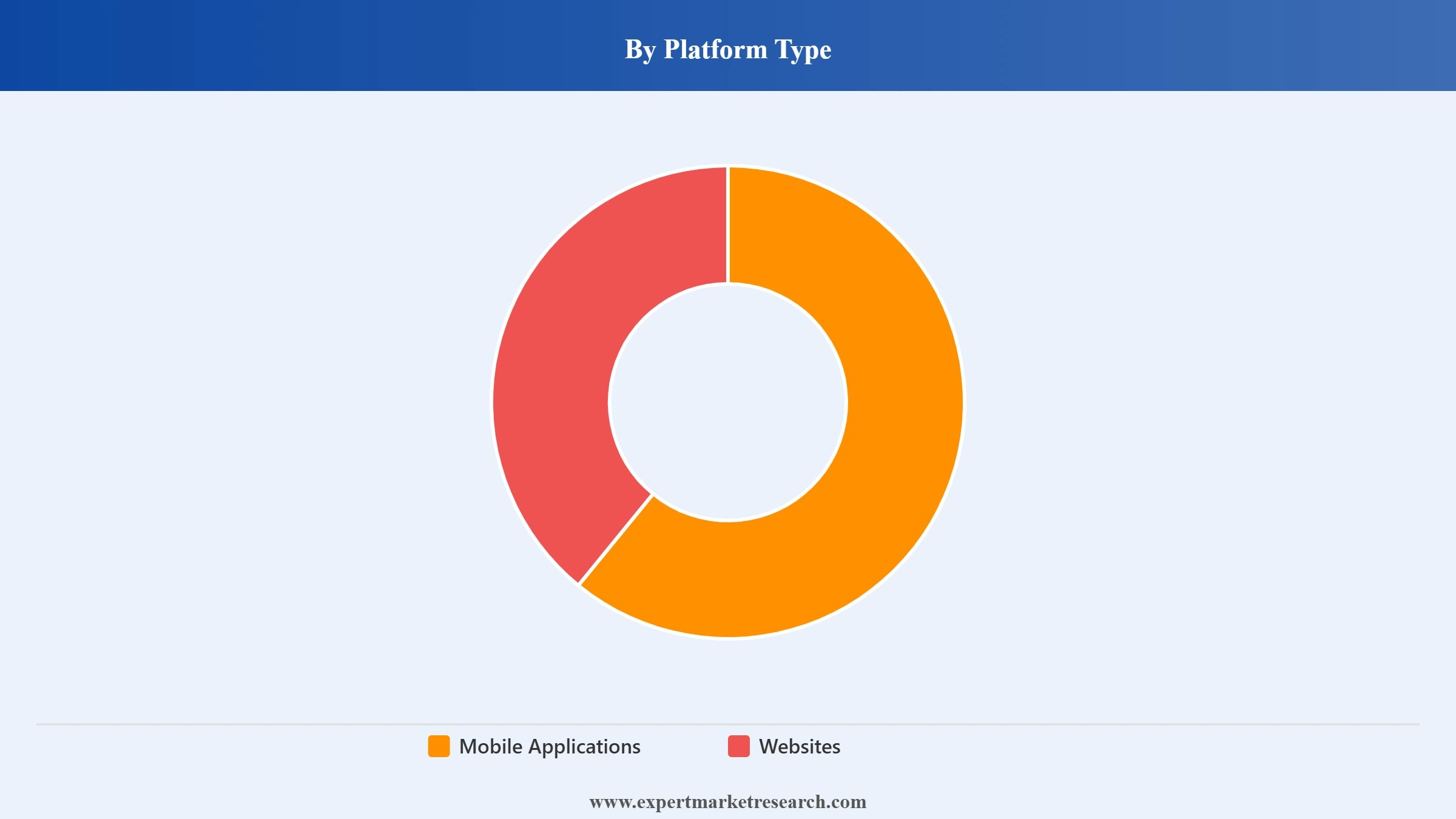

Market Breakup by Platform Type

Key Insight: Mobile applications hold an overwhelming share of the Philippines online food delivery market by platform type, underpinned by the country's smartphone penetration rate exceeding 75% and the continuous improvement of app user experiences by leading operators. GrabFood and Foodpanda have invested substantially in app-based personalization, real-time tracking, and integrated digital payment flows that retain users within their respective ecosystems. The website segment caters to a smaller but consistent base of desktop users, typically professionals ordering from the workplace. As smartphone prices continue to fall and regional internet access improves under DICT programs, the mobile segment is expected to continue capturing a disproportionate share of new user additions through the forecast period.

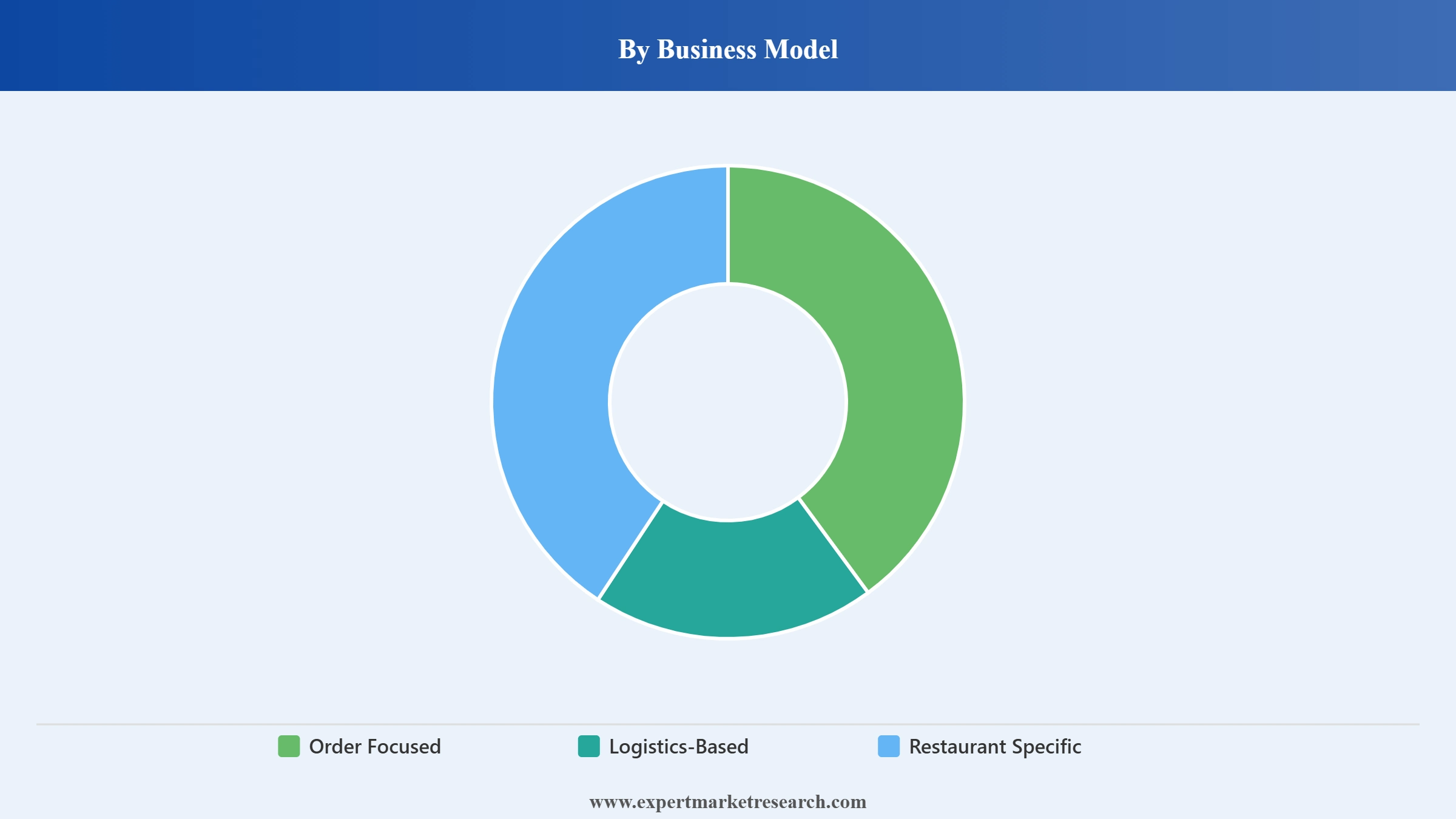

Market Breakup by Business Model

Key Insight: The logistics-based business model commands the largest revenue contribution in the Philippines online food delivery market, reflecting the dependence of restaurants, particularly SMEs and cloud kitchen operators, on platform-owned rider networks for last-mile delivery. GrabFood and Foodpanda both operate extensive logistics infrastructure that allows partner restaurants to outsource delivery without maintaining their own fleets. This model is expected to grow at a CAGR of 10.8% through the forecast period. The restaurant-specific model maintains a strong secondary position, principally driven by Jollibee Foods Corporation, whose proprietary delivery app and in-house logistics handle millions of orders annually. The order-focused model serves niche aggregation functions for premium and independent restaurant categories.

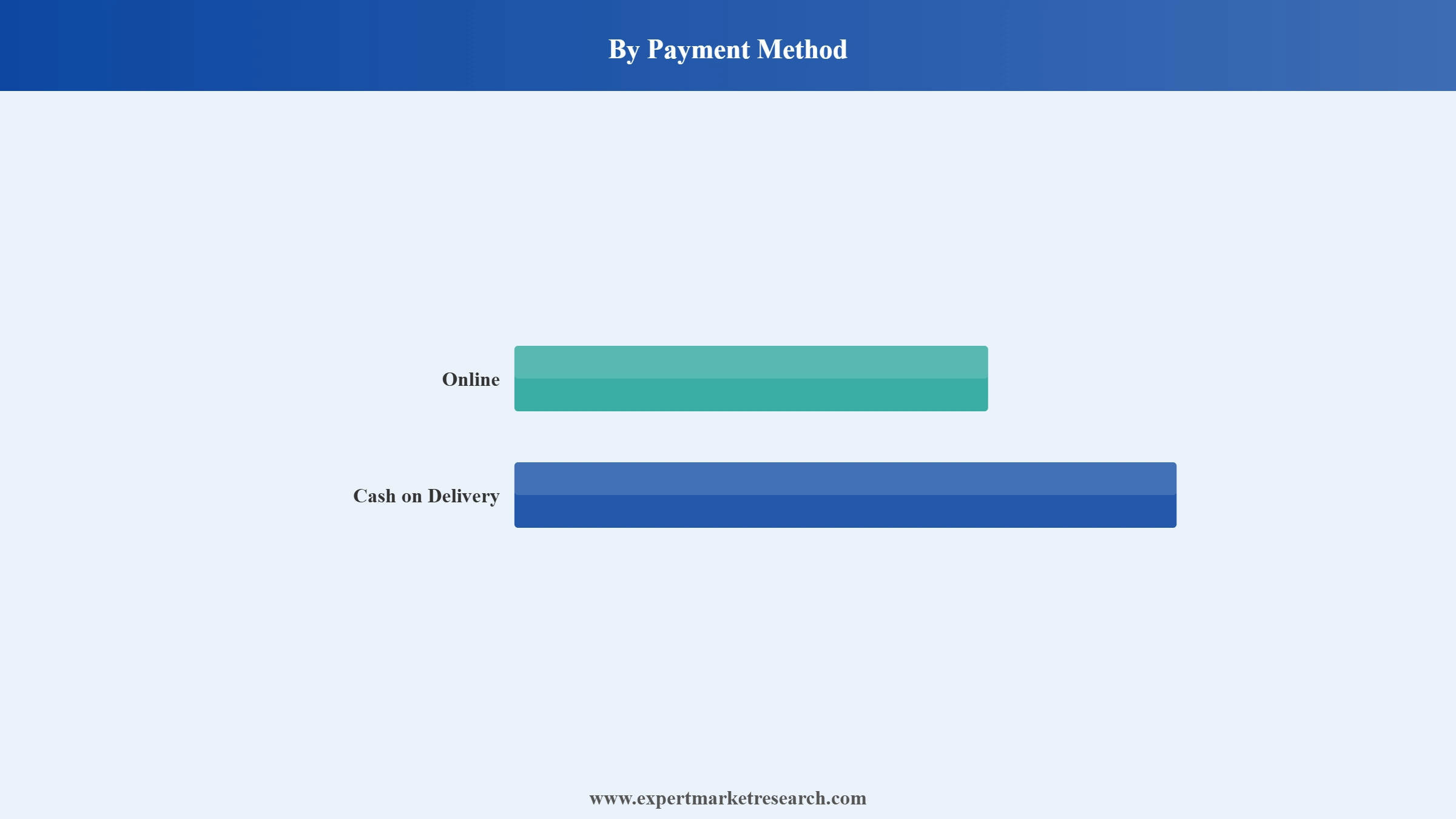

Market Breakup by Payment Method

Key Insight: Online payment methods are gaining ground rapidly across the Philippines as GCash surpassed 94 million registered users by 2024, and platforms actively reward digital transactions with exclusive promotions and loyalty benefits. The Bangko Sentral ng Pilipinas digital payments roadmap has accelerated the normalization of cashless transactions across income brackets. Cash on delivery, however, retains meaningful penetration in provincial markets and among lower-income consumer segments where trust in digital transactions is still building. This dual-payment model is a strategic asset for aggregators, broadening their total addressable market by ensuring they can serve both digitally-enabled urban consumers and cash-reliant regional users simultaneously.

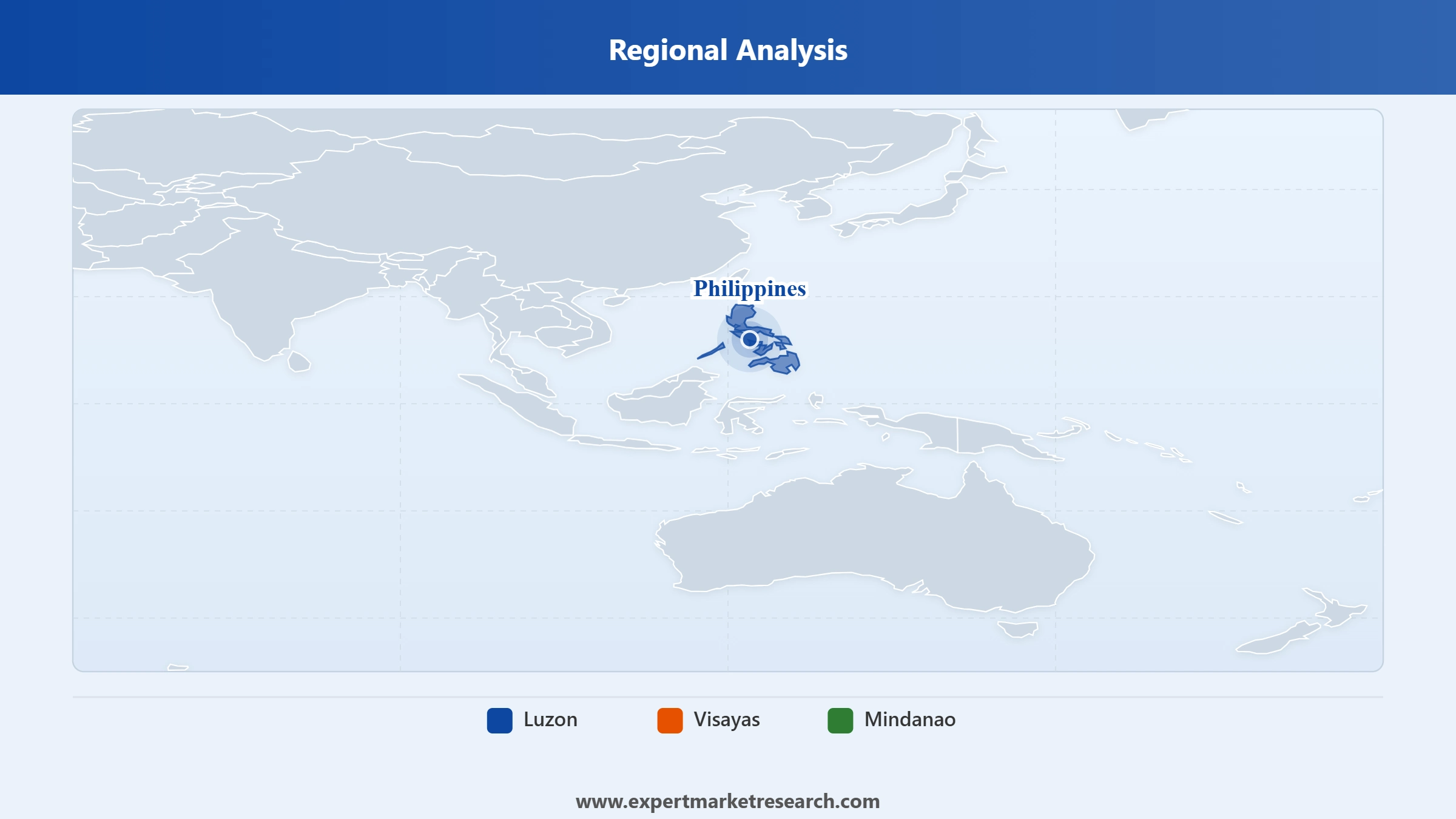

Market Breakup by Region

Key Insight: Luzon accounts for the largest share of total online food delivery revenue in the Philippines, with Metro Manila functioning as the commercial epicentre of platform activity, restaurant partnerships, and rider network density. Cebu City in the Visayas has emerged as the second-most strategically valuable market for food delivery operators, supported by a growing middle class, an active BPO workforce, and rising tourism traffic. Mindanao, led by Davao City, is transitioning from a nascent to a growth-stage market as DICT broadband programs close the connectivity gap between the southern island group and the national digital economy. Platforms including GrabFood and Foodpanda are increasingly directing regional expansion resources toward Visayas and Mindanao as Luzon market saturation grows.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Mobile applications dominate the Philippines online food delivery market within the platform type segmentation, reflecting a mobile-first digital culture that has made smartphones the primary interface for online commerce across the country. With over 60 million food delivery app installs nationwide and user penetration in the meal delivery segment reaching approximately 18.7% by 2025, the scale of mobile-based engagement is clear. GrabFood and Foodpanda have each invested in loyalty mechanics, push notification strategies, and AI-driven recommendation engines that deepen user retention within their respective apps. The website segment, while stable, holds a modest share and is primarily relevant for corporate or bulk ordering use cases where desktop interfaces offer practical advantages.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

In the business model segmentation, logistics-based platforms hold the dominant market share, as the majority of Philippine restaurant operators rely on GrabFood and Foodpanda for order management and rider dispatch. GrabFood's first-place market position with approximately 51% market share by early 2024 reflects the strength of its integrated logistics and super-app ecosystem. The restaurant-specific model is the second-most significant, driven almost entirely by Jollibee Foods Corporation and its proprietary delivery app.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Within the payment method dimension, online payments are displacing cash on delivery progressively in urban markets, with platforms incentivizing the shift through reward programs tied to GCash, PayMaya, and credit card transactions.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Luzon is the undisputed commercial centre of the Philippines online food delivery market, driven by the scale and density of Metro Manila's urban population and its concentration of food delivery-ready consumers. The region hosts the headquarters and primary logistics hubs of both GrabFood and Foodpanda Philippines, and it accounts for the highest volume of daily food delivery orders in the country. Over 450 cloud kitchen establishments operate in Metro Manila, generating a diverse and expanding supply of delivery-exclusive food options. Investment in digital payment infrastructure has been most intensive in Luzon, where GCash penetration among food delivery users is the highest nationally. Key cities including Pasig, Makati, Quezon City, and Manila proper each sustain dense rider networks that enable consistently short delivery windows, reinforcing the region's position as the benchmark for delivery service quality across the Philippines.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The Visayas region, centred on Cebu City, has developed into the second-most strategically important zone for online food delivery expansion. Cebu's growing business process outsourcing sector and rising middle-class population have created a young, digitally connected consumer base with strong app adoption rates. Both GrabFood and Foodpanda have invested in widening their restaurant partner networks in Cebu, and local cloud kitchen operators are establishing a foothold to serve demand in smaller Visayan cities. Mindanao, particularly Davao City, represents a compelling frontier market where DICT broadband investments under the Digital Cities program are improving mobile data quality at a pace that directly drives delivery platform registrations. The interplay between public-sector infrastructure spending and private-sector platform expansion in both regions is creating sustained structural momentum for market growth well beyond the forecast period.

The Philippines online food delivery market is structured around a two-player dominance at the aggregator level, with Delivery Hero Philippines operating Foodpanda and GrabExpress running GrabFood collectively accounting for the vast majority of platform-based orders. GrabFood overtook Foodpanda to capture approximately 51% of market share by March 2024, while Foodpanda holds the remainder of the aggregator segment with a particularly strong presence in provincial and tier-2 markets. The competition between the two is defined by aggressive promotion cycles, subscription service innovation, and ongoing investment in delivery logistics and merchant services.

Below the dominant duopoly, the market includes restaurant-owned delivery operations led by Jollibee Foods Corporation, which processes millions of orders annually through its proprietary app. Niche players including LAHAT Food and Habit Food Group serve specific regional or culinary segments that are underserved by dominant platforms. The competitive environment rewards scale in logistics and technology while creating adjacent opportunities for community-focused platforms targeting tier-2 and tier-3 cities.

Delivery Hero Philippines, Inc. operates the Foodpanda brand locally, having entered the Philippine market in 2014 as part of Delivery Hero's global network. The company is headquartered in Taguig and provides meal delivery, grocery delivery, and in-restaurant dining services across the country, with coverage extending to provincial areas beyond major cities. Foodpanda differentiates through its PandaPro subscription plan, frequent flash deals, and embedded merchant services including financing partnerships with Jia Financing Inc. Its integration of AI-powered QR menu tools through TabSquare positions the platform at the frontier of food tech innovation in the region.

GrabExpress, Inc. is the delivery arm of Grab's Southeast Asian super-app ecosystem, providing on-demand food delivery through GrabFood across the Philippines since 2018. Grab holds approximately 51% domestic food delivery market share and benefits from deep integration across ride-hailing, grocery, and digital payment services within a single app. The GrabUnlimited subscription plan fosters cross-service loyalty, while GrabPay enables seamless cashless transactions. GrabFood's geographic coverage spans Metro Manila, Cebu, Davao, Iloilo, and several additional cities, with ongoing expansion into regional markets supported by continued investment in rider network density.

Founded in 1978 and headquartered in Pasig City, Jollibee Foods Corporation is the Philippines' leading quick-service restaurant brand and a major independent force in the online food delivery landscape. The company operates its own delivery app with in-house logistics, app-exclusive promotions, and an integrated loyalty program that encourages direct consumer relationships outside third-party aggregator platforms. Jollibee's nationwide footprint across more than 1,600 outlets provides a last-mile advantage that no pure-play aggregator can replicate in breadth or brand familiarity. The company also maintains a presence on GrabFood and Foodpanda to capture aggregator-sourced demand.

LAHAT Food is a Philippines-based food delivery platform built around a community-driven, hyperlocal delivery model aimed at tier-2 and tier-3 cities that the dominant aggregators have not yet deeply penetrated. The platform prioritizes neighborhood restaurants, local carinderias, and independent food operators, enabling smaller communities to participate in the delivery economy on their own terms. LAHAT Food's approach aligns with the government's inclusive digital commerce agenda and taps into markets where consumer preference for locally familiar food options outweighs brand loyalty to global platforms. The company represents a growing category of regionally focused challengers building sustainable delivery businesses outside Metro Manila.

Other key players in the market are Habit Food Group, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Uncover the full opportunity landscape within the Philippines Online Food Delivery sector with our comprehensive 2026 market report. Keep pace with platform innovations, regional delivery expansion trends, and shifts in consumer payment behaviour that are reshaping how millions of Filipinos order food daily. Whether you are a food tech investor assessing entry points, a restaurant brand building its digital delivery strategy, or a platform operator targeting regional growth, this report gives you the clarity and data to move decisively. Download your free sample today and discover the key growth drivers within the thriving Philippine online food delivery space.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the Philippines online food delivery market reached an approximate value of USD 4.33 Billion.

The market is projected to grow at a CAGR of 12.30% between 2026 and 2035.

The key players in the market includes Delivery Hero Philippines, Inc., GrabExpress, Inc., LAHAT Food, Jollibee Foods Corporation, Habit Food Group, among others.

The strategies that stand out the most are the use of mobile applications, cloud kitchens, subscription services, eco-friendly packaging, and assistance from authorities which provide additional convenience, loyalty, and scope to the online food delivery services in the Philippines.

The market is projected to grow significantly during the forecast period 2026 to 2035 to reach USD 13.81 Billion by 2035..

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Platform Type |

|

| Breakup by Business Model |

|

| Breakup by Payment Method |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.