Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

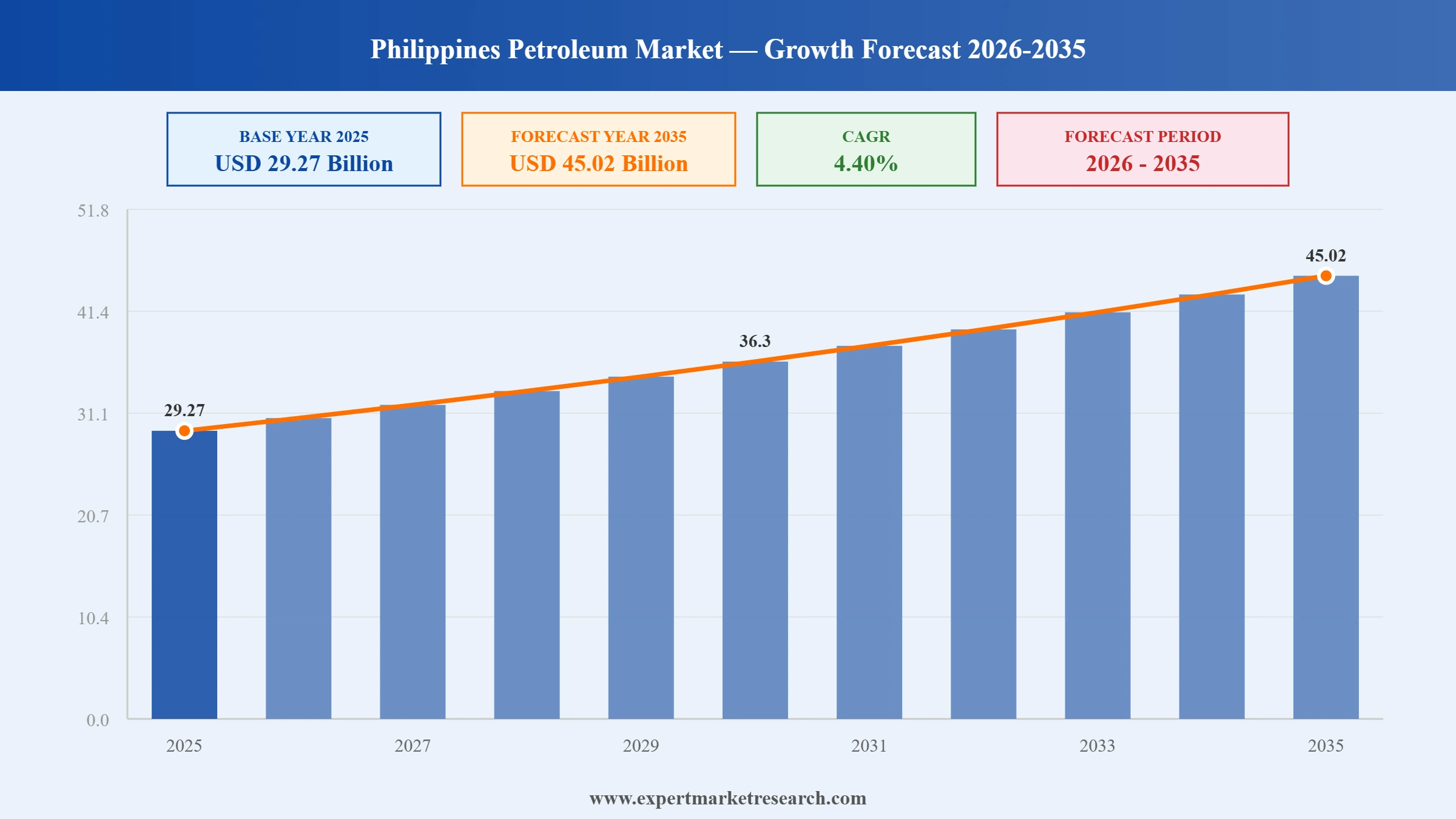

The Philippines Petroleum Market reached a value of USD 29.27 Billion at 2025 and is projected to expand at a CAGR of around 4.40% during the forecast period of 2026-2035. With rising transportation fuel demand, growing industrial and power generation activity, strategic offshore exploration in the West Philippine Sea, and active government infrastructure investment stimulating petroleum product consumption, the market is expected to reach USD 45.02 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

|

Philippines Petroleum Market Report Summary |

Description |

Value |

|

Base Year |

USD Billion |

2025 |

|

Historical Period |

USD Billion |

2019-2025 |

|

Forecast Period |

USD Billion |

2026-2035 |

|

Market Size 2025 |

USD Billion |

29.27 |

|

Market Size 2035 |

USD Billion |

45.02 |

|

CAGR 2019-2025 |

Percentage |

XX% |

|

CAGR 2026-2035 |

Percentage |

4.40% |

|

CAGR 2026-2035 - Market by Type |

Light |

5.0% |

|

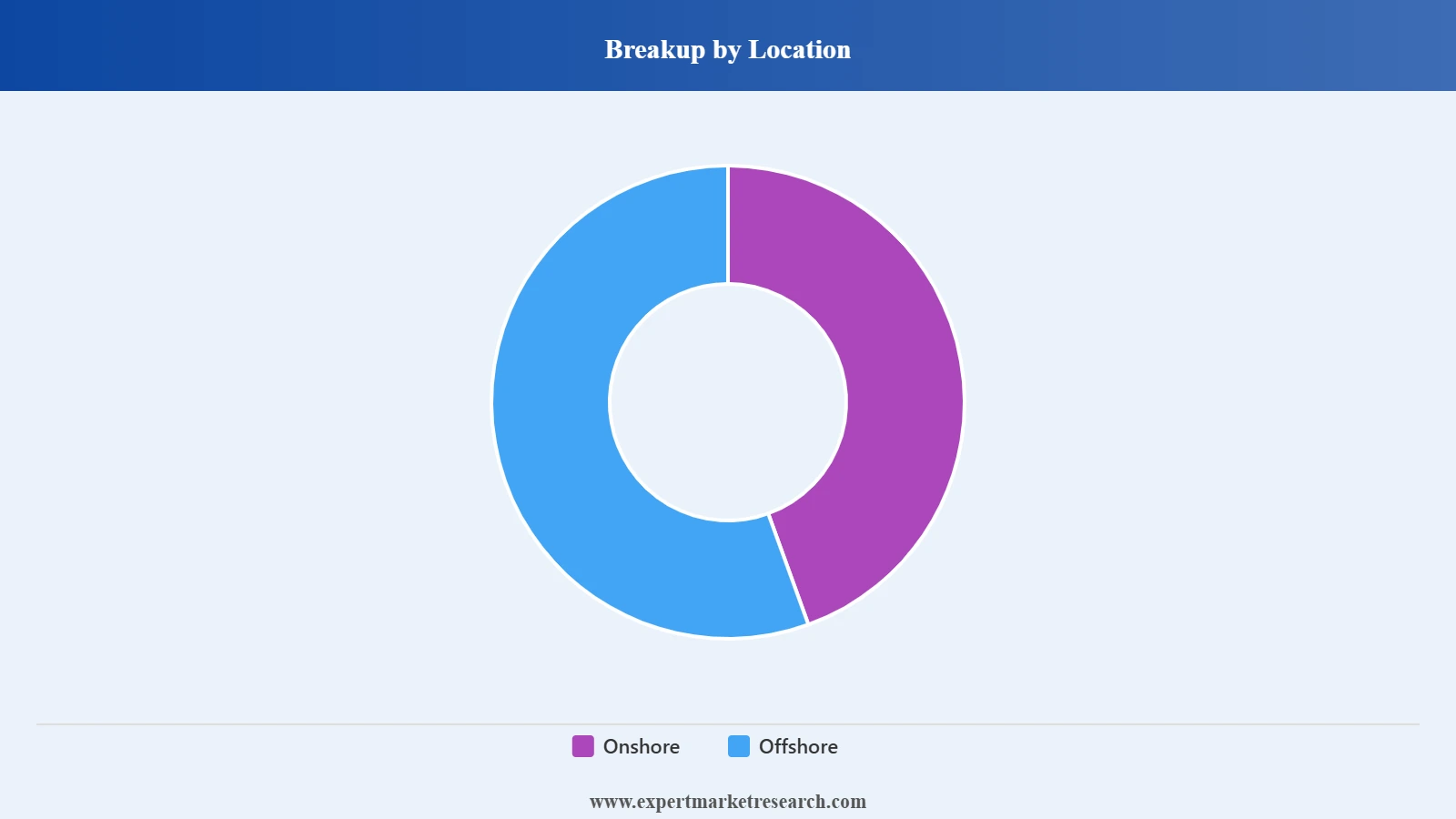

CAGR 2026-2035 - Market by Location |

Onshore |

4.9% |

The Philippines Petroleum Market is being shaped by structural demand growth from transportation and industry, strategic government efforts to develop domestic reserves and reduce import dependence, active expansion of fuel retail infrastructure into underserved provincial areas, and the entry of global petroleum majors into the domestic downstream market.

Industry data published in October 2025 confirmed a 10% year-on-year increase in domestic fuel consumption in the Philippines, driven by sustained transportation sector demand, expanded industrial operations, and the continued growth of logistics and delivery services linked to e-commerce and consumer goods distribution. The figure validated the market's structural demand trajectory and reinforced investment decisions by fuel retailers, terminal operators, and refinery upgrade planners. The transportation segment remained the dominant consumer, with diesel demand from commercial fleets and public utility vehicles serving as the primary growth driver, supplemented by rising gasoline demand from private vehicle owners in Metro Manila and major provincial cities.

Infrastructure developers and petroleum operators in the Philippines initiated significant upgrades to oil storage terminal facilities in June 2025, with projects aimed at increasing storage capacity and improving safety systems at key petroleum logistics hubs. The investments address the Philippines' vulnerability to supply disruptions stemming from limited onshore storage depth, which had historically constrained the country's ability to maintain strategic petroleum reserves during international price spikes or supply chain disruptions. Enhanced storage infrastructure also supports the government's goal of maintaining minimum strategic oil stock levels and improves the operational flexibility of fuel distributors serving remote island communities across the archipelago.

Several major fuel retail operators in the Philippines announced plans in June 2025 to expand their service station networks into provincial and growth corridor areas as vehicle ownership and road infrastructure development progressed beyond Metro Manila and major secondary cities. The expansion targets emerging economic zones in Mindanao, the Visayas inter-island highway network, and growth corridors in Luzon outside of the traditional Metro Manila footprint. Operators including Phoenix Petroleum and Seaoil have been at the forefront of this geographic expansion, competing to establish first-mover advantage in markets where fuel retail infrastructure remains underdeveloped relative to growing vehicle and commercial fleet demand.

PXP Energy Corporation, a Philippine petroleum company, announced in 2024 its intention to participate in a government-organised auction of energy reserve blocks in the western and southern Philippine maritime zones, including areas not subject to Chinese territorial claims. The company, which had previously encountered obstacles in the Reed Bank area due to geopolitical disputes in the South China Sea, was seeking new exploration blocks to rebuild its upstream portfolio. The Philippines government was simultaneously reviving its Service Contract award process after several years of inactivity, reflecting a renewed commitment to developing domestic petroleum reserves as part of the country's energy self-reliance strategy.

The Philippines petroleum market growth is attracting increasing attention from global energy corporations seeking to establish or expand their downstream market presence in Southeast Asia. Saudi Aramco's 2025 re-entry through a stake acquisition in Unioil Philippines is the most prominent recent example of this trend, but it reflects a broader pattern of international investment in the Philippine fuel retail and distribution sector. The combination of a growing middle class, rising vehicle ownership, and limited domestic refining capacity creating structural import dependency makes the Philippines an attractive market for global players with integrated crude supply chains. Multinational participation is also bringing capital for infrastructure upgrades, fuel quality improvements, and digital supply chain integration into the domestic market.

The Philippine government's commitment to reducing fuel import dependence by developing domestic petroleum reserves has been a consistent policy priority, gaining urgency as global price volatility and geopolitical risks in key supply corridors underscored the country's vulnerability. The Department of Energy has been actively restarting the Service Contract award process for offshore exploration blocks, with new contracts targeting the Palawan basin, Sulu Sea, and areas of the West Philippine Sea that are uncontested or accessible under bilateral arrangements. Estimated reserves in the broader West Philippine Sea region exceed 1 billion barrels of oil equivalent, representing a transformative supply opportunity if exploration barriers and geopolitical complexities can be navigated. PXP Energy's 2024 plans to participate in new block auctions signal renewed private sector confidence in domestic upstream opportunities.

The Philippine transportation sector remains the primary driver of petroleum demand, fuelled by rising vehicle ownership, fleet expansion by commercial logistics operators, and growing aviation and maritime passenger and cargo activity. The government's Build, Better, More infrastructure programme is simultaneously expanding road networks, port facilities, and airports, each of which generates primary and secondary petroleum demand. Fuel retail operators are responding by investing in network expansion, with outlets extending into new provincial corridors where vehicle density and infrastructure quality have reached commercial viability thresholds. In October 2025, official consumption data confirmed a 10% year-on-year increase in domestic fuel volumes, validating the investment strategies of retailers and terminal operators who had expanded capacity ahead of this demand growth.

Years of underinvestment in petroleum storage infrastructure have left the Philippines exposed to supply disruptions during global price spikes and logistics bottlenecks, prompting a wave of terminal and storage facility investments that gained momentum in 2025. Upgrades to bulk liquid storage terminals are improving the country's ability to maintain minimum strategic reserve levels and ensuring more reliable fuel supply to island communities across Visayas and Mindanao where supply chain logistics are structurally challenging. Operators including Seaoil, Phoenix Petroleum, and Pilipinas Shell are among those investing in expanded depot and distribution infrastructure. Modular and mini-refinery concepts are also gaining traction as a solution for serving remote areas where proximity to large refinery facilities is not economically viable, aligning with government-recommended strategies for provincial energy access.

The Expert Market Research's report titled "Philippines Petroleum Market Report and Forecast 2026 to 2035" offers a detailed analysis of the market based on the following segments:

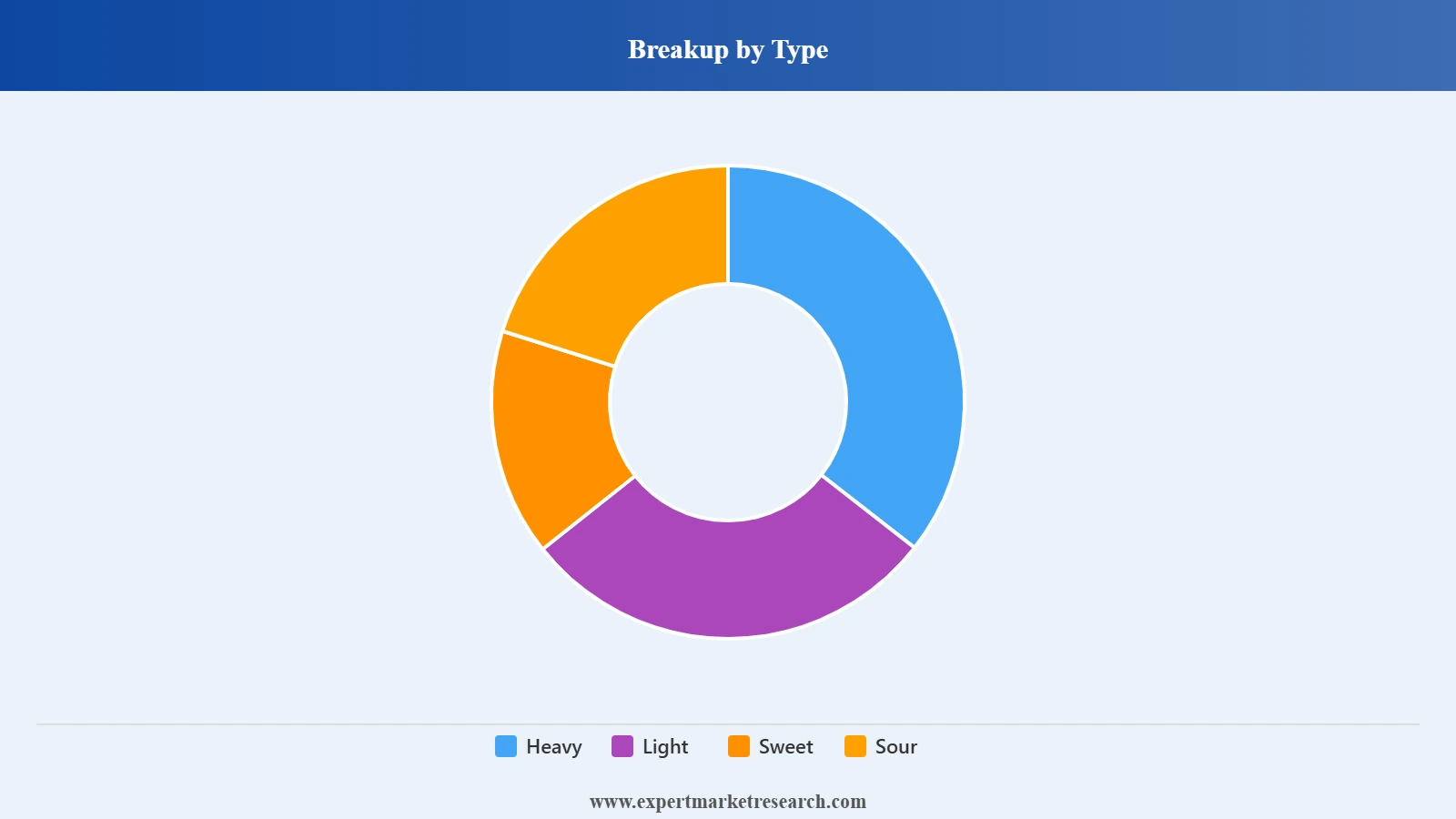

Market Breakup by Type

Key Insight: Light crude petroleum holds the dominant share in the Philippines market, reflecting the refinery configuration preferences of the country's primary refining operator and the demand profile of Philippine fuel consumers, who primarily use gasoline and diesel grades more efficiently produced from lighter crude feedstocks. Sweet crude, which carries a lower sulfur content and commands a processing cost advantage, is preferred by refiners seeking to minimise the incremental investment required in desulfurisation units. Heavy crude holds a smaller but stable position in the market, used by refineries with coking and conversion units that can economically upgrade heavier residues. Sour crude typically requires more complex refinery processing and is used in limited volumes where processing economics support its price discount over sweet grades.

Market Breakup by Location

Key Insight: Offshore petroleum dominates the Philippines' production profile given the archipelagic geography of the country and the location of its known and prospective reserves in offshore sedimentary basins. The Palawan basin, served by the Malampaya offshore gas and condensate field, has been the centrepiece of domestic petroleum production for decades and remains the most commercially significant producing asset. New offshore exploration activity is increasingly targeting deepwater blocks in the Sulu Sea and areas of the West Philippine Sea accessible under Philippine energy policy. Onshore petroleum production is minimal by comparison, with limited land-based fields in Mindanao and Palawan contributing a modest share of total domestic output. The majority of Philippines petroleum consumption is met through imports, making the development of offshore reserves a strategic energy security priority.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Light crude petroleum holds the largest share of the Philippines petroleum market by type, given the dominant demand for gasoline, naphtha, and lighter distillate products across transportation and industrial applications. Petron Corporation, as the country's sole remaining integrated refiner at its Bataan facility, has historically been configured to process predominantly light crude grades, which influences the market-wide product and feedstock mix. Sweet crude commands a premium market position among refinery operators because its low sulfur content minimises processing complexity and reduces the investment required for regulatory-compliant fuel production. Heavy crude has a smaller but consistent market presence, processed by facilities with the conversion units required to handle its heavier residue fraction.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Within the location segmentation, offshore petroleum represents the dominant domestic production source given the geological profile of the Philippines' sedimentary basins. The Malampaya field remains the country's most significant producing asset, supplying condensate and natural gas to power plants in Luzon. Onshore production is negligible in comparison, and the country's overall domestic output covers only a small fraction of total consumption, making it structurally dependent on petroleum imports - primarily from Middle Eastern and Southeast Asian suppliers. This import dependency is simultaneously a vulnerability that drives exploration investment and an opportunity that attracts global petroleum majors seeking downstream market access.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Luzon dominates the Philippines petroleum market in terms of consumption volume and revenue, driven by Metro Manila's 15 million urban population, its status as the primary industrial, commercial, and transportation hub of the country, and the concentration of power generation capacity that relies on petroleum fuel oil. The Manila Bay coastal corridor hosts the primary petroleum import terminal infrastructure and serves as the main distribution hub from which product is transported to provincial Luzon markets. The government's Build, Better, More infrastructure programme has accelerated road development in Luzon, expanding the accessible market for fuel retailers beyond the traditional National Capital Region core into emerging urban centres in Cavite, Laguna, Batangas, Rizal, and Bulacan, collectively generating new retail station investment demand. Luzon is also home to Petron's Bataan refinery, the only remaining domestic petroleum refining facility, which processes imported crude into a range of refined products for domestic consumption.

The Visayas region, centred on Cebu City, is the second-most commercially significant market for petroleum products in the Philippines, benefiting from a large inter-island maritime trade network and a growing manufacturing and tourism sector. Cebu's role as the main hub for inter-island cargo and passenger shipping creates consistent bunker fuel and marine diesel demand. Land-based transportation growth in Cebu and its satellite cities of Mandaue and Lapu-Lapu is driving retail fuel station expansion by Phoenix Petroleum, Seaoil, and Unioil. Mindanao, the southernmost major island group, represents the highest-growth frontier for petroleum demand in the country, supported by an expanding agribusiness sector with large agricultural equipment and cold chain energy requirements, growing mining activity, and rising consumer fuel consumption as incomes increase in Davao, Cagayan de Oro, and Zamboanga.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The Philippines petroleum market is structured around a small number of large integrated and retail-focused downstream operators, with the upstream production segment remaining highly concentrated given the limited domestic reserve base. Petron Corporation is the dominant player through its integrated refining and retail operations, while international oil company brands and independent fuel retailers compete for retail market share. The competitive dynamic has been evolving as global energy majors reassess their Philippine positions and as independent domestic retailers invest aggressively in network expansion and fuel quality differentiation.

The entry of Saudi Aramco into the downstream market via its Unioil stake acquisition in February 2025 signals a new phase of international competition that could shift the balance between integrated refining-retail players and pure-play import-dependent distributors. Digital supply chain technology, cleaner fuel formulations, and consumer loyalty programs are emerging as differentiating factors in a retail market where price parity across branded fuels is largely regulated.

Pilipinas Shell, founded in 1914, has been a pioneer in the retail fuels and supply chain innovation business in the Philippines. The company intends to upgrade terminals and adopt digital technology platforms to bring about smarter logistics and engage customers nationwide.

Incorporated in 1933, Petron is the largest refining and marketing company in the Philippines. The company is focused on increasing refining capacity, growing product diversity, and exporting surplus production to regional markets.

Based in Texas, United States, Chevron operates under the Caltex brand. The company’s strategy focuses on offshore exploration, premium fuel offerings, and optimizing customer experience through mobile technologies and loyalty programs.

Founded in 1954, San Jose Oil targets the regional marketplace of Visayas and Mindanao. The company invests in modular refineries and logistics fleets to increase rural market penetration and ensure last-mile fuel accessibility.

Other players in the Philippines petroleum market include Altisima Energy, Inc, Anglo-Philippine Oil & Mining Corporation, Japan Petroleum Exploration Co., Ltd., Phoenix Petroleum, Seaoil Philippines, Inc, Unioil Petroleum Philippines Inc., and Liquigaz Philippines Corp., among others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

The Philippines petroleum market operates under significant structural challenges, the most pressing of which is its acute dependence on imported crude. The country imports approximately 98% of its crude oil, sourcing the majority from the Middle East, particularly Saudi Arabia, while also relying on foreign suppliers for around 97% of liquid petroleum products. This concentration of supply creates considerable vulnerability to geopolitical disruptions, shipping delays, and price shocks in international markets. Any interruption in supply routes directly affects fuel accessibility and pricing within the country, and exposure to foreign exchange fluctuations further escalates costs for distributors and end consumers. The archipelagic geography of the Philippines adds another layer of complexity, as logistics challenges across islands significantly increase distribution costs, making last-mile delivery both expensive and operationally difficult.

Beyond operational hurdles, several structural restraints continue to limit market development. The Philippines historically recorded among the highest power rates in Asia estimated at 25% to as much as 87.5% higher than some Southeast Asian neighbors largely attributable to its heavy reliance on imported coal and oil. This cost burden suppresses industrial competitiveness and household purchasing power. Additionally, the anticipated depletion of the Malampaya natural gas field, which supplies approximately 20% of the country's energy needs, by 2027 threatens to deepen energy shortfalls unless alternative sources are secured in time. Regulatory complexities also weigh on the sector; in 2025, the Department of Energy cancelled 84 energy service contracts due to regulatory violations and project delays, representing the equivalent of more than 5,370 megawatts of capacity.

Despite these constraints, the market holds meaningful growth opportunities driven by policy reform and rising energy demand. The Department of Energy is actively pursuing regional oil stockpiling arrangements within ASEAN to strengthen collective energy security, while simultaneously advancing a long-term transition strategy. Policymakers and industry stakeholders have affirmed their commitment to an inclusive energy transition that reduces oil dependence through modern transport systems, energy-efficient industries, and expanded renewable generation. Investment in upstream exploration also presents a tangible avenue for growth, as the government has been awarding new petroleum service contracts to encourage domestic production a policy direction that, if sustained, could gradually reduce the market's reliance on external supply and improve long-term energy resilience.

Stay ahead of the curve in the Philippines petroleum sector with our authoritative 2026 market intelligence report. Whether you are a global energy company assessing downstream market entry, an independent retailer benchmarking expansion strategy, an infrastructure investor evaluating terminal and logistics opportunities, or a government analyst monitoring energy security trends, this report delivers the precision insight you need. Download your free sample today and explore the strategic opportunities driving growth in the Philippines petroleum market.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the Philippines petroleum market reached an approximate value of USD 29.27 Billion.

The market is projected to grow at a CAGR of 4.40% between 2026 and 2035.

The key players in the market include Pilipinas Corporation, Petron Corporation, Chevron Philippines, San Jose Oil Company, Incorporated, Altisima Energy, Inc, Anglo-Philippine Oil & Mining Corporation, Japan Petroleum Exploration Co., Ltd., Phoenix Petroleum, Seaoil Philippines, Inc, Unioil Petroleum Philippines Inc., and Liquigaz Philippines Corp., among others.

Key strategies driving the market include shifting towards cleaner fuel processing technologies, increase activities in offshore exploration and drilling, focus on mini and modular refineries for remote areas and integrate digital supply chain technolgies.

The major types of crude considered in the market report are light, heavy, sweet, and sour. The light segment is expected to grow at 5.0% CAGR during the forecast period.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Type |

|

| Breakup by Location |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.