Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

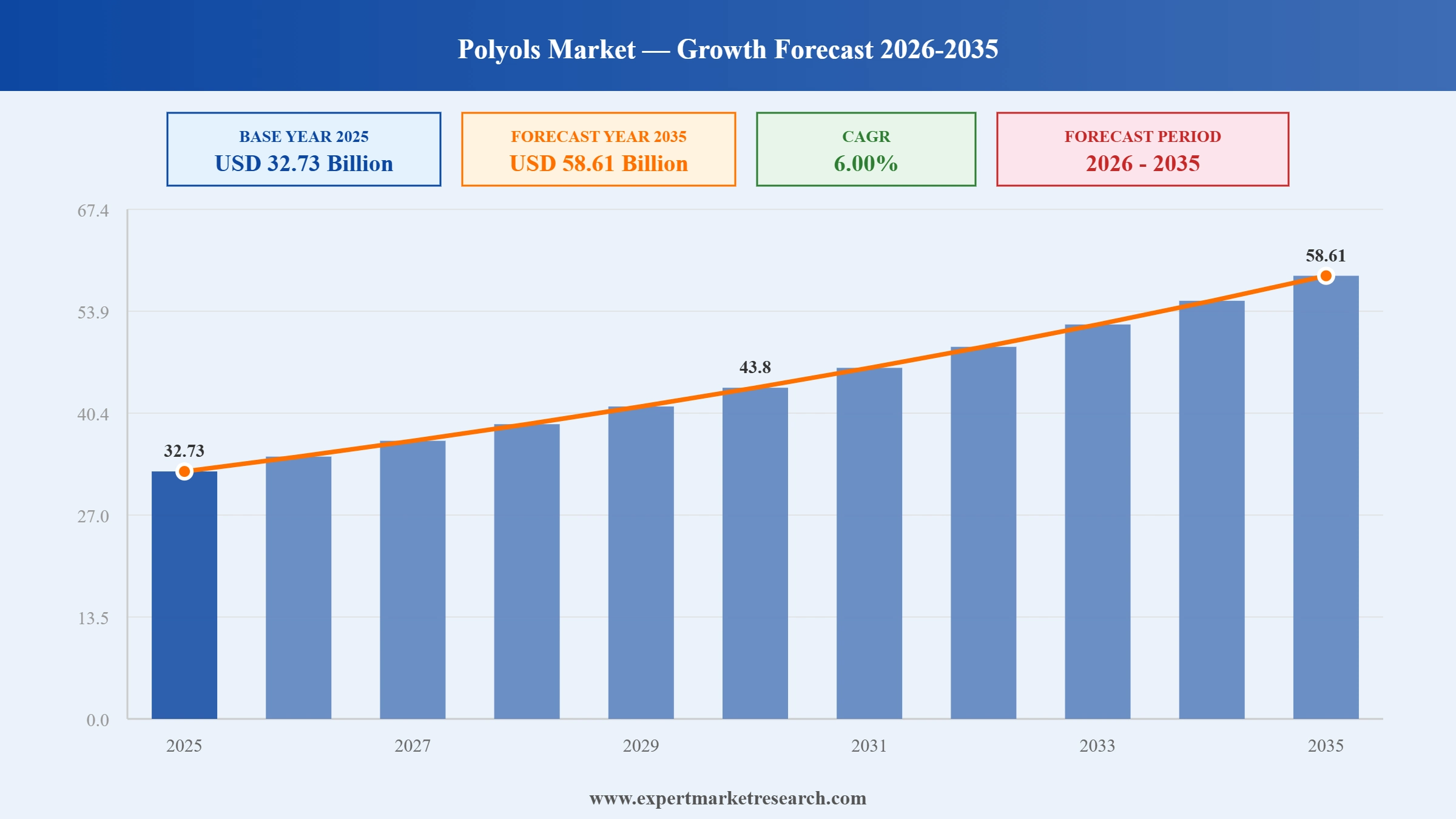

The global polyols market reached a value of USD 32.73 Billion at 2025 and is projected to expand at a CAGR of around 6.00% during the forecast period of 2026-2035. Driven by rising demand for polyurethane foams in construction insulation, growing automotive lightweighting requirements, expanding furniture and bedding industries, and accelerating adoption of bio-based polyol formulations globally, the market is expected to reach USD 58.61 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

| Global Polyols Market Report Summary | Description | Value |

| Base Year | USD Billion | 2025 |

| Historical Period | USD Billion | 2019-2025 |

| Forecast Period | USD Billion | 2026-2035 |

| Market Size 2025 | USD Billion | 32.73 |

| Market Size 2035 | USD Billion | 58.61 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 6.00% |

| CAGR 2026-2035 - Market by Region | Asia Pacific | 6.8% |

| CAGR 2026-2035 - Market by Country | India | 7.8% |

| CAGR 2026-2035 - Market by Country | Brazil | 7.1% |

| CAGR 2026-2035 - Market by Application | CASE (Coatings, Adhesives, Sealants & Elastomers) | 6.6% |

| CAGR 2026-2035 - Market by Industry | Automotive | 6.9% |

| Market Share by Country 2025 | Italy | 3.1% |

The global polyols market is undergoing a significant transformation, driven by the accelerating shift toward bio-based and recycled polyol formulations alongside sustained demand from the construction, automotive, and furniture industries. Major chemical producers are expanding capacity in Asia Pacific, investing in sustainable raw material partnerships, and deploying carbon-efficient production technologies to align with evolving environmental regulations and corporate sustainability commitments.

ADNOC finalised its acquisition of Covestro AG through subsidiary XRG in 2025 in a transaction valued at up to approximately EUR 16 billion. The deal integrated Covestro's leading polyurethane and polyols business into ADNOC's expanding chemicals platform, creating a major vertically integrated producer with global reach across polyols manufacturing, downstream polyurethane applications, and sustainability-driven material innovation.

BASF SE launched a new line of bio-based polyols in August 2025, derived from renewable feedstocks to meet growing demand for sustainable polyurethane raw materials across construction, automotive, and consumer goods sectors. The product expansion strengthened BASF's sustainable materials portfolio and positioned the company to capture growing share in the eco-conscious segment of the global polyols market amid tightening environmental regulations.

South Korea's Dongsung Chemical opened a new 81,000 square metre polyurethane production facility in Karawang, Indonesia, in May 2025. With an annual production capacity of 67,000 tonnes of polyurethane materials including polyester polyols and prepolymers, the investment tripled the company's previous combined output across China, Korea, and Vietnam, significantly expanding its footprint in the high-growth Southeast Asian polyols market.

Covestro and Shell plc formalised a long-term supply agreement for bio-circular polyols in the first quarter of 2025, establishing a strategic vertical integration model for sustainable polyurethane raw material sourcing. The agreement reflected both companies' commitment to circular feedstock adoption and signalled Covestro's proactive approach to securing renewable and recycled supply chains within the evolving global polyols market landscape.

Bio-based and recycled polyols are transforming the global polyols market as regulations and corporate sustainability targets drive adoption of renewable feedstocks. BASF's launch of bio-derived polyols from rapeseed and soybean in August 2025 exemplifies how leading producers are repositioning product portfolios to capture growing demand for sustainable polyurethane raw materials globally.

Asia Pacific is the fastest-growing region for the polyols market, driven by booming construction, automotive, and furniture industries in China, India, and Southeast Asia. Dongsung Chemical's new 67,000-tonne Indonesian polyurethane facility, operational from May 2025, reflects the strong foreign direct investment flowing into the region's rapidly expanding polyols production and demand landscape.

Stricter building energy efficiency standards globally are accelerating demand for rigid polyurethane foam insulation, creating sustained growth for the polyols market. Polyols-derived rigid foam delivers superior thermal performance for walls, roofs, and cold-chain applications. This structural demand is particularly strong in Europe and North America, where energy efficiency mandates are increasingly shaping building material specifications and procurement decisions.

The global automotive industry's shift toward electric vehicles is creating new demand for lightweight, high-performance polyurethane components derived from polyols across seating, acoustic insulation, and structural foam applications. Polyols producers are developing specialised low-density, high-resilience foam grades targeting EV manufacturers seeking both performance improvements and vehicle weight reductions critical for extending battery range efficiency globally.

The global polyols market is experiencing significant strategic consolidation, with ADNOC's acquisition of Covestro and BASF's joint venture with Wanhua Chemical in China reshaping competitive dynamics. These transactions indicate major producers prioritising scale, geographic diversification, and vertical integration across the polyurethane value chain to strengthen their positions in a market characterised by rising bio-based material demand and shifting regional growth patterns.

The Expert Market Research's report titled "Global Polyols Market Report and Forecast 2026-2035" offers a detailed analysis of the market based on the following segments:

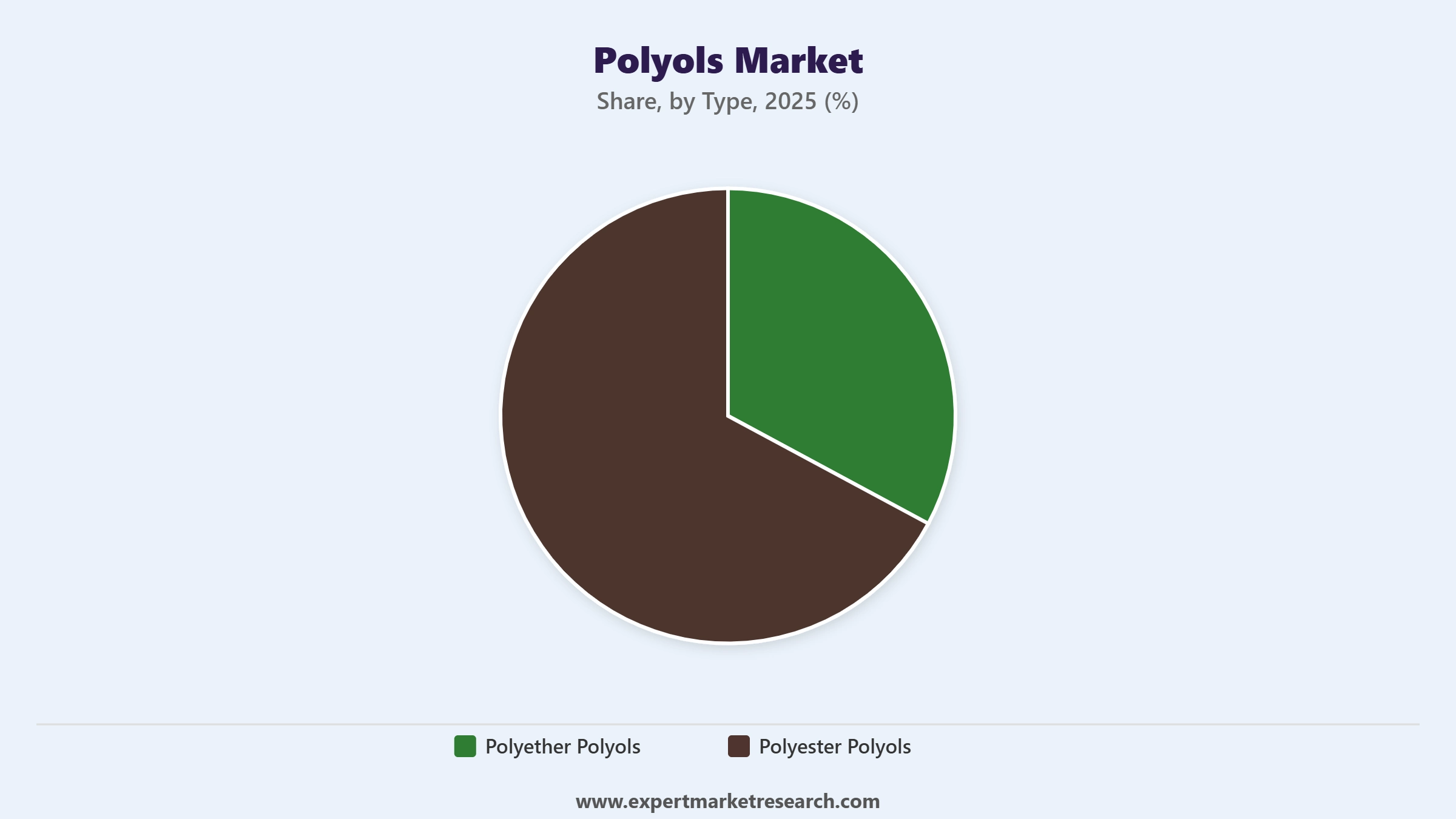

Market Breakup by Type

Key Insight: Polyether polyols dominate the global polyols market by type, accounting for the majority of production volume due to their superior flexibility, moisture resistance, and cost-effectiveness in flexible foam applications. They are the preferred raw material for mattress and furniture foam, automotive seating, and carpet backing. The bio-based segment within polyether polyols is growing rapidly, with producers such as BASF and Covestro investing in renewable feedstock sourcing and bio-circular supply agreements to serve sustainability-driven buyers.

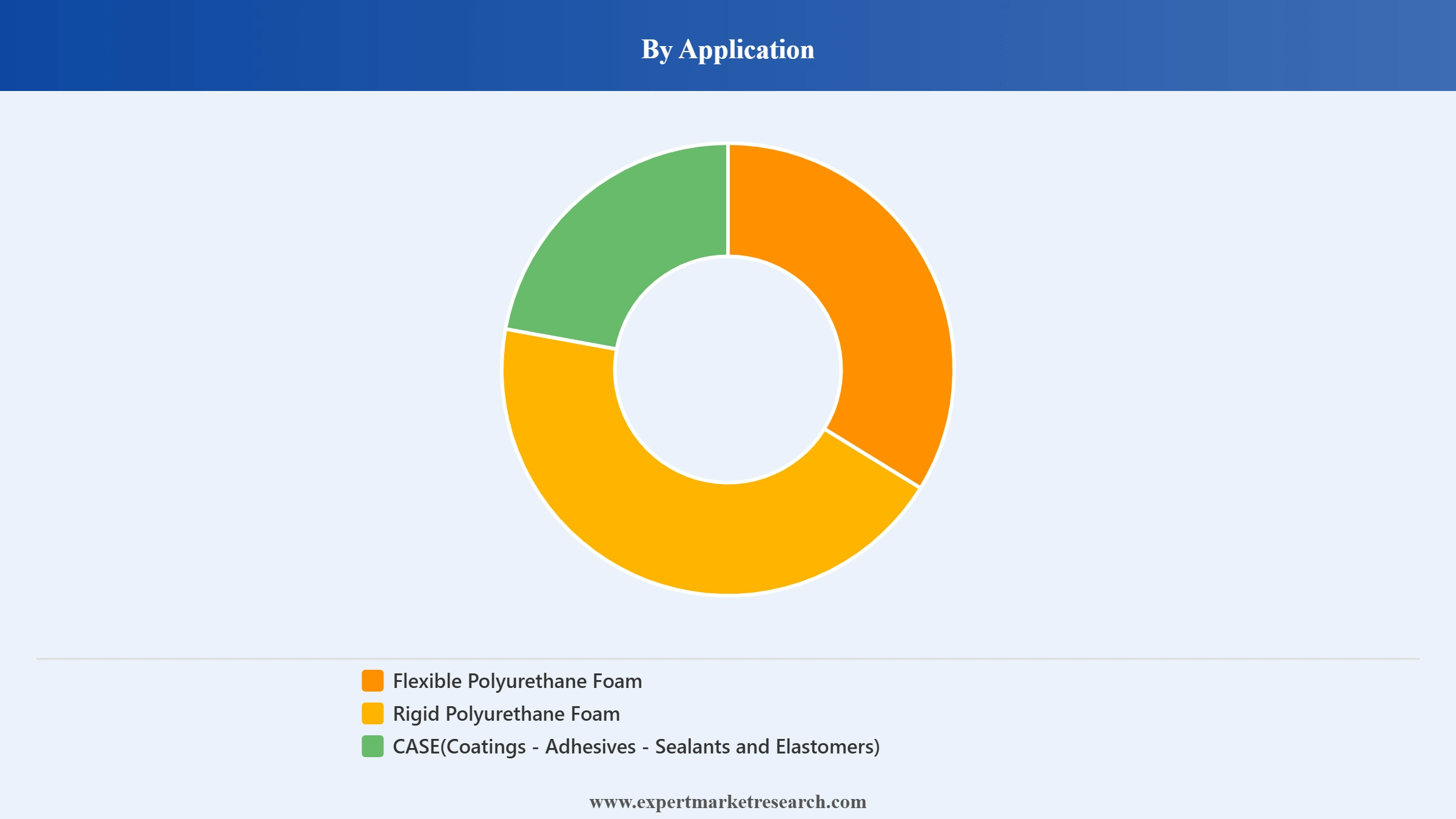

Market Breakup by Application

Key Insight: Flexible polyurethane foam leads the global polyols market by application, driven by pervasive use in furniture, mattresses, automotive seating, and consumer goods upholstery globally. Rigid polyurethane foam is the fastest-growing application, supported by tightening energy efficiency regulations in buildings and cold-chain logistics. In September 2024, BASF and Future Foam announced the first commercially produced flexible foam for bedding using 100% domestically produced bio-based toluene diisocyanate, reflecting the polyols market's push toward sustainable applications.

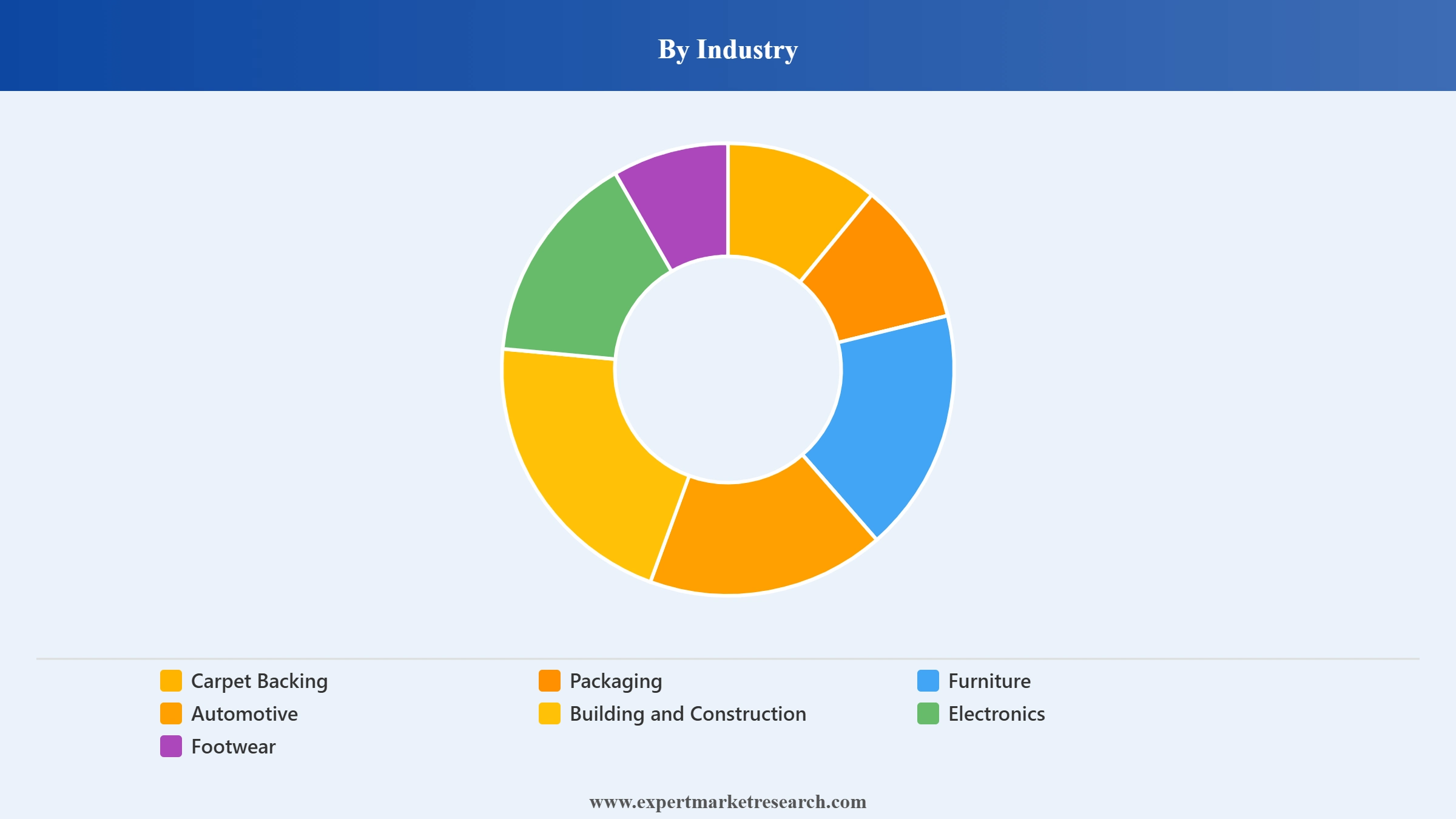

Market Breakup by Industry

Key Insight: Furniture represents the largest industry segment within the global polyols market, driven by consistent global demand for foam-based upholstered furniture, mattresses, and bedding products. Building and construction is the fastest-growing industry, propelled by energy efficiency mandates requiring high-performance insulation. The automotive industry is a significant growth segment, with EV manufacturers demanding lightweight polyurethane components for seating, insulation, and structural applications, accelerating polyols consumption across the automotive value chain.

Market Breakup by Region

Key Insight: Asia Pacific dominates the global polyols market by consumption volume, led by China and India's massive construction, automotive, and furniture manufacturing bases. North America and Europe are mature markets with growing bio-based and sustainable polyols adoption driven by regulatory pressure. The Middle East is an emerging polyols production hub, supported by petrochemical feedstock advantages and government-led industrial diversification programs under initiatives such as Saudi Arabia's Vision 2030.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Type, Polyether Polyols dominate the market due to their versatile performance properties and cost-effective production economics

Polyether polyols account for the dominant share of the global polyols market by type, reflecting their superior performance characteristics in flexible foam applications, including excellent resilience, low-temperature flexibility, and hydrolytic stability compared to polyester alternatives. Their lower production cost relative to polyester polyols makes them the preferred choice for high-volume applications in mattress, furniture, automotive, and carpet backing segments across all major producing regions.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Polyester polyols are gaining share in high-performance CASE applications including coatings, adhesives, sealants, and elastomers, where their superior mechanical strength and chemical resistance justify a premium over polyether grades. In May 2025, Dongsung Chemical's new Indonesian polyurethane plant, which includes polyester polyol production capacity, reflected the strategic investment in polyester polyols manufacturing to serve Southeast Asia's growing industrial demand within the global polyols market.

By Application, Flexible Polyurethane Foam accounts for the dominant share of the market due to its pervasive end-use demand across furniture, automotive, and bedding sectors

Flexible polyurethane foam represents the largest application segment in the global polyols market, driven by the globally consistent demand for foam-based seating, bedding, and cushioning products across furniture and automotive sectors. The segment's stability reflects the structural nature of consumer demand for comfort materials in both developed and emerging markets, with Asia Pacific's growing middle-class consumer base providing incremental demand growth for foam products.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Rigid polyurethane foam is demonstrating strong growth within the global polyols market, underpinned by accelerating adoption of high-performance building insulation under increasingly stringent energy efficiency codes in Europe and North America. Cold-chain logistics infrastructure expansion in Asia Pacific and Latin America is also generating incremental demand for rigid foam insulation panels. In September 2024, BASF and Future Foam's first commercial bio-based flexible foam for bedding highlighted the deepening integration of sustainability into the market.

By Industry, Building and Construction accounts for a growing share of the market due to rising demand for energy-efficient insulation materials globally

Building and construction is the fastest-growing industry segment in the global polyols market, driven by tightening energy efficiency regulations in Europe and North America and rapid construction sector expansion in Asia Pacific, Latin America, and the Middle East. Rigid polyurethane foam panels derived from polyols deliver superior thermal insulation performance, making them a preferred specification material for both new construction and retrofitting projects targeting energy consumption reductions.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The furniture industry remains the largest consumer of polyols globally, anchored by consistent demand from residential and commercial furniture producers across all geographies. Asia Pacific, particularly China and Vietnam, has become the dominant manufacturing hub for foam-based furniture, driving strong regional polyols demand. The transition toward bio-based polyols in furniture manufacturing is accelerating, as brands respond to retailer sustainability requirements and consumer preferences for environmentally responsible polyols market products.

Asia Pacific dominates the market due to its large-scale construction, automotive, and furniture manufacturing industries

Asia Pacific leads the global polyols market in consumption volume, driven by China's massive construction and furniture manufacturing base and India's rapidly expanding automotive and construction sectors. The region's polyols demand is reinforced by strong domestic consumption growth in bedding, upholstery, and insulation products, alongside a growing local manufacturing base with producers establishing dedicated regional facilities to serve the fast-growing Southeast Asian polyols market.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Europe represents the fastest-growing region in regulatory-driven bio-based polyols adoption, with manufacturers in Germany, France, and the Netherlands investing in renewable feedstock sourcing and circular polyurethane technologies under EU Green Deal mandates. In Q1 2025, Covestro and Shell's long-term bio-circular polyols agreement positioned Europe as a leading market for sustainable polyols innovation. North America continues to see steady polyols demand from the construction and automotive sectors, supported by nearshoring manufacturing initiatives and infrastructure investment programs boosting building materials demand within the global polyols market.

The global polyols market is moderately consolidated, with a small number of large chemical conglomerates holding significant production capacity and global distribution networks. Key players compete on product range breadth, sustainability credentials, pricing competitiveness, and geographic presence. The market is witnessing accelerating consolidation through major acquisitions and joint ventures as producers seek scale advantages and bio-based feedstock access to meet evolving customer and regulatory requirements.

Founded in 1865 and headquartered in Ludwigshafen, Germany, BASF SE is one of the world's largest chemical companies with a comprehensive polyols portfolio spanning flexible, rigid, and specialty grades under its Pluracol and Lupranate product lines. In August 2025, BASF launched a new bio-based polyols line derived from renewable feedstocks, reinforcing its position as a sustainability leader. BASF's global R&D network and integrated polyurethane systems capabilities make it a key supplier across construction, automotive, and furniture industries globally.

Founded in 2015 as a spin-off from Bayer and headquartered in Leverkusen, Germany, Covestro AG is a world-leading polyurethane and polyols producer. Acquired by ADNOC through XRG in 2025 in a transaction valued at up to approximately EUR 16 billion, Covestro supplies polyether and polyester polyols to major customers across construction, automotive, footwear, and coatings sectors globally. The company's CQ-Configurator tool for real-time CO2 footprint calculation reflects its leadership in digital transparency for sustainable polyols procurement.

Founded in 1897 and headquartered in Midland, Michigan, The Dow Chemical Company is a leading global materials science company with a major presence in the polyols market through its VORANOLTM product line serving flexible and rigid foam applications. Dow's VORANOLTM WK5750 next-generation polyether polyol targets hypersoft flexible foam for furniture, mattresses, and automotive seating. The company leads commercial development of bio-based polyol technology and foam recycling systems as part of its sustainability commitment across the global polyols market.

Founded in 1970 and headquartered in The Woodlands, Texas, Huntsman International LLC is a global manufacturer of differentiated chemical products including a strong polyurethane raw materials business encompassing polyols and isocyanates. Huntsman's JEFFOLTM polyol line serves flexible foam, rigid foam, and CASE applications across global markets. The company has invested in Asia Pacific production to serve growing regional demand and maintains technical service and formulation support capabilities for polyols customers worldwide.

Other key players in the market are Royal Dutch Shell Plc, Wanhua Chemical Group Co., Ltd., Stepan Company, Repsol S.A., and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Gain a competitive advantage in the evolving global polyols landscape with our comprehensive report for 2026. Covering type-level analysis, application trends, regional market dynamics, and competitive profiles, this report provides the insights needed to navigate a market driven by sustainability mandates and industrial growth. Download your free sample today and discover the key opportunities in the polyols market.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

The global polyols market reached a value of USD 32.73 Billion in 2025.

The global polyols market is projected to grow at a CAGR of nearly 6.00% in the forecast period of 2026-2035.

The global polyols market is estimated to reach a value of about USD 58.61 Billion by the year 2035.

The major drivers of the global polyols market include rising disposable incomes, increasing population, rising construction industry, and the growing demand from the automobile sector.

The rising production of bio-based polyols is expected to be a key trend guiding the growth of the market.

North America, Europe, the Asia Pacific, Latin America, and the Middle East and Africa are the leading regions in the market, with the Asia Pacific accounting for the largest market share.

The major product types in the market include polyether and polyester polyols.

Polyols find wide applications in flexible polyurethane foam, rigid polyurethane foam, and CASE (coatings, adhesives, sealants, and elastomers), among others.

Based on industry, the market is divided into carpet backing, packaging, furniture, automotive, building and construction, electronics, and footwear, among others.

The major players in the market are BASF SE, Royal Dutch Shell Plc, Covestro AG, The Dow Chemical Company, Wanhua Chemical Group Co., Ltd., Huntsman International LLC, Stepan Company, and Repsol S.A., among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Type |

|

| Breakup by Application |

|

| Breakup by Industry |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

| Report Price and Purchase Option | Explore our purchase options that are best suited to your resources and industry needs. |

| Delivery Format | Delivered as an attached PDF and Excel through email, with an option of receiving an editable PPT, according to the purchase option. |

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.