Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

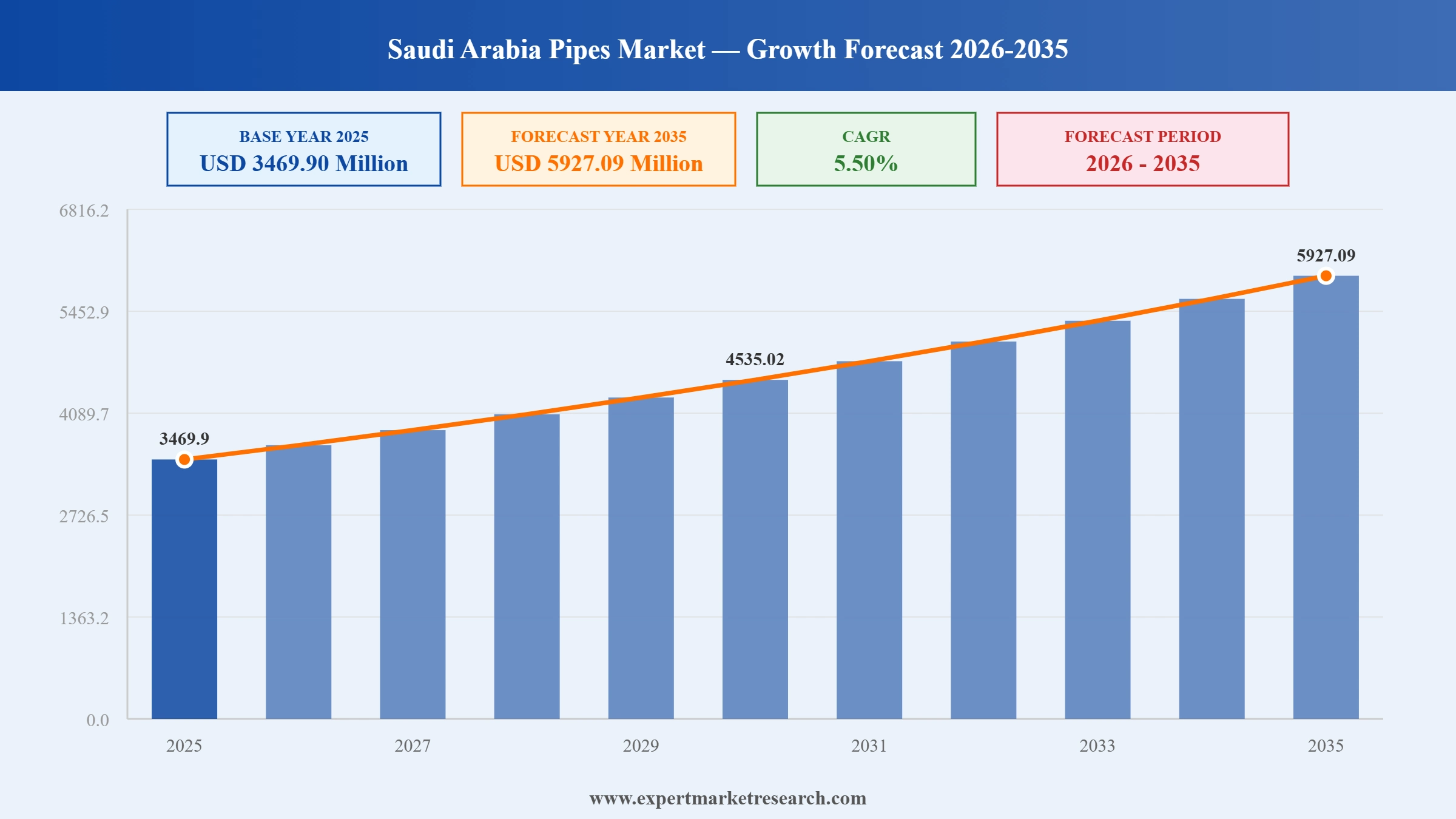

The Saudi Arabia Pipes Market reached a value of USD 3469.90 Million at 2025 and is projected to expand at a CAGR of around 5.50% during the forecast period of 2026-2035. With massive public infrastructure expenditure under Vision 2030 driving demand across water, sewage, and urban construction applications, the rapid rise of plastic pipes as the preferred material for municipal networks, ongoing expansion of industrial and manufacturing zones requiring specialized piping, and growing investments in smart and IoT-integrated pipeline monitoring systems, the market is expected to reach USD 5927.09 Million by 2035.

The Saudi Arabia pipes market is currently undergoing a transformation driven by Vision 2030 infrastructure mandates, water conservation goals, and industrial zone expansions. The growing focus on urban sustainability and non-oil sector investments is reshaping how pipes are manufactured, deployed, and maintained. As per the Saudi Ministry of Environment, Water and Agriculture, over SAR 1.2 billion (USD 320 million) has been allocated to water infrastructure projects by 2030, indirectly accelerating pipe demand across water transport, sewage management, and greywater reuse systems.

Advancements in material technology and project design are boosting the Saudi Arabia pipes market dynamics. Notably, the National Water Strategy is focusing on smart pipeline networks using IoT-enabled leak detection sensors and SCADA-integrated pipe flows. These are being embedded in regions like Eastern Province and Riyadh, where high population density demands predictive maintenance. According to data from the Saline Water Conversion Corporation (SWCC), the Kingdom produced over 7.5 million m³/day of desalinated water in 2024, necessitating durable, corrosion-resistant piping networks.

In addition to municipal developments, the industrial sector in Saudi Arabia is rapidly gaining momentum as a key driving factor of the pipes industry. Major giga-projects like NEOM and Red Sea Global are adopting advanced piping solutions for underground cooling, modular infrastructure, and high-pressure drainage. To meet these demands, suppliers are expanding their product portfolios with innovations such as smart pipe linings, antimicrobial coatings, and trenchless installation methods. These technologies are now becoming standard across large-scale infrastructure projects in the Kingdom.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

|

Saudi Arabia Pipes Market Report Summary |

Description |

Value |

|

Base Year |

USD Million |

2025 |

|

Historical Period |

USD Million |

2019-2025 |

|

Forecast Period |

USD Million |

2026-2035 |

|

Market Size 2025 |

USD Million |

3469.90 |

|

Market Size 2035 |

USD Million |

5927.09 |

|

CAGR 2019-2025 |

Percentage |

XX% |

|

CAGR 2026-2035 |

Percentage |

5.50% |

|

CAGR 2026-2035 - Market by Region |

Riyadh |

6.3% |

|

CAGR 2026-2035 - Market by Region |

Makkah |

5.8% |

|

CAGR 2026-2035 - Market by Material |

Plastic |

5.8% |

|

CAGR 2026-2035 - Market by Application |

Offices and Housing |

6.4% |

|

2025 Market Share by Region |

Eastern Province |

47.6% |

The Saudi Arabia Pipes Market is being shaped by an extraordinary public investment cycle, shifting material preferences, and the integration of digital monitoring into pipeline infrastructure. Vision 2030 is the central force, but its impact is reverberating across all segments, from municipal water networks to oil and gas flowlines and industrial utilities.

In April 2025, the National Water Company (NWC) completed a SAR 400 million project to deliver desalinated water to three governorates in the Riyadh region. The project involved the installation of extensive HDPE pipeline networks across the targeted governorates to ensure reliable delivery of clean water to residential and commercial areas. This development represents one of the most significant recent examples of the scale of water infrastructure investment under Saudi Vision 2030's water sector agenda, which has earmarked SAR 1.2 billion for water infrastructure by 2030. Projects of this nature translate directly into substantial demand for large-diameter plastic and concrete pipes across multiple governorates and construction phases.

In March 2025, the Saudi government awarded mining exploration licenses to several international firms including India's Vedanta and a consortium of Ajlan and Bros alongside China's Zijin Mining, covering mineral-rich regions including Jabal Sayid and Al Hajar, known for deposits of copper, zinc, gold, and silver. The licenses span a combined area of 4,788 square kilometres, with an initial investment of approximately USD 97.6 million planned over three years. The expansion of mining activities across the Kingdom is a direct and growing demand driver for pipes, as mineral extraction operations require extensive pipeline infrastructure for slurry transport, water management, and drainage. Vision 2030 designates mining as the third pillar of Saudi industrial growth after oil and gas and petrochemicals.

In January 2025, Strohm, a specialist in thermoplastic composite pipe (TCP) technology, secured a significant contract to supply 33 kilometres of TCP for Saudi Aramco's Fadhili gas plant expansion project in Saudi Arabia. Thermoplastic composite pipes are gaining traction in the oil and gas sector for their superior corrosion resistance, reduced weight compared to steel alternatives, and longer operational lifespan in chemically aggressive and high-pressure environments. The Strohm contract is one of the clearest indicators of the broader material shift underway in Saudi Arabia's oil and gas infrastructure, where non-metallic piping is steadily replacing conventional steel in flowline and process piping applications.

In October 2024, Saudi Vitrified Clay Pipe Co. (SVCP) and Qatar's Laffan Pipes Factory signed an agreement to establish a joint venture focused on the production and distribution of durable pipe products and related components for the Gulf region. The partnership is designed to combine manufacturing expertise and regional distribution reach, enabling both parties to better serve the rapidly growing infrastructure project pipeline across Saudi Arabia and the broader GCC. The alliance reflects the increasing consolidation activity among regional pipe manufacturers as they position themselves to capture a larger share of the infrastructure spending surge tied to Vision 2030 and equivalent national development programs in neighbouring states.

In July 2024, Perma-Pipe International Holdings, Inc. announced that it had been awarded contracts totalling USD 10 million for infrastructure projects spread across Riyadh, Madinah, and Mekkah in Saudi Arabia. The contracts specify the use of the company's advanced XTRU-THERM insulation technology for pipeline systems serving district cooling, water transmission, and utility networks. The contracts reflect the growing demand for thermally efficient and high-performance insulated piping solutions in Saudi Arabia's desert environment, where maintaining pipeline integrity against temperature extremes is a critical operational requirement. The awards highlight the growing appetite for specialized piping solutions beyond standard plastic and metal pipes across Saudi infrastructure projects.

Saudi Arabia's Vision 2030 initiative has moved well beyond planning and is now in large-scale execution, channelling billions into megacity construction, water network modernisation, sewage expansion, and industrial zone development. Every infrastructure category that vision touches creates direct pipe demand, from the plumbing of new residential communities to the heavy-diameter pipelines of NEOM and Jeddah Central. The Saudi Ministry of Environment, Water, and Agriculture has allocated over USD 320 million specifically for water infrastructure by 2030, a targeted commitment that is translating directly into procurement of pipes across plastic, metal, and concrete categories. This policy-driven demand has made Vision 2030 the dominant growth engine for the Saudi Arabia Pipes Market growth. In 2024, Saudi Arabia broadcast a trillion-dollar pipeline of planned infrastructure projects, creating multi-year forward demand certainty for pipe manufacturers and distributors operating across the Kingdom.

Saudi municipalities are moving beyond passive pipeline infrastructure toward intelligent, digitally monitored systems that can detect leaks, measure flow rates, and flag anomalies in real time. SCADA-linked sensors, RFID tags, and fibre-optic leak detection technologies are being embedded in new pipeline installations, particularly for water and sewage networks where loss reduction and system reliability are strategic priorities. This shift is also influencing material specifications, as buyers increasingly specify pipe types that accommodate sensor integration or smart-compatible installation methods. In 2024, the National Water Company piloted a fibre-optic-based leak detection system in Burayada, establishing a replicable model for intelligent pipeline management that is now being evaluated for broader rollout across the Kingdom's urban water networks.

HDPE and PVC pipes are progressively replacing traditional metal alternatives in a growing share of municipal and industrial pipe applications across Saudi Arabia. Their corrosion resistance in harsh desert conditions, lower weight, competitive cost, and suitability for trenchless installation techniques give them material advantages in the Kingdom's arid and sand-heavy terrain. HDPE currently holds over 62.9% of the PE pipes market in Saudi Arabia, reflecting its entrenched position in water supply, sewage, and gas distribution. The trend is being reinforced by government procurement preferences and the growing number of domestic plastic pipe manufacturers expanding capacity to serve Vision 2030 project requirements. In July 2024, Perma-Pipe secured USD 10 million in contracts for infrastructure in Riyadh, Madinah, and Mekkah using advanced insulated piping systems, demonstrating the premium increasingly placed on high-performance plastic-based solutions.

The Saudi government's industrial localization policy, operating under the Vision 2030 umbrella, is actively pushing pipe manufacturers to build or expand domestic production capacity. Companies that manufacture locally benefit from reduced logistics costs, shorter lead times, and eligibility for public sector contracts that now carry local content requirements. In response, several regional pipe producers are investing in new capacity, particularly for HDPE, PVC, and CPVC products that are in high demand from municipal and construction buyers. In January 2025, the Ministry of Energy allocated petrochemical feedstock to new industrial complexes at Jubail Industrial City through Tasnee and Sipchem, targeting combined polyethylene production that will feed directly into the domestic pipe manufacturing supply chain. This upstream investment is a structural shift that will lower input costs for Saudi pipe makers and improve long-term price competitiveness against imports.

The EMR’s report titled “Saudi Arabia pipes Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

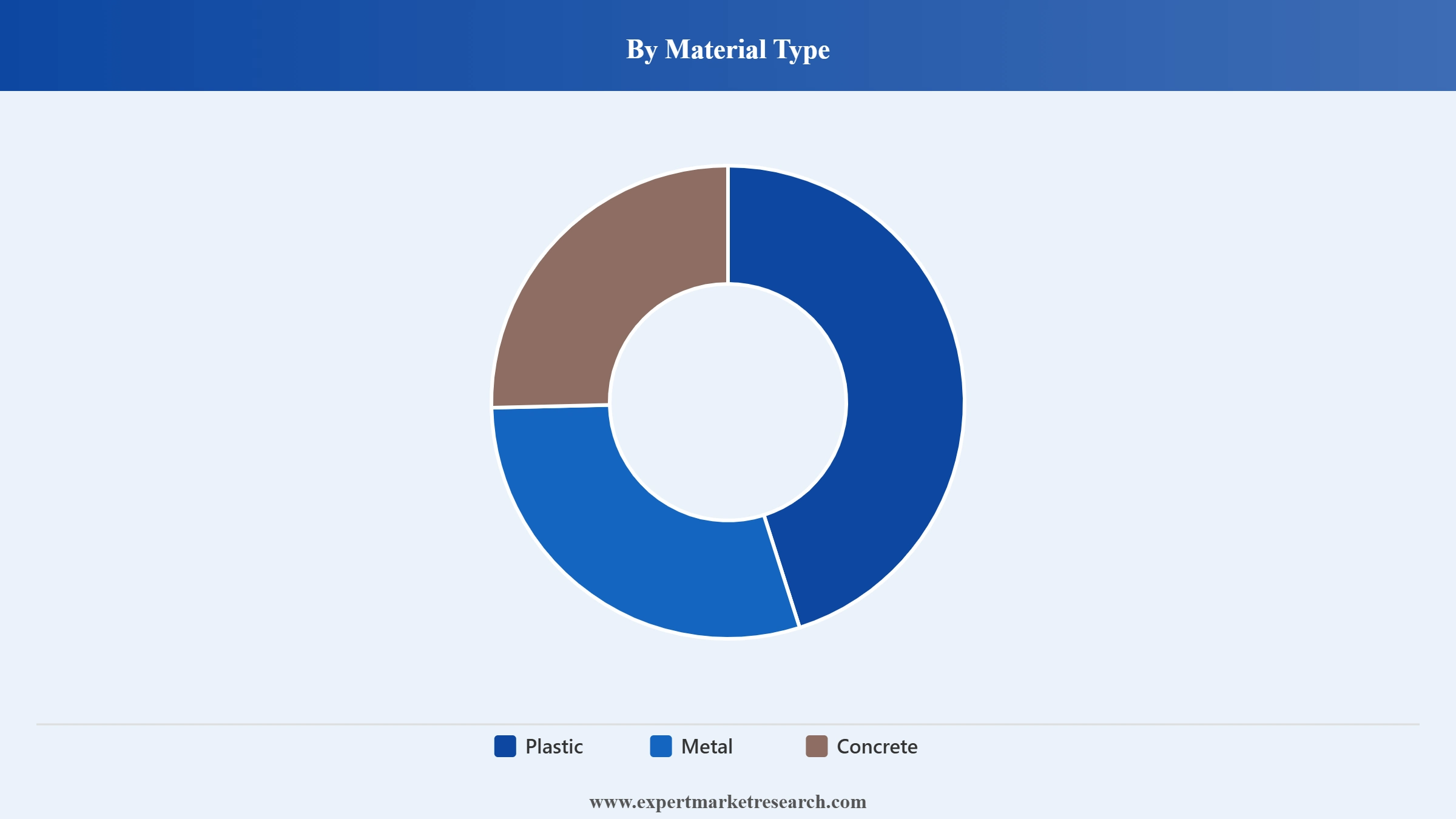

Market Breakup by Material Type

Key Insight: Plastic pipes dominate the Saudi Arabia pipes market, with HDPE holding the largest share within the plastic sub-segment given its superior corrosion resistance, flexibility, and suitability for demanding municipal and industrial applications in the Kingdom's extreme desert conditions. HDPE's dominance is particularly notable in water supply and sewage systems, where its long service life and chemical compatibility reduce lifecycle costs. PVC pipes follow as the second major plastic type, driven by their widespread use in sewerage, drainage, and residential plumbing. CPVC is gaining traction in applications requiring higher temperature and pressure tolerance, such as industrial process piping. Metal pipes, particularly ductile iron and ERW steel, remain critical for high-pressure transmission mains and oil and gas infrastructure where structural strength and pressure tolerance are paramount. Concrete pipes serve stormwater drainage and foundational works, particularly in arid regions prone to flash flooding.

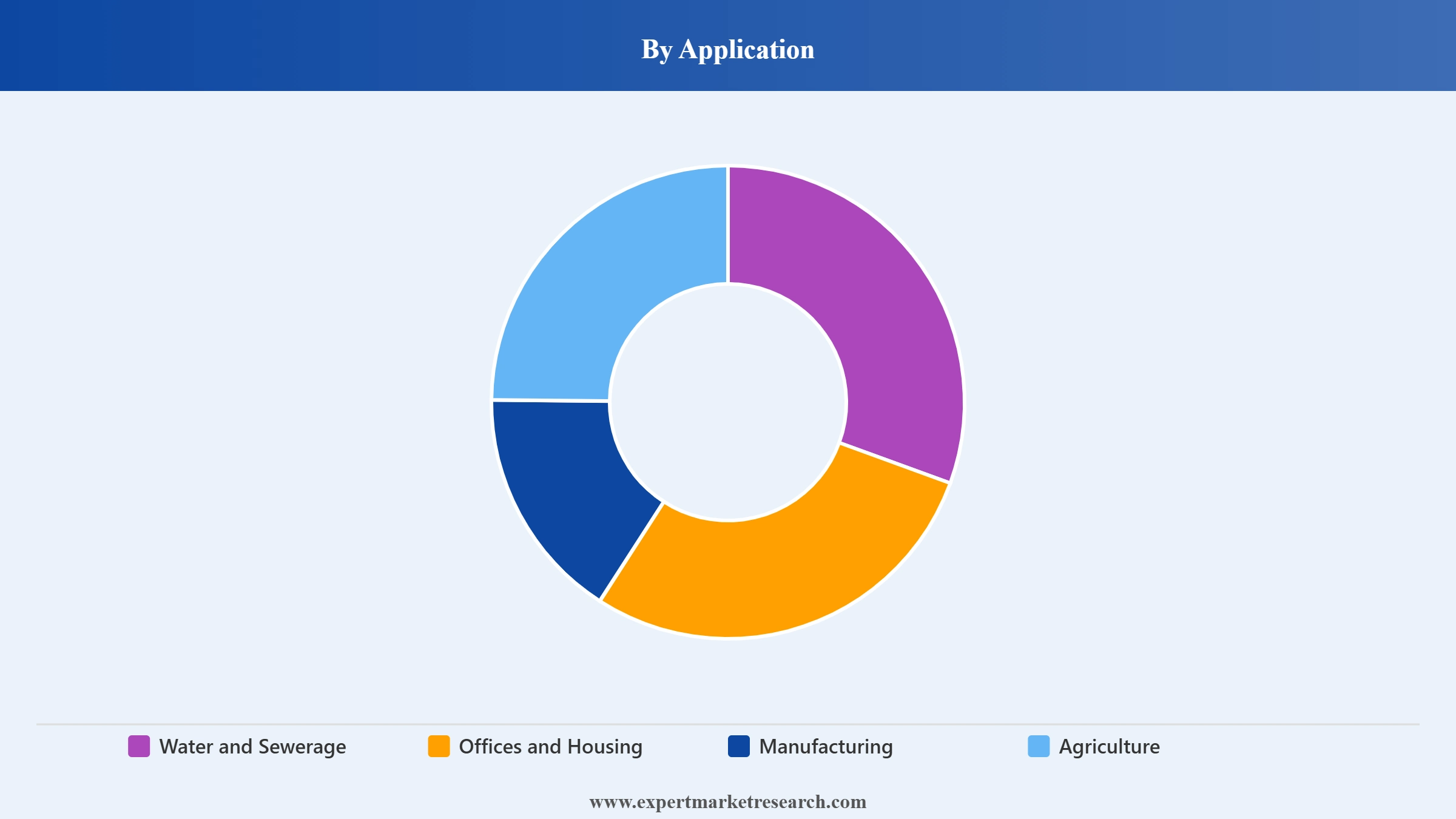

Market Breakup by Application

Key Insight: Water and sewerage is the dominant application, accounting for the largest share of Saudi Arabia's pipes market by value. The government's sustained investment in desalination plant construction, water distribution network upgrades, and sewage expansion across major urban centres has created long-term, policy-backed demand. The offices and housing segment is expanding rapidly in line with population growth, urbanisation, and the construction of new residential communities tied to megacity projects including NEOM and Jeddah Central. Manufacturing is the fastest-growing application segment as the Kingdom's industrial zone expansion under Vision 2030 creates new demand for process piping, chemical transfer lines, and cooling systems in factories and petrochemical facilities. Agriculture, while smaller in value, benefits from expanding irrigation infrastructure in arid regions.

Market Breakup by Diameter

Key Insight: Small-diameter pipes in the up to 50 mm and 50 to 100 mm categories are primarily used in residential plumbing and office building systems, benefiting from the steady pace of new construction across Saudi urban centres. Medium-diameter pipes in the 100 to 200 mm and 200 to 400 mm ranges serve municipal water distribution mains and sewage collection networks, representing the highest combined volume in the Saudi Arabia pipes market given ongoing investment in expanding water networks to growing cities and new residential zones. Large-diameter pipes above 400 mm serve major transmission mains, large-scale desalination plant connections, and industrial process lines, with demand linked closely to government-funded water infrastructure and energy sector projects. The NWC's April 2025 Riyadh water project specified pipes in the 200 to 500 mm range, illustrating the scale of mid-to-large diameter demand in municipal infrastructure.

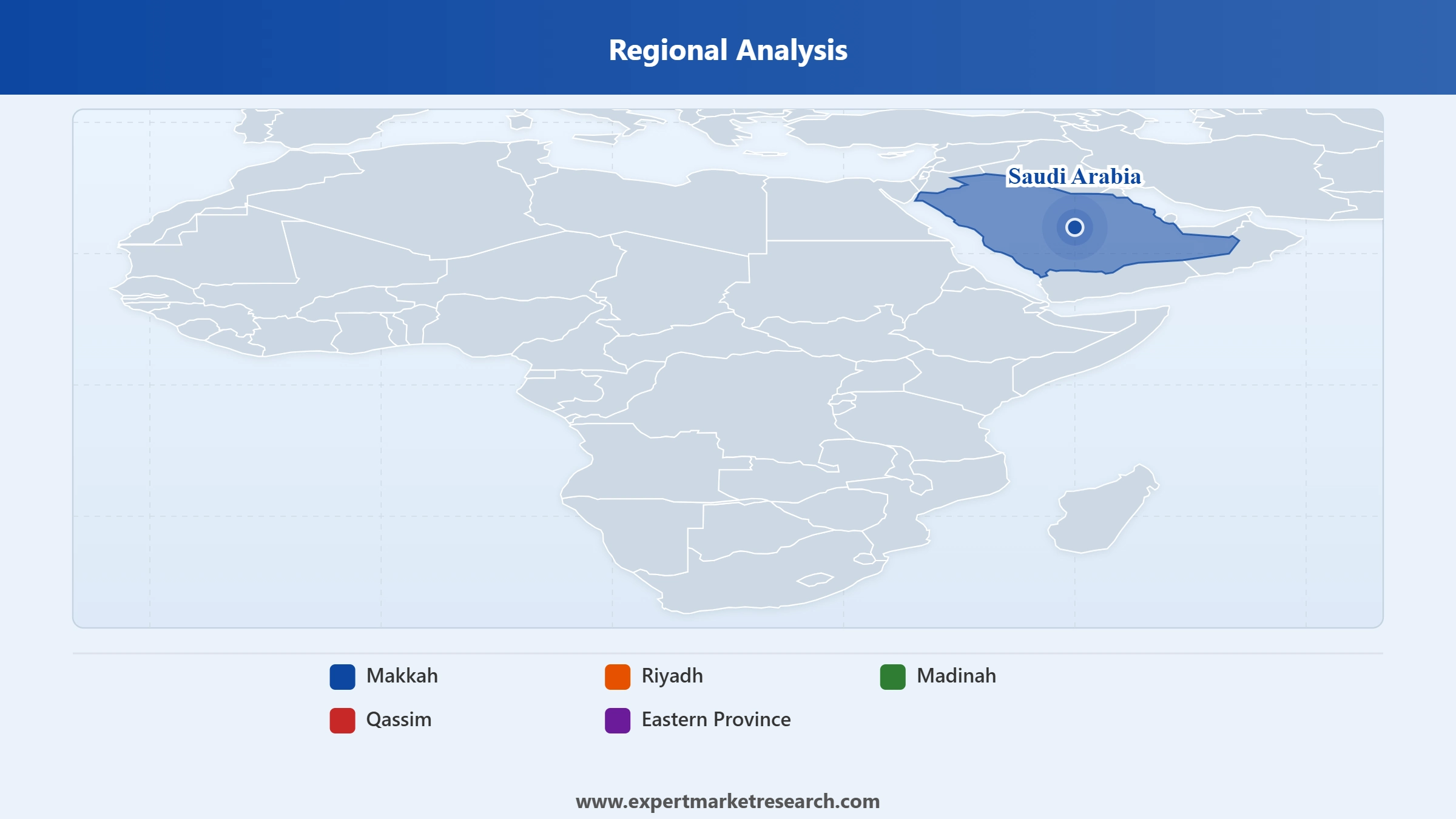

Market Breakup by Region

Key Insight: Riyadh commands the largest share of the Saudi Arabia pipes market due to its status as the political and administrative capital, its dense and rapidly growing population, and the concentration of large-scale infrastructure projects within its boundaries. The city's 2030 Smart City Blueprint has made it a testbed for intelligent pipeline systems. Makkah's pipe market is driven by the perpetual expansion of infrastructure to accommodate millions of Hajj and Umrah pilgrims annually, requiring continuous investment in water supply, sewage, and utility networks. Eastern Province is a key growth hub, anchored by the Jubail and Dammam industrial corridors, where oil and gas, petrochemical, and desalination facilities require high-specification pipe systems including large-diameter metal and specialised plastic pipe products.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Material Type, plastic pipes hold the dominant share in the Saudi Arabia pipes market, a position that has strengthened as government procurement and large-scale project specifications have increasingly favoured cost-efficient, corrosion-resistant materials over traditional metals. HDPE holds the largest share within the plastic category, accounting for over 62.9% of the PE pipes segment, driven by its widespread application in water supply, sewage, and gas distribution systems. PVC is the second-largest plastic pipe type, particularly dominant in sewerage, drainage, and residential construction, where its ease of installation and competitive cost make it the default choice for contractors and municipal utilities alike. Leading domestic players such as SAPPCO have built their market positions largely around plastic pipe manufacturing, making this sub-segment the most competitive in the broader pipes market.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Application, water and sewerage is the clear dominant application, accounting for the majority of market value and volume. The Saudi government's allocation of over USD 320 million for water infrastructure by 2030, combined with large-scale desalination projects and municipal water network expansion, creates consistent and policy-guaranteed demand for pipes in this application. Riyadh's ongoing East Riyadh Water Supply Project, which involved the installation of over 1,300 kilometres of mid-diameter thermoplastic pipes in 2023, exemplifies the scale of water and sewerage application demand in the Saudi market. Manufacturing is the fastest-growing application, with Vision 2030's industrial diversification agenda multiplying the number of factories, petrochemical facilities, and industrial processing operations that require specialized process piping, chemical transfer lines, and cooling systems.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Region, Riyadh dominates the Saudi Arabia pipes market, supported by the city's largest and fastest-growing urban population in the Kingdom, the concentration of government ministries that drive procurement decisions, and the active execution of multiple large-scale infrastructure projects. The 2024 expansion of King Salman Energy Park in the Eastern Province is creating significant additional demand for specialized industrial pipes, giving the Eastern Province a competitive second position in the market. Makkah, while smaller in total market volume, generates steady demand through perpetual religious tourism infrastructure expansion and the construction of new residential and hospitality facilities in the holy city and its surrounding areas.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Riyadh is the most dynamic market for pipes in Saudi Arabia, driven by the convergence of rapid population growth, ambitious city redevelopment plans, and a government commitment to making the capital a benchmark for smart, sustainable urban infrastructure. The 2030 Smart City Blueprint has introduced intelligent pipeline standards, including IoT-linked monitoring, automated flushing valves, and SCADA integration, making Riyadh a reference market for next-generation pipeline systems. In 2023 alone, over 1,300 kilometres of piping was installed for the East Riyadh Water Supply Project, largely using mid-diameter thermoplastic pipes. The April 2025 National Water Company desalination water delivery project, valued at SAR 400 million and serving three governorates in the Riyadh region, reinforces the ongoing scale of municipal infrastructure spending that positions Riyadh as the highest-demand region in the Saudi pipes market throughout the forecast period.

Eastern Province, anchored by the Jubail Industrial City, Dammam, and the King Salman Energy Park, represents Saudi Arabia's industrial heartland and is the fastest-growing region for high-specification pipe demand. The concentration of oil and gas production, petrochemical refining, and seawater desalination operations in this region generates consistent requirements for large-diameter metal pipes, corrosion-resistant HDPE pipes, and thermoplastic composite pipes capable of handling chemical exposure, extreme temperatures, and high-pressure transmission. The 2024 expansion of King Salman Energy Park added new industrial operations that specified durable and high-performance piping for cooling, process fluid transfer, and utility networks. As the Kingdom continues to attract new downstream and manufacturing investment into Jubail and surrounding industrial zones under Vision 2030's industrial localization agenda, Eastern Province is expected to record above-average growth in pipe consumption through 2035.

The Saudi Arabia pipes market operates within a moderately consolidated structure, with a mix of established domestic manufacturers, regional players, and select international producers serving distinct material and application segments. Domestic manufacturers benefit from proximity to construction project sites and growing government preference for locally produced materials under Vision 2030's industrial content requirements. Competitive differentiation is increasingly achieved through technical capability, product certification, and the ability to supply at the scale and specification demanded by large public infrastructure projects.

The market's competitive dynamic is shifting as government procurement increasingly favours domestic manufacturers and as leading players invest in capacity expansion and product diversification. International manufacturers with Saudi-based operations or distribution partnerships retain a competitive edge in high-specification segments such as oil and gas, where technical requirements exceed standard commercial grades. Companies that can offer complete piping system solutions, including fittings, jointing systems, and technical after-sales support, are building stronger positions in competitive public tenders.

Saudi Industries for Pipe Co., known as SIPCO, is one of the Kingdom's leading domestic pipe manufacturers, producing a broad range of plastic pipe products for water supply, sewerage, and agricultural applications. The company benefits from its established relationships with major Saudi utilities and construction contractors, enabling it to participate in large-scale public infrastructure tenders. SIPCO has built its market position around local production, competitive pricing, and compliance with Saudi standards and material specifications. Its presence in key regions including Riyadh and the Western Province allows for reliable supply chain coverage across major construction markets.

Fabco Plastic Factory is a specialist Saudi manufacturer of plastic pipe products, with a focus on PVC and HDPE pipes serving residential, commercial, and municipal applications. The company operates manufacturing facilities positioned to serve the Kingdom's construction markets and has developed a product range aligned with Saudi Standard specifications for plumbing, drainage, and water distribution systems. Fabco's competitive strength lies in its localized production capability and its ability to respond rapidly to volume orders from large construction and infrastructure contractors, which is particularly valuable during peak construction periods associated with Vision 2030 project execution.

SAPPCO is one of Saudi Arabia's most prominent plastic pipe manufacturers, with decades of presence in the Kingdom's construction and municipal infrastructure market. The company produces a comprehensive range of HDPE, PVC, and CPVC pipes serving water supply, sewerage, and industrial applications. SAPPCO's scale of operation and established brand recognition among Saudi contractors and government utilities have made it a go-to supplier for large-volume infrastructure projects. The company has been a consistent participant in major national water and sewage projects funded through government budgets, giving it a strong and recurring revenue base.

International Ductile Iron Pipes Co. Ltd is a key player in the metal pipe segment of the Saudi Arabia pipes market, specializing in the manufacture and supply of ductile iron pipes for high-pressure water transmission, sewage force mains, and industrial applications. Ductile iron pipes are specified for major water transmission mains and critical infrastructure where structural strength, pressure tolerance, and long service life are essential requirements. The company serves both government utilities and large private construction contractors, with its product range covering a wide diameter spectrum suited to municipal-scale infrastructure projects across the Kingdom.

Other key players in the market are Saudi Arabian Ductile Iron Pipes Co, Ltd (SADIP), Tenaris Saudi Steel Pipes, National Pipe Co Ltd, Welspun Corporation Limited, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Ready to understand where the Saudi Arabia pipes market is heading between 2026 and 2035? Our comprehensive report delivers current intelligence on material trends, regional demand drivers, key players, and the infrastructure projects shaping the next decade of pipe consumption across the Kingdom. Whether you are a manufacturer evaluating capacity investment, a distributor mapping regional opportunities, or an investor assessing exposure to Saudi infrastructure growth, this report provides the clarity you need. Download a free sample today and discover the opportunities in Saudi Arabia's fast-expanding pipes sector.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the Saudi Arabia pipes market reached an approximate value of USD 3469.90 Million.

The market is projected to grow at a CAGR of 5.50% between 2026 and 2035.

The market is estimated to witness healthy growth in the forecast period of 2026-2035 to reach a value of around USD 5927.09 Million by 2035.

Key strategies driving the market include localising production, integrating IoT into product lines, collaborating with EPCs for adaptive tech, and offering lifecycle analytics to meet Saudi Arabia’s ambitious urban, industrial, and ESG-linked pipe needs.

The key challenges are procurement volatility, project delays, and localisation compliance hurdles.

The major regions in the market are Makkah, Riyadh, Madinah, Qassim, and Eastern Province.

The various material types considered in the market report are plastic, steel, and concrete.

The various applications considered in the market report are water and sewerage, offices and housing, manufacture, agriculture, and others.

The diameters considered in the Saudi Arabia pipes market report are up to 50 mm, 50-100 mm, 100-200 mm, 200-400 mm, and above 400 mm.

The major players in the market are Saudi Industries for Pipe Co., Fabco Plastic Factory Co Ltd, SAPPC0, International Ductile Iron Pipes Co. Ltd, Saudi Arabian Ductile Iron Pipes Co, Ltd (SADIP), Tenaris Saudi Steel Pipes, Tenaris Saudi Steel Pipes, National Pipe Co Ltd, and Welspun Corporation Limited, among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Material Type |

|

| Breakup by Application |

|

| Breakup by Diameter |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.