Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

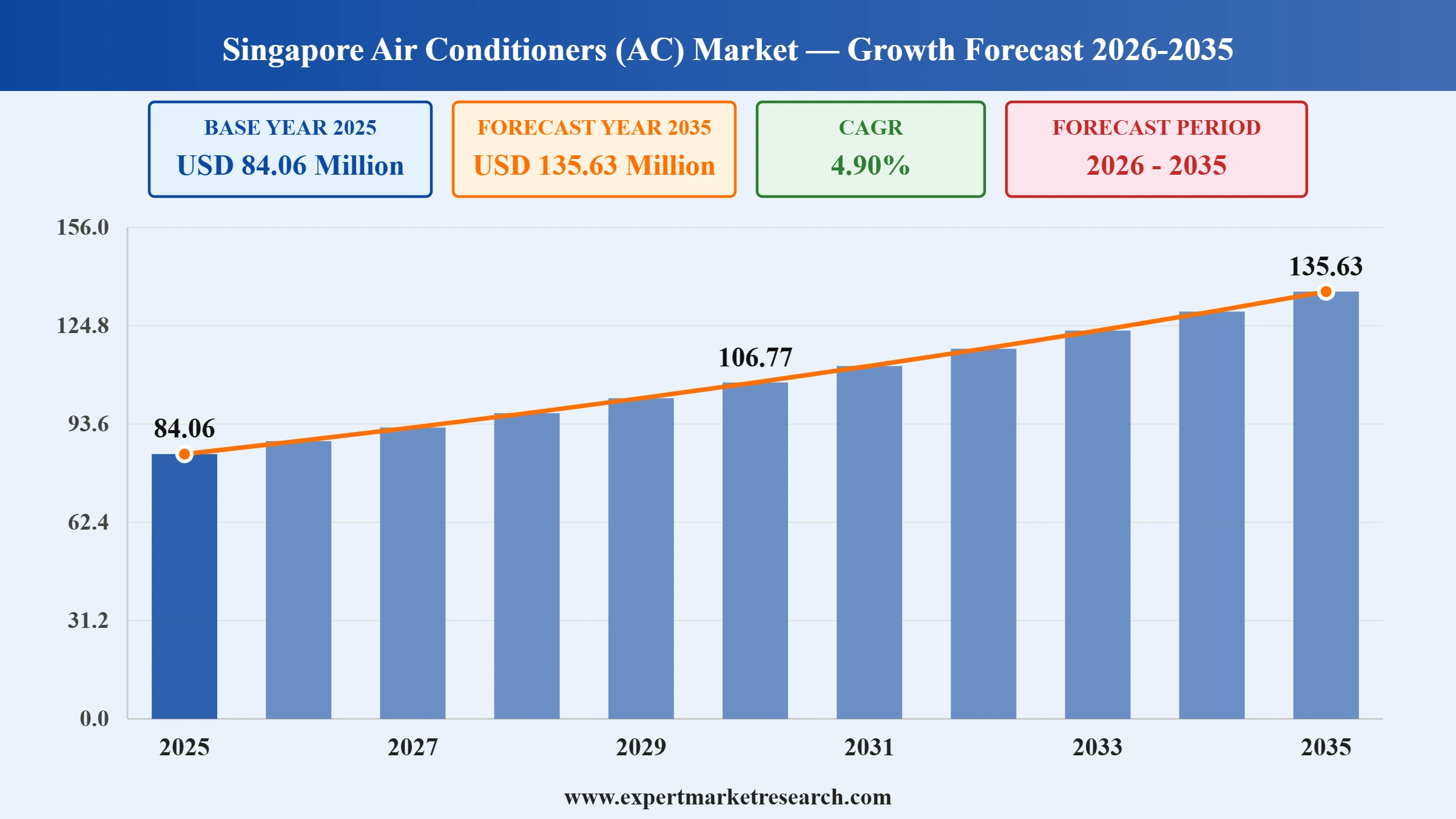

The Singapore Air Conditioners (AC) Market reached a value of USD 84.06 Million at 2025 and is projected to expand at a CAGR of around 4.90% to 2035. With rising ambient temperatures, stricter energy efficiency mandates, widening adoption of smart and inverter technologies, and government-funded consumer incentives, the market is expected to reach USD 135.63 Million by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The Singapore Air Conditioners (AC) Market reached USD 84.06 Million in 2025, underpinned by the country’s tropical climate, near-universal household penetration, and continued densification of its high-rise residential and commercial real estate. Air conditioning remains a year-round necessity rather than a seasonal appliance, and heightened heat-stress days are lengthening daily operating hours across homes, offices, retail outlets, and the hospitality sector.

A clear growth driver is the policy push toward energy efficiency. From 1 April 2025, the National Environment Agency tightened Minimum Energy Performance Standards for single-phase split-type and VRF air conditioners, while the enhanced Climate Friendly Households Programme now offers eligible HDB and private households up to SGD 400 in Climate Vouchers to offset the cost of 5-tick rated units. These interventions are accelerating the replacement cycle from older, low-efficiency equipment toward inverter-driven, Wi-Fi-enabled models, directly lifting value demand in the market even as volumes remain broadly stable.

On 27 August 2025, Panasonic R&D Center Singapore (PRDCSG) officially opened its new Innovation Hub at Punggol Digital District. Positioned as Panasonic’s flagship innovation facility for Singapore and Southeast Asia, the hub is dedicated to developing and testing AI-powered smart building technologies and robotics solutions, including next-generation climate control and indoor air quality systems relevant to the local air conditioning market.

On 23 July 2025, Midea Building Technologies Singapore held a ribbon-cutting ceremony for its new local premises, attended by over 70 partners from government agencies and enterprise clients including China Communications Construction Company, China Railway Construction Corporation, Engie, and China Telecom. The facility is intended to deepen Midea’s commercial HVAC and chiller footprint in the city-state, following its Midea Insight Building HVAC Engineering Conference earlier in the year aimed at advancing green building solutions.

On 20 June 2025, Samsung Electronics announced the launch of its new smart system air conditioner lineup for Southeast Asia and Oceania, including Singapore. The expansion emphasised the 1-Way Cassette model aimed at the residential B2C segment, combining design-forward ceiling-mounted installation with space efficiency compared with conventional wall-mounted units. The rollout followed the June 2025 introduction of the 2025 Bespoke AI appliance range across Singapore, Indonesia, Malaysia, Thailand, Philippines, and Vietnam.

KM Marketing Pte Ltd, the authorised Singapore distributor of Mitsubishi Heavy Industries, unveiled the new YYS series residential air conditioners on 3 April 2025. The range was engineered to meet the revised National Environment Agency standards effective 1 April 2025, and features enhanced maximum cooling capacity, up to 20 percent higher indoor airflow, a reinforced outdoor unit top plate, and built-in Wi-Fi for remote smartphone control. Management positioned the launch as a response to rising population-driven demand and Singapore’s environmental sustainability goals.

In April 2025, Samsung Electronics Singapore introduced its Bespoke AI appliance lineup, showcasing its “AI Home” vision. The range includes refrigerators, laundry machines, vacuum cleaners, and air conditioners that integrate AI-driven controls, intuitive touch screens, and Knox security. For air conditioners, the focus is on adaptive cooling, voice and app integration, and improved energy management tailored to the Singapore household, reflecting a broader shift toward connected, 5-tick rated residential cooling.

Effective 1 April 2025, the National Environment Agency raised the Minimum Energy Performance Standards for single-phase split-type and VRF air conditioners up to 17.6 kW cooling capacity, alongside stricter standby power limits. With suppliers given a one-year grace period until 31 March 2026, manufacturers such as Mitsubishi Heavy Industries, Daikin, and Panasonic have fast-tracked higher-tick inverter models, driving a visible premiumisation of the Singapore air conditioners market growth.

From 15 April 2025, eligible HDB households can claim an additional SGD 100 in Climate Vouchers on top of the existing SGD 300, and Singapore Citizen households living in private residential properties became eligible for the first time. Vouchers are redeemable only on 5-tick air conditioners at over 500 outlets across 150 participating retailers, accelerating replacement of older low-efficiency units and incentivising retailers to widen their 5-tick shelves.

Panasonic’s new Innovation Hub at Punggol Digital District, opened on 27 August 2025, is testing AI-powered smart building and climate control solutions, while Samsung’s Bespoke AI and smart SAC launches and Mitsubishi Heavy Industries’ built-in Wi-Fi YYS series have brought app-based remote control, occupancy sensing, and energy-usage analytics into mainstream residential ranges. This is elevating average selling prices and expanding the addressable value pool for connected cooling in Singapore.

The Centre for Climate Research Singapore’s Third National Climate Change Study projects very hot days above 35 degrees Celsius rising from about 4 per year historically to between 41 and 351 days per year by end-century, with warm nights above 26.3 degrees becoming near-continuous. Households and commercial operators are already running air conditioners for longer daily hours, reinforcing steady replacement demand and lifting premium unit penetration.

The report of the Expert Reports titled “Singapore Air Conditioners (AC) Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

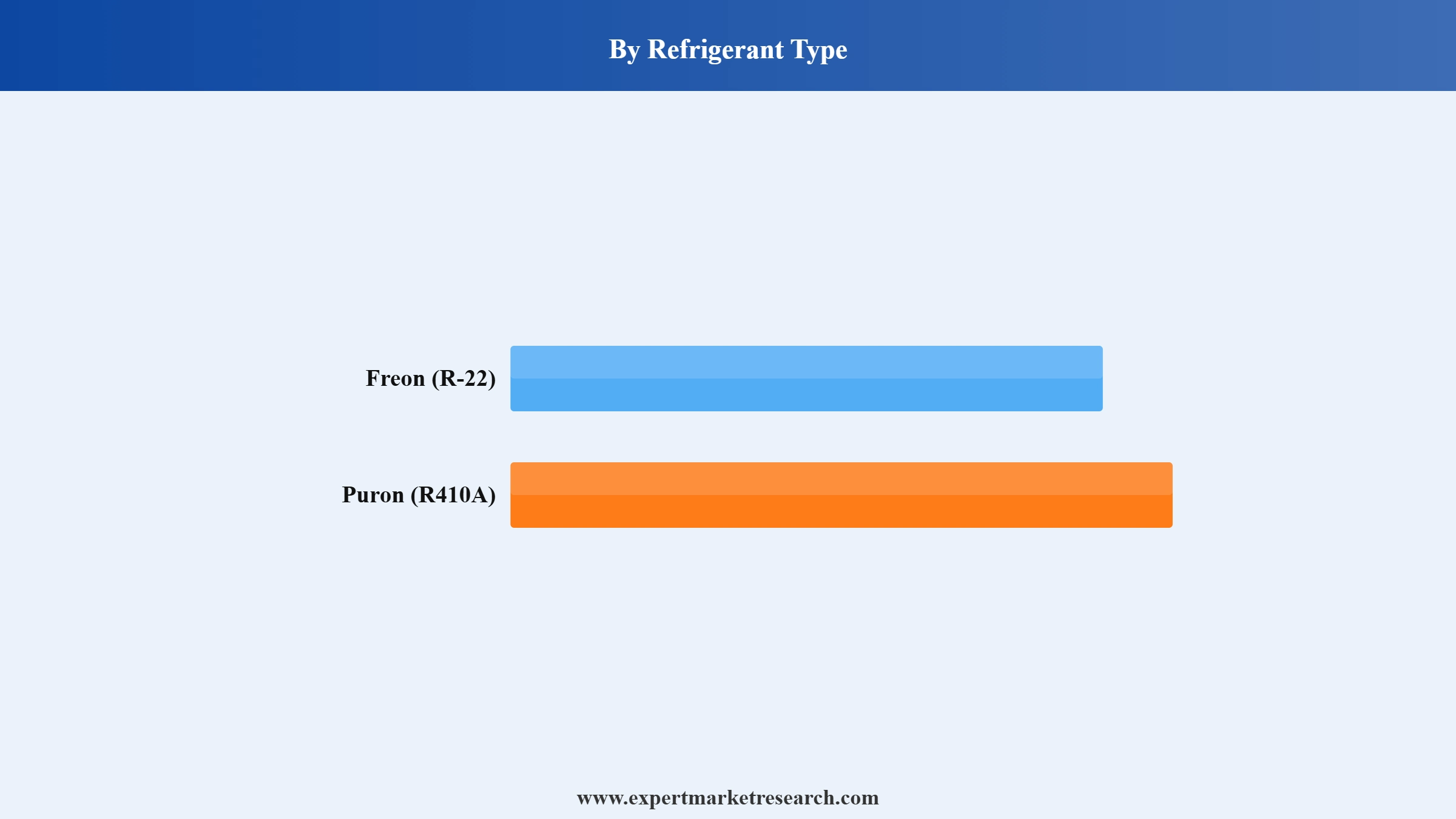

Market Breakup by Refrigerant Type

Key Insights: Puron (R410A) accounts for the bulk of new installations in Singapore, reflecting both the global phase-down of R-22 under the Montreal Protocol Kigali Amendment and the domestic preference of Daikin, Mitsubishi Electric, Panasonic, LG, and Samsung for R410A and increasingly R32 units in their imported model ranges. R-22 demand is now concentrated in servicing and spare parts for legacy stock, particularly in older HDB flats and small commercial shophouses. Rising 5-tick adoption under the Climate Vouchers scheme is further skewing the mix toward Puron and next-generation refrigerants with lower global warming potential, and manufacturers have aligned their Singapore product catalogues accordingly.

Market Breakup by Size

Key Insight: The 12K-36K BTU band dominates Singapore air conditioner demand because it aligns with the cooling load of typical HDB bedrooms and small living rooms, which account for around 80 percent of the resident housing stock. System 2 and System 3 multi-split configurations in this capacity range from Daikin, Mitsubishi Electric, Panasonic, and Midea are standard fitments in BTOs, resale flats, and condominiums. The <12K BTU segment is expanding in studio and shoebox units, while the 36K-60K BTU and 60K+ BTU ranges are concentrated in landed properties, offices, retail outlets, and hospitality spaces. Climate Vouchers, which apply only to 5-tick rated units, are pulling consumer preference upward within each band.

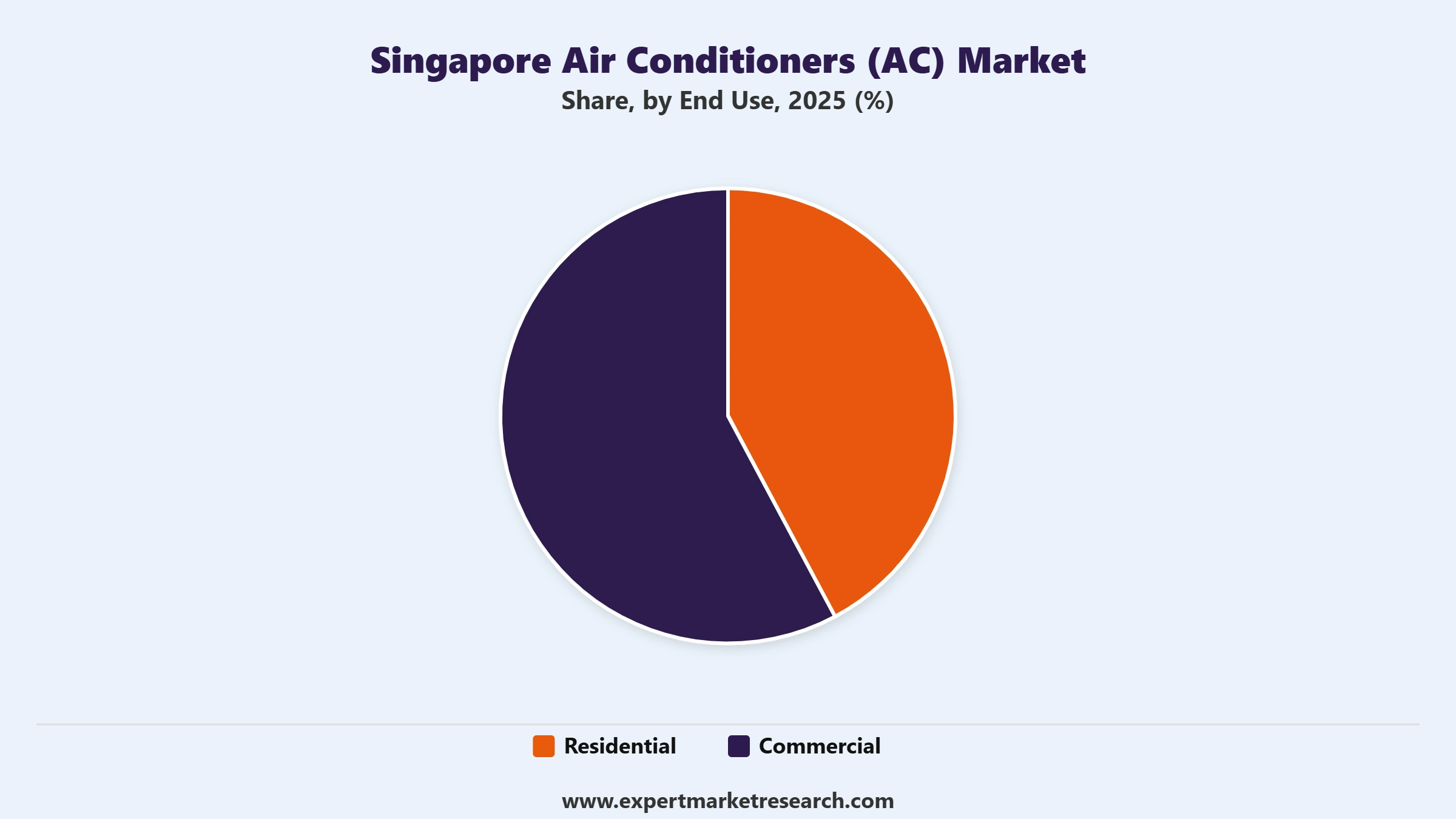

Market Breakup by End Use

Key Insight: Residential applications account for a substantial share of the Singapore air conditioners market given year-round hot and humid conditions, high-rise living, and near-universal household penetration. Multi-split and single-split units from Daikin, Mitsubishi Electric, Panasonic, LG, Samsung, and Midea dominate this segment, with multi-split System 2 to System 4 configurations especially popular for HDB and condominium use. The commercial segment, including Precision Air Conditioners for data centres and Mini or Maxi VRV systems for offices, retail, hospitality, and healthcare, is growing steadily. Midea’s July 2025 Building Technologies Singapore launch and Johnson Controls-Hitachi’s VRF offerings underpin this institutional pipeline.

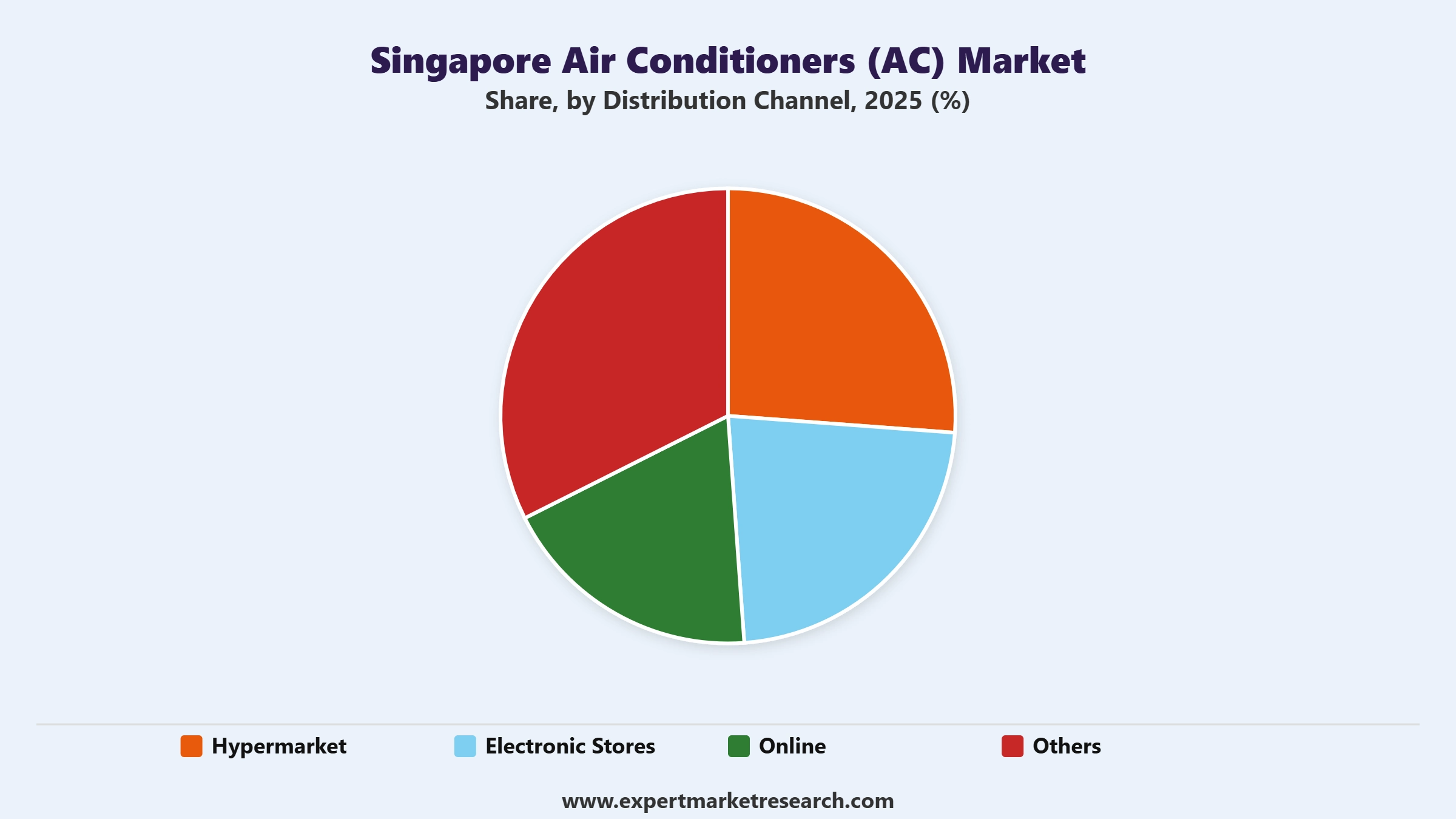

Market Breakup by Distribution Channel

Key Insight: Electronic stores, including Gain City, Courts, Harvey Norman, Best Denki, and Mega Discount Store, account for a significant share of the Singapore air conditioners market because consumers place high value on physical inspection, expert advice, professional BCA-certified installation, bundled warranty packages, and post-sales service for a long-life appliance. Online channels, via brand websites, Shopee, Lazada, and retailer e-commerce platforms, are the fastest-growing route, benefiting from transparent pricing, product reviews, and Climate Voucher redemption integrations. Hypermarkets and appliance chains round out the channel mix, while “Others” covers direct B2B sales by commercial installers such as KM Marketing for MHI and Midea Building Technologies for institutional projects.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Refrigerant Type

Puron (R410A) holds the dominant share within the refrigerant type segmentation because all new split and multi-split residential units imported into Singapore by Daikin, Mitsubishi Electric, Panasonic, LG, Samsung, and Midea now use R410A or the newer R32, while R-22 equipment has not been imported in new models for several years as part of Singapore’s commitments under the Montreal Protocol Kigali Amendment. Freon (R-22) demand is largely confined to servicing an ageing installed base in older HDB blocks. Following the NEA’s April 2025 MEPS revisions, distributors such as KM Marketing accelerated rollouts of Puron-based inverter ranges, reinforcing the dominant share of R410A and next-generation refrigerants in the Singapore market.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By End Use

Residential end-use commands the leading share of the Singapore air conditioners market, reflecting a city-state where the Energy Market Authority and industry data indicate that the overwhelming majority of households rely on installed air conditioning for daily comfort. Multi-split System 2 to System 4 units from Daikin’s iSmile Eco and Mitsubishi Electric’s Starmex series, Panasonic’s Premium XU, and LG and Samsung inverter ranges, dominate HDB and condominium installations. The April 2025 extension of Climate Vouchers to private-property households and the additional SGD 100 top-up have further tilted residential demand toward 5-tick rated models, supporting the segment’s dominance in both volume and value terms.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Distribution Channel

Electronic stores are the dominant distribution channel in Singapore air conditioners sales, as they bundle product selection, on-site advice, installation subcontracting, and extended warranty management under one roof. Chains such as Gain City, Courts, Harvey Norman, and Best Denki host the full Daikin, Mitsubishi Electric, Panasonic, LG, and Samsung catalogues, and have integrated Climate Voucher redemption since April 2025, converting the SGD 400 subsidy into immediate shelf traffic. Online channels are the second most important and fastest-growing route, with brand sites and marketplace listings offering 5-tick filters, tick-rating comparison tools, and same-week BCA-certified installation slots, making them particularly attractive to tech-savvy buyers in the 25 to 45 age cohort.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Central Region

The Central Region is the single largest value contributor to the Singapore air conditioners market, anchored by the Central Business District, Orchard Road, Marina Bay, and Bugis commercial corridors. Continuous investment in Grade A offices, integrated resorts, hospitals, and the five-star hotel pipeline sustains demand for Mini VRV, Maxi VRV, and Precision Air Conditioners from Daikin, Mitsubishi Electric, Panasonic, Johnson Controls-Hitachi, and Midea Building Technologies, whose new Singapore hub opened in July 2025. The Energy Efficiency Grant providing up to 70 percent co-funding for SMEs and 30 percent for non-SMEs under pre-approved Daikin systems is further accelerating retrofit demand from food and beverage, retail, and small-office tenants concentrated in this region.

North-East Region

The North-East Region, covering fast-growing HDB townships such as Punggol, Sengkang, Hougang, and Ang Mo Kio, is a major residential volume contributor. Successive BTO completions and en-bloc renewals have created a steady pipeline of new-build and replacement air conditioner installations, dominated by multi-split System 2 to System 4 units from Daikin, Mitsubishi Electric, Panasonic, LG, Samsung, and Midea. Panasonic’s 27 August 2025 opening of its Innovation Hub at Punggol Digital District illustrates how integrated commercial-residential districts are converging demand for smart, AI-enabled cooling. Rising heat-stress readings, including the 37 degrees Celsius peak recorded in Ang Mo Kio in 2023, continue to reinforce year-round operating demand across this region.

The Singapore air conditioners market is moderately consolidated, with a small group of Japanese and Korean original equipment manufacturers controlling the majority of residential and light commercial value share, while Chinese challengers such as Midea and niche local distributors compete aggressively on price and warranty. Competitive priorities centre on 5-tick energy efficiency, Wi-Fi and AI-enabled smart controls, quiet inverter operation, and nationwide BCA-certified installation networks.

Product differentiation increasingly depends on compliance with the 1 April 2025 NEA MEPS revisions, participation in the Climate Vouchers ecosystem, and alignment with Singapore’s Green Plan 2030. Leading suppliers are deepening local R&D, service, and training footprints through facilities such as Panasonic’s Punggol Innovation Hub and Midea Building Technologies Singapore, while distributors such as KM Marketing drive launch momentum for MHI and other specialist brands.

Founded in 1924 and headquartered in Osaka, Japan, Daikin Industries Ltd. is the world’s largest dedicated air conditioning manufacturer. In Singapore it has operated for over 50 years, offering single-split, multi-split, and VRV system ranges for HDB, condominium, commercial, and industrial applications, and provides pre-approved systems under the Energy Efficiency Grant. Its iSmile Eco series remains a benchmark in the 5-tick residential category.

Incorporated in 1921 and headquartered in Tokyo, Japan, Mitsubishi Electric Corporation is a diversified electronics and systems group whose Starmex series is among the most widely specified residential air conditioners in Singapore. Its portfolio spans inverter-based single-split, multi-split, and VRF systems, with strong penetration among HDB upgraders and a dense islandwide installer network.

Incorporated in 1918 and based in Osaka, Japan, Panasonic Corporation operates across Automotive, Lifestyle, Industry, Connect, and Energy segments. In Singapore, its air conditioning range features nanoe X air purification and inverter efficiency, and in August 2025 it opened its flagship Innovation Hub at Punggol Digital District to develop AI-powered smart building and climate control technologies for Singapore and Southeast Asia.

Founded in 1958 and headquartered in Seoul, South Korea, LG Electronics Inc. is a global home appliance and electronics leader. Its 2026 inverter aircon lineup for Singapore emphasises the ThinQ AI platform, smart home integration, and energy-efficient 5-tick models. LG operates an extensive Singapore sales and service network, and has reinforced its presence through its first LG Subscribe brand store.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Other key players in the Singapore Air Conditioners (AC) Market include Samsung Electronics Co., Ltd., Midea Group Co. Ltd., Johnson Controls – Hitachi Air Conditioning Company, Prism Tech Private Limited, Strategic Marketing (S) Pte Ltd, and Others.

Unlock the most recent intelligence on the Singapore Air Conditioners (AC) Market 2026 with our in-depth report. Stay ahead of shifting consumer preferences, regulatory changes, and technology disruption with authoritative data on product launches, end-user demand, and the highest-growth segments. Whether you are launching a new 5-tick model, expanding a VRV commercial offering, or reviewing distribution strategy, this report equips you with the clarity to decide. Request your free sample now and uncover the key opportunities shaping Singapore Air Conditioners (AC).

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market reached an approximate value of USD 84.06 Million.

The market is projected to grow at a CAGR of 4.90% between 2026 and 2035.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035, reaching a value of around USD 135.63 Million by 2035.

The major market drivers are the rise in disposable income, a shift in consumer preference towards enhanced comfort, and year-round warm and humid climate in Singapore.

The key trends of the market include the growing integration of remote-control apps of ACs with smartphones and other smart devices, the burgeoning popularity of ACs with in-built air filters, and favourable government incentives that promote energy-efficient systems in buildings.

Different refrigerant types are Freon (R-22) and Puron (R410A).

Various sizes are <12K BTU, 12K-36K BTU, 36K-60K BTU, and 60K+ BTU, among others.

The key players in the market are Daikin Industries Ltd., Mitsubishi Electric Corporation, Panasonic Corporation, LG Electronics Inc., Samsung Electronics Co., Ltd., Midea Group Co. Ltd., Johnson Controls - Hitachi Air Conditioning Company, Prism Tech Private Limited, and Strategic Marketing (S) Pte Ltd, among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Refrigerant Type |

|

| Breakup by Size |

|

| Breakup by End Use |

|

| Breakup by Distribution Channel |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.