Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

The global solar central inverters market attained a value of USD 10.52 Billion in 2025 and is projected to expand at a CAGR of 7.90% through 2035. The market is further expected to achieve USD 22.50 Billion by 2035. Increased utility-scale solar farms and renewable hybrid systems are increasing the need for powerful grid-friendly central inverters equipped with predictive maintenance and advanced thermal management in industry-wide energy infrastructure applications.

Sungrow and Huawei retained their AAA ratings in the latest PV InverterTech bankability assessment, jointly holding above 50% of global inverter market share and dominating the Wood Mackenzie 2025 manufacturer ranking with scores of 93.9 and 93.7. SMA Solar's distress-zone Altman-Z score and ongoing EU and US scrutiny of Chinese imports are reshaping competitive bidding for utility-scale tenders, PV-Tech reported.

Huawei Digital Power introduced its FusionSolar 9.0 Smart PV Solution headlined by the SUN2000-506K smart string high-power inverter and a new 11 MW PV array configuration, the largest in the industry. The platform incorporates the first kV AC architecture and grid-forming smart string capabilities, designed for utility-scale and commercial projects in markets with high renewable penetration, as detailed in Solar Power World coverage.

Factors that are boosting growth in the solar central inverters market include increased adoption of solar-plus-storage installations needing smart grid integration solutions. Utilities are seeking inverters that can manage variable energy flows from renewables while keeping the frequency of power grid systems constant during peak hours of use. In addition, companies are working on developing energy-efficient inverters made of silicon carbide semiconductor technology and using liquid cooling methods to prevent overheating of devices in desert regions. The other factor driving the market is the increasing trend of inverter manufacturing domestically in the United States, India, and Europe as part of national efforts.

The global solar central inverters market is experiencing an aggressive technological transition with the need for high conversion efficiency, reduced maintenance intervals, and grid support capability for large-scale PV power plants. For example, in April 2025, Sungrow Power Supply Co., Ltd. released its latest 1+X modular central inverter platform with AI-based fault detection capabilities, specifically designed for large-scale solar farms in deserts and hot areas. The introduction was announced amid a sharp rise in utility-scale solar additions within the Asia Pacific and Middle East regions, where grid administrators prefer the use of centralized inverter systems.

The trend towards grid modernization and integration of hybrid renewables further drive changes in the solar central inverters market. Leading vendors are investing in next-gen grid-forming inverters that can handle voltage regulation and frequency response requirements in weak grid areas. Vendors such as Huawei Technologies Co., Ltd. and FIMER S.p.A. are targeting utility companies by offering liquid-cooled inverter systems and prefabricated inverter stations for quick deployment. Some manufacturers are incorporating cybersecurity protection and predictive maintenance modules in their inverter solutions. For example, in March 2026, onsemi partnered with Sineng Electric, enhancing solar inverters and energy storage systems with advanced high-efficiency semiconductor power modules.

Compound Annual Growth Rate

7.9%

Value in USD Billion

2026-2035

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

| Global Solar Central Inverters Market Report Summary | Description | Value |

| Base Year | USD Billion | 2025 |

| Historical Period | USD Billion | 2019-2025 |

| Forecast Period | USD Billion | 2026-2035 |

| Market Size 2025 | USD Billion | 10.52 |

| Market Size 2035 | USD Billion | 22.50 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 7.90% |

| CAGR 2026-2035 - Market by Region | Asia Pacific | 17.4% |

| CAGR 2026-2035 - Market by Country | India | 19.9% |

| CAGR 2026-2035 - Market by Country | USA | 10.9% |

| CAGR 2026-2035 - Market by Source | Utility | 14.7% |

| Market Share by Country 2025 | Japan | 5.7% |

Fujiyama Power Systems opened up a plant producing solar panels at a capacity of 2 GW in India, increasing domestic production capability in renewable energy equipment. Such developments provide opportunities for inverter suppliers to develop their integrated solutions in line with growing utility-scale solar projects.

The acquisition of Zigor and Apex Power inverter assets by NextPower UK ESG increased technological capability and market position within the renewable energy equipment industry. Such mergers encourage organizations in the solar central inverters market to look into strategic alliances and acquisitions for their inverter technology portfolio.

Delta Electronics released an innovative 1.1 MW central inverter, allowing greater flexibility, efficiency, and scalability for use in large solar panel systems. This development is expected to create a chance for competitors to create modular inverters for large-scale solar energy systems that require such capabilities.

Ingeteam unveiled a 5.4 MW capacity central inverter technology. Such developments in the solar central inverters market prompt companies to consider high-power central inverter designs that would address the challenge of integrating renewable energy sources into power grids.

In the current market scenario, companies are incorporating artificial intelligence into solar central inverters to compete based on their ability to reduce maintenance expenses and improve plant availability. These devices are embedding predictive analytics software that identifies potential thermal stress, voltage instability, and part degradation prior to failure, reshaping the solar central inverters market dynamics. In February 2026, India advanced AI-integrated solar technologies, improving predictive analytics, smart grids, renewable optimization, and energy infrastructure resilience across the nation. Grid managers are further inclined toward adopting predictive maintenance models due to the substantial influence of unexpected inverter downtimes on power generation capacity in multi-gigawatt projects.

There is a growing trend in the solar central inverters market toward constructing hybrid renewable energy plants, increasing the need for central inverters designed to integrate battery storage systems with utility-scale photovoltaic plants. The developers now demand central inverters that enable dynamic load balancing, grid stability management, and efficient battery integration capabilities. Aligning with this trend, in April 2026, Huawei launched FusionSolar9.0 Smart PV solutions, enhancing AI-driven grid stability, inverter efficiency, and lifecycle optimization across Asia Pacific renewable energy projects.

Policies on domestic manufacturing are expected to transform the procurement process in the market due to the national efforts to become self-reliant in regard to energy equipment. The United States, India, and European nations are promoting local inverter manufacturing using subsidies, tax reductions, and renewable manufacturing incentives. For example, in June 2024, Gamesa Electric supplied 245 MW Proteus solar inverters to Repsol, enhancing Spain’s large-scale renewable energy infrastructure efficiency. India's Production Linked Incentives are also inspiring suppliers to manufacture inverters locally, impacting the solar central inverters market value.

The growing trend in the adoption of liquid cooled central inverter designs is evident among utility-scale operators in high temperature zones. Air cooled inverter designs usually suffer performance challenges when used in areas where the weather is extremely harsh, especially in desert areas in both the Middle East and North African countries. Governments of all Gulf nations are implementing plans for utility scale solar development projects, thereby propelling demand in the solar central inverters market. In November 2025, Sungrow unveiled liquid-cooled inverters and energy storage systems, improving thermal efficiency, grid reliability, and large-scale renewable energy performance.

Grid-forming capability is emerging as a significant technological trend, gaining increasing prominence as higher volumes of renewable energy are integrated into electricity grids across the world. Utility companies are looking for central inverters from solar energy that can help support functions such as voltage regulation, inertial response, and frequency regulation, which were previously performed by fossil-based power stations. In April 2025, Hitachi launched grid-forming inverter microgrid systems, enhancing renewable integration, energy resilience, and emergency backup power reliability, thereby propelling growth in the market.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The Expert Market Research's report titled “Global Solar Central Inverters Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

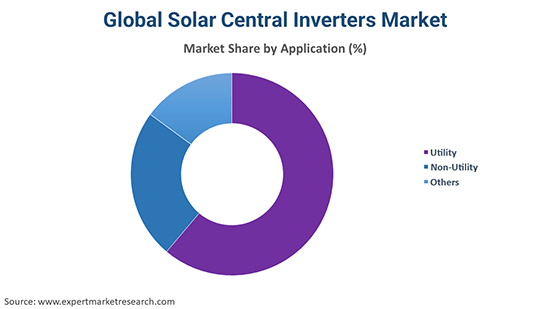

Market Breakup by Application

Key Insight: The utility-scale applications keep dominating the solar central inverters market as government agencies and energy companies are aggressively investing in PV plants that necessitate the efficient conversion of power at one location. Commercial and industrial investments keep growing as businesses explore ways of reducing their costs of operations while remaining energy self-sufficient. The residential market is growing at a steady pace as there is an inclination towards using string inverters.

Market Breakup by Region

Key Insight: The leadership of Asia Pacific in the solar central inverters market is led by the robustness of its manufacturing industries, governmental plans aimed at expanding renewables, and constant utility-scale installations of solar energy sources. The development of solar plus storage technology and the upgradation of renewable grid infrastructure are boosting North America’s performance. For instance, in August 2025, SMA launched Sunny Central Storage UP-S inverter, improving grid stability, storage efficiency, and utility-scale renewable energy integration capabilities. In Europe, attention is being paid to the inverter grid structures, which can help create sustainable renewable energy-based power generation systems. Latin America and Middle East regions are able to attract investments due to competitive solar auction deals and improved grid infrastructure.

By end use, utility-scale projects register the largest share of the market due to massive solar farm deployments

Central inverters dominate the overall solar central inverters market revenue, powered by utility-scale installations owing to the high efficiency of centralized technology in managing large-scale photovoltaic farms, which require grid-level energy management. The multi-megawatt scale solar farms use central inverters because of the ease of maintenance, high efficiency, and low balance-of-system costs. Utility-scale project approvals are continuing in China, the United States, India, and the Middle East due to government renewable targets. For example, in May 2026, in India, Jitendra Singh inaugurated CEL’s 200 MW solar module manufacturing line, strengthening India’s renewable energy manufacturing and clean energy infrastructure.

Commercial and industrial installations are expected to be the fastest growing application segment, driven by the growth in renewable energy purchases at manufacturing units, logistics parks, and data centers. Industrial customers are increasingly installing medium-scale solar installations with central inverters in order to effectively manage energy-intensive processes. Central inverters that support battery storage and energy management are preferred by companies with industrial campuses.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Asia Pacific secures the leading position of the market due to aggressive utility-scale solar infrastructure expansion initiatives

Asia Pacific leads the solar central inverters market revenue growth owing to widespread utility-scale renewable energy installation in China, India, and Southeast Asian countries. The authorities in all these nations are focusing on enhancing solar infrastructure to ensure energy security and reduce the consumption of fossil fuels. Chinese manufacturers are also increasing manufacturing capabilities for central inverter systems suitable for large photovoltaic parks. For example, in May 2026, Chinese solar manufacturers expanded high-efficiency module production, supporting utility-scale projects, advanced inverter integration, and accelerating renewable infrastructure deployment.

The Middle East and Africa region emerges as the fastest-growing solar central inverters market due to growing investment in large solar projects in the desert areas. Countries like Saudi Arabia and the United Arab Emirates are working hard to increase utility-scale renewable energy capacity in order to diversify their energy sources and avoid relying too much on hydrocarbons. Liquid-cooled central inverter systems that can withstand harsh weather conditions are preferred in the Middle East and Africa regions.

The market is witnessing increasing competition due to the emphasis on intelligent grid support technology, liquid cooling systems, and AI-based predictive maintenance technology. Significant investments are being directed toward manufacturing higher-capacity inverter models designed specifically for utility-scale solar plants and hybrid solar parks integrated with battery storage systems. Partnerships between the solar central inverters market players and EPCs, battery pack suppliers, and digital energy management system vendors are being formed in order to secure long term pipeline projects.

Regional manufacturing units are being established by some vendors due to domestic procurement requirement norms in countries such as United States, India, and Europe. Growing interest in desert-specific solar inverters is driving development efforts toward highly thermally stable inverter systems with enhanced dust-resistant features. Energy optimization platform using software technology is an important differentiator for solar central inverter companies where power electronics can be combined with intelligent energy management capabilities.

ABB Ltd. was incorporated in 1988 in Zurich, Switzerland. It is a multinational corporation dealing in the provision of electricity technologies. The company is involved in the production of central inverters, power-grid integration systems, energy management platforms, as well as utility-scale solar systems.

Delta Electronics Inc. was incorporated in 1971 in Taipei, Taiwan. It is an international business organization involved in the development of power electronics and renewable energy products. The company develops solar central inverters, energy storage systems, EV chargers, and automation technologies. Delta provides utility-scale solar systems in global markets using highly efficient inverter systems.

Ingeteam S.A., a Spanish firm, established in 1972, offers various services including power conversion systems, renewable energy technologies, and industrial electrical products. Some of the solar solutions offered by Ingeteam S.A. to the photovoltaic plant operators globally include central solar inverters, power stations, monitoring software and integration systems for energy storage.

Sungrow Power Supply Co., Ltd. is one of the world’s largest providers of solar inverter technology, which was founded in 1997 and has its headquarters in Hefei, China. Sungrow Power Supply Co., Ltd. manufactures solar inverters, energy storage systems, floating solar power generation equipment, and management systems for renewable energy. Over 150 nations have been served by Sungrow’s solar products that offer features such as AI-based energy management systems and liquid-cooled inverter systems.

Other key players in the market include SMA Solar Technology AG, among others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Unlock the latest insights with our solar central inverters market trends 2026 report. Discover regional growth patterns, consumer preferences, and key industry players. Stay ahead of competition with trusted data and expert analysis. Download your free sample report today and drive informed decisions in the market.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

The market is projected to grow at a CAGR of 7.90% between 2026 and 2035.

The major drivers of the market include the increasing usage of renewable energy sources, increasing investments in renewable energy, continuous infrastructural development, rising demand for 24*7 electricity supply, increasing greenhouse gas effect, rising environmental issues, and rapid urbanisation.

An increasing adoption of clean energy technologies and increasing public assistance and investments are the key industry trends propelling the market's growth.

The major regions in the industry are North America, Latin America, the Middle East and Africa, Europe, and the Asia Pacific.

Solar central inverters find their major application in utility and non-utility, among others.

The major players in the industry are ABB Ltd., Delta Electronics Inc., Ingeteam Corp. SA, SMA Solar Technology AG, and Sungrow Power Supply Co. Ltd., among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Application |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

| Report Price and Purchase Option | Explore our purchase options that are best suited to your resources and industry needs. |

| Delivery Format | Delivered as an attached PDF and Excel through email, with an option of receiving an editable PPT, according to the purchase option. |

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.