Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

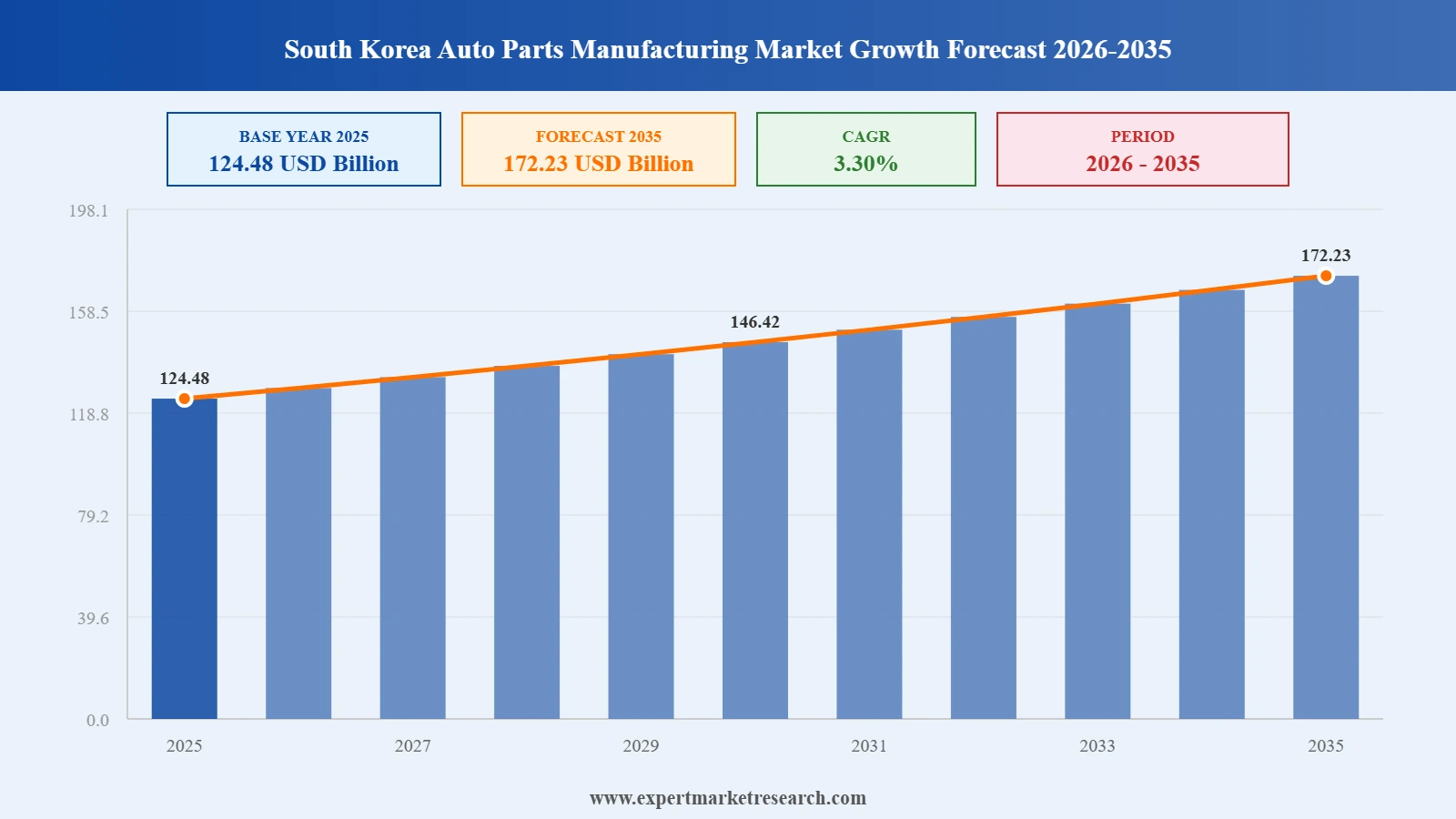

The South Korea auto parts manufacturing market reached a value of USD 124.48 Billion in 2025 and is projected to expand at a CAGR of around 3.30% during the forecast period of 2026-2035. Hyundai Motor Group's landmark USD 86.5 Billion domestic investment plan (2026-2030), South Korea's EV transition driving pivot from ICE to electric drivetrain components, Robert Bosch Korea's KRW 200 Billion Daejeon factory investment, and Hyundai Motor Group's KRW 24.3 Trillion 2025 domestic investment are driving South Korea auto parts manufacturing market growth. The market is expected to reach USD 172.23 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The South Korea auto parts manufacturing market is driven by Hyundai Motor Group's record domestic investment commitment, the EV transition requiring retooling from ICE to electric drivetrain components, Bosch Korea factory expansion, the US tariff environment redirecting Korean auto parts strategies, and AI-enabled manufacturing automation investment from Hyundai and global tier-1 suppliers.

Hyundai Motor Group announced a landmark USD 86.5 Billion domestic investment plan for South Korea on November 2025, covering the 2026-2030 period. The plan includes USD 86.5 Billion in EV capacity, AI manufacturing, robotics, and supply chain support for tier-1 to tier-3 Korean auto parts suppliers. Hyundai committed to covering all US tariff costs incurred by tier-1 suppliers in 2025 and developing new support programmes for tier-2 and tier-3 auto parts manufacturers to stabilise the domestic supply chain.

South Korea's electric vehicle sales growth in 2025 accelerated the auto parts manufacturing industry's pivot from internal combustion engine components to EV battery systems, electric motors, power electronics, and advanced thermal management components. Korean auto parts manufacturers are retooling production lines from ICE-specific components such as exhaust, transmission, and fuel injection parts toward EV-compatible battery packs, power inverters, and high-voltage wiring harnesses in collaboration with LG Energy Solution, Samsung SDI, and SK On.

Robert Bosch GmbH's Korean subsidiary invested KRW 200 Billion (approximately USD 178.5 Million) in its Daejeon factory in 2025 to establish a new gasoline engine parts production line targeting Hyundai Motor, Kia, and Genesis. The investment reinforces South Korea's role as a strategic auto parts manufacturing hub for Bosch's Asia Pacific supply chain.

Hyundai Motor Group announced its 2025 domestic South Korea investment plan of KRW 24.3 Trillion (approximately USD 17 Billion) in January 2025, the largest ever annual investment commitment by the group. The investment targets electric vehicles, software-defined vehicles, hydrogen vehicles, and autonomous vehicle technology, with significant funds allocated to Hyundai Mobis auto parts integration and advanced manufacturing capacity at Korean plants supporting Hyundai Motor and Kia export production.

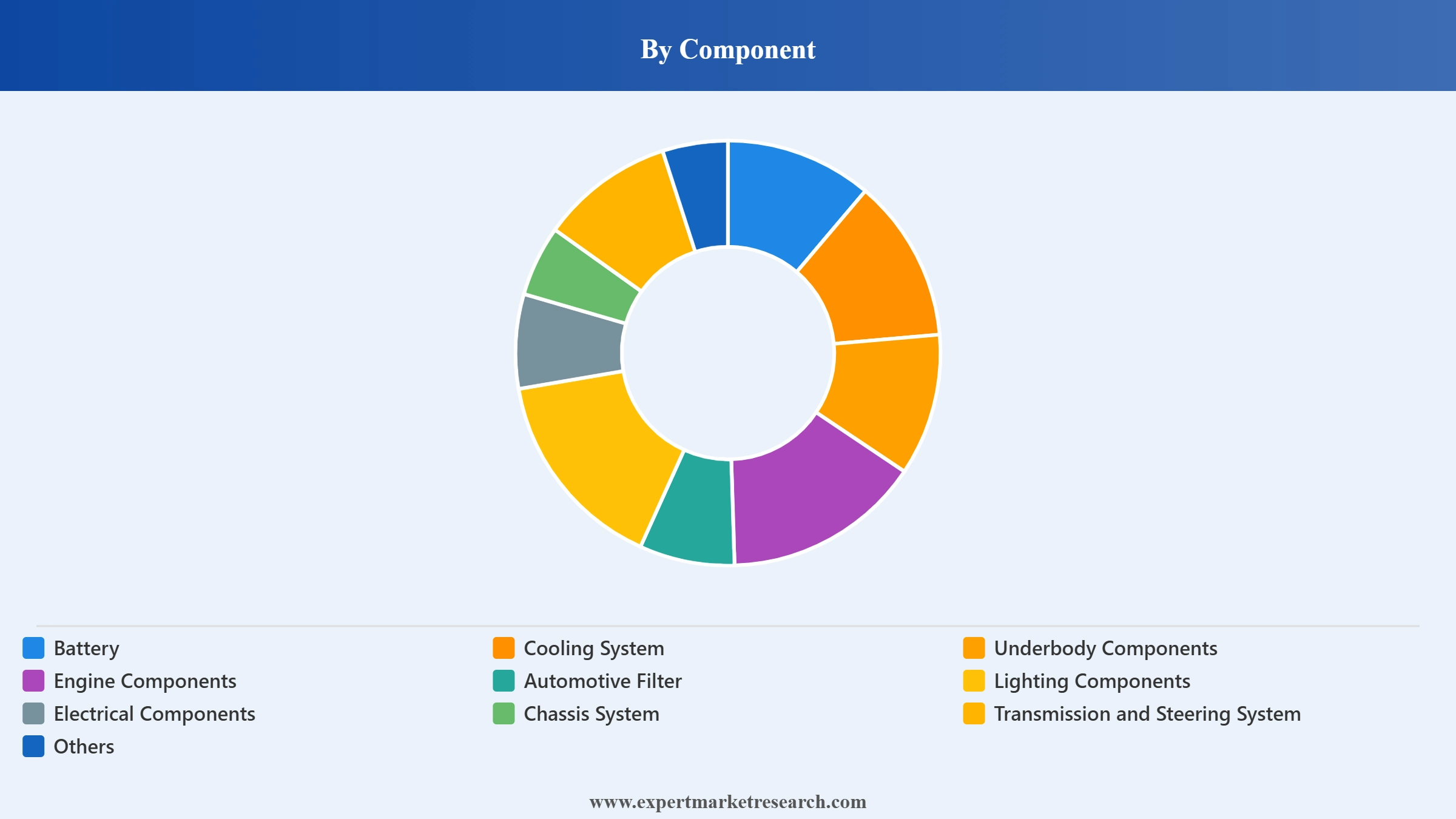

Battery is the fastest-growing South Korea auto parts component through EV adoption. Engine Components are the largest traditional ICE segment. Cooling System is significant through thermal management for both ICE and EV vehicles. Electrical Components are growing through vehicle electrification. Transmission and Steering System are significant through ICE and hybrid applications.

Engine Components including starter, alternator, and pump are significant South Korea auto parts through the established ICE vehicle fleet. Underbody Components including brake and exhaust are significant. Chassis System serves both ICE and EV platforms. Automotive Filter is significant through replacement demand for South Korea's large ICE vehicle aftermarket.

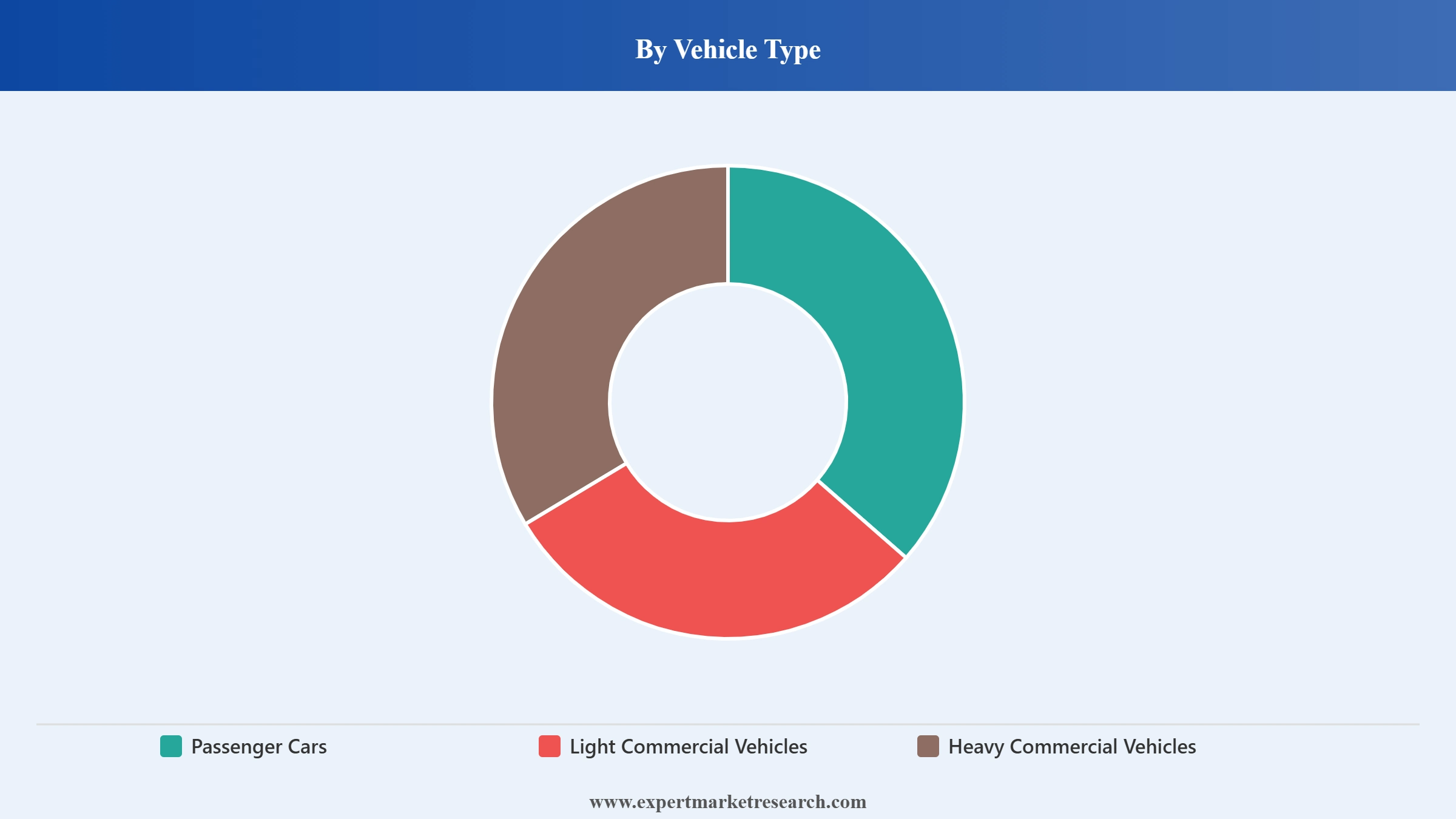

Passenger Cars are the dominant South Korea auto parts vehicle type through Hyundai Motor and Kia Corporation production scale. Light Commercial Vehicles are significant through delivery and logistics fleet demand. Heavy Commercial Vehicles are significant through Hyundai Truck, Kia Cargo, and Daewoo Trucks domestic and export production.

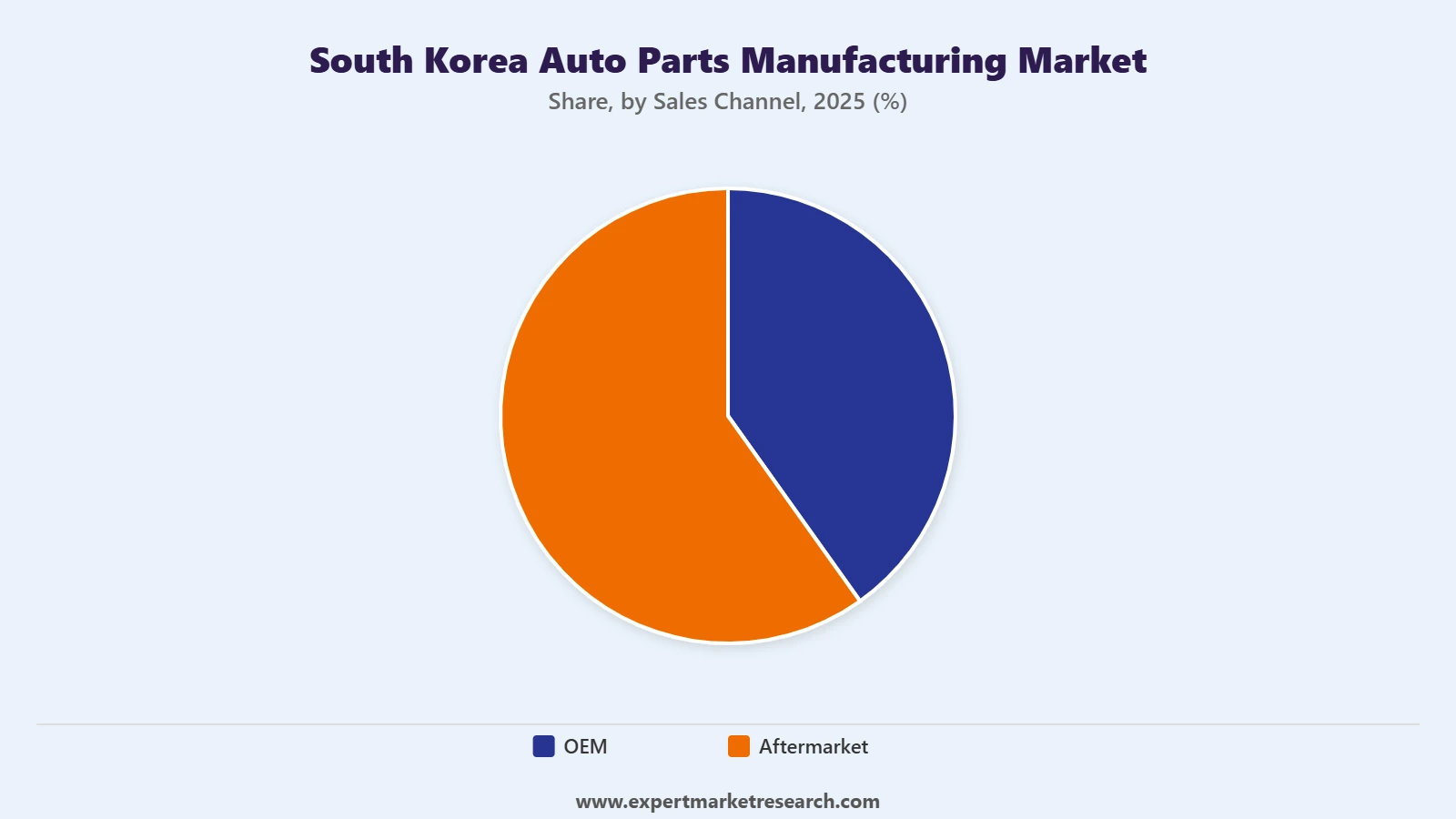

OEM is the dominant South Korea auto parts sales channel through Hyundai Motor, Kia, and Genesis direct procurement from tier-1 manufacturers including Hyundai Mobis, Bosch Korea, Denso Korea, and Valeo Korea. Aftermarket is significant through Korea's large in-service vehicle fleet requiring replacement parts through authorised dealers and independent service centres.

The Asia Pacific auto parts manufacturing market provides the broader supply chain and competitive context for South Korea's industry. South Korean auto parts manufacturers export to Japan, China, ASEAN, India, and North America as both OEM-integrated tier-1 suppliers and independent aftermarket distributors. South Korea accounts for a significant share of Asia Pacific auto parts manufacturing through Hyundai Mobis and domestic tier-2 supplier networks.

“South Korea Auto Parts Manufacturing Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

Market Breakup by Component

Key Insight: Battery is fastest-growing through EV adoption. Engine Components are the largest ICE segment. Electrical Components are growing through vehicle electrification. Cooling System is significant.

Market Breakup by Vehicle Type

Key Insight: Passenger Cars are the dominant South Korea auto parts vehicle type. Light Commercial Vehicles are significant. Heavy Commercial Vehicles serve logistics and industrial sectors.

Market Breakup by Sales Channel

Key Insight: OEM is the dominant South Korea auto parts channel through Hyundai, Kia, and Genesis procurement. Aftermarket is significant through replacement demand.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Component, Engine Components are dominant while Battery is fastest-growing

Engine Components command a significant South Korea auto parts share through the large installed ICE vehicle fleet requiring starter, alternator, and fuel system component supply from Bosch Korea and Denso Korea. Battery is the fastest-growing component through South Korea's accelerating EV adoption and LG Energy Solution, Samsung SDI, and SK On battery pack supply. Electrical Components are growing through vehicle electrification and software-defined vehicle transition driving expanded ignition and high-voltage wiring demand.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Vehicle Type, Passenger Cars are the dominant vehicle type

Passenger Cars command the largest South Korea auto parts vehicle type share through Hyundai Motor and Kia Corporation's combined annual production of over 3 million passenger vehicles driving consistent OEM and aftermarket parts demand. Light Commercial Vehicles are significant through the expanding last-mile delivery and logistics fleet. Heavy Commercial Vehicles are significant through Hyundai Truck and Kia Cargo domestic and export production supporting the construction and logistics sectors.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Sales Channel, OEM is the dominant channel in the South Korea auto parts market

OEM commands the largest South Korea auto parts channel share through Hyundai Motor, Kia, and Genesis direct procurement with tier-1 manufacturers including Hyundai Mobis, Bosch Korea, and Denso Korea. Aftermarket is significant through South Korea's large in-service vehicle fleet requiring replacement parts through authorised dealers and service centres.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The South Korea auto parts manufacturing market is competitive, with German engineering conglomerates, Japanese tier-1 auto parts specialists, European chassis and safety system manufacturers, and German driveline and safety technology companies competing alongside South Korean OEM-integrated suppliers for Hyundai, Kia, and Genesis contracts.

Robert Bosch GmbH has a dominant South Korea auto parts market presence through Bosch Korea's engine management, EV powertrain, and chassis control systems. In 2025, Bosch Korea invested KRW 200 Billion in a new Daejeon factory production line, serving Hyundai Motor, Kia, and Genesis as a tier-1 OEM supplier.

Denso Corp. is a Japanese automotive components company with a significant South Korea auto parts market presence through thermal management, powertrain control, and ADAS systems for Hyundai Motor Group and Korean OEM customers.

Continental AG is a German automotive technology company with a significant South Korea auto parts manufacturing market presence through chassis safety systems, ADAS, and powertrain electronics for Hyundai Motor, Kia, and Genesis. Continental Korea supplies tyre pressure monitoring, electronic brake systems, and EV powertrain modules.

ZF Friedrichshafen AG has a significant South Korea auto parts market presence through automatic transmissions, electric drive systems, and steering systems for Hyundai, Kia, and Genesis, with growing EV driveline component investment.

Other key players include Marelli Holdings, Hyundai Motor Co., Sumitomo Electric, Magna International Inc., Valeo S.A., and Aisin Corporation, among others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Our full report for 2026-2035 provides comprehensive market sizing, segmentation analysis across component, vehicle type, and sales channel dimensions, and competitive benchmarking for the South Korea auto parts manufacturing market. Coverage spans historical data from 2019 through 2035, equipping auto parts manufacturers, OEM suppliers, and automotive investors with targeted intelligence on South Korea's EV component transition. Reach out to our team to access the complete report or request a customised version.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market reached an approximate value of USD 124.48 Billion.

The market is estimated to grow at a CAGR of 3.30% between 2026 and 2035.

The market is estimated to witness a healthy growth during 2026-2035 to reach around USD 172.23 Billion by 2035.

The market is being driven due to growth of the automotive sector, the presence of a broad range of vehicles, and the rising export opportunities.

The key trends aiding the market include favourable government incentives and technological advancements.

Based on vehicle type, market segmentations include passenger cars, light commercial vehicles, and heavy commercial vehicles.

Different sales channels are OEM and aftermarket.

The major players in the market are Robert Bosch GmbH, Denso Corp., Continental AG, ZF Friedrichshafen AG, Marelli Holdings Co., Ltd., Hyundai Motor Co., Sumitomo Electric Industries, Ltd., Magna International Inc., Valeo S.A., and Aisin Corporation, among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Component |

|

| Breakup by Vehicle Type |

|

| Breakup by Sales Channel |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.