Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

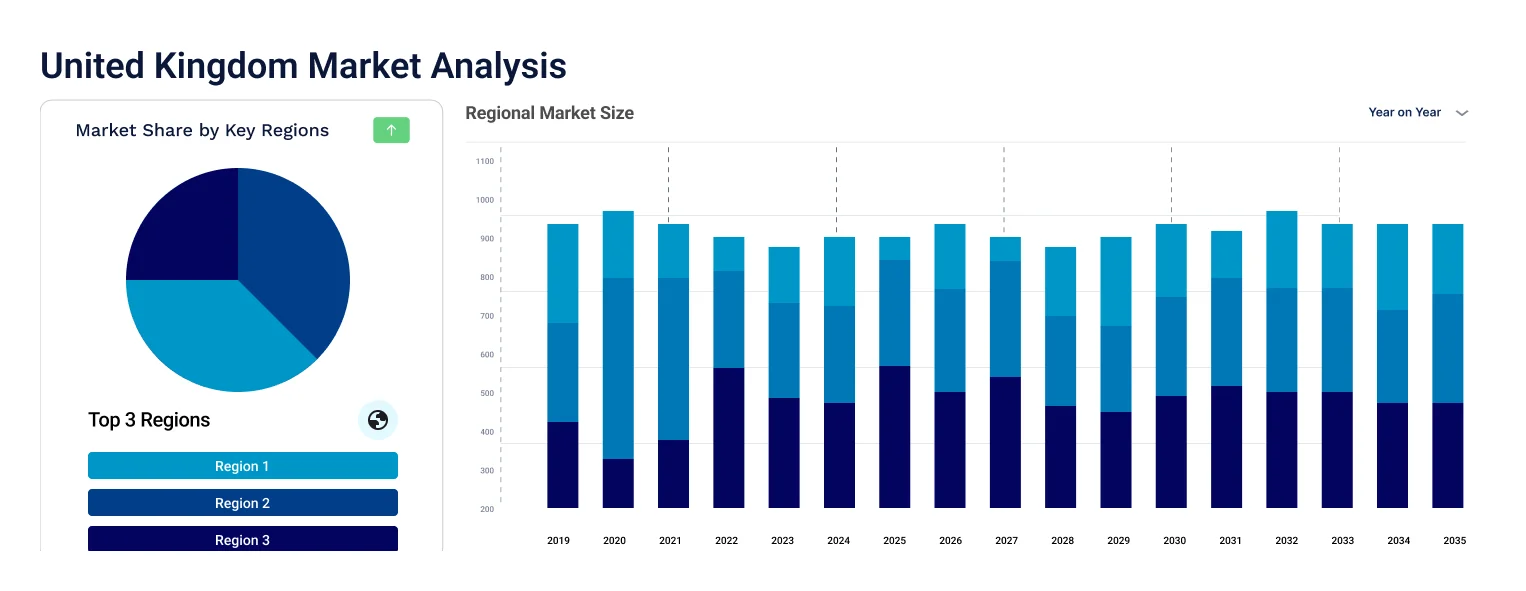

The United Kingdom heart valve devices market was valued at USD 4.04 Billion in 2025, driven by the increasing incidence of valvular heart diseases such as aortic stenosis and mitral regurgitation in the region. The market is anticipated to grow at a CAGR of 9.50% during the forecast period of 2026-2035, with the values likely to reach USD 10.01 Billion by 2035.

The US-Israel-Iran conflict, which began on 28 February 2026, is introducing supply chain and cost pressures into the United Kingdom heart valve devices market. The effective closure of the Strait of Hormuz has reduced commercial shipping to 90% below pre-war levels, while global air cargo capacity in the Gulf region has dropped by 79%. Heart valve devices, including transcatheter aortic valve replacement (TAVR) systems and surgical bioprosthetic valves manufactured by Edwards Lifesciences, Medtronic, Abbott, and Boston Scientific, depend on globally sourced components including medical-grade titanium, bovine and porcine pericardial tissue, and precision-machined delivery catheter systems. The disruption of global logistics corridors is extending lead times and inflating freight costs for these critical cardiovascular components.

The UK heart valve devices market, valued at approximately USD 3.69 billion in 2024 and projected to grow at a 9.5% CAGR through 2034, operates within the NHS procurement framework that emphasizes cost efficiency across the supply chain. Rising energy prices, with Brent crude exceeding USD 120 per barrel, are increasing manufacturing costs for device producers. Ethylene oxide, used to sterilize approximately half of all medical devices globally, is derived from petrochemical feedstocks now under supply pressure from the Gulf disruption. Titanium, essential for mechanical heart valve components and delivery system housings, has seen price increases as supply routes from key producers including Israel are affected by the conflict. NHS Supply Chain's integrated procurement approach aims to minimize the impact of price fluctuations, but sustained cost escalation could pressure hospital budgets allocated to cardiac procedures.

Demand for heart valve devices in the UK remains strong, driven by the high prevalence of aortic stenosis and mitral regurgitation in an aging population. The MHRA's regulatory framework continues to facilitate device approvals, supporting market access for next-generation TAVR and transcatheter mitral valve repair systems. However, the conflict environment introduces a cybersecurity dimension as well; a recent cyberattack against medical device manufacturer Stryker has been linked to broader Iran-related cyber threats targeting the healthcare industry. NHS procurement teams face the challenge of maintaining uninterrupted access to cardiac valve devices while managing the cost implications of a prolonged Middle East conflict.

Government: NHS Supply Chain's integrated procurement approach is being tested by conflict-driven cost escalation across medical device supply chains, requiring adaptive strategies to contain cardiac device spending. The MHRA continues to facilitate device regulatory approvals, but rising manufacturing and logistics costs may slow the rate at which next-generation heart valve technologies reach NHS hospitals. The UK government faces broader energy cost pressures from the Strait of Hormuz closure, with potential downstream effects on NHS operational budgets for energy-intensive hospital environments.

Market: The UK heart valve devices market, valued at USD 3.69 billion in 2024, faces component cost inflation as titanium supply routes from Israel and other regions are disrupted by the conflict. Leading manufacturers Edwards Lifesciences, Medtronic, and Abbott face elevated logistics expenses as global air freight capacity from the Gulf drops 79%, extending delivery timelines for TAVR and surgical valve systems. A cyberattack against Stryker linked to Iran-related threats highlights the growing cybersecurity risk dimension for medical device manufacturers operating during the conflict.

Procurement: Ethylene oxide sterilization costs for heart valve devices are rising as petrochemical feedstock supply from the Gulf is disrupted, increasing per-unit processing expenses for device distributors. NHS cardiac procurement teams are building buffer inventories of transcatheter valve systems and qualifying alternative shipping routes to ensure continuity for urgent cardiac procedures. Titanium and specialty alloy prices for mechanical valve components are increasing as conflict-related supply disruptions affect sourcing from Israel and complicate global logistics corridors.

The United Kingdom is reported to experience a growing burden of valvular heart diseases, such as aortic stenosis and mitral regurgitation, particularly in people over 65, which is likely to boost market growth.

The presence of a favorable regulatory system, led by the MHRA (Medicines and Healthcare products Regulatory Agency) and NHS England, is projected to elevate the United Kingdom heart valve devices market value in the forecast period.

The rising interest in customized, retrievable, and repositionable valves, especially for complex anatomies and younger patients, is a major market trend.

Compound Annual Growth Rate

9.5%

Value in USD Billion

2026-2035

The market is experiencing significant growth, driven by advancements in medical technology, an aging population, and increasing awareness of cardiovascular health. The UK's aging population is another key market driver, as valvular heart diseases such as aortic stenosis and mitral regurgitation are more common among older individuals. The demand for biological (tissue) valves, which require less long-term care compared to mechanical valves, is particularly high, aligning with healthcare preferences for less invasive, patient-friendly treatments. Moreover, the growing awareness of cardiovascular health, coupled with the NHS's initiatives to improve cardiovascular care, is expected to support the market expansion in the forecast period.

Rising Prevalence of Cardiovascular Diseases to Support Market Growth

Heart valve disease is prevalent in the United Kingdom, affecting approximately 11.3% of people over the age of 65. The rising burden of heart valve disease, particularly among the aging population, is a primary driver of growth in the heart valve devices market. As individuals age, the incidence of valvular heart diseases like aortic stenosis and mitral regurgitation increases, further contributing to the demand for effective valve replacement and repair solutions.

The market is witnessing several trends and developments to improve the current scenario. Some of the notable trends are as follows:

The market report offers a detailed analysis of the market based on the following segments:

Market Breakup by Valve Type

Market Breakup by Product Type

Market Breakup by Procedure

Market Breakup by End User

Segmentation Based on Valve Type to Hold a High Market Value

Based on the valve type, the market is segmented into biological (tissue) valve and mechanical valve. In the United Kingdom, the biological (tissue) valve segment holds a substantial market share, primarily due to its growing preference among elderly patients and those looking to avoid long-term anticoagulation therapy required with mechanical valves. These valves are increasingly used in both surgical and transcatheter procedures, including TAVR, and are supported by evolving clinical guidelines that favor tissue valves for patients over a certain age or with lifestyle considerations.

The market shows varied growth patterns across different regions, influenced by healthcare accessibility, demographic profiles, and the distribution of specialized cardiac centers. In Northern England, treatment rates are notably higher, indicating more active adoption of valve interventions in certain areas. On the other hand, Southern regions tend to show relatively lower treatment rates, revealing opportunities for further market development and improved access to advanced cardiac care.

The key features of the market report comprise patent analysis, grants analysis, funding and investment analysis, and strategic initiatives by the leading players. The major companies in the market are as follows:

Medtronic plc, headquartered in Ireland, offers a comprehensive range of transcatheter and surgical heart valves. The company's Evolut platform is widely used across NHS trusts and private hospitals, offering alternatives for patients unfit for open-heart surgery. Medtronic supports UK-based training programs, clinical trials, and registry data collection, helping to shape clinical guidelines and improve access to advanced care.

Edwards Lifesciences is a U.S.-based company specializing in structural heart disease, critical care, and surgical monitoring technologies. In the UK, the company has made a significant impact with its SAPIEN transcatheter valve series, which is widely used across NHS and private hospitals. Edwards actively collaborates on clinical research and national registry programs, helping to validate the safety and long-term effectiveness of its devices.

Abbott is recognized for its role in expanding transcatheter mitral valve repair (TMVr) in the UK, particularly through its MitraClip system. MitraClip has become a leading therapeutic option for patients with mitral regurgitation who are not suitable candidates for open-heart surgery. Abbott has also reinforced its presence in the transcatheter aortic valve replacement (TAVR) space with the introduction of the Portico and Navitor systems.

Corcym is one of the key market players in the surgical heart valve segment. Its sutureless valve technology (Perceval) enables faster surgical procedures and recovery, making it a valuable solution in high-volume centers. The company contributes to ongoing UK cardiac surgery education and partners with surgeons to optimize outcomes for complex valve repair and replacement cases.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Other key players in the market include Boston Scientific Corporation, B. Braun SE, Getinge AB, JenaValve Technology, Inc., and Meril Life Sciences Pvt. Ltd.

Upto 15% Off

USD

$1999 $1799

$3099 $2789

$4599 $3909

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Valve Type |

|

| Breakup by Product Type |

|

| Breakup by Procedure |

|

| Breakup by End User |

|

| Market Dynamics |

|

| Supplier Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 1,999

USD 1,799

tax inclusive*

Single User License

One User

USD 3,099

USD 2,789

tax inclusive*

Five User License

Five User

USD 4,599

USD 3,909

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.