Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

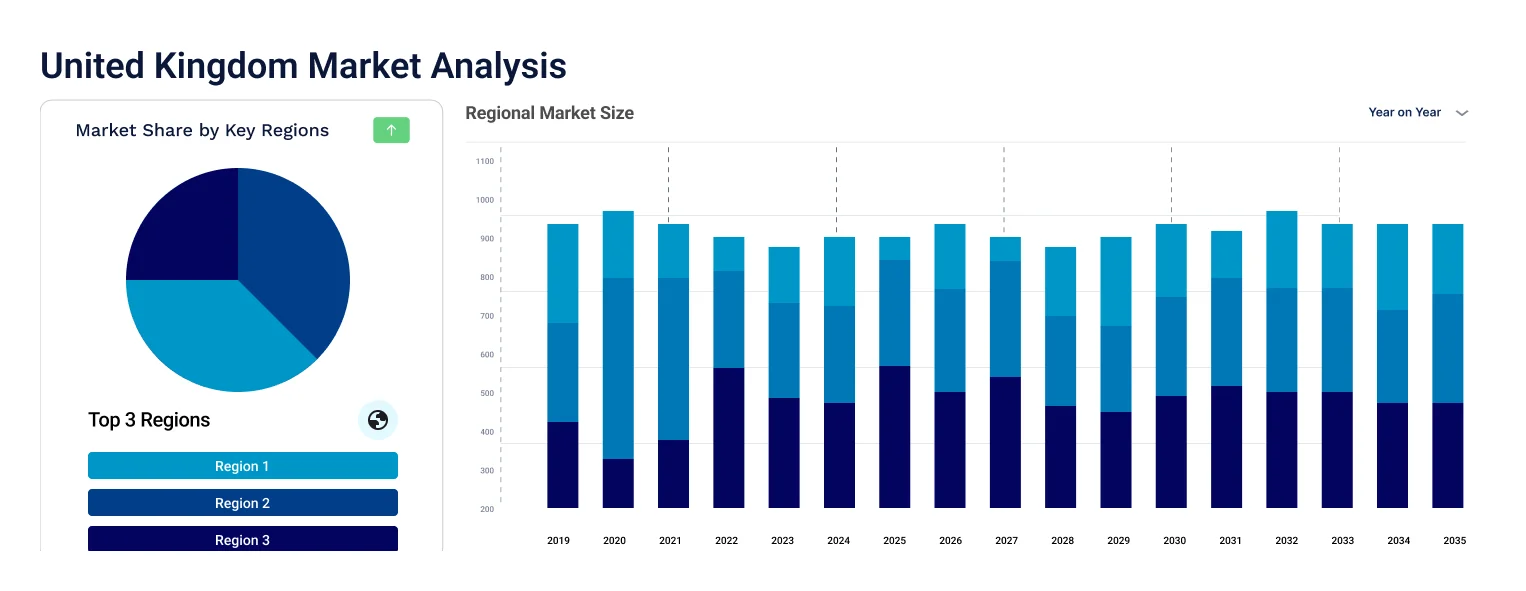

The United Kingdom Ice Cream Market reached a value of USD 1.31 Billion at 2025 and is projected to expand at a CAGR of around 4.50% during the forecast period of 2026-2035. With rising consumer demand for premium indulgence experiences, accelerating growth of vegan and plant-based ice cream lines, dynamic product innovation including miniature formats and exotic flavors, and expanding digital and convenience retail access, the market is expected to reach USD 2.03 Billion by 2035.

Compound Annual Growth Rate

4.5%

Value in USD Billion

2026-2035

| United Kingdom Ice Cream Market Report Summary | Description | Value |

| Base Year | USD Billion | 2025 |

| Historical Period | USD Billion | 2019-2025 |

| Forecast Period | USD Billion | 2026-2035 |

| Market Size 2025 | USD Billion | 1.31 |

| Market Size 2035 | USD Billion | 2.03 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 4.50% |

| CAGR 2026-2035 - Market by Region | Scotland | 4.7% |

| CAGR 2026-2035 - Market by Region | England | 4.3% |

| CAGR 2026-2035 - Market by Product Type | Cups and Tubs | 4.6% |

| CAGR 2026-2035 - Market by Type | Vegan | 7.6% |

| 2025 Market Share by Region | England | 89.4% |

The United Kingdom ice cream market is being reshaped by premiumization, plant-based innovation, evolving retail formats, and culturally driven product launches that reflect how British consumers engage with indulgence in an increasingly health-conscious and experience-oriented environment.

In March 2025, UK-based ice cream giant Froneri International Limited announced a licensing and distribution agreement with Lotus Bakeries to produce, market, and distribute Lotus Biscoff-branded ice cream across several European countries from 2026, with planned expansion through 2028. The deal leverages Lotus Biscoff's strong brand recognition in the UK biscuit and spread category to drive demand for Biscoff-flavored frozen desserts. For Froneri, the arrangement opens a scalable premium product line with built-in consumer awareness, while for Lotus, it deepens its brand presence in the frozen dessert aisle without requiring direct investment in manufacturing capability.

In February 2025, Magnum launched the Utopia range in the United Kingdom, described as the brand's most premium and indulgent product line to date. The range features marbled ice cream sticks in Double Cherry and Double Hazelnut flavours, produced using an innovative ingredient marbling technique that creates a multisensorial eating experience. The launch demonstrates Magnum's ongoing commitment to occupying the ultra-premium tier of the UK ice cream market and reflects a broader trend of major brands investing in artisanal-quality manufacturing processes to differentiate from private label and mid-market products.

In July 2025, Wall's, a brand under Unilever, launched a limited-edition Minecraft-themed ice cream product in the United Kingdom, distributed exclusively through Morrisons supermarkets before a planned rollout across Europe. The product features colourful ice cream blocks inspired by the Minecraft video game universe, targeting Gen Z and gaming-focused consumers. The launch was supported by a dedicated TikTok influencer marketing campaign, illustrating how major UK ice cream brands are blending pop culture moments with social media-native promotional strategies to capture younger consumer demographics who respond to culturally relevant, limited-availability products.

In October 2024, Magnum, the flagship ice cream brand under Unilever, launched Bon Bons in the United Kingdom, its first-ever bite-sized ice cream range presented in tub format. The product was released in three of the brand's most popular flavour profiles including White Chocolate and Cookies, Gold Caramel Billionaire, and Salted Caramel and Almond. The launch reflects a strategic push by major brands to combine the snacking convenience of handheld formats with the at-home sharing appeal of tubs, targeting consumers who want premium indulgence in flexible portion sizes that suit both individual and social consumption occasions

In August 2024, Ferrero UK launched Nutella Ice Cream Tubs in the United Kingdom, extending its core Nutella brand into the frozen desserts category for the first time. The product features hazelnut-flavored ice cream with Nutella swirls, designed to capitalize on the UK's growing premium ice cream tub segment and the strong brand loyalty Nutella commands among British consumers. The launch exemplifies the trend of established confectionery and snack brands leveraging their brand equity to enter adjacent dessert categories and capture demand from consumers who associate familiar brand flavors with quality and indulgence.

The introduction of miniature and bite-sized ice cream formats, most visibly exemplified by Magnum's October 2024 launch of Bon Bons in the UK, reflects a broader consumer desire for flexible indulgence. Smaller formats allow consumers to manage portion sizes without sacrificing premium quality, appealing to both health-conscious buyers and those seeking shareable, social eating experiences. This format innovation is also widening the category's suitability for occasions beyond traditional summer consumption, contributing meaningfully to UK ice cream market growth by extending the purchase and eating window across all seasons

Vegan ice cream has moved from a niche dietary option to a mainstream product category in the UK. The shift is driven by a combination of dietary health preferences, environmental consciousness, and the improvement of plant-based formulations that now closely replicate dairy ice cream in texture and richness. Major brands including Magnum, Ben and Jerry's, and a growing number of artisanal producers have expanded their vegan lines in response to this demand, with products gaining shelf space across major supermarkets. The Wales Government reported a 49% rise in milk production between 2022 and 2023, yet plant-based adoption continues to grow in parallel, suggesting a widening total market rather than a substitution dynamic

UK consumers are increasingly drawn to ice cream products that offer complex, novel, and elevated taste experiences. Ferrero's 2024 entry into the category with Nutella Ice Cream Tubs, alongside Magnum's Utopia marbled range and Froneri's Biscoff collaboration, illustrates the trend of brands importing established flavour identities into frozen desserts to create instant appeal. This premiumization push is elevating average retail price points across the category, supporting revenue growth even in periods where volume growth remains modest due to cost-of-living pressures among UK consumers.

Ice cream brands in the UK are increasingly using culture-led collaborations and social media-amplified campaigns to build relevance with younger consumers. Wall's Minecraft-themed July 2025 launch, backed by a TikTok influencer campaign, is a tangible example of how the category is integrating gaming culture, digital communities, and limited-edition scarcity to drive purchase urgency and social sharing. This approach is redefining ice cream marketing from seasonal advertising toward year-round cultural engagement, generating visibility and consumer interest during periods when traditional frozen dessert demand would otherwise be subdued.

The Expert Market Research’s report titled “United Kingdom Ice Cream Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

Market Breakup by Product Type

Key Insight: Bars and pops hold the largest share of the UK ice cream market by product type, benefiting from their universal convenience and cross-demographic appeal. Their portability and single-serve format make them ideal for both impulse purchases and planned treats across retail, petrol stations, leisure venues, and convenience stores. Cups and tubs are the fastest-growing format, expanding at a CAGR of approximately 4.6%, as at-home consumption grows and consumers invest in larger premium formats for sharing and experiential eating. The growth of cups and tubs is closely linked to the premiumization trend, with brands launching artisanal, high-ingredient-quality products in this format to justify higher price points.

Market Breakup by Type

Key Insight: Dairy and water-based ice cream commands the dominant share, reflecting the long-established cultural preference in the UK for milk-fat-rich frozen desserts. The category's quality improvement trajectory, driven by premium ingredient sourcing, artisanal production techniques, and innovative flavour development, continues to sustain strong consumer spending. The vegan segment is growing at a notably faster pace, as plant-based dairy alternatives improve in taste and texture parity with dairy products. Consumer adoption is expanding beyond dietary-specific buyers into mainstream shoppers who view plant-based options as a lighter, more environmentally responsible choice for occasional consumption.

Market Breakup by Flavour

Key Insight: Chocolate maintains the leading flavour share in the UK ice cream market, supported by its versatile application across premium products, seasonal gifting, and indulgent confectionery-crossover innovations such as Nutella-flavored and Biscoff-swirl varieties. Vanilla holds the second position as a core and consistent flavour with broad household and food service demand. Fruit flavours are gaining traction, particularly among vegan and health-conscious consumers seeking lighter, naturally-derived taste profiles. The Others category, which includes exotic and hybrid flavours such as salted caramel, coffee, and seasonal limited editions, is showing steady growth as consumer adventurousness and brand experimentation increase.

Market Breakup by Distribution Channel

Key Insight: Off-trade channels, particularly supermarkets and hypermarkets, dominate the UK ice cream market distribution landscape, providing mass market access for both everyday and premium products at competitive price points. Online grocery channels are the fastest-growing off-trade sub-category, reflecting the post-pandemic permanence of digital grocery shopping and the increasing availability of cold chain delivery infrastructure. On-trade channels, covering restaurants, cafes, food service venues, and entertainment venues, contribute a meaningful share to market revenue, supported by food service sector recovery and the continuing appeal of ice cream as a dessert and refreshment option in casual dining environments.

Market Breakup by Region

Key Insight: England accounts for the largest regional share of the UK ice cream market by a significant margin, reflecting its population size, higher concentration of major retail chains, and the volume of food service venues operating in cities like London, Manchester, and Birmingham. Scotland contributes meaningfully to both domestic production, with its established dairy farming heritage, and consumption, with Mackie's Ltd. being a notable indigenous brand. Wales has seen rising dairy output, with milk production growing 49% between 2022 and 2023 according to the Welsh Government, supporting expanded regional supply. Northern Ireland, while the smallest market by size, benefits from strong dairy traditions and growing consumer interest in premium regional ice cream products.

| CAGR 2026-2035 - Market by | Region |

| Scotland | 4.7% |

| England | 4.3% |

| Wales | XX% |

| Northern Ireland | XX% |

By Product Type: Bars and pops command the dominant share of the UK ice cream market, underpinned by their decades-long status as the default handheld dessert format across British consumer culture. Leading brands such as Magnum, Cornetto, and Wall's Calippo have built powerful recognition around this format, maintaining relevance through regular flavor innovation and premium line extensions. Cups and tubs are the fastest-growing format, attracting both premium and mainstream buyers as at-home socializing has elevated demand for larger formats that lend themselves to sharing. The October 2024 launch of Magnum Bon Bons demonstrates how brands are creatively blending the convenience of bar formats with the tub-format sharing occasion, a hybrid approach that is resonating strongly with UK consumers.

By Distribution Channel: Off-trade channels retain the dominant share of UK ice cream sales, with supermarkets and hypermarkets representing the primary purchase point for both ambient stock and impulse-buy freezer cabinet products. The largest retailers, including Tesco, Sainsbury's, Asda, and Morrisons, dedicate prominent freezer shelf space to national and premium ice cream brands, ensuring year-round visibility. Online channels are the fastest-growing sub-category within off-trade, supported by expanding home delivery capabilities and the growing convenience of online grocery ordering. On-trade channels serve a complementary role, generating higher per-serving revenue from food service settings where ice cream is presented as a premium dessert option with service uplift.

England dominates the United Kingdom ice cream market, accounting for the overwhelming majority of total consumption volume given its population of approximately 57 million people and its concentration of large metropolitan areas, retail infrastructure, and food service density. London alone represents a disproportionately large share of premium ice cream consumption, driven by high household incomes, a diverse consumer base that embraces global flavor trends, and a dense concentration of cafes, restaurants, and artisan ice cream parlors. Major supermarket chains headquartered in England, including Tesco, Sainsbury's, and Asda, exert significant influence over category shelf space allocation and promotional activity, directly shaping purchasing trends across the country. England's high proportion of urban consumers also drives above-average online grocery adoption, benefiting the fastest-growing distribution sub-channel.

Scotland is the second most commercially significant market within the UK for ice cream, with a heritage in dairy production that supports both regional manufacturing and consumer quality expectations. The Scotland-based Mackie's Ltd. is one of the country's best-known indigenous ice cream brands, recognized for its traditional dairy-based products and premium market positioning. Scotland's tourist economy, centered on its countryside and coastal destinations, provides additional seasonal demand from visitors, supporting artisanal and locally produced ice cream sales. Government data showing a 49% rise in Welsh milk production between 2022 and 2023 is also relevant to the broader UK context, as it reflects an increase in the raw material supply available to regional producers, supporting both product quality and pricing competitiveness.

The United Kingdom ice cream market is moderately consolidated at its upper tier, dominated by multinational players with extensive brand portfolios and distribution scale. Unilever, through its Magnum, Ben and Jerry's, Wall's, and other brands, commands a commanding share of impulse and take-home categories. Froneri, the strategic joint venture formed by Nestle and PAI Partners, occupies a similarly strong position through its broad brand and manufacturing network. However, the market also features a vibrant tier of regional and artisan producers who command loyal followings, particularly in Scotland and the premium gifting segment.

Competition in the UK ice cream market is increasingly multi-dimensional. Price remains a baseline competitive variable, but innovation in flavours, formats, sustainability credentials, and cultural relevance has become equally important for maintaining consumer attention and justifying premium pricing. Licensing partnerships, such as the Froneri-Lotus Biscoff arrangement, illustrate how brands are seeking growth through collaboration rather than purely organic product development.

Founded in 1929 and headquartered in London, Unilever is the UK ice cream market's largest player by revenue, operating some of the most recognized brands in the category including Magnum, Wall's, Ben and Jerry's, Cornetto, and Carte d'Or. The company has a dominant presence in both off-trade supermarket channels and on-trade food service. Unilever's 2024 and 2025 product activity, including Magnum Bon Bons, the Utopia marbled range, and Wall's Minecraft collaboration, demonstrates an active innovation pipeline designed to maintain consumer engagement across demographics. The company has also committed to spinning off its ice cream division as a standalone entity targeting 3-5% annual growth from 2026 onward.

Founded in 1866 and headquartered in Minneapolis, General Mills operates in the UK ice cream market through its Haagen-Dazs brand, which holds a premium positioning focused on indulgent, high-quality dairy ice cream in tubs and sticks. Haagen-Dazs has built strong brand loyalty among UK consumers who associate it with occasional treats and gifting occasions. The brand competes effectively at the super-premium tier through a consistent emphasis on ingredient quality, limited-edition seasonal launches, and elegant packaging design that differentiates it from both mass-market and artisan competitors.

Froneri International is a joint venture formed by Nestle and private equity firm PAI Partners, with UK operations spanning multiple brands and manufacturing facilities. The company distributes a wide portfolio of branded and private label ice cream products across the UK's retail and food service channels. Froneri's March 2025 agreement with Lotus Bakeries to produce and distribute Biscoff-branded ice cream from 2026 marks a significant commercial expansion that leverages a well-known biscuit flavor brand to create immediate consumer interest in a new product line. Froneri's manufacturing scale and distribution infrastructure position it well to execute on such licensing arrangements.

Founded in 1866 and headquartered in Vevey, Switzerland, Nestle has a longstanding presence in the UK ice cream market through brands including Mivvi, Fab, and the Kit Kat ice cream range. The company's collaboration structure with Froneri allows it to maintain brand exposure in the UK frozen desserts sector while benefiting from Froneri's operational efficiency. Nestle's global flavour and ingredient innovation capabilities allow it to bring new product concepts to the UK market rapidly, keeping its branded portfolio fresh relative to competitors. Its extensive retail distribution relationships ensure strong on-shelf availability across both major supermarkets and convenience formats.

Other key players in the market are Mondelez International Inc., Mackie's Ltd., Willen Ice Cream Company, Marshfield Farm Ice Cream Ltd., and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Stay ahead of the competition in the United Kingdom's premium and fast-evolving ice cream sector with our definitive 2026 market report. From vegan product trends and flavour innovation strategies to regional demand data and competitive brand analysis, this report delivers the clarity you need to make confident decisions. Whether you are a manufacturer looking to expand your UK range, an investor evaluating category growth, or a retailer optimizing your frozen aisle, this report has you covered. Download your free sample today and explore the opportunities shaping the UK's thriving ice cream market.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the United Kingdom ice cream market reached an approximate value of USD 1.31 Billion.

The market is projected to grow at a CAGR of 4.50% between 2026 and 2035.

The market is estimated to witness healthy growth in the forecast period of 2026-2035 to reach a value of around USD 2.03 Billion by 2035.

The major drivers of the market are the growing dairy and dairy products industry, the popularity of food delivery applications, and the innovation of new flavours by major brands.

The key trends of the market include the growing popularity of soft-serve ice cream, the preference for handheld ice cream cones and sticks, as well as the introduction of sustainable and eco-friendly packaging.

The regional markets include England, Wales, Scotland, and Northern Ireland.

The various product types of ice cream considered in the market report are bars and pops, and cups and tubs among others.

The major types of ice creams are dairy, water-based, and vegan.

The significant segments based on flavours considered in the market report are chocolate, vanilla, and fruit among others.

The key players in the market are Unilever Plc, General Mills, Inc., Mondelēz International, Inc., Froneri International Limited, Nestlé S.A., Mackie’s Ltd., Willen Ice Cream Company, and Marshfield Farm Ice Cream Ltd., among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Product Type |

|

| Breakup by Type |

|

| Breakup by Flavour |

|

| Breakup by Distribution Channel |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.