Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

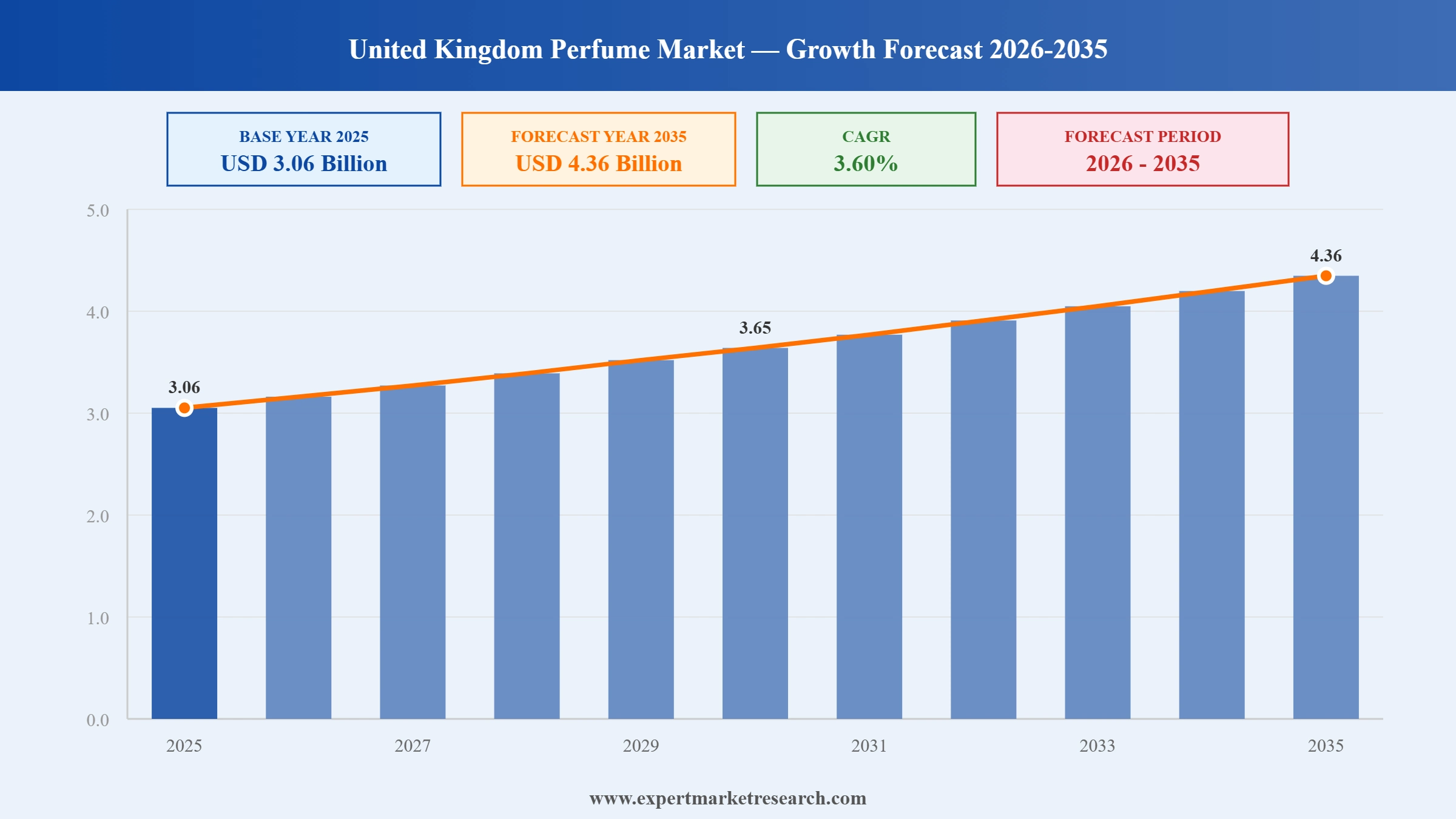

The United Kingdom perfume market reached a value of USD 3.06 Billion in 2025 and is projected to expand at a CAGR of around 3.60% during the forecast period of 2026-2035. Rising income levels, growing number of working women, diversification of fragrances, the emergence of unisex perfume brands, sustainable packaging trends, and thriving e-commerce are driving United Kingdom perfume market growth. The market is expected to reach USD 4.36 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

| United Kingdom Perfume Market Report Summary | Description | Value |

| Base Year | USD Billion | 2025 |

| Historical period | USD Billion | 2019-2025 |

| Forecast Period | USD Billion | 2026-2035 |

| Market Size 2025 | USD Billion | 3.06 |

| Market Size 2035 | USD Billion | 4.36 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 3.60% |

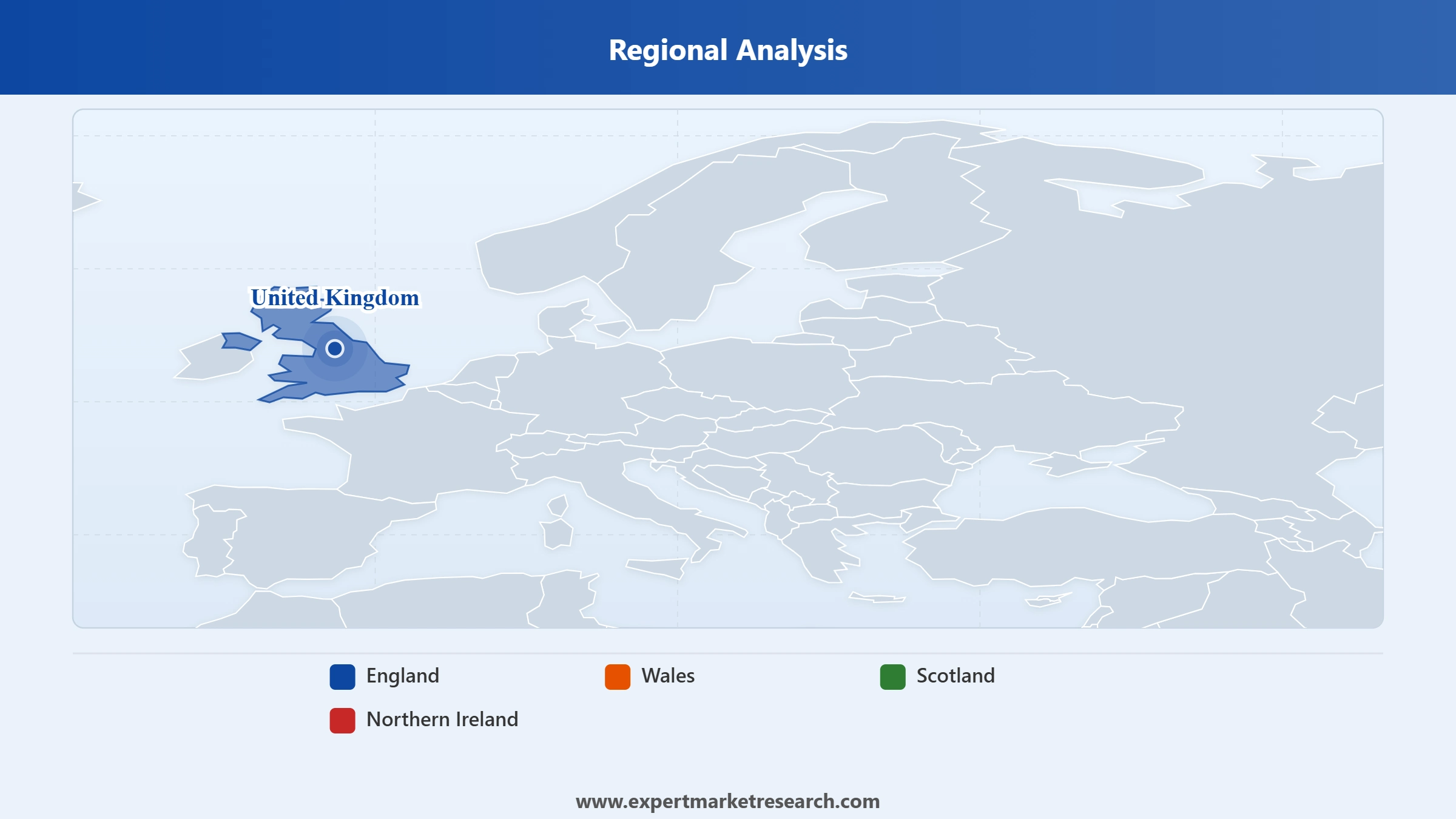

| CAGR 2026-2035 - Market by Region | Scotland | 4.0% |

| CAGR 2026-2035 - Market by Region | Wales | 3.8% |

| CAGR 2026-2035 - Market by Type | Eau De Parfum (EDP) | 4.4% |

| CAGR 2026-2035 - Market by Distribution Channel | Offline | 7.9% |

| Market Share by Region | England | 58.0% |

The United Kingdom perfume market is driven by rising consumer spending on premium fragrances, rapid growth of online fragrance retail, the emergence of unisex and niche perfume segments, celebrity endorsements, and sustainable ingredient innovations.

Estee Lauder Companies opened its first fragrance innovation centre, L'Atelier, in October 2025, with CEO Stephane de La Faverie highlighting fragrance as a key pillar of the company's path back to growth. L'Atelier is a collaborative space for Estee Lauder's fragrance brands to research and co-create new scents and fragrance formats for the UK and global markets.

Chanel launched BLEU DE CHANEL L'EXCLUSIF in August 2025, incorporating sustainably sourced sandalwood from New Caledonia. The launch reinforces Chanel's luxury position in the UK premium perfume market and reflects the growing consumer demand for sustainably sourced fragrance ingredients. Chanel's focus on sustainable ingredient sourcing aligns with the UK perfume market trend toward sustainable packaging.

Jo Malone London, the British fragrance house owned by Estee Lauder Companies, announced in January 2025 plans to open 12 new stores in market towns and smaller UK cities by mid-2025, expanding its UK store network from 37 to 45 locations. The expansion targets towns including Wilmslow, Farnham, Market Harborough, Leamington Spa, and Chichester. Jo Malone London plans to expand to 51 UK stores by mid-2026.

Estee Lauder launched the Legacy Fragrance Collection in February 2024, featuring five of the brand's iconic fragrances (Azuree, Estee, Knowing, Private Collection, and White Linen) in updated formulas developed by fragrance editor Frederic Malle. The Legacy Collection strips back non-essential ingredients to amplify the core character of each fragrance for UK consumers seeking high-quality heritage fragrances with modern refinement.

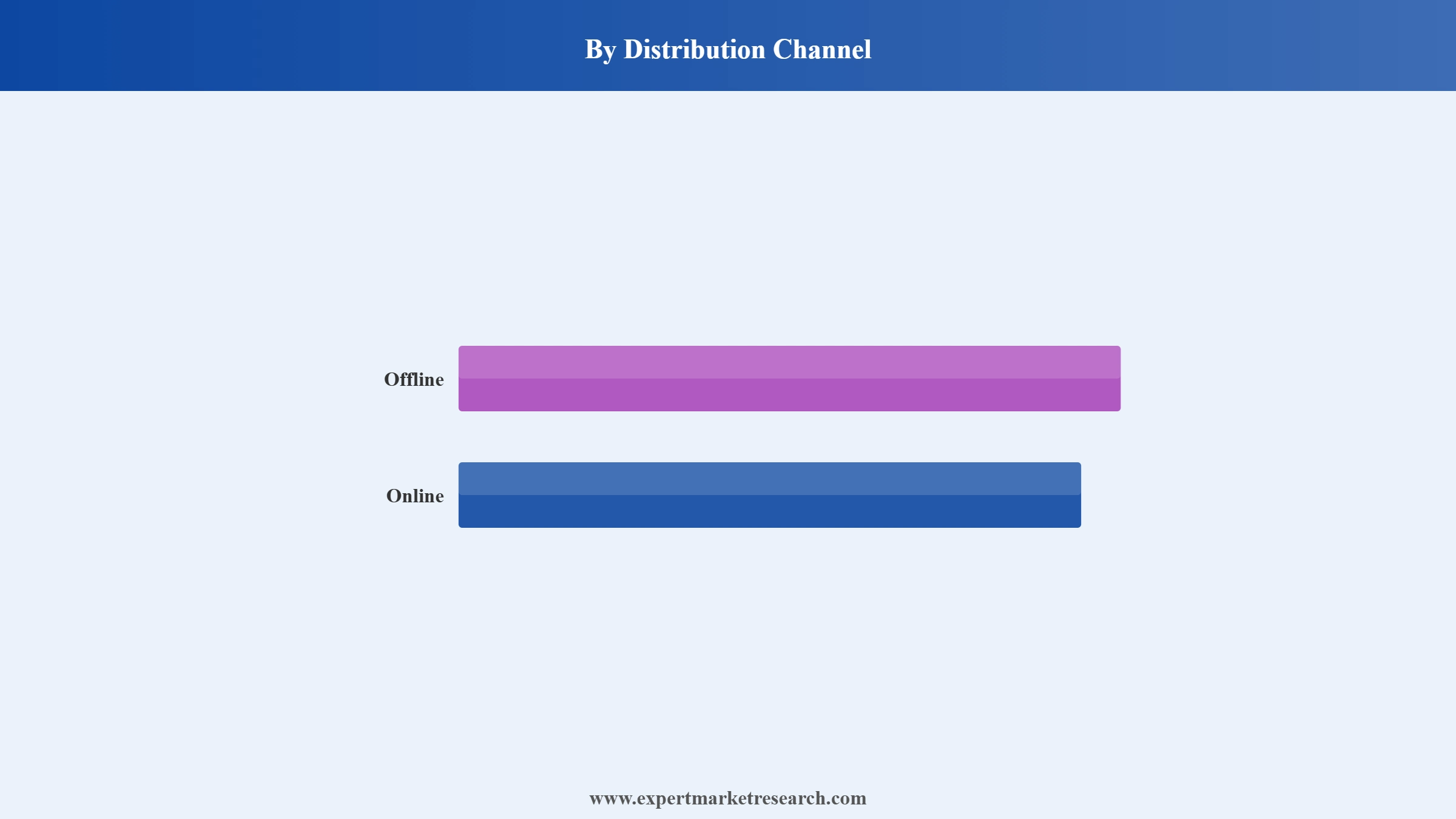

Online is the fastest-growing UK perfume distribution channel at approximately 7.9% CAGR, driven by the rapid adoption of digital beauty platforms, direct-to-consumer brand websites, and subscription fragrance discovery services. Online channels allow UK consumers to access a wider range of niche, artisan, and international perfume brands.

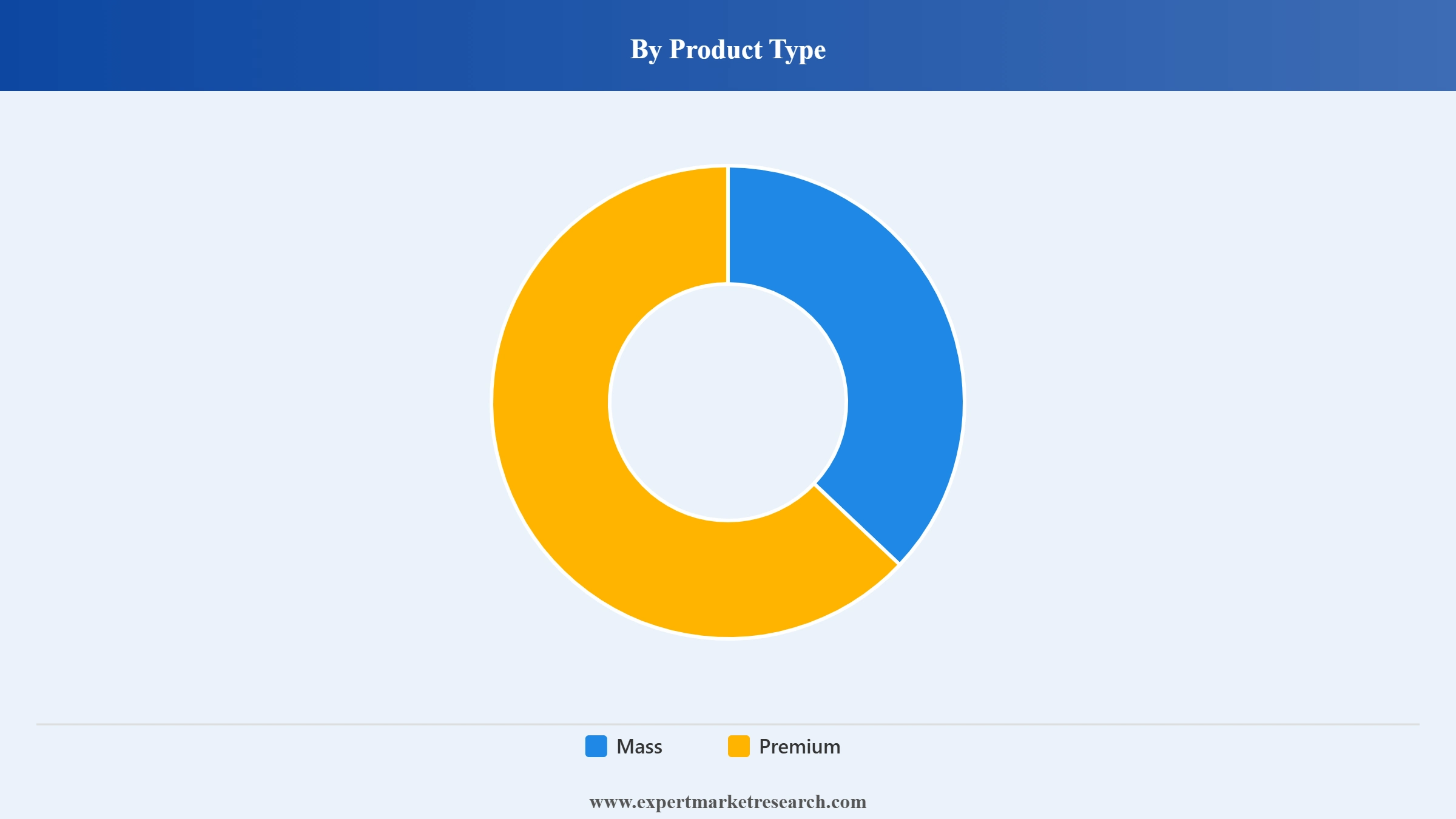

Premium is the dominant UK perfume product type by revenue, commanding approximately 57.5% of total UK perfume market revenue, driven by rising consumer preference for luxury, niche, and artisan fragrances. Premium brands leverage celebrity collaborations and limited-edition launches to sustain premium pricing and brand desirability.

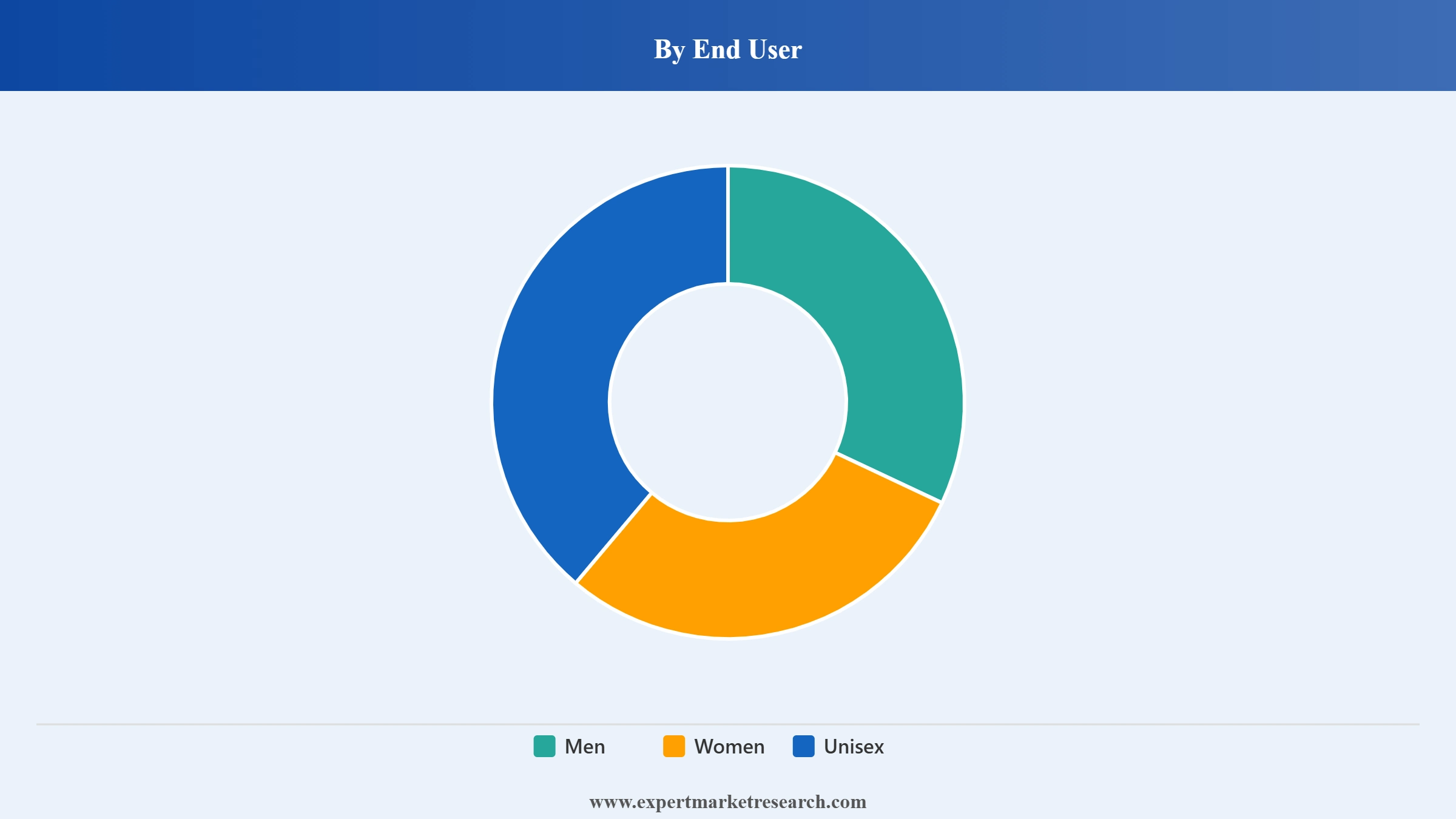

Women are the dominant UK perfume end-user segment by revenue, driven by higher perfume purchase frequency and strong affinity for premium and luxury fragrance brands. The Unisex end-user segment is the fastest-growing, reflecting the growing UK consumer preference for gender-neutral fragrances and the rise of unisex and genderless perfume brands. The Men end-user segment is growing through premiumisation and increasing adoption of premium eau de parfum and parfum formats.

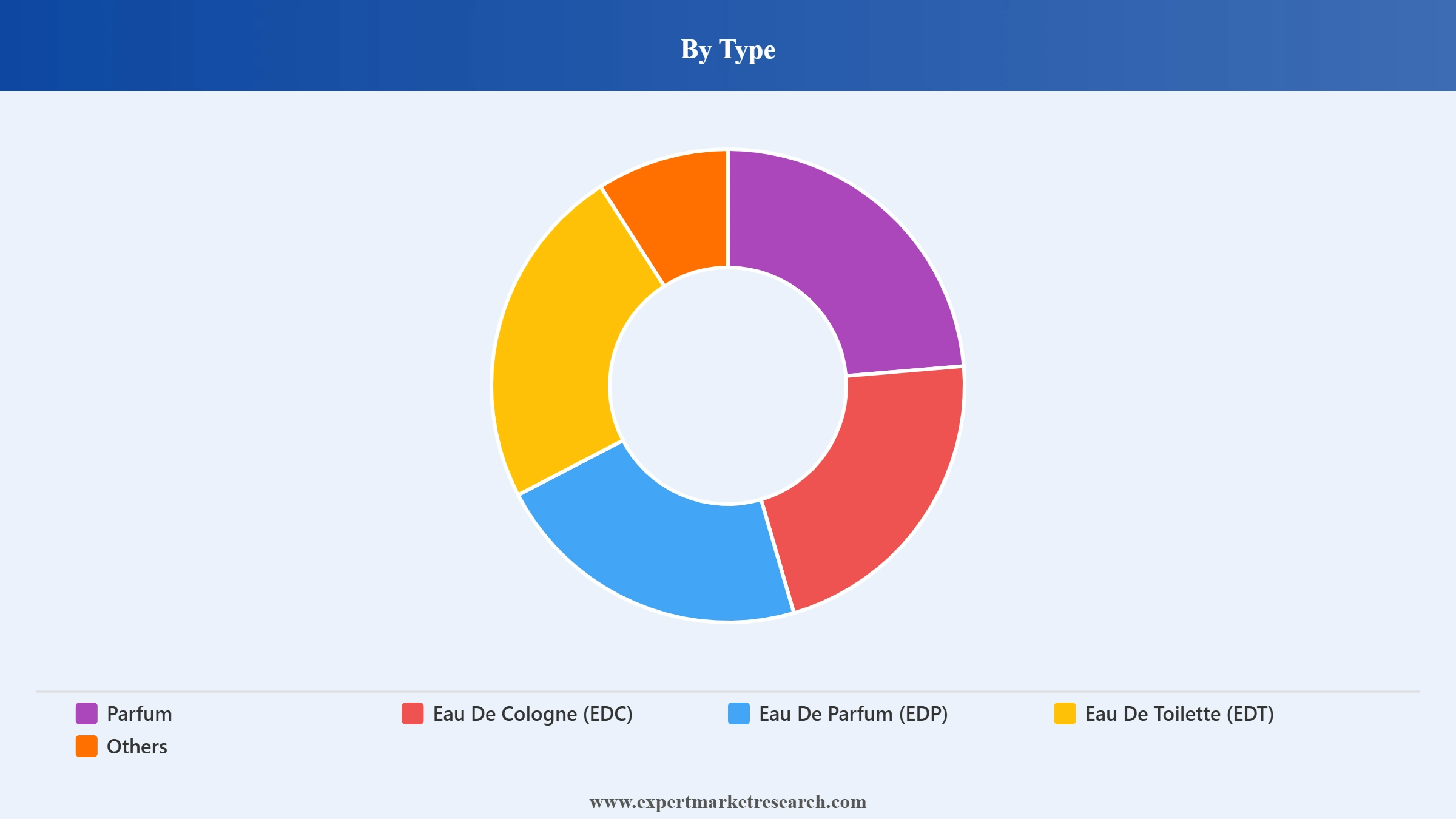

Parfum and Eau De Parfum (EDP) are the fastest-growing UK perfume types, driven by the strong premiumisation trend and consumer demand for longer-lasting, higher-concentration fragrances. Eau De Toilette (EDT) remains the most popular mass and premium format. The UK exported USD 743.8 million in perfumes and toilet waters in 2023, primarily to the Netherlands, Ireland, United States, Belgium, and Australia.

England commands the largest United Kingdom perfume market share by region, driven by London’s concentration of luxury department stores, niche perfumeries, and brand boutiques, and its large urban consumer base with strong spending on premium and luxury fragrances. Scotland is the fastest-growing UK region at approximately 4.0% CAGR through rising disposable incomes and growing demand for premium and niche fragrances. Wales and Northern Ireland represent growing regional perfume markets served by national retailers and online channels.

The "United Kingdom Perfume Market Report and Forecast 2026-2035" by Expert Market Research offers analysis across the following segments:

Market Breakup by Type

Key Insight: Parfum and EDP are growing through premiumisation. EDT remains a dominant mass and premium format. EDC serves the mass fragrance segment.

Market Breakup by Product Type

Key Insight: Premium is the dominant UK perfume product type commanding approximately 57.5% of market revenue. Mass is growing through accessible fragrance options and digital channel expansion.

Market Breakup by End User

Key Insight: Women is the dominant UK perfume end-user segment by revenue. Unisex is the fastest-growing end-user segment through growing gender-neutral fragrance trends.

Market Breakup by Distribution Channel

Key Insight: Online is the fastest-growing UK perfume distribution channel at approximately 7.9% CAGR. Offline remains the dominant channel through department stores, specialty stores, and beauty retailers.

Market Breakup by Region

Key Insight: England is the largest UK perfume region through London's luxury retail dominance and large urban consumer base. Scotland grows at approximately 4.0% CAGR through rising premium fragrance demand.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Type, Eau De Parfum (EDP) and Eau De Toilette (EDT) are the dominant perfume types by revenue

Eau De Parfum (EDP) and Eau De Toilette (EDT) are the dominant UK perfume types by revenue, reflecting consumer preference for mid-to-high concentration fragrance formats with longer-lasting performance. Parfum is the fastest-growing type through premiumisation. Eau De Cologne (EDC) serves the mass and casual fragrance segments. The UK's perfume and toilet water exports reached USD 743.8 million in 2023, mainly to the Netherlands, Ireland, United States, Belgium, and Australia.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Product Type, Premium is the dominant product type commanding 57.5% of UK perfume revenue

Premium commands the largest UK perfume market share by product type at approximately 57.5% of revenue, driven by the UK's strong consumer preference for luxury and high-end fragrance experiences. Mass is growing through accessible price point fragrances in supermarkets, pharmacy chains, and online platforms. The premium segment benefits from celebrity collaborations and limited-edition launches by Estee Lauder, Chanel, LVMH, and Hermes.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By End User, Women is the dominant end user segment in the UK perfume market

Women command the largest UK perfume market share by end user through higher purchase frequency and strong spending on premium and luxury fragrances. Men is a growing segment through premiumisation and increasing adoption of premium EDP formats. Unisex is the fastest-growing end-user segment through the growing UK consumer preference for gender-neutral and genderless fragrances.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Distribution Channel, Online is the fastest-growing channel at 7.9% CAGR

Online is the fastest-growing UK perfume distribution channel at approximately 7.9% CAGR, reflecting the rapid shift to digital beauty platforms and fragrance e-commerce. Offline remains the dominant channel through department stores, specialty perfumeries, health and beauty retailers, and direct brand boutiques. Jo Malone London is expanding its UK store network from 37 to 45 stores by mid-2025.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The United Kingdom is a key Europe perfume market driven by strong premium fragrance demand, growing online channel adoption, unisex fragrance trends, and sustainable ingredient innovation

The United Kingdom perfume market operates within the broader Europe perfume market. The UK’s perfume and toilet water exports totalled USD 743.8 million in 2023, primarily to the Netherlands, Ireland, United States, Belgium, and Australia. Premium fragrances account for approximately 57.5% of UK perfume market revenue.

England commands the largest UK perfume market share through London’s luxury retail concentration and the large urban consumer base. Scotland is growing at approximately 4.0% CAGR through rising disposable incomes and growing demand for premium fragrances. Wales and Northern Ireland serve growing regional perfume markets.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The United Kingdom perfume market is highly competitive, with global luxury fragrance conglomerates, independent fragrance houses, and heritage British brands competing through product innovation, celebrity endorsements, sustainable ingredient sourcing, and digital marketing.

Estee Lauder Companies Inc. is a US-based global beauty conglomerate with a significant UK perfume market presence through its fragrance brands including Jo Malone London, Tom Ford Beauty, Frederic Malle, and Le Labo. In October 2025, Estee Lauder opened its first fragrance innovation centre, L'Atelier. In February 2024, Estee Lauder launched the Legacy Fragrance Collection (five iconic reformulations by Frederic Malle). Jo Malone London is expanding to 45 UK stores by mid-2025.

Chanel SA is a France-based luxury fashion and beauty house with a dominant UK perfume market presence through its iconic fragrance portfolio including Chanel No. 5, Coco Mademoiselle, and BLEU DE CHANEL. In August 2025, Chanel launched BLEU DE CHANEL L'EXCLUSIF with sustainably sourced sandalwood from New Caledonia, reinforcing its luxury position in the UK premium perfume market. Chanel's premium fragrance portfolio benefits from strong brand heritage and exclusive retail distribution.

LVMH Moet Hennessy Louis Vuitton SE is a France-based global luxury conglomerate with a significant UK perfume market presence through its Perfumes and Cosmetics division, including fragrance brands such as Christian Dior Parfums, Givenchy Parfums, Guerlain, and Acqua di Parma. LVMH's Perfumes and Cosmetics division generated USD 9.11 billion in revenue in 2024 with 4% organic revenue growth.

Hermes International S.A. is a France-based luxury goods house with a growing UK perfume market presence through its Hermes Parfums portfolio, including iconic fragrances such as Terre d'Hermes, Twilly d'Hermes, and Eau des Merveilles. Hermes positions its fragrance range as ultra-premium luxury perfumery, leveraging heritage craftsmanship and exclusive distribution, benefiting from growing UK demand for ultra-premium and niche fragrance.

Other key players include Shiseido Co., Ltd., Burberry Group PLC, Dolce & Gabbana S.r.l., Kering SA, PVH Corp., Ralph Lauren Corporation, and Natura &Co., among others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Our full report for 2026-2035 delivers the market data, competitive analysis, and strategic insights to capture the United Kingdom's growing perfume market. Reach out to our team to access the complete report or request a customised version.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market reached an approximate value of USD 3.06 Billion.

The United Kingdom perfume market is estimated to grow at a CAGR of 3.60% between 2026 and 2035.

The United Kingdom perfume market is estimated to witness healthy growth in the forecast period of 2026-2035 to reach a value of USD 4.36 Billion by 2035.

The market is being driven by increase in income level, rising number of working women, diversification of fragrances, and emergence of unisex perfume brands.

The key trends aiding the market include an increase in consumer-centric and sustainable packaging, thriving e-commerce sector, and increasing brand endorsement by celebrities.

The various types of perfumes are parfum, eau de cologne (EDC), eau de parfum (EDP), and eau de toilette (EDT), among others.

The major players in the market are Estee Lauder Companies Inc., Chanel SA, LVMH Moet Hennessy Louis Vuitton, Hermès International S.A, Shiseido Co., Ltd., Burberry Group PLC, Dolce & Gabbana, Kering SA, PVH Corp., Ralph Lauren Corporation, and Natura &Co., among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Type |

|

| Breakup by Product Type |

|

| Breakup by End User |

|

| Breakup by Distribution Channel |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.