Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

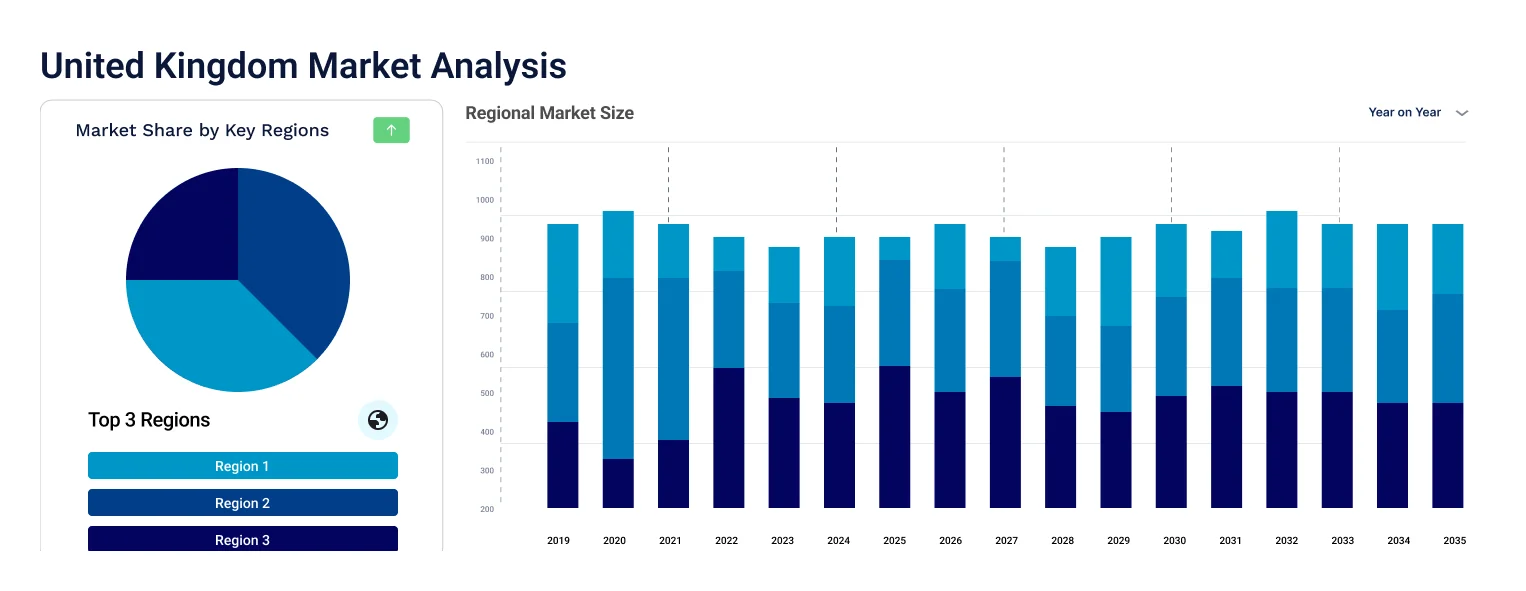

The United Kingdom third party logistics (3PL) market size reached approximately USD 30.99 Billion in 2025. The market is projected to grow at a CAGR of 2.60% between 2026 and 2035, reaching a value of around USD 40.06 Billion by 2035.

DHL Supply Chain announced in April a major multi year third party logistics contract with a leading UK grocery retailer, covering automated warehousing and last mile delivery operations across England and Scotland. The deal underscores rising demand for outsourced logistics among British retailers facing margin pressure. DHL plans to deploy advanced robotics at the new sites, The Telegraph reported.

UK third party logistics providers accelerated investment in warehouse automation in March amid persistent labour shortages and rising wage costs. Companies including Wincanton and GXO Logistics rolled out new robotic picking systems at sites in the Midlands and South East. Industry bodies expect automation to drive productivity gains across British logistics throughout 2026, Sky News reported.

The main driver of the United Kingdom 3PL market is the increase in both domestic and international trade.

Third party logistics in the UK have grown significantly, creating a substantial number of jobs throughout the country.

Key players are attempting to achieve net zero emissions amid the growing trend of sustainability.

Compound Annual Growth Rate

2.6%

Value in USD Billion

2026-2035

Read more about this report - Request a Free Sample

Third party logistics providers are independent organisations that offer single or multiple logistics services to other businesses. This framework allows companies to outsource their supply chain activities such as inventory management and product distribution to specialised organisations.

Third party logistics providers perform a variety of functions, including inventory storage, packaging, warehousing, shipping, and distribution, among others. By outsourcing these services, organisations can benefit from cost-saving measures and flexible solutions tailored to their specific needs. Furthermore, the growing focus by businesses to minimise infrastructure costs and eliminate the need for storage and warehouse space, transportation, and shipment is aiding the United Kingdom third party logistics (3PL) market growth.

Third-party logistics companies, also known as 3PL or fulfillment providers, are crucial in the UK's supply chain. The logistics sector in the United Kingdom receives support from the government in the form of investments. For instance, in June 2023, the Department for Transport (DfT) announced £300,000 of government funding to support Generation Logistics, a campaign aimed at inspiring young people to pursue a career in the logistics industry.

Read more about this report - Request a Free Sample

Increasing cross-border trades, rise in employment opportunities, reduction in operating cost, and adoption of sustainable practices are the major trends impacting the United Kingdom third party logistics (3PL) market growth

| Date | Company | Action |

| April 12th, 2023 | EGLO | Teamed up with third party logistics to strengthen its presence in the UK |

| May 12th, 2023 | AIT Worldwide Logistics | Extended its business domain in Europe by acquiring Mach II Shipping |

| Oct 23, 2023 | Kuehne+Nagel UK | Joined forces with the UK Government's 'Zero Emission HGV and Infrastructure Demonstrator Programme' |

| Trend | Details |

| Reducing operating costs | Third party logistics services are a crucial aspect of achieving supply chain efficiency and reducing operational expenses. |

| Rise in job opportunities | The logistics industry is one of the largest in the UK, employing approximately 1.25 million people, which is almost 4.1% of all UK jobs. |

| Adoption of sustainable practices by 3PL providers | To reduce their carbon footprint, third-party logistics companies are adopting environmentally friendly business practices and green initiatives. |

| Increase in cross border trade | The UK is an open economy with its trade relations expanded to different parts of the world. Easy movement of goods requires a robust logistics mechanism. |

| Integration of advanced technologies in 3PL services | Technologies like artificial intelligence and machine learning are increasingly integrated into 3PL services to optimise routes, provide real-time updates, and facilitate predictive maintenance. |

Due to the rise in e-commerce and trade activities, the demand for third-party logistics is expected to grow in the coming years. Favorable government regulations are also supporting the United Kingdom third party logistics (3PL) market expansion. Freight forwarders are consolidating their functions and services effectively by sharing centralised management facilities and logistic facilities to provide competent services.

Furthermore, third party logistics handles the supply chain and logistic operations of external businesses. By outsourcing fulfillment operations, customers of third-party logistics companies can save on investing in warehouse space, transportation, logistics labourers, distribution sites, retail outlets, e-commerce platforms, and logistics management software.

While a company may be a specialist in a particular industry with excellent product knowledge and customer relationships, managing the logistics of the supply chain is a completely different specialisation. Third-party logistics companies are supply chain experts who stay up to date on the best industry practices and developments. Their role is to help businesses ensure sustainable growth in terms of profitability and customer base, without the expense of physically expanding or relocating.

Cross-border trade is increasing due to more than 70 trade agreements signed by the UK with different countries. This facilitates the free flow of goods and services across borders, stimulating the growth of the United Kingdom third party logistics (3PL) market. Efficient integrated logistics services are required to export domestically manufactured goods, including transportation and logistics-related services management.

The EMR’s report titled “United Kingdom Third Party Logistics (3PL) Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

Market Breakup by Mode

Market Breakup by Services

Market Breakup by End Use

Read more about this report - Request a Free Sample

The demand for 3PL services from the retail sector is expected to increase in the coming years due to their ability to facilitate convenience and ease for customers.

The retail sector holds a significant portion of the United Kingdom third party logistics market share. The United Kingdom’s retail sector is continuously expanding due to untamed competition, multichannel strategies, and a rise in consumer demand. To adjust to these dynamics, retailers are embracing 3PL services to improve their customer services and gain a competitive edge.

The new era of e-commerce has changed the retail environment, further driving the demand for optimal 3PL services. Meanwhile, the automotive industry in the UK is renowned for premium and sports car marques including Aston Martin, Bentley, Caterham Cars, Daimler, and Jaguar. This also requires a robust supply chain, including third-party logistics.

Major players in the United Kingdom third party logistics (3PL) market are focusing on decarbonisation amid the rising trend of sustainability:

| Company | Established Year | Headquarters | Description |

| Kuehne + Nagel International AG | 1890 | Switzerland | International transport and logistics company |

| Deutsche Post AG | 1995 | Germany | German multinational supply chain management and package delivery company |

| Wincanton plc | 1925 | United Kingdom | Provides logistics and transport services, including supply chain management for businesses and high-capacity warehouses |

| Schenker AG | 1872 | Germany | German logistics company and a subsidiary of Deutsche Bahn |

Other players in the United Kingdom third party logistics (3PL) market are XPO, Inc., Yusen Logistics Co., Ltd., FedEx Corporation, Fidelity Supply Chain Solutions, and PostNord AB, among others.

In October 2023, Kuehne+Nagel UK partnered with the UK Government's £200 million 'Zero Emission HGV and Infrastructure Demonstrator Programme' to help the UK achieve its net-zero goals by transitioning heavy goods vehicles to operate with zero emissions. This initiative is in collaboration with Innovate UK, and it would bring approximately 370 zero-emission trucks and around 57 refueling and electric charging sites via four consortiums. Kuehne and Nagel's involvement is expected to play a vital role in decarbonising the UK's haulage sector.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market reached an approximate value of USD 30.99 Billion.

The market is estimated to grow at a CAGR of 2.60% between 2026 and 2035.

The market is estimated to witness a healthy growth during 2026-2035 to reach around USD 40.06 Billion by 2035.

The robust growth of the e-commerce sector and a rise in cross-border trade are the major drivers of the market.

The key trends aiding the market expansion include sustainable practices adopted by third party logistics companies and increased job opportunities.

Roadways, railways, waterways, and airways are the different modes of third party logistics (3PL).

Automotive, manufacturing, chemical, retail, healthcare and pharmaceuticals, and construction, among others, are the various end uses of third party logistics (3PL).

The major players in the market are Kuehne + Nagel International AG, Deutsche Post AG, Wincanton plc, Schenker AG, XPO, Inc., Yusen Logistics Co., Ltd., FedEx Corporation, Fidelity Supply Chain Solutions, and PostNord AB, among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Mode |

|

| Breakup by Services |

|

| Breakup by End Use |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.