Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

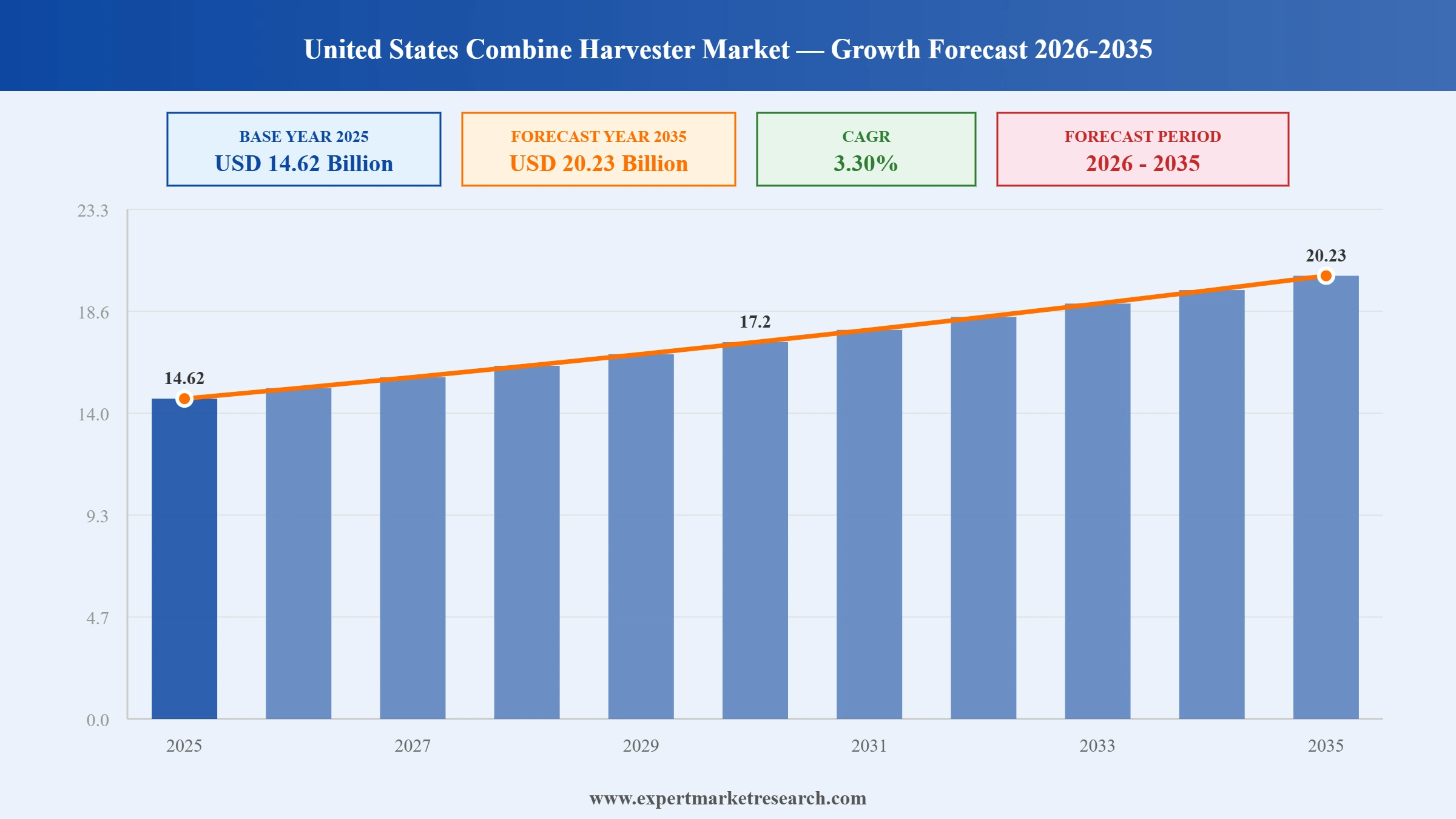

The United States Combine Harvester Market reached a value of USD 14.62 Billion at 2025 and is projected to expand at a CAGR of around 3.30% during the forecast period of 2026-2035. With ongoing farm consolidation creating demand for higher-capacity and technologically advanced combine harvesters, rapid deployment of autonomous and AI-enabled precision harvesting systems, persistent agricultural labour shortages accelerating machinery adoption, and crop production expanding across the 97 million hectares of US cultivated land, the market is expected to reach USD 20.23 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

| United States Combine Harvester Market Report Summary | Description | Value |

| Base Year | USD Billion | 2025 |

| Historical Period | USD Billion | 2019-2025 |

| Forecast Period | USD Billion | 2026-2035 |

| Market Size 2025 | USD Billion | 14.62 |

| Market Size 2035 | USD Billion | 20.23 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 3.30% |

| CAGR 2026-2035 - Market by Region | New England | 3.8% |

| CAGR 2026-2035 - Market by Region | Mideast | 3.5% |

| CAGR 2026-2035 - Market by Type | Self-propelled | 3.6% |

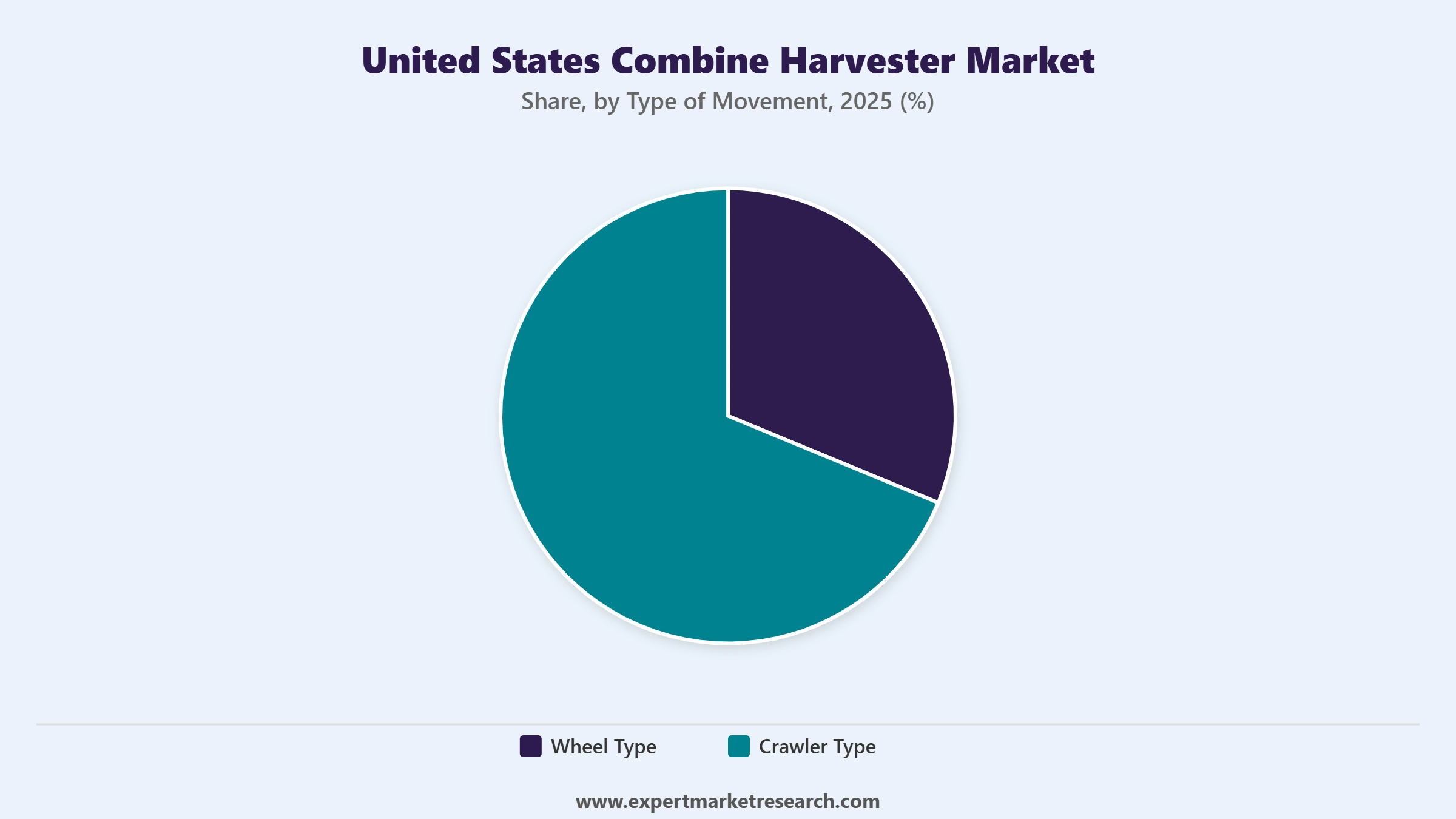

| CAGR 2026-2035 - Market by Type of Movement | Crawler Type | 3.7% |

| 2025 Market Share by Region | Great Lakes | 14.1% |

The United States Combine Harvester Market is being fundamentally reshaped by the convergence of autonomous technology deployment, large-scale farm consolidation, persistent labour availability pressures, and precision agriculture adoption. Together, these forces are lifting the performance and intelligence expectations farmers have for modern harvesting equipment, driving sustained investment in advanced combine harvester models across the forecast period.

In February 2025, John Deere unveiled a new generation of combine front-end equipment designed for enhanced field efficiency across US grain and row crop operations. The range includes a three-piece hinged draper reel system and an 18-row corn head engineered for improved throughput and reduced crop losses during harvesting. The launch was accompanied by expanded automation features, including predictive ground speed automation that continuously adjusts machine settings based on real-time crop conditions and harvest settings optimization to reduce operator input demands. These advancements reflect John Deere's continued investment in precision-enabled harvesting equipment for the US agricultural market.

In July 2024, Case IH, a flagship agricultural brand of CNH Industrial, launched the Axial-Flow 260 series of combine harvesters targeting US growers and custom harvesting operators. Built on Case IH's proprietary single-rotor technology, the 260 series is engineered to maximize throughput and grain handling capacity, catering to large-scale farming operations that require high daily harvest volumes. The launch reflects CNH Industrial's commitment to offering differentiated harvesting solutions across the US market, where operational efficiency and machine reliability are primary purchase drivers for professional growers.

In May 2024, John Deere launched a fully autonomous combine harvester pilot programme in the United States, deploying 68 machines across approximately 12,300 hectares of farmland in Iowa and Nebraska. The programme represents one of the largest real-world deployments of autonomous combine technology in commercial US agriculture to date. The machines operate using AI-driven navigation, real-time crop sensing, and automated yield monitoring systems that enable continuous harvesting without direct operator intervention. This initiative signals a pivotal shift in how large-scale American grain farming operations approach harvest automation and labour optimization.

In February 2024, John Deere unveiled its S7 Series combine harvesters alongside 830 horsepower 9RX series tractors and C-Series air carts at the Commodity Classic agricultural trade event held in Houston, Texas. The S7 Series is engineered for high-throughput grain harvesting with improved operator comfort features, integrated precision agriculture connectivity, and enhanced grain handling capabilities suitable for large US farm operations. The Commodity Classic launch provided John Deere with direct access to US grain growers, showcasing the company's latest portfolio of productivity-enhancing harvesting solutions for the American market.

In 2024, AGCO Corporation invested USD 140 million in a new Georgia-based manufacturing facility specializing in precision agriculture component integration for its agricultural equipment portfolio, including harvesting machinery. The facility focuses on the production of advanced sensor systems, automation hardware, and precision crop monitoring components that are integrated into AGCO's Massey Ferguson and Fendt equipment lines serving the North American market. This investment reinforces AGCO's strategic commitment to capturing growing demand for precision-equipped harvesting solutions among large-scale US farm operators.

Autonomous harvesting technology is transitioning from controlled trials to real-world field deployment across the United States, marking one of the most significant operational shifts in American grain farming in decades. Manufacturers are integrating AI-driven navigation, real-time crop monitoring, and machine-to-machine communication into combine platforms to deliver full harvest automation without continuous operator presence. The United States Combine Harvester Market growth is being reinforced by this trend as farmers seek to maximize machine utilization across extended harvest windows. In May 2024, John Deere deployed 68 fully autonomous combine harvesters across Iowa and Nebraska, operating across approximately 12,300 hectares in what represents one of the largest commercial-scale autonomous harvesting operations in the US to date.

Equipment manufacturers are embedding increasingly sophisticated automation layers directly into new combine hardware, moving beyond GPS guidance toward systems that continuously optimize machine performance in response to real-time field data. Predictive ground speed automation, automated harvest settings optimization, and multi-row crop-specific front-end configurations are becoming standard features across premium combine lines serving US grain producers. In February 2025, John Deere launched a new generation of combine front-end equipment incorporating a three-piece hinged draper reel system, an 18-row corn head, and expanded predictive automation capabilities, reflecting the industry's push toward machinery that adapts continuously to crop and field variability across diverse US agricultural zones.

The ongoing consolidation of US farmland into larger operating units, combined with persistent labour shortages in agricultural regions, is creating structural demand for higher-capacity, lower-operator-dependency combine harvesters. Farms exceeding 1,000 acres, particularly across the Midwest and Plains regions, increasingly require combine harvesters capable of processing larger daily grain volumes within narrow weather-dependent harvest windows. In 2024, AGCO invested USD 140 million in a new Georgia facility specializing in precision agriculture components, reflecting manufacturers' confidence in sustained demand for technologically advanced harvesting solutions as US farm operations continue to grow in scale and mechanization intensity.

As US grain farms grow larger, equipment manufacturers are competing intensely on throughput capacity, operational reliability, and multi-crop versatility to secure placement in high-value farm operations. Leading brands are launching new combine series specifically engineered for the operational realities of commercial-scale US grain, corn, and soybean production, where daily harvest volume and machine uptime are critical profitability drivers. In July 2024, Case IH launched the Axial-Flow 260 series, designed specifically for large US growers and custom harvesting operators, leveraging its proprietary single-rotor technology to maximize throughput capacity and grain handling efficiency across the diverse crop and terrain conditions of the American agricultural landscape.

The Expert Market Research's report titled “United States Combine Harvester Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

Market Breakup by Type

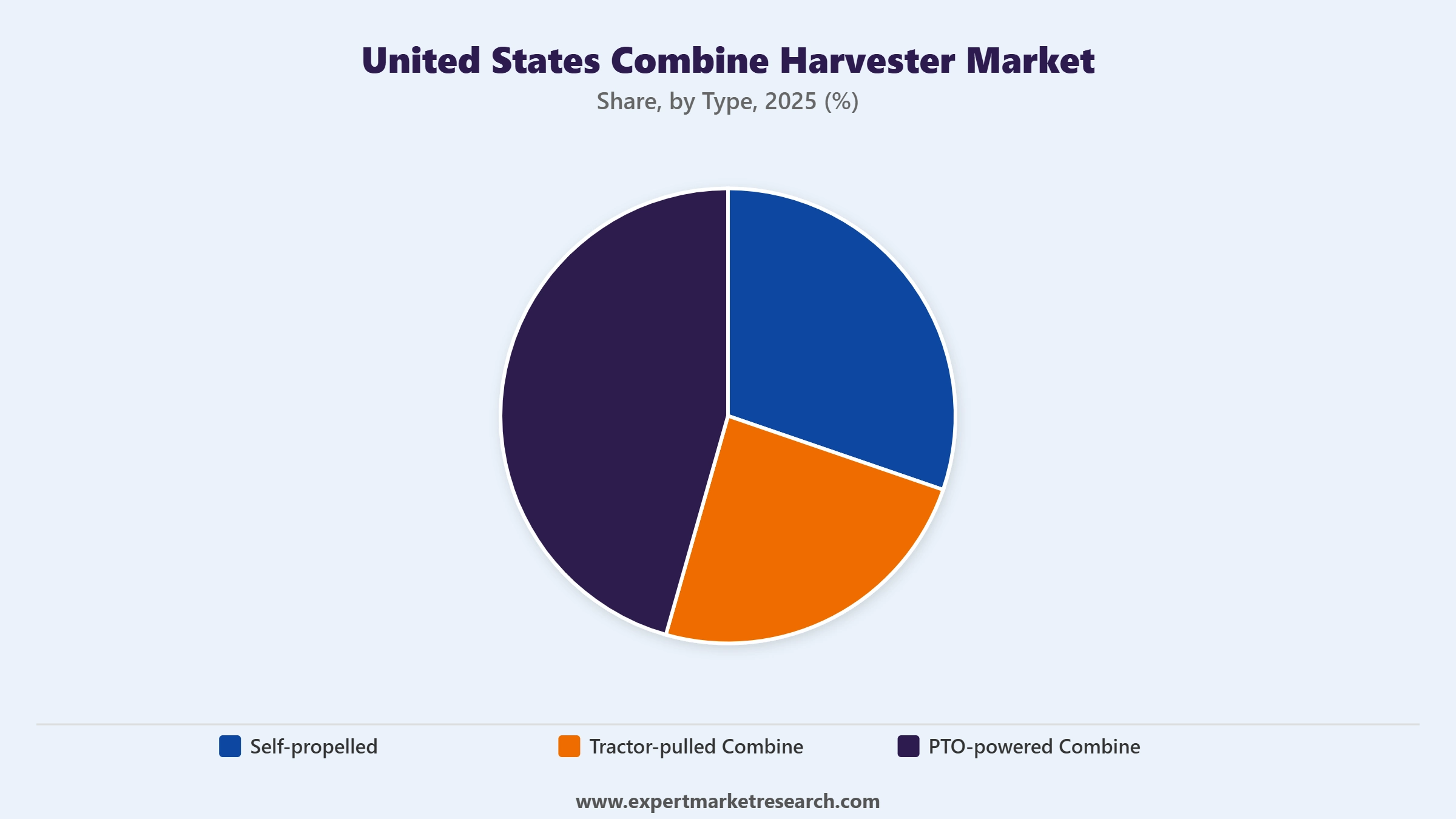

Key Insight: Self-propelled combine harvesters dominate the US market, accounting for the vast majority of market revenue and recording a forecast CAGR of 3.6% over the forecast period. Their ability to integrate reaping, threshing, and winnowing in a single internally powered machine makes them the preferred choice for large-scale US grain, corn, and soybean operations, where operational efficiency and harvest speed are critical. Over 70% of large US farms rely on self-propelled units, and manufacturers including Deere and Company and CNH Industrial continue to invest heavily in this segment with new model launches featuring advanced automation and precision agriculture integration. Tractor-pulled combine harvesters serve medium-scale farm operations that already possess powerful tractors and seek to expand harvest capability without purchasing an independent machine. PTO-powered combines remain relevant for smaller and specialized farm operations, particularly in the Southeast and Southwest where smaller farm footprints make lower-cost options more economical.

Market Breakup by Type of Movement

Key Insight: Wheel Type combine harvesters command the dominant share of the US market, benefiting from their operational versatility across the diverse terrain types encountered in American agricultural regions, from the flat, drained soils of the Corn Belt to the rolling fields of the Southeast. Wheel-type machines offer superior manoeuvrability and road transport capability, enabling custom harvesting operators to move efficiently between farms across multiple states during the harvest season. Crawler Type combine harvesters serve a specialized segment of the market, primarily addressing the needs of US farm operations in wetter, heavier-soil environments such as the rice-producing regions of the Mississippi Delta and California's Sacramento Valley, where conventional wheeled machines risk soil compaction and reduced traction. Advances in rubber-track crawler technology by brands including Deere and Company have expanded the appeal of crawler-type machines to larger, higher-horsepower combine platforms in recent years.

Market Breakup by Region

Key Insight: The Plains region is the dominant combine harvester market in the United States, encompassing the core grain-producing states of Iowa, Nebraska, Kansas, South Dakota, and North Dakota, which together host the highest concentration of large-scale wheat, corn, and soybean production in the country. The Great Lakes region, including Illinois, Indiana, and Ohio, represents the second most significant regional market, contributing major volumes of corn and soybean harvest that sustain consistent demand for high-capacity self-propelled combines. The Southeast is experiencing growing mechanization as more farm operations transition from labour-intensive to machine-assisted harvesting, particularly for soybean and cotton crops in states such as Mississippi, Alabama, and Georgia. The Far West, anchored by California's rice and specialty crop production, maintains steady demand for crawler-type and specialized harvest equipment suited to irrigated and wetter field conditions.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Type

Within the type segmentation, self-propelled combine harvesters account for the dominant market revenue share in the United States, reflecting both the scale of large-scale grain farming operations and the growing capital investment appetite of US farm operators seeking the most productive and technologically advanced harvest solutions. Leading brands including Deere and Company, CNH Industrial, and AGCO compete intensely within this segment, regularly introducing new model series with upgraded automation, precision crop monitoring, and fuel efficiency capabilities. The tractor-pulled combine segment retains meaningful revenue contribution from mid-sized farm operations, while PTO-powered combines serve value-oriented, small-to-medium farm businesses particularly concentrated in the Southeast and Southwest regions.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Type of Movement

Within the type of movement segmentation, wheel type combine harvesters command the majority of US market revenue, driven by their broad applicability across the flat-to-gently-rolling terrain that characterizes the dominant Corn Belt and Plains farming regions. Wheeled machines offer the operational flexibility needed by custom harvest contractors who service multiple farms across wide geographic areas during the season, and they benefit from lower unit costs and wider manufacturer support networks compared to crawler alternatives. Crawler type machines, while representing a smaller market share, command premium pricing due to their specialized capability in high-moisture and heavy-soil environments, creating a well-defined and stable demand niche within the overall US combine harvester market.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The Plains region is the largest and most strategically significant market for combine harvesters in the United States, driven by its role as the country's primary grain production zone. States including Iowa, Nebraska, Kansas, South Dakota, and North Dakota together account for a disproportionately large share of US wheat, corn, and soybean acreage, generating consistent and high-volume demand for large-capacity self-propelled combines throughout each harvest season. The region is also the primary deployment zone for autonomous and precision-enabled harvesting technology, with John Deere's May 2024 autonomous combine pilot programme deployed specifically across Iowa and Nebraska farmland. As farm consolidation continues to reduce the number of farm operators while increasing average farm size across the Plains, the shift toward higher-specification, higher-capacity combine harvesters is expected to intensify over the forecast period.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The Great Lakes region, which encompasses the corn and soybean-dominated agricultural states of Illinois, Indiana, and Ohio, represents the second most important regional combine harvester market in the United States. The region's farms are highly productive and largely mechanized, with significant adoption of precision agriculture technologies including yield mapping, variable-rate application, and harvest automation systems. Illinois alone is consistently ranked among the top US soybean and corn-producing states, generating substantial annual demand for machine replacements and upgrades. Manufacturer presence is strong in the region, with Deere and Company's Moline, Illinois headquarters and extensive Midwest dealer network providing strong service infrastructure. The Great Lakes region also benefits from high farmer income levels and access to USDA financing programmes that support equipment investment, sustaining robust combine harvester purchasing activity through economic cycles.

The United States Combine Harvester Market is highly consolidated at the top, with Deere and Company, CNH Industrial, and AGCO Corporation collectively commanding the majority of market revenue through their John Deere, Case IH, New Holland, and Massey Ferguson brands respectively. These three conglomerates benefit from extensive US dealer and service networks, strong brand recognition built over decades of agricultural equipment supply, and deep investments in precision agriculture and autonomous harvesting R&D. Japanese manufacturers Kubota and Yanmar hold smaller but growing shares, primarily in the mid-range and compact harvester segments, leveraging their engineering precision and fuel efficiency credentials.

Competition in the US market is increasingly driven by technology differentiation, as automation capability, telematics connectivity, and precision crop monitoring features become primary purchase criteria alongside traditional metrics of throughput capacity and reliability. Manufacturers that can demonstrate seamless integration with farm management software platforms and offer robust remote diagnostic and fleet management services are gaining competitive advantage, particularly among professional large-scale farm operations that manage multiple machines across diverse regional terrain.

Founded in 1890 and headquartered in Osaka, Japan, Kubota Corporation is a globally diversified agricultural machinery manufacturer with a growing presence in the US combine harvester market. Kubota offers a range of combine harvesters under its own brand and through its AGCO partnership arrangements, targeting mid-scale US grain and specialty crop farm operations. The company's US market strategy emphasizes fuel efficiency, compact machine dimensions suited to smaller field plots, and strong dealer-based service networks across agricultural states, with significant distribution infrastructure built through its extensive US dealer channel.

Founded in 1912 and headquartered in Osaka, Japan, Yanmar Holdings is a diversified industrial equipment manufacturer with agricultural machinery as a core business segment. In the US combine harvester market, Yanmar serves small-to-medium-scale farm operations and specialty crop producers, offering compact, fuel-efficient combine models suited to vegetable, rice, and grain operations in regions including the Far West and Southeast. Yanmar's US market presence is supported by its precision engineering heritage, strong after-sales service capability, and growing integration of smart agriculture technologies across its machinery platforms.

Formed in 2013 through the merger of CNH Global and Fiat Industrial, CNH Industrial N.V. is headquartered in Amsterdam, Netherlands, and operates the Case IH and New Holland Agriculture brands across the US combine harvester market. Case IH's Axial-Flow series are among the most widely used combines in large-scale US grain farming, particularly across the Plains and Great Lakes regions. CNH Industrial's scale of US dealer coverage, continuous investment in single-rotor and harvesting technology innovation, and strong presence in custom harvesting operations make it one of the two dominant forces in the American combine harvester segment.

Founded in 1837 and headquartered in Moline, Illinois, Deere and Company is the market leader in US combine harvester sales through its John Deere brand. The company's S Series and X Series combine platforms command the highest market share among large-scale US grain and row crop producers, supported by an industry-leading dealer network and the John Deere Operations Center digital farm management platform. Deere's USD 3.5 billion investment in autonomous and electric agricultural machinery underscores its commitment to maintaining technology leadership across the full US harvesting equipment spectrum through 2035 and beyond.

Other key players in the market are Iseki and Co. Ltd., AGCO Corp., CLAAS KGaA mbH, SDF Group, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Planning your next move in the US agricultural equipment sector? Our 2026-2035 report on the United States Combine Harvester Market delivers comprehensive market sizing, segment forecasts, regional growth analysis, and detailed competitive intelligence on the leading players driving innovation and market share across American grain country. Whether you are a machinery manufacturer, agricultural retailer, component supplier, or institutional investor, this report provides the intelligence foundation for confident strategic decisions. Download your free sample today and explore the full scope of opportunity in the US combine harvester market.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market attained a value of nearly USD 14.62 Billion.

The market is assessed to grow at a CAGR of 3.30% between 2026 and 2035.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach about USD 20.23 Billion by 2035.

The market is being driven by the increasing size of farms, expansion of the agricultural sector, and the rising emphasis on precision agriculture.

The major regions considered in the market are New England, Mideast, Great Lakes, Plains, Southeast, Southwest, Rocky Mountain, and Far West.

The major types of combine harvester in the market are self-propelled, tractor-pulled combine, and PTO-powered combine.

The major players in the market are Kubota Corporation, Yanmar Holdings Co., Ltd., CNH Industrial N.V., Deere & Company, Iseki & Co., Ltd., AGCO Corp., CLAAS KGaA mbH, and SDF Group, among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Type |

|

| Breakup by Type of Movement |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.