Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

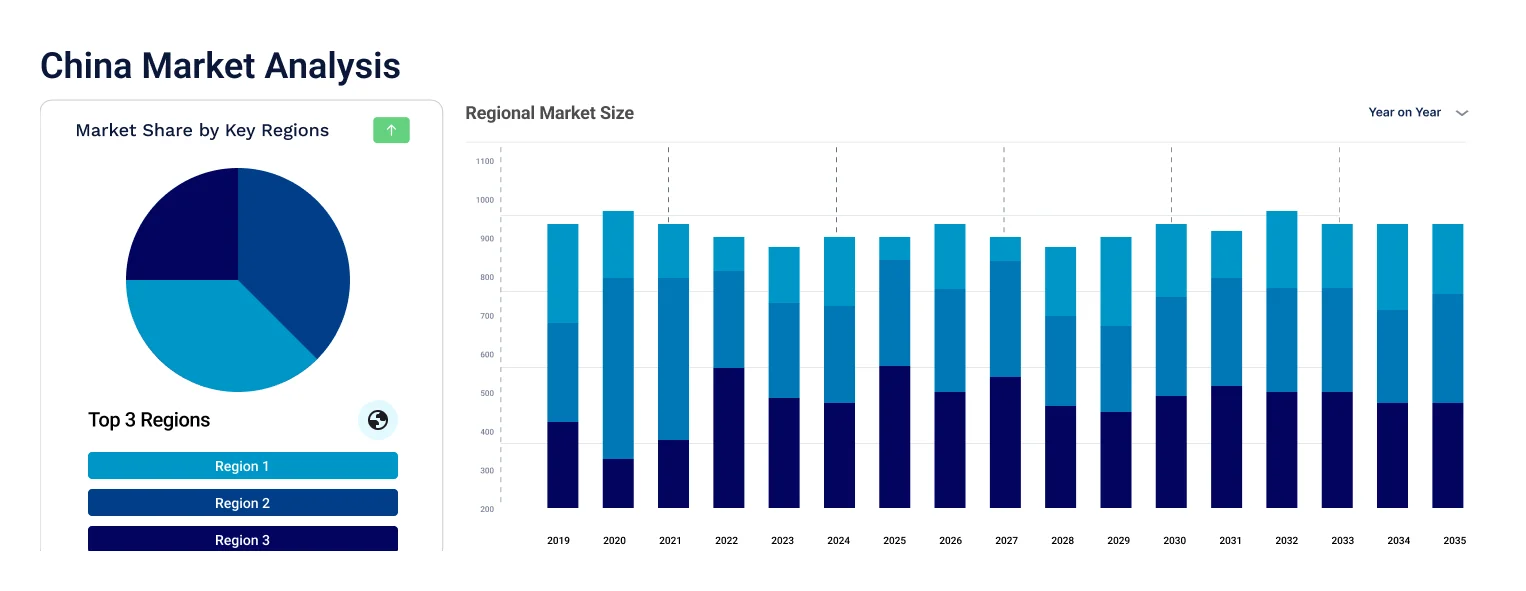

The China Proptech Market was valued at USD 6.80 Billion in 2025. The market is expected to grow at a CAGR of 17.20% during the forecast period of 2026–2035 to reach a value of USD 33.25 Billion by 2035. China's massive urban residential market, government-led smart city programmes, and rapid technology adoption across real estate platforms are catalysing a structural transformation of the country's property technology landscape.

The China proptech market analysis reflects a sector experiencing rapid expansion driven by China's large residential and commercial real estate stock, extensive government smart city investment programmes, and a domestic technology ecosystem capable of developing and deploying sophisticated proptech solutions at scale. China's smart city initiatives, funded through national and provincial budgets, have created an extensive digital infrastructure base incorporating GIS mapping, smart utility metering, and integrated urban management platforms that directly support proptech development. The country's large Internet user base, exceeding 1 billion people, and near-universal smartphone penetration have created a digital-first property search and transaction culture, with major platforms including Beike and 58.com serving hundreds of millions of property seekers annually.

China proptech market dynamics are shaped by a maturing ecosystem of dedicated real estate platforms and technology-enabled developer marketing tools. KE Holdings (Beike), China's leading integrated residential real estate platform, connects buyers, sellers, and agents through a digitised brokerage network supported by AI-driven property recommendation and transaction management systems. The company's platform connects over 450,000 agent stores across major Chinese cities. Alibaba Group's Taobao Fang and JD.com's real estate platform are expanding digital property transaction capabilities, while rental platforms including Ziroom and Mofang are digitising the long-term rental segment. Government digital economy policy frameworks continue to support proptech investment and platform development across Chinese cities.

Compound Annual Growth Rate

17.2%

Value in USD Billion

2026-2035

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

|

China Proptech Market Report Summary |

Description |

Value |

|

Base Year |

USD Billion |

2025 |

|

Historical Period |

USD Billion |

2019-2025 |

|

Forecast Period |

USD Billion |

2026-2035 |

|

Market Size 2025 |

USD Billion |

6.80 |

|

Market Size 2035 |

USD Billion |

33.25 |

|

CAGR 2019-2025 |

Percentage |

XX% |

|

CAGR 2026-2035 |

Percentage |

17.20% |

|

CAGR 2026-2035 - Market by Region |

Central and Western China |

18.6% |

|

CAGR 2026-2035 - Market by Technology |

Artificial Intelligence and Machine Learning |

19.3% |

|

CAGR 2026-2035 - Market by Solution Type |

Transaction Platforms |

16.8% |

|

2025 Market Share by Region |

East China |

29.3% |

The China proptech market is being reshaped by government policy packages stabilising the residential property market and stimulating digital platform engagement, alongside accelerating adoption of AI-powered property recommendation, automated valuation, and smart building technologies. New National Data Administration rules on property data commercialisation create fresh foundations for AI-driven proptech products.

Alibaba Group's Taobao Fang and JD.com's real estate division continued expanding their developer-facing digital property marketing and transaction platforms in 2025, adding AI-powered buyer analytics, virtual property tour features, and integrated financing applications. These platforms offer Chinese residential developers access to e-commerce-style buyer acquisition and property sales management, reflecting the China proptech market trend toward technology platform integration where massive existing consumer ecosystems become real estate transaction distribution channels.

KE Holdings, operator of China's largest residential real estate platform Beike, continued expanding its AI-driven property recommendation engine and digital agent management system in 2025, leveraging machine learning algorithms trained on hundreds of millions of property transaction records. The platform's Housing Dictionary database covers over 240 million property listings, enabling AI-powered personalised search, automated valuation, and predictive buyer behaviour analytics that reflect the China proptech market analysis trend toward data-intensive intelligent property matching.

China's National Data Administration issued regulations in early 2025 governing the commercialisation of government-held real estate data, enabling licensed proptech firms to access verified property registration, transaction history, and urban planning data for AI-powered valuation and analytics products. The framework allows KE Holdings, Fang Holdings, and property analytics firms to build AI models trained on verified government property transaction records, creating a significant structural enabler for China proptech market growth in data-driven property intelligence services.

China's Ministry of Housing and Urban-Rural Development published a property market stabilisation policy package in January 2025, including measures to reduce first-home buyer transaction costs, simplify online mortgage application procedures, and expand digital pre-sales permit systems for new residential developments. The policy package directly benefits China proptech market companies facilitating buyer engagement and transaction management, with simplified digital mortgage integration becoming a competitive differentiator for online real estate portals targeting first-time homebuyers.

China's Ministry of Housing and Urban-Rural Development continued expanding its digital real estate transaction and property registration infrastructure in 2024, with national rollout of online property transaction verification, electronic contract signing, and digital mortgage application platforms. The government's digital real estate administration initiative reduces transaction friction and increases data transparency, creating a richer data environment for China proptech market companies developing analytics, valuation, and regulatory compliance products.

Ziroom, China's leading long-term apartment rental platform, launched upgraded AI-driven smart apartment management and tenant matching systems in 2024, deploying IoT sensors, smart access systems, and predictive maintenance modules across its managed rental portfolio in Beijing, Shanghai, Shenzhen, and Hangzhou. Ziroom's smart rental model integrates digital tenant lifecycle management with automated billing and maintenance scheduling, reflecting the China proptech market dynamics in managed residential rental technology.

China's National Development and Reform Commission and Ministry of Housing allocated continued investment to smart city digital infrastructure in 2024, expanding GIS property mapping, digital building permit systems, and integrated urban management platforms to 150 additional Tier 2 and Tier 3 cities. These government-funded investments create a data-rich environment that supports China proptech market platform expansion into smaller Chinese cities beyond Tier 1 urban markets.

AI-powered property valuation tools are rapidly displacing traditional manual appraisal methodologies in China's residential market. KE Holdings' automated valuation model, trained on over 240 million property listings and millions of historical transaction records, delivers real-time estimated prices with measurable accuracy improvements. These AI valuation tools reduce transaction negotiation friction and enable digital mortgage lenders to automate collateral assessment workflows at scale within the China proptech market scope.

China's proptech market is extending beyond its traditional Tier-1 city concentration as rising urban populations in secondary cities including Chengdu, Wuhan, Changsha, and Xi'an generate demand for digital property search, management, and transaction services. National proptech platforms are deploying localised product versions and mobile-first interfaces adapted to secondary city user behaviour patterns, reflecting the China proptech market growth opportunity in cities beyond the established Tier-1 metro cluster.

The Expert Market Research's report titled "China Proptech Market Report and Forecast 2026-2035" offers a detailed analysis of the market based on the following segments:

Market Breakup by Solution Type

Key Insight: Property management software is the dominant solution type in the China proptech market, reflecting China's large-scale residential and commercial property management sector that requires integrated software solutions for building operations, billing, maintenance, and community service management across millions of housing units. Transaction and digital brokerage platforms are the fastest-growing solution type within the China proptech market analysis, driven by government policies reducing digital transaction friction and the scaling of AI-powered buyer matching capabilities by platforms including KE Holdings (Beike) and Anjuke.

Market Breakup by End-User

Key Insight: Real estate developers are the highest-revenue enterprise end-user segment in the China proptech market, driving platform adoption of AI-enabled pre-sales, digital construction management, and smart community management solutions as major Chinese developers invest in technology-differentiated project delivery and buyer engagement. Individual buyers and renters constitute the largest user-base end-user segment, with consumer-facing platforms including Beike, Anjuke, and Taobao Fang collectively serving hundreds of millions of registered residential property search users across China's major urban markets.

Market Breakup by Technology

Key Insight: Artificial Intelligence and Machine Learning is the dominant and fastest-growing technology segment in the China proptech market scope, with a projected CAGR exceeding 19% through the forecast period, driven by widespread adoption of AI-powered property recommendation engines, automated valuation models, and predictive demand analytics by major platforms. Government National Data Administration regulations enabling real estate data commercialisation in 2025 have significantly expanded the data assets available for AI model training, accelerating the competitive differentiation of AI-capable platforms versus data-limited competitors.

Market Breakup by Region

Key Insight: East China leads the China proptech market by platform transaction volume and enterprise proptech adoption, anchored by Shanghai's position as China's highest-value residential and commercial real estate market and the region's deep technology enterprise base that drives rapid proptech innovation adoption. South China is the second-largest regional market within the China proptech market analysis, driven by Shenzhen's technology sector concentration and Guangzhou's large residential real estate transaction volume. Central and Western China cities are the fastest-growing regional segment as urbanisation investment extends Tier-2 proptech market demand.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Solution Type, Property Management Software dominates the market due to scale deployment across China's large residential and commercial building management sector

Property management software holds the dominant solution share within the China proptech market, reflecting China's vast residential housing cooperative and commercial property management sector. China's approximately 300 million urban housing units across apartment complexes of varying scale require integrated property management software for maintenance management, fee billing, resident communication, and regulatory compliance reporting. Major property management software providers serving this segment have achieved significant deployment scale across the managed residential sector.

Transaction and digital brokerage platforms are gaining the largest absolute revenue growth within the China proptech market scope, as government policies reducing digital transaction friction and AI-powered buyer matching tools improve conversion rates and transaction throughput. Smart building and IoT management solutions are gaining adoption among new high-specification commercial and premium residential developments, where integrated building automation, energy management, and resident service applications create recurring platform revenue for proptech providers.

By End-User, Real Estate Developers lead in enterprise revenue due to platform investment in AI pre-sales, digital community management, and smart project delivery tools

Real estate developers represent the highest-revenue enterprise end-user category within the China proptech market analysis, driving substantial platform investment as major Chinese developers adopt AI-enabled pre-sales management, digital construction management, and smart community operation systems to differentiate project delivery in a competitive residential market. Leading developers including Vanke, Poly Developments, and Greenland are deploying comprehensive proptech suites that integrate buyer digital engagement, smart home installation, and post-sale community service management.

Individual buyers and renters constitute the largest user-base segment within the China proptech market dynamics, with consumer-facing platforms collectively registering hundreds of millions of users across residential property search, rental discovery, and home purchase facilitation verticals. Government and municipal authorities are an emerging institutional end-user segment, adopting proptech analytics platforms for urban planning intelligence, RERA-equivalent regulatory compliance monitoring, and smart city real estate data integration.

By Technology, Artificial Intelligence and Machine Learning leads due to widespread platform adoption for property recommendation, valuation, and transaction automation

Artificial Intelligence and Machine Learning holds the largest and fastest-growing technology share within the China proptech market, driven by widespread platform investment in property recommendation engines, automated valuation models, demand prediction analytics, and conversational AI tools for buyer qualification and agent productivity enhancement. Government National Data Administration regulations enabling commercialisation of verified property data from government registration systems have significantly expanded the training data available for AI model development, widening the capability gap between AI-investing platforms and conventional listing portals.

IoT and smart building systems are gaining meaningful technology share within the China proptech market dynamics, particularly in premium residential developments and commercial real estate where smart access control, energy management, and predictive maintenance platforms generate recurring service revenue beyond the initial transaction. Blockchain adoption remains experimental, with select pilot projects in property title registry and smart contract-based rental agreements, though regulatory clarity for blockchain-based property rights instruments remains pending.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

East China dominates the market due to Shanghai's position as China's highest-value real estate market and the region's technology enterprise ecosystem driving rapid proptech innovation adoption

East China leads the China proptech market by platform transaction volume and enterprise proptech adoption, anchored by Shanghai's status as China's highest per-square-metre residential and commercial property market and the region's deep technology enterprise ecosystem spanning Zhejiang and Jiangsu provinces. Major proptech platforms including KE Holdings and Anjuke report their highest per-transaction revenue from the East China region, reflecting the premium valuation of Shanghai, Hangzhou, Nanjing, and Suzhou residential and commercial assets.

South China is the second-largest regional market within the China proptech market analysis, driven by Shenzhen's technology sector concentration and Guangzhou's large residential real estate transaction volume. North China represents a major volume market centred on Beijing's premium residential and commercial real estate segments, with government entity and enterprise proptech adoption concentrated in the capital. Central and Western China cities including Chengdu, Chongqing, and Wuhan are emerging as the fastest-growing proptech demand regions as urbanisation investment and Tier-2 city residential market expansion extends the China proptech market's geographic footprint.

|

CAGR 2026-2035 - Market by |

Region |

|

East China |

14.5% |

|

South China |

15.2% |

|

North China |

13.8% |

|

Central and Western China |

18.6% |

|

Others |

16.4% |

The China proptech market players landscape is dominated by KE Holdings (Beike) in the residential transaction and digital brokerage segment, with major internet platforms including Alibaba and JD.com extending into property transactions through their existing e-commerce ecosystems. Competition is characterised by intense rivalry for developer marketing relationships, AI technology investment, and geographic expansion into Tier-2 and Tier-3 city markets.

China proptech market companies are differentiating through three primary strategies: AI investment that enables more accurate buyer-property matching and reduces transaction time through automated valuation and document processing; deep developer integration that embeds proptech platforms into new project pre-sales and digital community management from project inception; and geographic expansion into secondary cities where government urbanisation investment and rising smartphone penetration are creating new addressable real estate transaction markets.

Founded in 2018 and headquartered in Beijing, China, KE Holdings operates Beike, China's largest online and offline platform for real estate transactions and services, serving millions of buyers, renters, and agents across more than 100 cities. Beike's Housing Dictionary covers over 240 million property listings. Key strength: KE Holdings' proprietary Housing Dictionary database and AI-powered buyer matching engine, trained on hundreds of millions of verified property transactions, provide an unmatched data asset moat in the China proptech market that enables personalised recommendation accuracy unavailable to data-limited competitors.

Founded in 1999 and headquartered in Beijing, China, Fang Holdings (formerly SouFun) operates China's longest-established real estate media and technology platform, providing property listing services, real estate data analytics, and developer marketing solutions across residential and commercial real estate segments. Key strength: Fang Holdings' two-decade data archive of Chinese real estate market transactions, pricing trends, and developer activity provides a historical data advantage for real estate analytics products and market intelligence services within the China proptech market that newer entrants cannot rapidly replicate.

Founded in 2008 and headquartered in Shanghai, China, Anjuke operates as part of 58.com's real estate classifieds ecosystem, providing residential property search, new home sales, and rental listing services across China's major cities. Anjuke focuses on high-traffic property discovery for individual buyers and renters in the secondary residential market. Key strength: Anjuke's integration within 58.com's broad online classifieds ecosystem provides access to the platform's extensive user base and cross-category traffic for residential property listing discovery, delivering high-volume consumer reach at competitive customer acquisition costs within the China proptech market.

Founded in 2005 and headquartered in Beijing, China, 58.com operates one of China's largest online classifieds platforms, with its real estate vertical delivered principally through subsidiary Anjuke, covering residential listings, new home sales, and rental services across hundreds of Chinese cities. The company was taken private in a landmark 2020 buyout following a decade as a NYSE-listed leader in China's digital classifieds sector. Key strength: 58.com's broad classifieds ecosystem and majority ownership of Anjuke give it direct access to a vast, diversified user base spanning property, employment, and local services, supporting cost-efficient cross-category traffic acquisition within the China proptech market.

Other key players in the China Proptech Market report include JD.com Real Estate Platform, E-House China Enterprise Holdings Ltd., Mofang Gongyu (Flats Apartment), Alibaba Group (Taobao Fang), Ziroom (Self-Renovation Rental), JD Property (JD.com), KE Holdings' Ziru rental platform, and regional smart city proptech vendors, among others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Explore the latest trends shaping the China Proptech Market 2026–2035 with our in-depth report. Gain strategic insights, future forecasts, and key market developments that can help you stay competitive. Download a free sample report or contact our team for customised consultation on China Proptech Market trends 2026.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the China Proptech Market reached an approximate value of USD 6.80 Billion.

The market is projected to grow at a CAGR of 17.20% between 2026 and 2035.

The key players include KE Holdings Inc. (Beike), Fang Holdings Ltd. (SouFun), Anjuke Inc., 58.com Inc., E-House China Enterprise Holdings Ltd., Alibaba Group (Taobao Fang), JD.com Real Estate Platform, Mofang Gongyu (Flats Apartment), Ziroom (Self-Renovation Rental), JD Property (JD.com), and KE Holdings' Ziru rental platform.

Key strategies include AI-powered platform development, government smart city programme integration, digital rental ecosystem expansion, and technology giant entry through e-commerce-style real estate platforms.

Key challenges include real estate sector regulatory tightening, developer financial stress impacting technology procurement, data privacy regulation compliance, and intense platform competition compressing monetisation margins.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

|

Report Features |

Details |

|

Base Year |

2025 |

|

Historical Period |

2019-2025 |

|

Forecast Period |

2026-2035 |

|

Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

|

Breakup by Solution Type |

|

|

Breakup by End-User |

|

|

Breakup by Technology |

|

|

Breakup by Region |

|

|

Market Dynamics |

|

|

Competitive Landscape |

|

|

Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.