Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

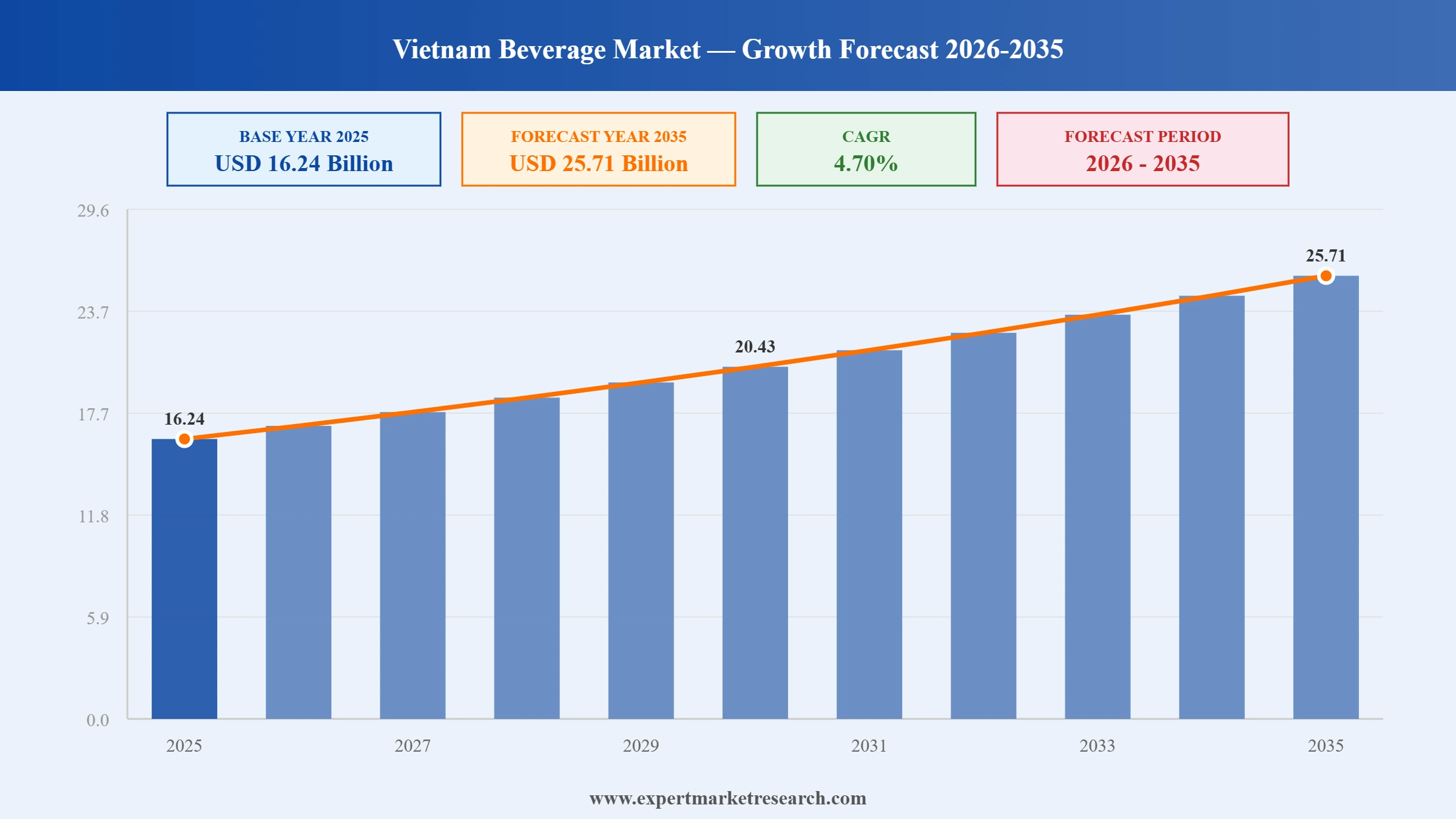

The Vietnam Beverage Market reached a value of USD 16.24 Billion at 2025 and is projected to expand at a CAGR of around 4.70% during the forecast period of 2026-2035. With rising health consciousness among Vietnamese consumers, robust e-commerce channel expansion, premiumisation across both alcoholic and non-alcoholic categories, and increasing foreign manufacturing investment, the market is expected to reach USD 25.71 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

|

Vietnam Beverage Market Summary |

Description |

Value |

|

Base Year |

USD Billion |

2025 |

|

Historical period |

USD Billion |

2019-2025 |

|

Forecast Period |

USD Billion |

2026-2035 |

|

Market Size 2025 |

USD Billion |

16.24 |

|

Market Size 2035 |

USD Billion |

25.71 |

|

CAGR 2019-2025 |

Percentage |

XX% |

|

CAGR 2026-2035 |

Percentage |

4.70% |

|

CAGR 2026-2035 - Market by Region |

Southeast |

5.4% |

|

CAGR 2026-2035 - Market by Region |

Red River Delta |

5.0% |

|

CAGR 2026-2035 - Market by Product Type |

Non-Alcoholic Beverage |

5.3% |

|

CAGR 2026-2035 - Market by Distribution Channel |

Online |

6.1% |

|

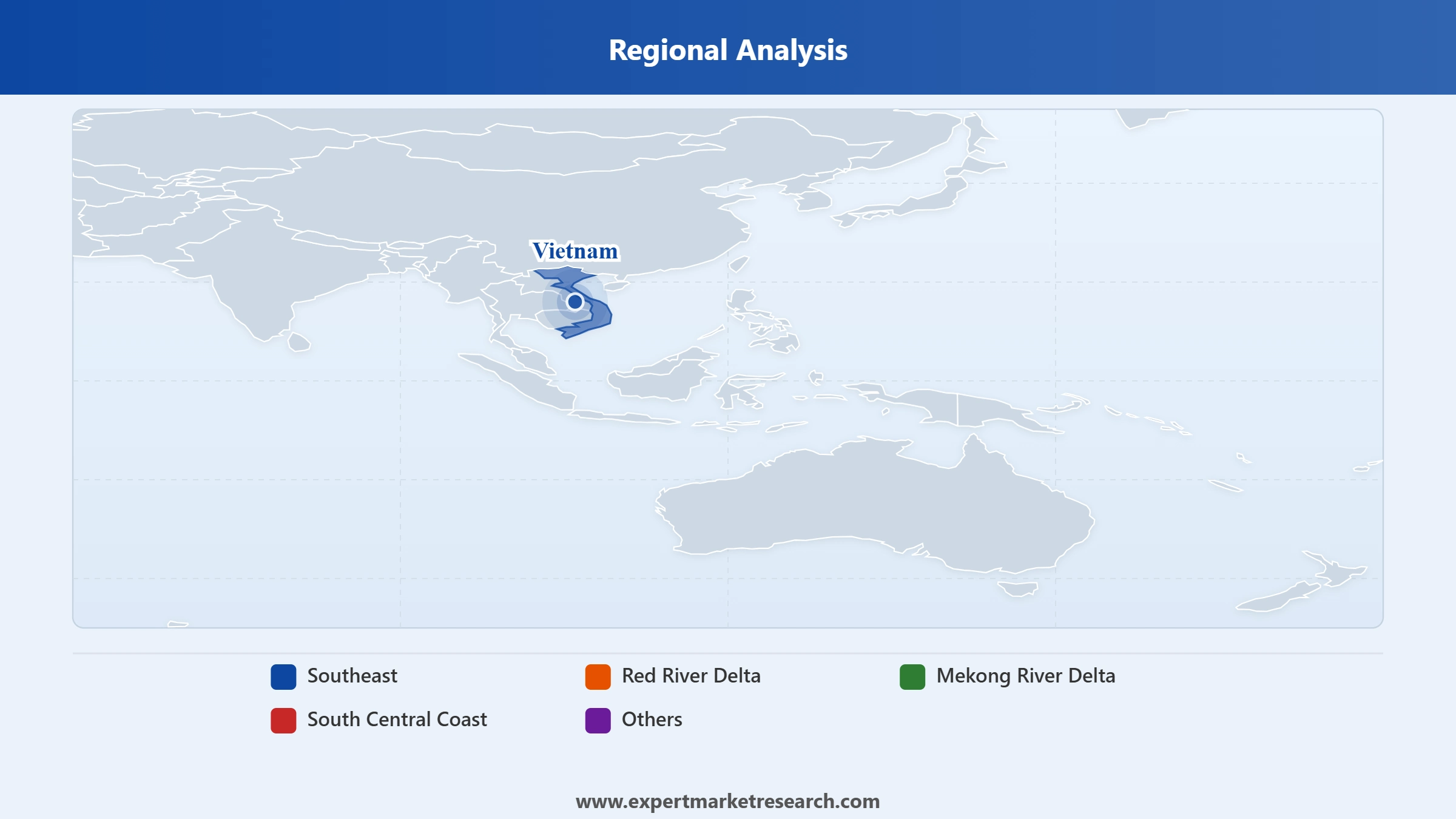

Market Share by Region 2025 |

Mekong River Delta |

15.4% |

Growing focus on health and wellness; the increasing trend of green consumption; rising demand for premium and craft beer; and the emergence of online delivery services are the major factors favouring the Vietnam beverage market growth.

In December 2025, Coca-Cola Beverages Vietnam set a nationally recognised record, acknowledged by the Vietnam Record Organisation (VietKings), for the creation of the largest artwork assembled entirely from 100,000 recycled PET (rPET) bottles at its Tay Ninh Province factory. The installation, composed of six curved walls stretching over 100 metres, served to highlight the company's ongoing sustainability journey and commitment to a circular economy in Vietnam. Coca-Cola Vietnam has been expanding its use of 100% rPET packaging across its Coca-Cola Original and Coca-Cola Zero Sugar product lines, with a stated ambition to eliminate approximately 2,000 tonnes of new plastic use in the country annually

In June 2025, Vietnam's National Assembly passed amendments to the Law on Special Consumption Tax, introducing the country's first-ever excise tax on sugar-sweetened beverages. Drinks containing more than 5 grams of sugar per 100 ml will face a 0% rate in 2026, rising to 8% from January 2027 and 10% from 2028. Products such as milk, 100% fruit juice, coconut water, and mineral water are exempt. The legislation, effective from January 2026, is expected to reshape product formulation strategies across the beverage industry, accelerating the shift toward low-sugar and functional drink offerings in both the alcoholic and non-alcoholic segments.

In April 2025, HEINEKEN Vietnam announced it had achieved its 2030 water balance ambition in the Tien River Basin five years ahead of schedule, replenishing over 690 million litres of water annually back into the local ecosystem. This milestone resulted from a sustained multi-year collaboration with the Ministry of Agriculture and Environment, WWF-Vietnam, and local provincial authorities. By the end of 2024, cumulative replenishment efforts in the Tien River Basin had exceeded 559 million litres. The achievement highlights HEINEKEN Vietnam's broader sustainability commitments and reflects the growing importance of environmental stewardship among leading beverage companies operating in Vietnam.

In October 2024, Suntory PepsiCo Vietnam Beverage announced plans to expand the annual production output of its under-construction Long An factory by approximately 56%, raising the target from an initial 796 million litres per year to 1.24 billion litres. To accommodate the scale-up, the company will relocate four production lines from its Ho Chi Minh City operations to the new facility. The expansion reflects the joint venture's confidence in Vietnam's long-term beverage consumption growth and its ambition to firmly consolidate market leadership in both carbonated and non-carbonated categories.

In April 2024, Suntory PepsiCo Vietnam Beverage commenced construction of its sixth and largest facility in the Asia-Pacific region, located in the Huu Thanh Industrial Park, Long An Province. The project, representing a total investment exceeding USD 300 million, spans approximately 20 hectares and is designed to achieve an annual production capacity of 800 million litres of beverages, including carbonated drinks and bottled water. The plant will be powered entirely by renewable energy sources, including biomass and solar power, and will use 100% recycled PET packaging, marking a significant step in Vietnam's foreign beverage investment landscape.

Vietnamese consumers are progressively moving away from high-sugar drinks, a shift that has gained legislative support with the passage of Vietnam's first sugar-sweetened beverage excise tax in June 2025. Brands are reformulating products to stay below the 5-gram-per-100ml threshold, and the non-alcoholic segment is seeing growth in RTD tea, low-calorie soft drinks, and functional waters. This trend is driving Vietnam beverage market growth in health-forward categories and pushing manufacturers to launch cleaner-label alternatives, particularly targeting younger, urban consumers who are more active in reading nutritional information. In June 2025, Vietnam's National Assembly passed the amended Special Consumption Tax Law, formally placing high-sugar beverages on the excise tax schedule for the first time.

Online beverage sales in Vietnam have accelerated substantially, propelled by the rapid adoption of social commerce through platforms such as TikTok Shop, Shopee, and Facebook Live. Convenience-driven consumers, particularly in Tier 1 cities, are ordering packaged beverages in bulk for home delivery, bypassing traditional wet markets and convenience stores. This distribution shift is especially pronounced in the bottled water, RTD tea, and energy drink sub-segments, where impulse purchase behaviour can be effectively captured through livestream promotions and flash discounts. In 2025, Suntory PepsiCo Vietnam Beverage ramped up production capacity at its under-construction Long An plant, in part to meet the growing demand generated through online and quick-commerce channels, reflecting how digital sales are directly informing manufacturing scale decisions.

Vietnam's rising middle class is gravitating toward premium and craft beverage options, moving beyond mass-market lagers and standard soft drinks in favour of imported craft beers, artisanal spirits, and premium RTD tea and coffee products. Hospitality sector expansion, particularly in tourist hubs such as Ho Chi Minh City and Da Nang, has amplified on-trade premium consumption. International players including Heineken and Diageo have responded by diversifying their Vietnam portfolios with higher-margin products targeting aspirational consumers. This premiumisation trend is notable in the Southeast and Red River Delta regions, where urban density and higher household incomes create a ready audience for value-added products.

Environmental sustainability has moved from a peripheral concern to a core brand differentiator in Vietnam's beverage sector. Leading multinationals are investing in renewable energy-powered breweries, water replenishment programs, and recyclable packaging materials. In April 2025, HEINEKEN Vietnam achieved its 2030 water balance ambition in the Tien River Basin five years ahead of schedule, replenishing over 690 million litres of water annually. Similarly, Coca-Cola Vietnam has committed to avoiding around 2,000 tonnes of virgin plastic annually by switching to 100% rPET bottle packaging. These moves are partly driven by consumer expectations and partly by Vietnam's evolving regulatory environment, which increasingly rewards green manufacturing practices.

The Expert Markt Research’s report titled “Vietnam Beverage Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

Breakup by Product Type

Key Insight: The Non-Alcoholic Beverage segment is the faster-growing category within Vietnam's beverage market, driven by increasing health awareness, the spread of modern convenience retail, and government legislation targeting high-sugar drinks. Beer continues to represent the largest component of the Alcoholic Beverage segment, with SABECO's Saigon Beer brand holding a dominant domestic share. The energy and sports drink sub-segment, led by brands such as Red Bull, is gaining traction among younger urban consumers. RTD tea and coffee are expanding rapidly, reflecting evolving on-the-go consumption habits in Vietnam's growing urban centres.

Breakup by Packaging Type

Key Insight: Bottles represent the dominant packaging format across Vietnam's beverage market, widely used across both alcoholic and non-alcoholic categories including beer, bottled water, soft drinks, and RTD beverages. The can format is gaining ground in the premium and on-the-go segments, particularly within the energy drink and craft beer sub-categories where portability and convenience are prioritised. The industry is also witnessing a material shift toward sustainable packaging, with leading players such as Coca-Cola Vietnam and Suntory PepsiCo committing to 100% recycled PET bottle usage, a trend that is gradually influencing consumer expectations around packaging standards.

Breakup by Distribution Channel

Key Insight: Offline distribution continues to command the majority of Vietnam's beverage sales, encompassing traditional wet markets, hypermarkets, convenience stores, restaurants, and on-trade outlets. However, the Online channel is the fastest-growing segment, expanding at a projected 6.1% CAGR through 2035, driven by social commerce, quick delivery apps, and growing consumer comfort with digital payment platforms. Platforms such as TikTok Shop, Shopee, and Lazada have become significant beverage sales venues, particularly for bottled water, energy drinks, and packaged juices. Leading brands are increasing their direct-to-consumer digital presence as e-commerce increasingly shapes purchase decisions in urban Vietnam.

Breakup by Region

Key Insight: The Southeast region, anchored by Ho Chi Minh City, is Vietnam's largest and fastest-growing beverage market, benefiting from the highest concentration of modern trade channels, an affluent urban consumer base, and major production facilities. The Red River Delta, centred on Hanoi, is the second-largest regional market and is home to significant brewing and beverage manufacturing operations. The Mekong River Delta represents a key growth frontier, supported by rising rural incomes, infrastructure improvement, and the growing reach of fast-moving consumer goods distribution networks. The South Central Coast, encompassing prominent tourism cities, is experiencing beverage consumption growth aligned with hospitality sector expansion.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

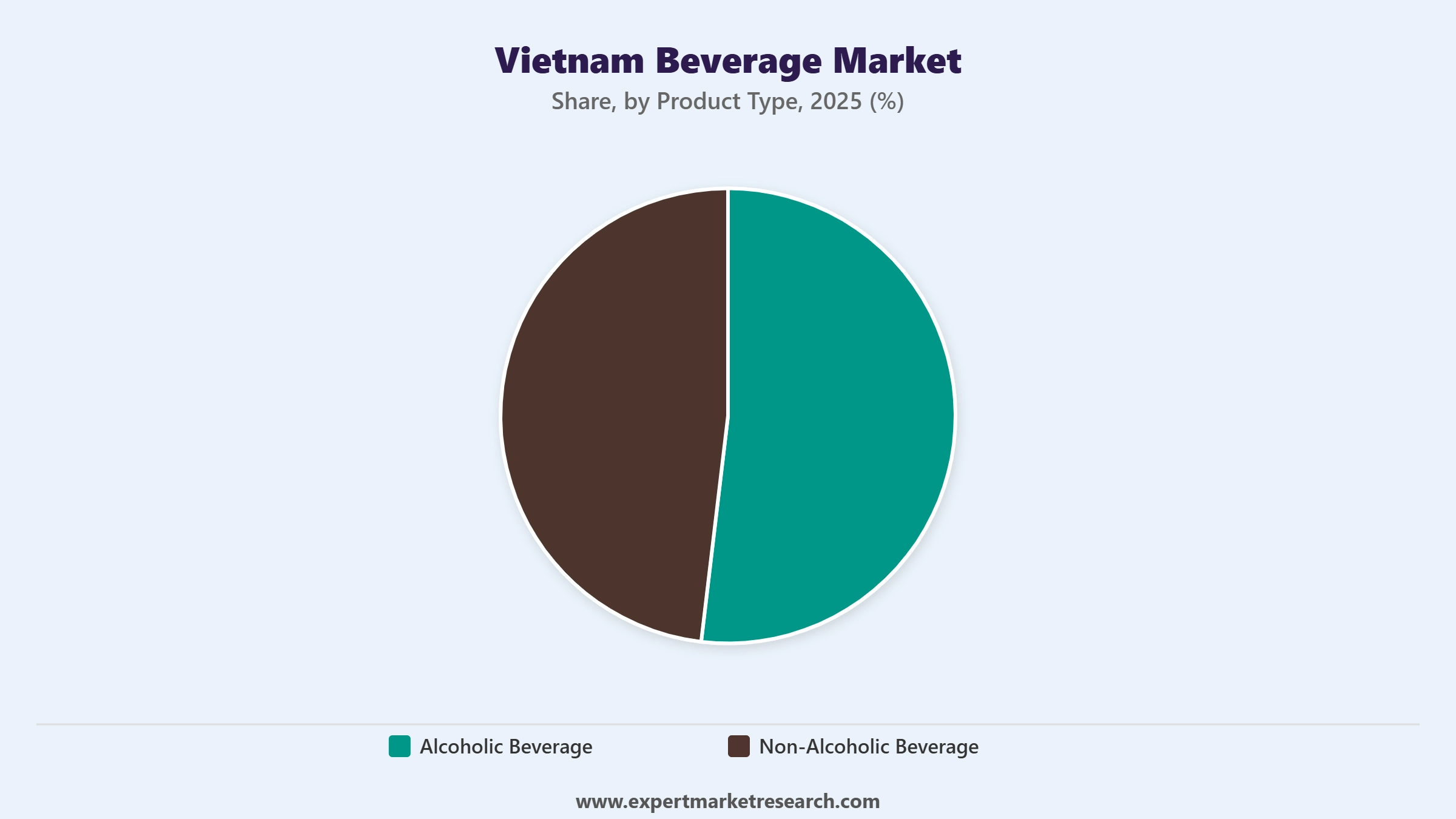

Vietnam's beverage market by Product Type is led by the Alcoholic Beverage segment in overall value terms, with Beer accounting for the bulk of this category's revenue. Vietnam has one of the highest per capita beer consumption rates in Southeast Asia, and domestic brands such as SABECO's Saigon Beer have maintained commanding market positions for decades. Beer's dominance reflects deep-rooted social consumption culture, affordable price points, and widespread availability across on-trade and off-trade channels. Within the Non-Alcoholic Beverage segment, Bottled Water and Soft Drinks represent the largest sub-segments by volume, though RTD Tea and Coffee and Energy and Sports Drinks are growing at a notably faster pace as health and lifestyle preferences evolve among younger Vietnamese consumers.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Within packaging, Bottles account for the majority of beverage packaging across Vietnam, reflecting their versatility across product categories from water and juice to spirits and beer. Bottles allow for a wide range of sizes and lend themselves to branding differentiation, which is particularly valuable in premium and craft beverage positioning. The Can segment holds meaningful share in the beer and energy drink categories and is growing steadily.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

In distribution, the Offline channel currently accounts for the dominant share of beverage sales, with wet markets, convenience stores, and supermarkets serving as the primary purchase touchpoints. However, the Online segment is expanding rapidly as Vietnamese consumers increasingly purchase beverages through digital platforms, making channel investment a strategic priority for both domestic and international players.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The Southeast region, centred on Ho Chi Minh City, is Vietnam's largest and most dynamic beverage market. It is home to a concentration of food and beverage manufacturing plants, including Suntory PepsiCo's flagship Long An facility under development, and hosts the densest network of modern trade retailers, on-trade outlets, and e-commerce distribution hubs in the country. The region's youthful demographic profile, high urbanisation rate, and above-average household incomes generate robust demand across both alcoholic and non-alcoholic product categories. A projected CAGR of 5.4% through 2035 reflects the Southeast's role as the primary growth engine of Vietnam's beverage sector, driven by premiumisation trends, expanding on-premise consumption, and the rapid rise of digital and quick-commerce channels serving urban consumers.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The Red River Delta, centred on Hanoi, is Vietnam's second-largest beverage market and a key production base for the domestic industry. The region's consumer profile is characterised by strong brand loyalty and a growing appetite for premium beverages, particularly in the craft beer and RTD tea segments. Government infrastructure investment in Hanoi's surrounding provinces has improved logistics connectivity, reducing distribution costs and enabling manufacturers to reach previously underserved semi-urban areas. HEINEKEN Vietnam operates significant brewing capacity in the region, and international spirit brands continue to expand their retail footprint across Hanoi's expanding middle-class neighbourhoods. The Red River Delta's well-developed organised retail sector provides a strong foundation for both domestic and imported beverage brands to compete effectively.

Vietnam's beverage market is moderately concentrated at the top, with a handful of international majors and one dominant domestic player, SABECO, collectively accounting for the largest share of production volume and revenues. Competition is particularly intense in the beer and soft drinks segments, where brand recognition, distribution reach, and pricing strategy are critical to market position. Global beverage corporations including The Coca-Cola Company, PepsiCo, Heineken, and AB InBev have maintained long-standing operations in Vietnam, continuously reinvesting in local manufacturing capacity and product localisation to retain their footholds.

The competitive landscape is also seeing the entry and expansion of niche and functional beverage brands targeting health-conscious consumers, particularly in the RTD tea, energy drink, and packaged juice sub-segments. Local players such as Interfresh Food and Beverage Company Ltd. and Saigon Beer Corporation have distinct advantages in regional distribution networks and consumer familiarity, while international firms leverage global R&D, branding, and sustainability credentials to command premium positioning. The passage of the 2025 Special Consumption Tax amendments is expected to sharpen competitive dynamics by accelerating product reformulation across the board.

Founded in 1866 and headquartered in Vevey, Switzerland, Nestlé SA is one of the world's largest food and beverage companies. In Vietnam, Nestlé operates across several beverage categories including ready-to-drink coffee, bottled water, and nutritional drinks. The company has invested significantly in its local manufacturing footprint and supply chain, leveraging its Milo, Nescafé, and Nestlé Pure Life brands to appeal to health-conscious and convenience-oriented Vietnamese consumers. Nestlé's broad distribution network and strong brand heritage position it as a key participant in Vietnam's growing non-alcoholic beverage segment.

Founded in 1892 and headquartered in Atlanta, United States, The Coca-Cola Company has operated in Vietnam since the early 1990s. The company markets a wide portfolio of carbonated soft drinks, still beverages, and water products through its Vietnamese bottling partnership. Coca-Cola Vietnam has committed to a circular economy agenda, transitioning its Coca-Cola Original and Zero Sugar lines to 100% rPET packaging to eliminate approximately 2,000 tonnes of virgin plastic use annually. The company's robust route-to-market infrastructure and global brand equity give it a durable competitive position across both urban and semi-urban Vietnamese markets.

Founded in 1864 and headquartered in Amsterdam, Netherlands, Heineken NV operates in Vietnam through HEINEKEN Vietnam, a joint venture with Saigon Trading Group. With six breweries and a portfolio spanning Heineken, Tiger, Larue, Bia Viet, and Strongbow, the company commands a substantial share of Vietnam's premium and mainstream beer segments. Heineken Vietnam has set sustainability benchmarks in the industry, achieving its 2030 water balance ambition in the Tien River Basin five years ahead of schedule in April 2025, and operates with 99% renewable energy across its Vietnamese brewing facilities.

Founded in 1875 and headquartered in Ho Chi Minh City, Vietnam, SABECO is the country's leading domestic beverage producer and the maker of the iconic Saigon Beer brand. The company commands one of the largest beer market shares in Vietnam, with its products distributed through an extensive nationwide network spanning modern trade, traditional outlets, and the on-trade sector. SABECO's deep local consumer relationships, broad regional distribution capabilities, and established production infrastructure make it a formidable domestic player, though it faces increasing competitive pressure from international brewers targeting the premium segment.

Other key players in the market are Red Bull GmbH, PepsiCo Inc., Diageo plc, Bacardi & Company Limited, AB InBev, Interfresh Food and Beverage Company Ltd., and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Unlock the full potential of Vietnam's fast-growing beverage sector with our comprehensive Vietnam Beverage Market Report 2026-2035. Discover the latest data on product innovation, shifting consumer preferences, and high-growth regional opportunities. Whether you're planning a new product launch, expanding your brand footprint, or seeking a detailed competitive landscape overview, this report equips you with the insights to move forward with confidence. Download your free sample today and take the first step into one of Southeast Asia's most dynamic beverage markets.

United States Out-of-Home Food and Beverage Market

Australia Sugar Free Food and Beverage Market

Australia Carbonated Beverages Market

Beverage Processing Equipment Market

Carbonated Beverage Market

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market reached an approximate value of USD 16.24 Billion.

The market is projected to grow at a CAGR of 4.70% between 2026 and 2035.

The market is estimated to witness healthy growth in the forecast period of 2026-2035 to reach a value of around USD 25.71 Billion by 2035.

The different regions considered in the market report include Southeast, Red River Delta, Mekong River Delta, and South Central Coast, among others.

The different types of products in the market are alcoholic beverages and non-alcoholic beverages.

The different types of beverage packaging are bottles and cans, among others.

The different distribution channels in the market are online and offline.

Key players in the market are Nestlé SA, Red Bull GmbH, The Coca-Cola Company, PepsiCo, Inc., Diageo plc, Bacardi & Company Limited, AB InBev, Heineken NV, Interfresh Food and Beverage Company Ltd., and Saigon Beer - Alcohol – Beverage Corporation, among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Product Type |

|

| Breakup by Packaging Type |

|

| Breakup by Distribution Channel |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.