Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

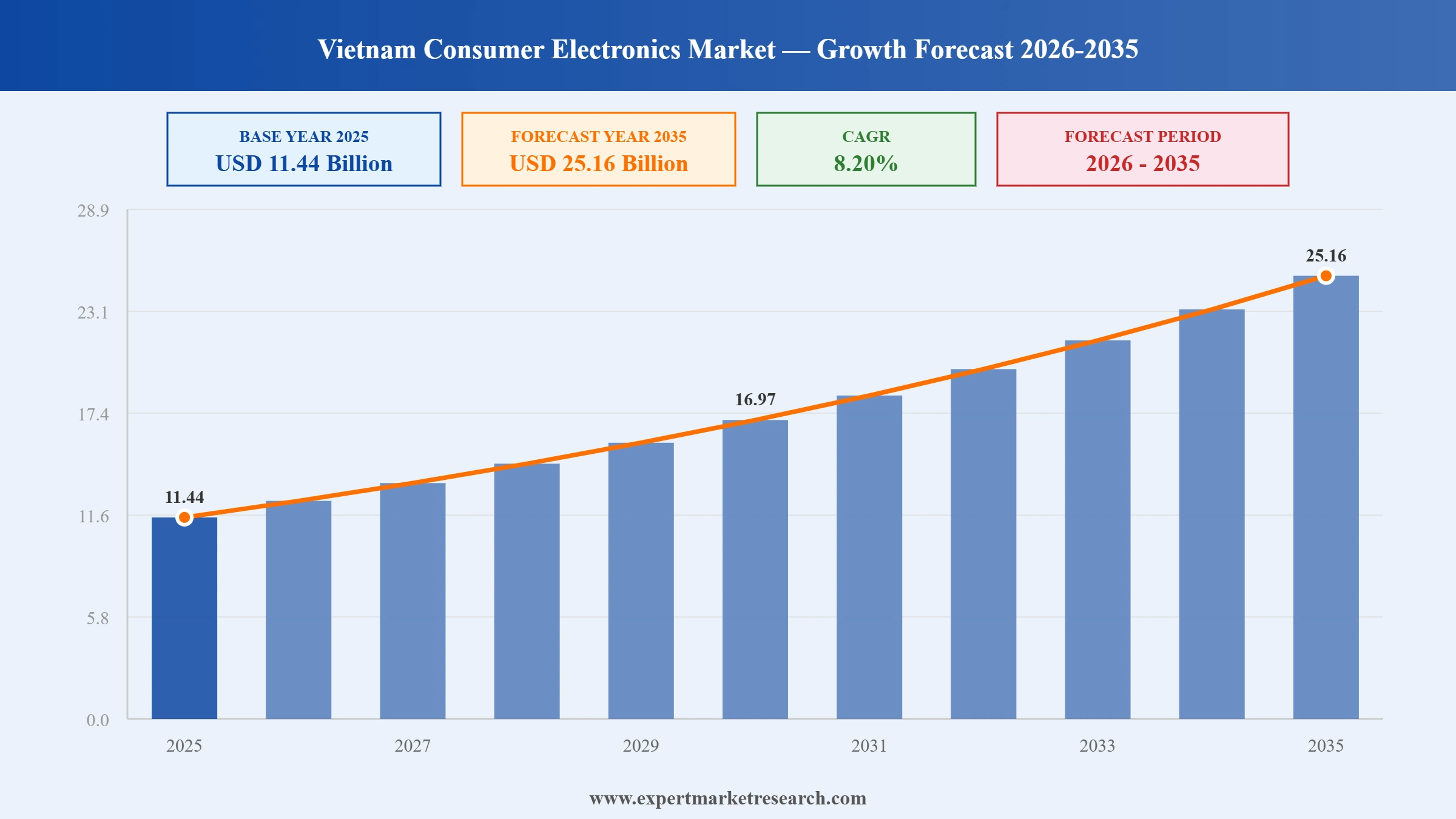

The Vietnam Consumer Electronics Market reached a value of USD 11.44 Billion at 2025 and is projected to expand at a CAGR of around 8.20% during the forecast period of 2026-2035. With rapid urbanisation driving demand for smart devices and connected home appliances, the expansion of 5G networks accelerating upgrades to next-generation smartphones and electronics, surging foreign direct investment in local electronics manufacturing, and e-commerce platforms becoming the dominant retail channel for consumer electronics, the market is expected to reach USD 25.16 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

| Vietnam Consumer Electronics Market Report Summary |

Description |

Value |

|

Base Year |

USD Billion |

2025 |

|

Historical Period |

USD Billion |

2019-2025 |

|

Forecast Period |

USD Billion |

2026-2035 |

|

Market Size 2025 |

USD Billion |

11.44 |

|

Market Size 2035 |

USD Billion |

25.16 |

|

CAGR 2019-2025 |

Percentage |

XX% |

|

CAGR 2026-2035 |

Percentage |

8.20% |

|

CAGR 2026-2035- Market by Region |

Southeast |

9.3% |

|

CAGR 2026-2035 - Market by Region |

Mekong River Delta |

8.4% |

|

CAGR 2026-2035 - Market by Product Type |

Electronic Devices |

8.7% |

|

CAGR 2026-2035 - Market by Distribution Channel |

Online |

14.6% |

| 2025 Market Share by Region | Red River Delta |

26.1% |

The Vietnam consumer electronics market is one of Southeast Asia’s most dynamic growth stories, powered by a youthful, digitally native population, accelerating urbanisation, an expanding 5G network, and the country’s emergence as a global electronics manufacturing hub. Consumers are trading up to premium devices while first-time buyers in smaller cities and rural areas are entering the market for the first time, creating a dual growth dynamic that sustains broad market expansion across price tiers.

The Vietnam International Electronics and Smart Appliances Expo held in May 2025 attracted over 350 electronics companies from Vietnam and China, serving as a major platform for showcasing the latest innovations in consumer electronics, home appliances, smart lighting, and IoT components. The event reflected the increasing maturity of Vietnam’s consumer electronics ecosystem, bringing together manufacturers, distributors, and retailers to explore collaboration opportunities, launch products, and assess emerging market trends. The expo underscored Vietnam’s rising profile as both a consumer electronics production hub and a growing domestic consumption market, with exhibitors presenting innovations spanning energy-efficient appliances, 5G-enabled devices, and AI-integrated smart home solutions.

Goertek, a major Chinese consumer electronics and acoustic components manufacturer, committed an investment of approximately VND 9,717 billion (around USD 391 million) to expand its manufacturing footprint in Vietnam in April 2025. The company, which produces earbuds, wearable devices, and audio components for global brands including Apple and Meta, sees Vietnam as a strategically important production hub within its Asia Pacific operations. This investment adds to Goertek’s existing Vietnam operations and underscores the broader trend of global electronics supply chains diversifying manufacturing capacity from China into Vietnam, driven partly by tariff and geopolitical risk considerations.

T3 Technology, a Vietnamese technology company, entered into a three-way partnership with Viettel Telecom, one of Vietnam’s largest telecom operators, and Tuya Smart, a global IoT platform provider, in March 2025 to accelerate the development of Vietnam’s smart home and Artificial Intelligence of Things (AIoT) ecosystem. The partnership combines Viettel’s nationwide network infrastructure, Tuya’s cloud-based IoT platform and device interoperability ecosystem, and T3 Technology’s local market expertise to create a scalable platform for smart home device connectivity in Vietnam. This collaboration signals the growing convergence between consumer electronics, telecom infrastructure, and AI-powered home automation in the Vietnamese market.

LG Electronics announced a strengthening of its research and development capabilities at its Vietnam operations in November 2024, broadening its local R&D program to encompass the webOS smart TV platform, vehicle electronic components, and home appliance technology. This expansion reflects LG’s recognition of Vietnam’s growing pool of engineering and software talent and its strategic importance as a manufacturing and innovation hub within the company’s global operations. By deepening R&D activity in Vietnam beyond pure manufacturing, LG is investing in the country’s capacity to develop proprietary technology for consumer electronics and connected home products with export potential across Asia Pacific.

Meta Platforms disclosed in October 2024 its intention to begin manufacturing virtual reality headsets in Vietnam starting from 2025, marking a significant milestone in Vietnam’s rise as a destination for high-value consumer electronics production. Meta’s decision to expand its hardware manufacturing to Vietnam aligns with the country’s growing roster of advanced technology production facilities, which already includes Samsung, Intel, and LG. VR and mixed reality headsets represent a high-growth consumer electronics category globally, and Meta’s Vietnam manufacturing commitment positions the country to participate directly in the production of next-generation wearable computing devices.

Vietnam has emerged over the past decade as one of the most important global destinations for consumer electronics manufacturing, and that trajectory is accelerating into a new phase. The combination of competitive labour costs, improving infrastructure, government incentives for foreign direct investment, and proximity to key Asian supply chains has made Vietnam an increasingly attractive alternative to China for electronics production. As trade tensions and supply chain diversification pressures grow globally, multinational electronics companies are directing substantial capital into Vietnam. The Vietnam consumer electronics market growth is being supported directly by these FDI inflows, which create jobs, raise incomes, and strengthen the domestic consumer base. In April 2025, Goertek invested approximately USD 391 million to expand its Vietnam operations, adding to the country’s existing footprint of Samsung, Intel, LG, and Meta production facilities.

Vietnamese consumers are increasingly interested in connected home devices that offer convenience, energy efficiency, and integration with smartphones and voice assistants. The smart home category, spanning smart speakers, security cameras, smart lighting, smart locks, and connected air conditioners, is growing rapidly as 5G coverage expands and broadband internet penetration deepens. Vietnam’s tech-savvy urban middle class is proving receptive to AIoT-enabled products, particularly in Ho Chi Minh City and Hanoi where household income levels support premium electronics purchases. Platform partnerships between telecom operators and global IoT providers are building the connectivity layer needed for seamless smart home experiences. In March 2025, T3 Technology, Viettel Telecom, and Tuya Smart formed a strategic alliance to accelerate smart home and AIoT development across Vietnam.

A notable qualitative shift is taking place in Vietnam’s electronics sector as leading multinational brands move beyond pure manufacturing to establish local research and development capabilities. This shift elevates Vietnam’s role in the global electronics value chain from an assembler of products designed elsewhere to a genuine contributor to product development, software engineering, and technology innovation. Local R&D investment by global brands creates higher-skilled employment, builds engineering talent pipelines, and positions Vietnam to attract more complex, high-value electronics investments over time. In November 2024, LG Electronics expanded its Vietnam R&D program to include work on the webOS smart TV platform, vehicle electronics, and home appliance technologies, reflecting the company’s confidence in Vietnam’s engineering workforce and its long-term commitment to the market.

Vietnam is not only growing as a consumer of established electronics categories like smartphones and home appliances, it is also positioning itself to participate in the production and early adoption of next-generation device categories such as virtual reality headsets, wearable devices, and AI-powered smart electronics. The arrival of manufacturing mandates for advanced consumer electronics from global brands signals confidence in Vietnam’s infrastructure and workforce quality. For Vietnamese consumers, the domestic production of premium electronics can over time reduce prices and improve product availability, accelerating adoption of categories that are currently early-stage. In October 2024, Meta announced plans to produce virtual reality headsets in Vietnam from 2025, making the country one of a small number of manufacturing bases globally for the company’s VR hardware.

The report of the Expert Market Research report titled “Vietnam Consumer Electronics Market Report and Forecast 2026 to 2035" offers a detailed analysis of the market based on the following segments:

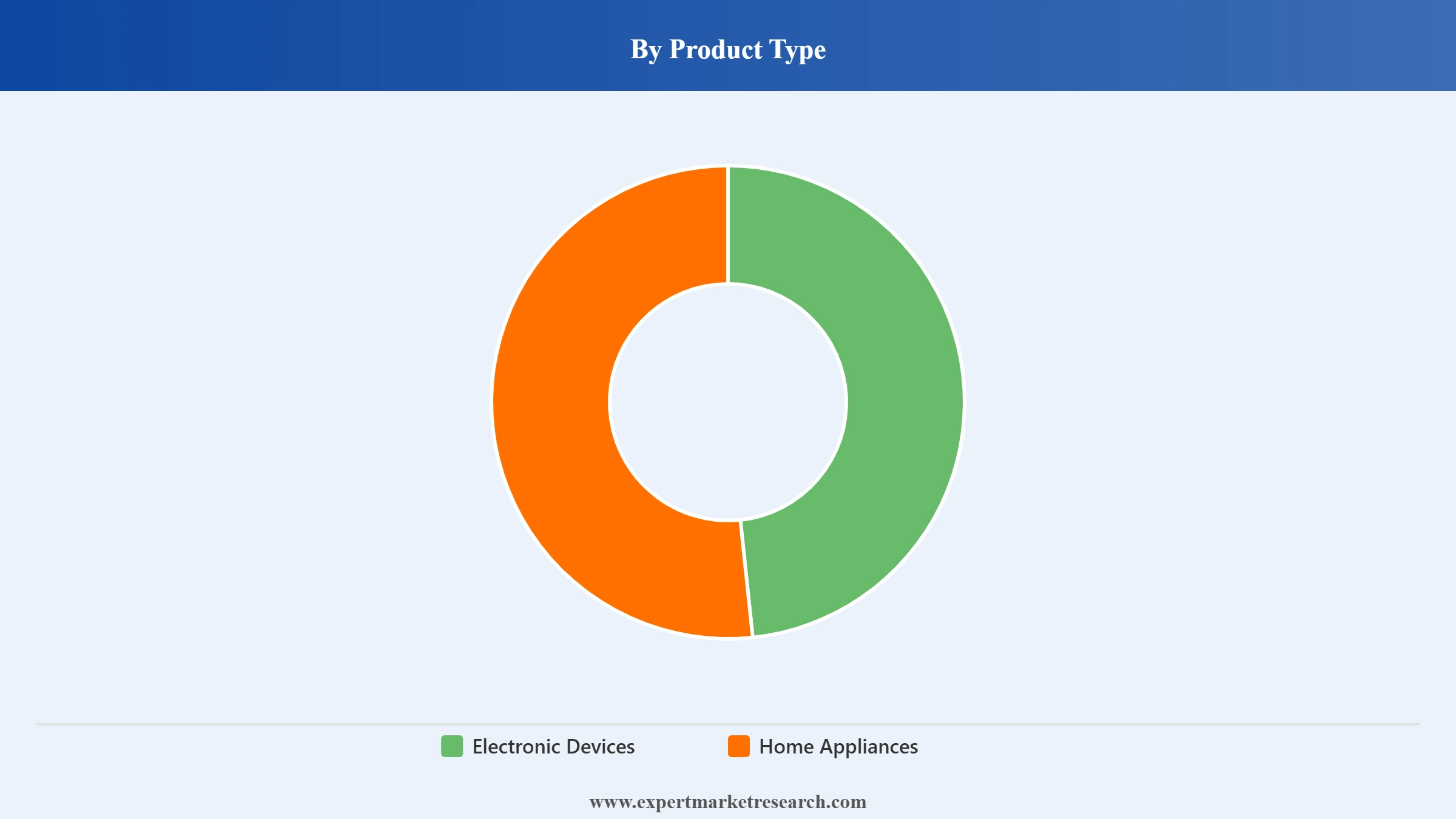

Market Breakup by Product Type

Key Insight: Electronic Devices is the dominant product type segment in Vietnam’s consumer electronics market, reflecting the country’s high smartphone penetration and growing appetite for personal computing devices. Approximately 84 million people in Vietnam used smartphones with apps in 2023, and ongoing 5G rollout is driving upgrade cycles for 5G-enabled handsets. Laptops and tablets are benefiting from the normalization of hybrid work and remote learning patterns, particularly in urban centres. Home Appliances represent the second major segment and are growing steadily as rising household incomes enable first-time purchases of refrigerators, washing machines, and air conditioners. Air conditioners are growing particularly fast given Vietnam’s hot climate and the expanding urban middle class. Smart home-enabled versions of traditional appliances are increasingly preferred by higher-income consumers.

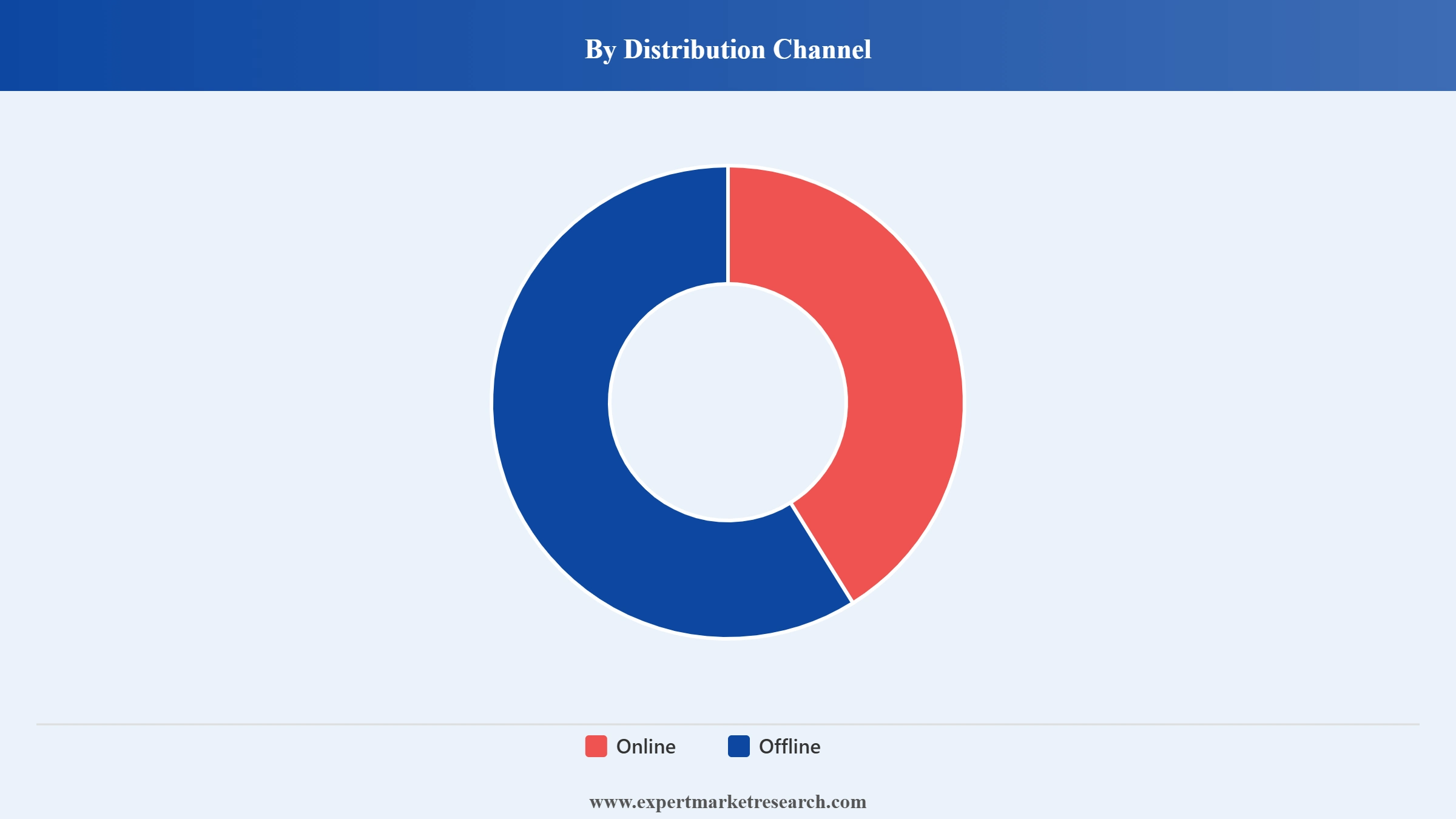

Market Breakup by Distribution Channel

Key Insight: Vietnam’s consumer electronics distribution landscape is being fundamentally reshaped by e-commerce, with online channels growing at a substantially faster pace than traditional offline retail. Consumer electronics led all product categories on Vietnam’s e-commerce platforms in 2025, accounting for approximately 26% of total e-commerce revenue. Platforms like Lazada, Shopee, and TikTok Shop are driving electronics sales among younger, mobile-first consumers who value competitive pricing, product variety, and convenient delivery. Mobile World Investment Corp, Vietnam’s largest consumer electronics retailer, reported strong 2025 revenues, reflecting the continued importance of the offline channel particularly for products where consumers want hands-on experience before purchase. The dual-channel model, combining physical stores for discovery and trust with online channels for price comparison and convenience, is increasingly the norm across urban Vietnam.

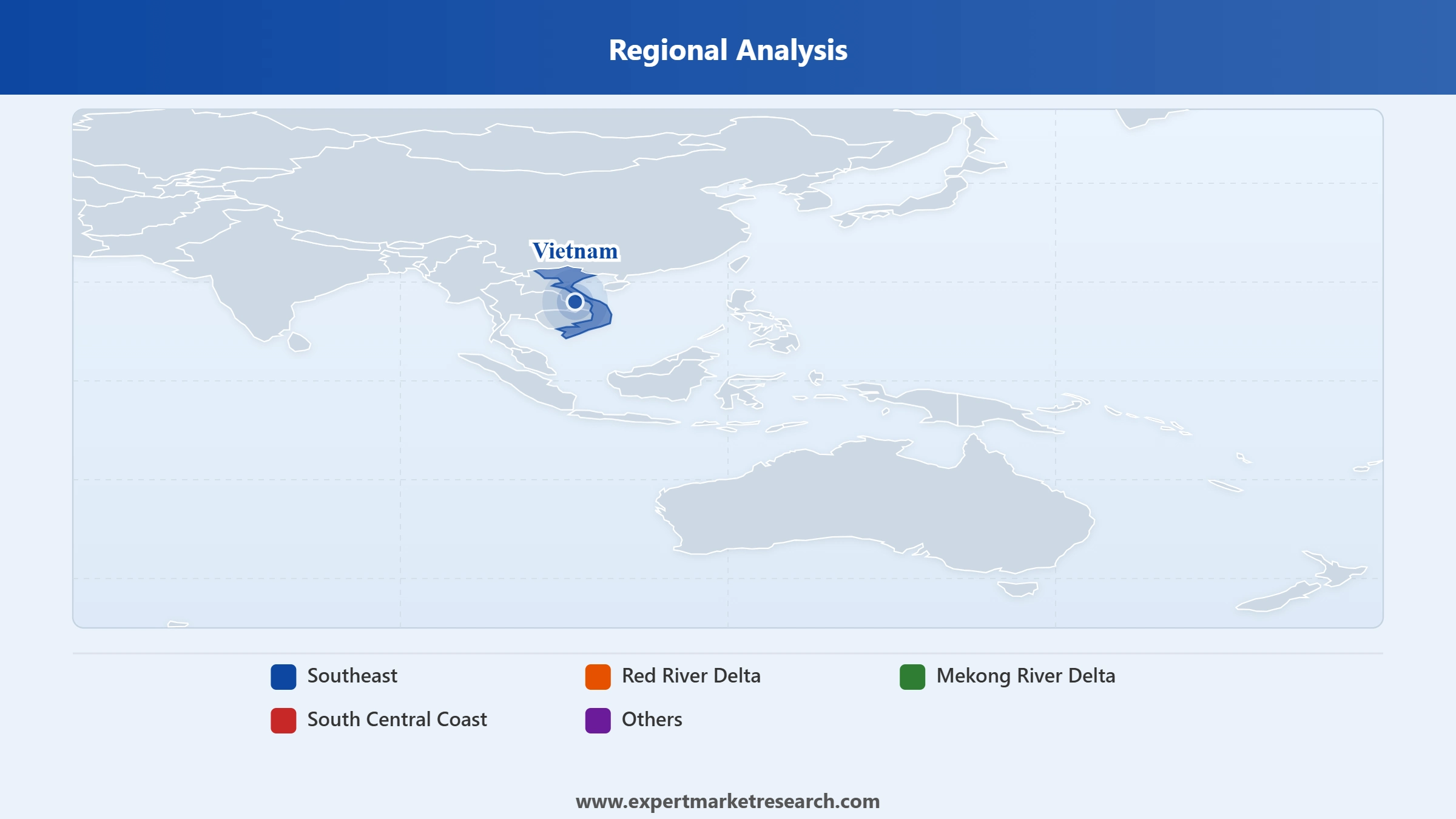

Market Breakup by Region

Key Insight: The Southeast region, anchored by Ho Chi Minh City, is Vietnam’s largest and most commercially sophisticated consumer electronics market. The city’s dense retail infrastructure, high household incomes relative to the national average, and strong e-commerce adoption make it the primary consumption zone for premium electronics brands. The Red River Delta, centred on Hanoi, is the second-largest market and has a significant concentration of technology retail flagships alongside growing online purchasing behaviour. The Mekong River Delta is an emerging market as rising agricultural incomes and improving digital connectivity expand access to consumer electronics in what was historically an underserved region. The South Central Coast, with cities like Da Nang and Nha Trang, is developing as a mid-tier consumer electronics market with growing tourist spending on electronics alongside rising domestic demand.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Product Type: Electronic Devices command the dominant share of Vietnam’s consumer electronics market, with mobile phones alone accounting for a substantial portion of total market value. Vietnam’s high smartphone penetration rate and active upgrade culture among its young population sustain robust demand for the latest handset models. Samsung and Apple together hold the largest combined share of the premium smartphone segment, while Xiaomi and Oppo lead in the budget-to-mid-range categories. Home Appliances represent the second-largest product category and are growing in significance as the country’s housing market expands and homeownership rates rise, driving first-time purchases of major household appliances. Smart, energy-efficient appliance variants are increasingly commanding a premium within this segment, particularly among urbanites in Ho Chi Minh City and Hanoi.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Distribution Channel: Offline channels, primarily through specialist electronics retailers and brand-owned stores, currently account for the majority of consumer electronics revenue in Vietnam, given consumers’ preference for seeing and testing devices before purchase. Mobile World Investment Corp dominates the offline retail landscape with its nationwide network. However, online channels are growing at a meaningfully faster rate and are rapidly closing the gap in market share, particularly for repurchases, accessories, and categories where consumers have high brand familiarity. E-commerce platforms’ competitive pricing, cash-on-delivery options, easy returns, and the convenience of mobile-first browsing are all contributing to accelerating online adoption across urban and suburban Vietnam.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Southeast Vietnam, centred on Ho Chi Minh City and its surrounding provinces, is the dominant consumer electronics market in the country by both revenue and consumer sophistication. The region’s high urbanisation rate, Vietnam’s largest concentration of multinational company offices, and a young professional population with rising disposable incomes create a self-reinforcing cycle of demand for the latest electronics. Flagship stores from Samsung, Apple, LG, and Xiaomi are concentrated in Ho Chi Minh City’s commercial districts, while e-commerce penetration in the city is among the highest in Southeast Asia. The region is also home to many of Vietnam’s electronics retailers’ headquarters, making it the key battleground for market share among distributors and retail chains. Samsung’s massive manufacturing complex in Binh Duong Province adjacent to Ho Chi Minh City underpins the region’s role as both a production and consumption hub for electronics.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Red River Delta, centred on Hanoi, is Vietnam’s second-largest consumer electronics market and the country’s political and administrative capital. Hanoi’s large civil service workforce, university student population, and growing private sector employment base create steady demand for laptops, tablets, and smartphones. The city’s electronics retail landscape, anchored by FPT Retail and Mobile World stores, is increasingly supplemented by strong online purchasing as residents embrace e-commerce. The government’s National Digital Transformation Program, centred on building a digital government by 2030, has accelerated technology procurement and IT spending within Hanoi’s public sector and educational institutions, generating significant B2B and institutional demand for laptops, peripherals, and enterprise-grade electronics.

Vietnam’s consumer electronics market is dominated by global technology brands competing across price tiers, distribution footprints, and product category breadth. Samsung holds a structurally advantaged position given its dual role as both a major manufacturer and a leading consumer brand in Vietnam, while Apple commands the aspirational premium segment despite higher price points. Chinese brands Xiaomi, Midea, and Daikin compete aggressively in the mid-range and home appliance segments with strong value propositions. Japanese brands including Sony, Panasonic, and Daikin retain loyalty in specific premium categories like audio and air conditioning.

The competitive dynamic is intensifying as more global brands establish local manufacturing and R&D, while e-commerce creates a more price-transparent environment that rewards brands with strong value-to-quality ratios. Vietnamese electronics retailers like Mobile World are increasingly influential in shaping brand visibility at the point of sale, giving distributors meaningful negotiating leverage over global brands. Local market knowledge, after-sales service quality, and financing options are emerging as competitive differentiators alongside product specifications and pricing.

Samsung Electronics Co., Ltd. was founded in 1969 and is headquartered in Suwon, South Korea. The company is Vietnam’s most prominent consumer electronics presence, both as a manufacturer and as a top-selling brand. Samsung operates major assembly plants in Thai Nguyen and Binh Duong Provinces, producing smartphones, tablets, and consumer electronics for global export as well as the domestic market. In Vietnam, Samsung holds leading positions across smartphones, televisions, and home appliances. The company’s comprehensive product portfolio spanning budget, mid-range, and premium tiers allows it to serve virtually all segments of Vietnam’s consumer market, reinforcing its position as the country’s most-recognised electronics brand.

Apple Inc. was founded in 1976 and is headquartered in Cupertino, California, United States. Apple occupies the premium tier of Vietnam’s consumer electronics market, with its iPhone, iPad, MacBook, and AirPods products consistently commanding the highest price points and strongest brand loyalty among urban professionals and younger consumers. Apple launched its official online Apple Store in Vietnam in May 2023, improving direct access for Vietnamese consumers and signalling the country’s growing commercial importance to the company. Vietnam is also playing a growing role in Apple’s manufacturing strategy, with suppliers like Goertek, Foxconn, and Luxshare producing Apple components and devices in the country.

Xiaomi Corporation was founded in 2010 and is headquartered in Beijing, China. Xiaomi has established a strong foothold in Vietnam’s consumer electronics market by offering smartphones, tablets, smart home devices, and home appliances at competitive prices that appeal to Vietnam’s price-sensitive but feature-conscious consumers. The company’s ecosystem approach, linking smartphones with a broad range of smart home products, aligns well with Vietnam’s growing smart home adoption trends. Xiaomi’s direct-to-consumer online sales model and aggressive retail store expansion in Vietnam’s major cities have made it one of the most visible mid-range electronics brands across the country.

LG Corporation was founded in 1958 and is headquartered in Seoul, South Korea. LG has a significant and deepening presence in Vietnam that goes beyond retail, encompassing manufacturing and research and development. The company operates major electronics manufacturing facilities in Hai Phong and is expanding its Vietnam R&D capabilities to cover webOS smart TV development, home appliance innovation, and vehicle electronic components. LG’s product portfolio in Vietnam includes premium OLED televisions, air conditioners, refrigerators, and washing machines, where the brand holds strong recognition among mid-to-high income consumers prioritising quality and energy efficiency.

Other key players in the market are Lenovo Group Limited, Sony Group Corporation, Dell Technologies Inc., HP Inc., Panasonic Holdings Corporation, Alphabet, Inc., Daikin Industries, Ltd., Midea Group, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Get ahead of the growth curve in one of Southeast Asia’s fastest-expanding consumer electronics markets. Our comprehensive report covers smartphone and home appliance demand dynamics, online versus offline channel evolution, regional opportunity maps, FDI trends, and profiles of the 12 leading brands shaping Vietnam’s consumer electronics landscape through 2026 to 2035. Whether you are a manufacturer, retailer, distributor, or investor, this report equips you with the data and insight to make confident decisions. Download your free sample now and discover the key opportunities in Vietnam’s thriving consumer electronics space.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

At 2025, the market reached an approximate value of USD 11.44 Billion.

The market is projected to grow at a CAGR of 8.20% between 2026 and 2035.

The market is projected to grow significantly during the forecast period 2026 to 2035 to reach USD 11.44 Billion in 2025

Vietnam’s consumer electronics market is driven by a powerful combination of demographic, economic, and policy forces. The country’s rapid urbanisation, with the urban population expected to exceed 50% by 2030, is creating first-time buyers for smartphones, appliances, and personal computing devices. Rising disposable incomes, particularly among the growing middle class where 60% of households are expected to earn over USD 5,000 annually by 2027, are fuelling premiumisation and upgrade cycles. Vietnam’s commercial 5G rollout is accelerating demand for 5G-capable devices across smartphones and other categories. Significant foreign direct investment by global electronics manufacturers is simultaneously improving the availability of locally produced devices and strengthening Vietnam’s consumer income base. The government’s National Digital Transformation Program is creating sustained public-sector and consumer demand for digital devices. E-commerce expansion is making electronics more accessible to consumers beyond major urban centres.

The Vietnam consumer electronics market is segmented by product type into Electronic Devices (Mobile Phones, Tablet, Laptop, Desktop Computers, Headphones and Speakers, and Others) and Home Appliances (Television, Refrigerator, Washing Machine, Air Conditioner, and Others). Electronic Devices represents the dominant product type, with mobile phones being the single largest sub-segment. Approximately 84 million Vietnamese had smartphones with apps in 2023, and ongoing 5G adoption is supporting upgrade demand. Home Appliances is growing steadily as household formation rates and incomes rise, with air conditioners and smart televisions showing particularly robust growth within this category.

The Vietnam consumer electronics market is being shaped by four key trends. First, Vietnam is consolidating its position as a major global electronics manufacturing destination, with significant FDI from Goertek, Meta, Samsung, and LG deepening the country’s production and R&D capabilities. Second, smart home and AIoT ecosystems are taking shape through partnerships between local technology companies, telecom operators, and global IoT platform providers. Third, global electronics brands are expanding R&D activity in Vietnam beyond manufacturing, elevating the country’s role in the global electronics value chain. Fourth, next-generation device categories including VR headsets and AI-integrated smart electronics are entering the market both as domestically produced and as imported premium products.

The key players in the market include Samsung Electronics Co., Ltd., Apple Inc., Xiaomi Corporation, LG Corporation, Lenovo Group Limited, Sony Group Corporation, Dell Technologies Inc., HP Inc., Panasonic Holdings Corporation, Alphabet, Inc., Daikin Industries, Ltd., Midea Group, and others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Product Type |

|

| Breakup by Distribution Channel |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.