Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

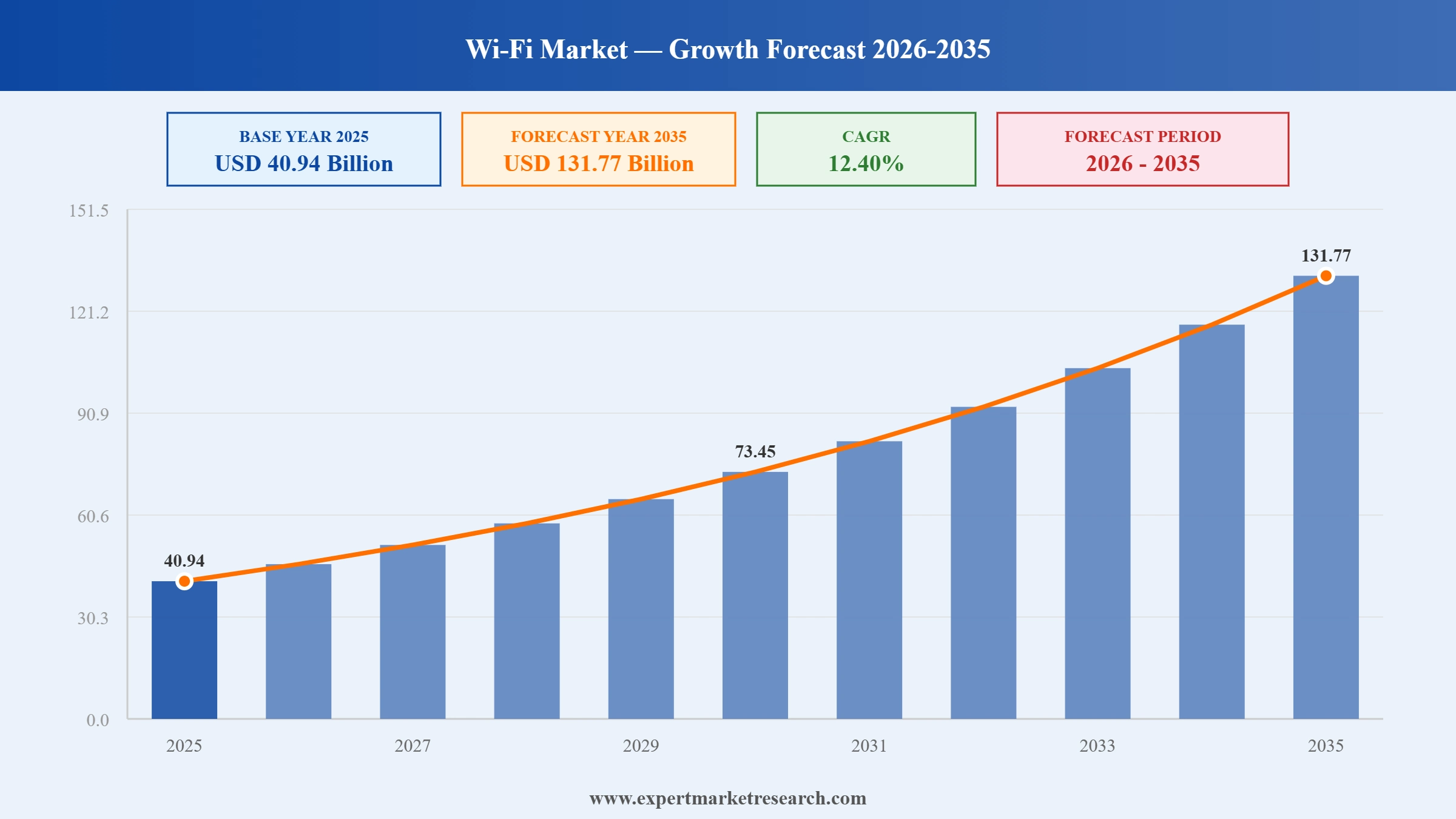

The Global Wi-Fi Market reached a value of USD 40.94 Billion at 2025 and is projected to expand at a CAGR of around 12.40% during the forecast period of 2026-2035. With the rapid adoption of Wi-Fi 7 standards across enterprise and consumer segments, growing proliferation of connected IoT devices, increasing government investments in public Wi-Fi infrastructure, and accelerating integration of AI-native network management, the market is expected to reach USD 131.77 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

| Global Wi-Fi Market Report Summary | Description | Value |

| Base Year | USD Billion | 2025 |

| Historical Period | USD Billion | 2019-2025 |

| Forecast Period | USD Billion | 2026-2035 |

| Market Size 2025 | USD Billion | 40.94 |

| Market Size 2035 | USD Billion | 131.77 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 12.40% |

| CAGR 2026-2035 - Market by Region | Latin America | 12.8% |

| CAGR 2026-2035 - Market by Country | India | 13.4% |

| CAGR 2026-2035 - Market by Country | Saudi Arabia | 13.1% |

| CAGR 2026-2035 - Market by Application Type | Outdoor | 12.9% |

| CAGR 2026-2035 - Market by Density | High-Density Wi-Fi | 13.2% |

| Market Share by Country 2025 | Brazil | 3.1% |

The global Wi-Fi market is at a genuine inflection point. Three decades of incremental improvements have given way to fundamental shifts in how wireless infrastructure is designed, deployed, and managed. Four trends stand out as the primary forces shaping the market today and through the remainder of the decade.

In July 2025, Hewlett Packard Enterprise officially completed its USD 14 billion acquisition of Juniper Networks after the US Department of Justice dropped its legal challenge to the transaction. Following the close, HPE's enterprise WLAN revenues - combining the Aruba and Juniper Mist portfolios - rose to a combined market share of approximately 19.3% in the third quarter of 2025 according to IDC data, positioning the combined entity as the most credible challenger to Cisco's dominant position in the global enterprise Wi-Fi market. The merger is expected to accelerate innovation in AI-native wireless network management.

In November 2024, Cisco introduced its next-generation Wi-Fi 7 access points, the CW9176 and CW9178 series, making them available to order in November 2024 with shipping commencing in December 2024. These access points are Cisco's first truly global models requiring no regional SKUs, intelligently detecting deployment location on activation. Built with native AI capabilities and unified subscription licensing, they support IEEE 802.11be with 320 MHz channel bandwidth and 4K QAM modulation. The launch positions Cisco to capture the next wave of enterprise Wi-Fi upgrades as organisations transition from Wi-Fi 6 and 6E.

In March 2024, CommScope announced a significant expansion of its US-based manufacturing capabilities for its fiber-optic connectivity portfolio, with production increases planned from summer 2024 to support the growing demand generated by BEAD programme-funded broadband projects. The expansion targeted Build America Buy America compliant fiber connectivity products, including splice closures, fiber distribution cabinets, and connectorised fiber terminals. As the parent company of Ruckus Networks, a key enterprise Wi-Fi brand, CommScope's manufacturing investments reinforce its broader strategy of scaling supply chain capacity to support accelerating wireless and broadband infrastructure deployments globally.

In January 2024, Fortinet announced the launch of its FortiAP 441K, becoming the first vendor in the industry to deliver a comprehensive Wi-Fi 7 secure networking solution that integrates wireless performance with AI-powered security services. The access point was paired with the FortiSwitch T1024, purpose-built with 10 Gigabit Ethernet access and 90W PoE technology to handle Wi-Fi 7 bandwidth requirements. By converging networking and security into a single platform, Fortinet established a differentiated position in the enterprise Wi-Fi market, targeting organisations seeking integrated connectivity and cyber protection without deploying separate solutions.

In January 2024, Hewlett Packard Enterprise announced its intention to acquire Juniper Networks for approximately USD 14 billion, a move that would combine HPE Aruba's enterprise Wi-Fi portfolio with Juniper's AI-driven Mist WLAN platform. The transaction, which attracted scrutiny from the US Department of Justice in early 2025, was ultimately cleared and completed in July 2025. The deal created one of the most significant consolidations in the global Wi-Fi and enterprise networking market, combining the second and fifth-largest WLAN vendors by revenue to form a stronger competitive counterweight to market leader Cisco.

The commercial availability of Wi-Fi 7 (IEEE 802.11be) represents the most significant leap in wireless standard capabilities in years, offering peak data rates exceeding 40 Gbps, multi-link operation across frequency bands, and substantially reduced latency. Enterprise IT decision-makers are increasingly prioritising Wi-Fi 7 infrastructure as the foundation for AI-native operations, augmented reality applications, and high-density venue connectivity. In November 2024, Cisco launched its first globally unified Wi-Fi 7 access point portfolio, the CW9176 and CW9178 series, shipping in December 2024 and designed to eliminate regional SKU complexity. This Global Wi-Fi Market growth milestone signals that the largest networking vendor views Wi-Fi 7 as a mass-market upgrade cycle rather than a niche deployment.

Traditional Wi-Fi access points and cybersecurity solutions have historically been purchased and managed separately, but the enterprise market is increasingly demanding integrated offerings that address both connectivity and security requirements from a single platform. Regulatory pressure, rising cyber threats targeting wireless networks, and the complexity of managing multiple vendor relationships are driving this convergence. In January 2024, Fortinet launched the FortiAP 441K, the industry's first Wi-Fi 7 access point with integrated AI-powered security services, positioning itself at the intersection of networking and cybersecurity. The development reflects a broader market shift where security-first vendors are competing directly with traditional networking equipment providers.

Artificial intelligence is no longer an optional overlay in enterprise Wi-Fi; it is fast becoming the operational baseline for network performance, security, and predictive maintenance. Vendors are embedding AI directly into access points and cloud management platforms, enabling real-time radio frequency optimisation, anomaly detection, and automated troubleshooting that reduces the burden on IT teams. In 2025, HPE's acquisition of Juniper Networks was driven in large part by Juniper's AI-driven Mist WLAN platform, which had been recognised as a leader in AI-native network management. Post-merger, the combined Aruba and Mist portfolio gives HPE one of the most comprehensive AI networking offerings available to enterprises globally.

Government-led smart city programmes and public broadband expansion initiatives are emerging as a meaningful demand driver for outdoor Wi-Fi infrastructure, complementing the traditionally dominant enterprise indoor segment. From transit hubs and municipal parks to educational campuses and healthcare facilities, public Wi-Fi networks are being positioned as essential civic infrastructure. In 2024, the US government's BEAD programme began driving significant demand for broadband-connected wireless infrastructure, prompting CommScope to expand US manufacturing capacity in March 2024. As digital inclusion policies gain traction across North America, Europe, and Asia Pacific, public sector Wi-Fi deployments are expected to represent a growing share of overall market demand through 2035.

The Expert Market Research's report titled “Global Wi-Fi Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

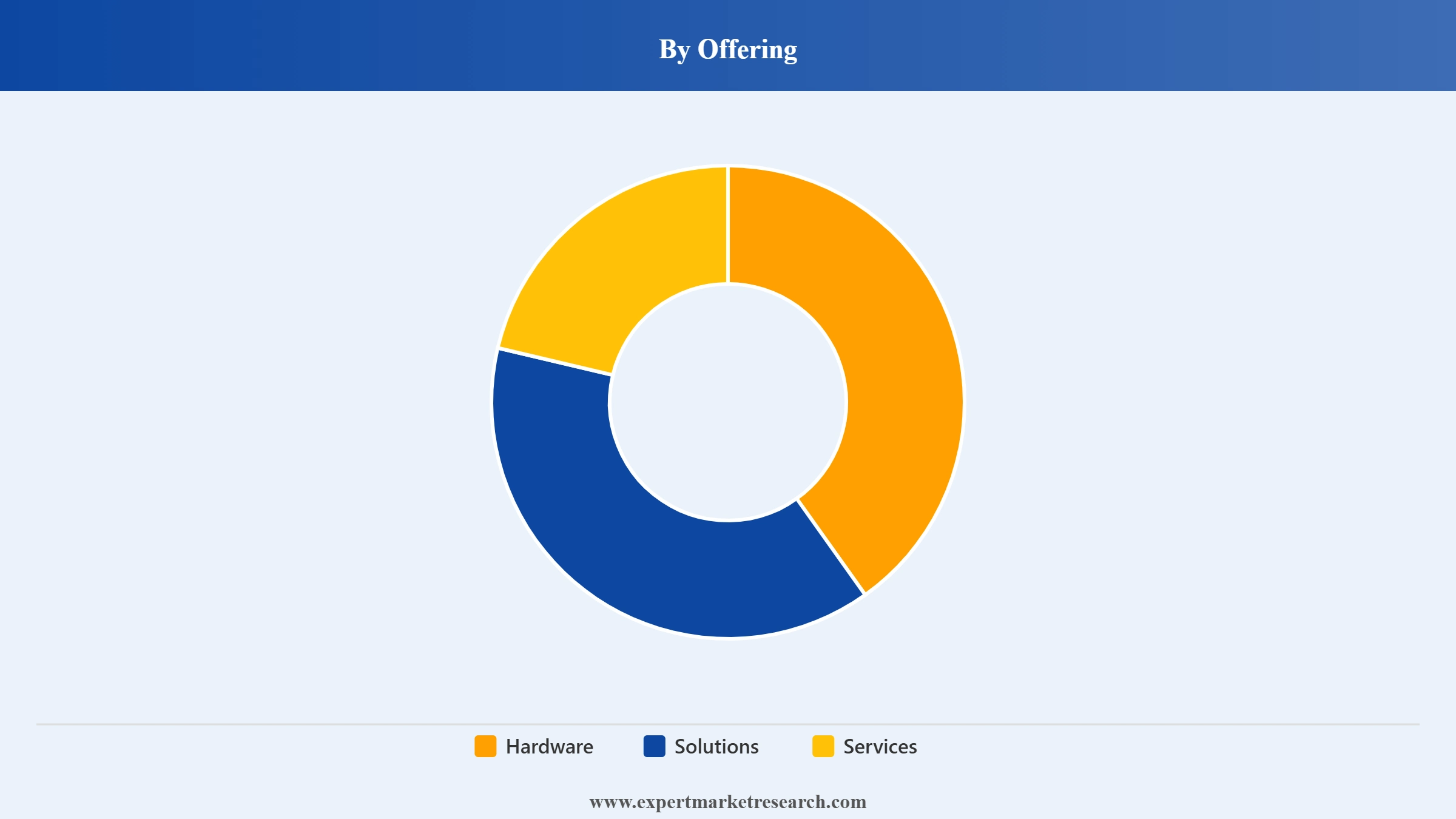

Market Breakup by Offering

Key Insight: The hardware segment holds the largest share within the Global Wi-Fi Market by offering, with access points representing the single most widely deployed hardware category. The ongoing enterprise-wide transition from Wi-Fi 6 to Wi-Fi 7 infrastructure has driven a fresh wave of access point procurement, with Cisco, HPE Aruba, and Huawei leading deployment volumes globally. WLAN controllers and wireless hotspot gateways are growing categories as network complexity scales across large enterprise and public environments. The solutions segment, encompassing cloud management platforms and network analytics, is the fastest-growing offering category, driven by demand for AI-powered network visibility tools. Services, including managed Wi-Fi and professional services, are gaining traction as mid-market and public sector organisations increasingly outsource wireless network operations to specialist providers.

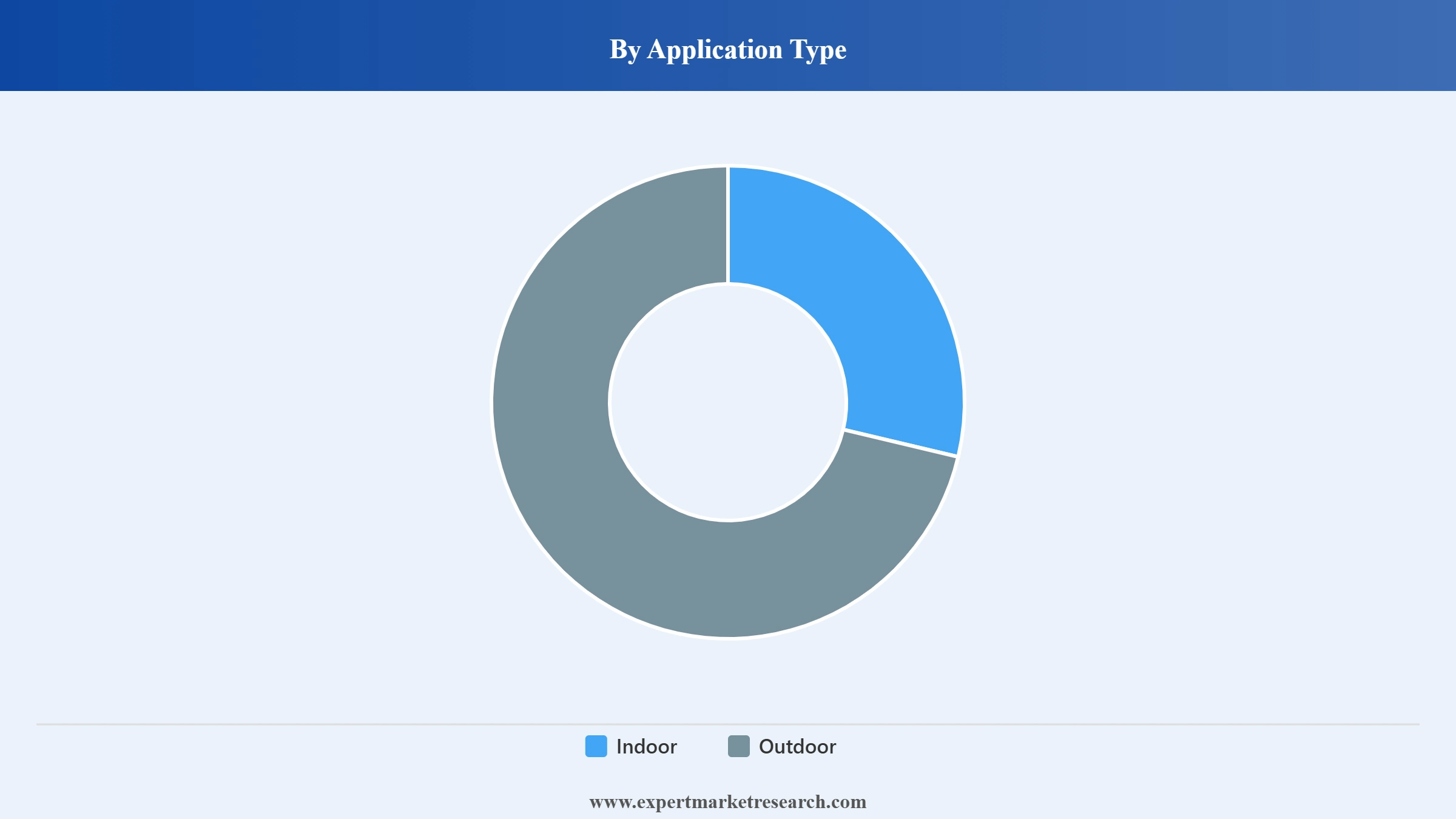

Market Breakup by Application Type

Key Insight: Indoor Wi-Fi applications represent the dominant share of the global market, driven by enterprise demand for reliable, high-capacity wireless networks in office buildings, retail stores, hospitals, educational institutions, and hospitality venues. The shift toward hybrid work models has reinforced indoor Wi-Fi investment as a business-critical priority. Cisco's Q1 2025 enterprise WLAN market share of 39.5% reflects the concentrated spending in indoor enterprise environments. Outdoor Wi-Fi, while smaller in absolute terms, is the faster-growing application segment, propelled by government smart city programmes, transportation hub deployments, and stadium connectivity projects. The expansion of public Wi-Fi in urban centres across Asia Pacific and North America is expected to sustain above-average growth in the outdoor segment through the forecast period.

Market Breakup by Density

Key Insight: Enterprise-class Wi-Fi remains the largest density segment, serving the broad base of corporate office, healthcare, retail, and government deployments that require reliable performance at moderate device densities. High-density Wi-Fi is the faster-growing segment, designed for environments where hundreds or thousands of devices connect simultaneously - including stadiums, convention centres, university campuses, and transport hubs. The commercial availability of Wi-Fi 7 with multi-link operation and 320 MHz channel widths has significantly improved the technical capability of high-density Wi-Fi deployments. Huawei and HPE Aruba have made notable advances in high-density Wi-Fi solutions, and global stadium and smart venue projects are expected to be a key demand driver for this segment through 2035.

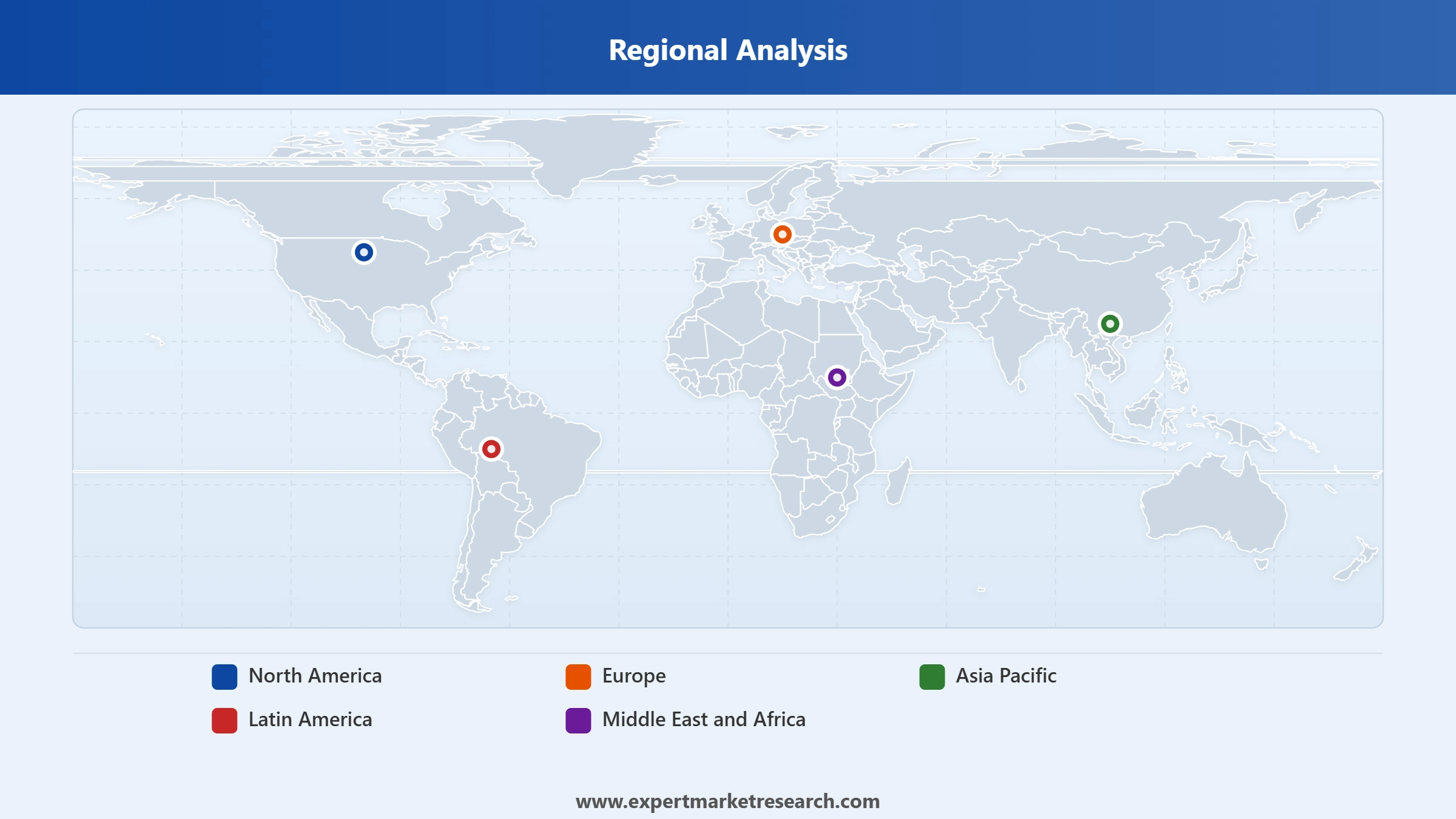

Market Breakup by Region

Key Insight: North America leads the global Wi-Fi market and is projected to record the highest regional CAGR during the forecast period, supported by concentrated enterprise IT investment, large-scale smart infrastructure programmes such as the US BEAD broadband initiative, and the rapid domestic adoption of Wi-Fi 7. Asia Pacific represents the largest and fastest-growing regional market by volume, driven by China's smart city investments, India's digital infrastructure expansion, and Japan and South Korea's advanced enterprise networking environments. Europe follows with steady investment in enterprise connectivity and public Wi-Fi, underpinned by EU digital agenda initiatives. Latin America and the Middle East and Africa are emerging growth markets as connectivity investments accelerate in major urban centres.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Offering

The hardware segment, specifically access points, commands the dominant share of the global Wi-Fi market by offering. Cisco leads this category with approximately 39.5% of enterprise WLAN revenue as of Q1 2025, according to IDC, a position reinforced by its November 2024 launch of globally unified Wi-Fi 7 access points. HPE Aruba, now combined with Juniper Mist following the July 2025 acquisition, holds approximately 19.3% combined share in enterprise WLAN, making the hardware segment a two-player dominated space with meaningful contributions from Huawei (approximately 9%), Ubiquiti, and CommScope's Ruckus brand. The solutions and services segments are growing at an accelerated pace as cloud-managed Wi-Fi platforms and AI-native management tools attract investment from enterprise customers seeking operational efficiency and network intelligence beyond basic connectivity.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Application Type

Indoor Wi-Fi applications account for the majority of global market revenue by application type, driven by the consistently high volume of enterprise, healthcare, education, and retail deployments. The sustained investment in corporate office connectivity - even in the face of hybrid work trends - reflects the enduring importance of on-premises wireless networks for data-sensitive operations and collaboration applications. Outdoor Wi-Fi, while smaller in share, is the more dynamic segment for new project wins, particularly in Asia Pacific and North America where smart city programmes and public venue upgrades are generating substantial Wi-Fi infrastructure demand. High-density Wi-Fi deployments are seeing particularly strong growth as stadiums, transit hubs, and large educational campuses upgrade to Wi-Fi 7 infrastructure capable of supporting thousands of simultaneous connections.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

North America

North America is the dominant regional market for Wi-Fi globally and is expected to record the highest CAGR during the forecast period, underpinned by a combination of deep enterprise IT investment, aggressive government broadband expansion programmes, and rapid adoption of next-generation Wi-Fi standards. The United States accounts for the bulk of regional revenue, with Cisco holding roughly 40% of global enterprise WLAN market share and HPE Aruba maintaining a strong presence across large enterprise and education verticals. The US BEAD programme, which allocates substantial federal funding for broadband infrastructure in underserved communities, has created significant incremental demand for wireless networking equipment, including outdoor Wi-Fi hotspot gateways. Canada is also investing in public Wi-Fi infrastructure as part of national digital connectivity strategies, adding further depth to the regional demand base. US-headquartered vendors including Cisco, CommScope, Ubiquiti, Motorola Solutions, and Cloud4Wi all maintain primary development and go-to-market operations in the region.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Asia Pacific

Asia Pacific is the largest regional Wi-Fi market by volume and is expected to sustain strong growth through the forecast period, supported by China's ambitious smart city investment programmes, India's rapid digital infrastructure expansion under the BharatNet initiative, and the advanced enterprise networking environments of Japan, South Korea, and Australia. Huawei maintains a particularly strong position in the Asia Pacific Wi-Fi market, especially in China where it competes with local and global players across enterprise, carrier, and government verticals. India's government has committed to expanding Wi-Fi coverage in rural areas and public institutions, generating substantial demand for affordable access point and hotspot gateway solutions. The ASEAN region is also experiencing accelerating Wi-Fi adoption as enterprise digitalisation programmes and foreign direct investment into manufacturing and logistics create new wireless networking requirements. China's rollout of Wi-Fi 7 trials in industrial IoT and smart manufacturing environments is expected to be a significant regional demand accelerator through 2035.

The global Wi-Fi market is led by a small group of technology giants that command the majority of enterprise WLAN revenue, while a broader field of specialised vendors serves specific verticals, geographies, and price points. Cisco maintains a commanding lead with approximately 39.5% of global enterprise WLAN revenue in Q1 2025, a position built on its dominant product portfolio, extensive channel relationships, and deep enterprise customer loyalty. The HPE-Juniper combination created in July 2025 is the most significant competitive challenge to emerge in years, bringing together Aruba's scale and Juniper's AI-driven Mist platform into a single entity with combined market share approaching 20%.

Beyond the top two, Huawei remains a formidable competitor in Asia Pacific, with approximately 9% global enterprise WLAN market share in Q2 2025. Fortinet has carved out a differentiated niche at the intersection of Wi-Fi and cybersecurity, while Ubiquiti serves the value-conscious enterprise and prosumer segment with a growing product portfolio. The competitive dynamics of the market are increasingly shaped by AI integration, cloud management capabilities, and the pace of Wi-Fi 7 product deployment, with vendors investing heavily in these areas to differentiate their offerings and capture the next enterprise upgrade cycle.

Founded in 1984 and headquartered in San Jose, California, USA, Cisco is the undisputed leader in global enterprise Wi-Fi with approximately 39.5% market share in enterprise WLAN revenue as of Q1 2025. Its portfolio spans access points, WLAN controllers, and cloud management solutions, including its Meraki and Catalyst lines. In November 2024, Cisco launched the CW9176 and CW9178 Wi-Fi 7 access points, its first globally unified hardware models, designed with native AI capabilities and simplified subscription licensing. Cisco's broad distribution, deep enterprise relationships, and AI-enhanced network management tools through Cisco Spaces and ThousandEyes make it the default choice for large enterprise deployments worldwide.

Hewlett Packard Enterprise (HPE) is headquartered in Spring, Texas, USA and operates its Wi-Fi business primarily through the HPE Aruba Networking division. Following the USD 14 billion acquisition of Juniper Networks, completed in July 2025, HPE combined the Aruba enterprise Wi-Fi portfolio with Juniper's AI-driven Mist WLAN platform to create a significantly strengthened competitive offering. The combined entity held approximately 19.3% of enterprise WLAN revenue share in Q3 2025 according to IDC. HPE's strength lies in its ability to serve large and mid-market enterprises with AI-powered network management, security integration, and a strong global channel partner network.

CommScope, founded in 1976 and headquartered in Claremont, North Carolina, USA, operates in the Wi-Fi market primarily through its Ruckus Networks division, which offers enterprise-grade access points, WLAN controllers, and cloud-managed wireless solutions. Ruckus is particularly well-regarded for high-density Wi-Fi deployments in venues such as stadiums, hotels, and campuses. CommScope's March 2024 decision to expand US manufacturing capacity for its fiber connectivity portfolio reflects its broader strategy of scaling infrastructure supply to support growing broadband and wireless demand globally. The company serves enterprise, carrier, and public sector customers across North America, Europe, and Asia Pacific.

Juniper Networks, founded in 1996 and headquartered in Sunnyvale, California, USA, built a strong reputation in the Wi-Fi market through its Mist AI platform, which applies artificial intelligence and machine learning to automate network operations, self-healing, and user experience assurance. Juniper's enterprise WLAN revenues grew 20.4% year-over-year in Q2 2025, reflecting strong demand for its AI-native approach. As of July 2025, Juniper became part of Hewlett Packard Enterprise following a USD 14 billion acquisition. Juniper's technology continues to operate as a distinct platform within HPE's networking portfolio, targeting enterprises seeking AI-first wireless operations.

Other key players in the market are Telefonaktiebolaget LM Ericsson, Huawei Technologies Co. Ltd., Fortinet Inc., Ubiquiti Inc., Motorola Solutions Inc., Cloud4Wi Inc., and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Find out what is really behind the Global Wi-Fi Market's rapid growth trajectory with our comprehensive report for 2026. From the Wi-Fi 7 technology transition reshaping enterprise budgets to the smart city programmes unlocking outdoor connectivity demand, this report delivers a data-driven view of where the market is heading and who is winning. Whether you are a technology vendor planning your next product launch, an investor evaluating the wireless networking space, or an enterprise assessing your infrastructure strategy, our report gives you the clarity to move forward with confidence. Download your free sample today and explore the opportunities defining the future of global wireless connectivity.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market attained a value of nearly USD 40.94 Billion.

The market is assessed to grow at a CAGR of 12.40% between 2026 and 2035.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach about USD 131.77 Billion by 2035.

The market is being driven by the expansion of the 5G network across the globe and the proliferation of IoT devices.

The key trends aiding the market expansion include the expansion of smart homes and the growing usage of mobile devices.

The major application types of Wi-Fi are indoor and outdoor.

The major regions considered in the market are North America, Europe, the Asia Pacific, Latin America, and the Middle East and Africa, among others.

The major players in the market are Cisco Systems Inc., Hewlett Packard Enterprise Company, Commscope Holding Company Inc., Juniper Networks, Inc., Telefonaktiebolaget LM Ericsson, Huawei Technologies Co., Ltd., Fortinet Inc., Ubiquiti Inc., Motorola Solutions Inc., and Cloud4Wi, Inc., among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Offering |

|

| Breakup by Application Type |

|

| Breakup by Density |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.