Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

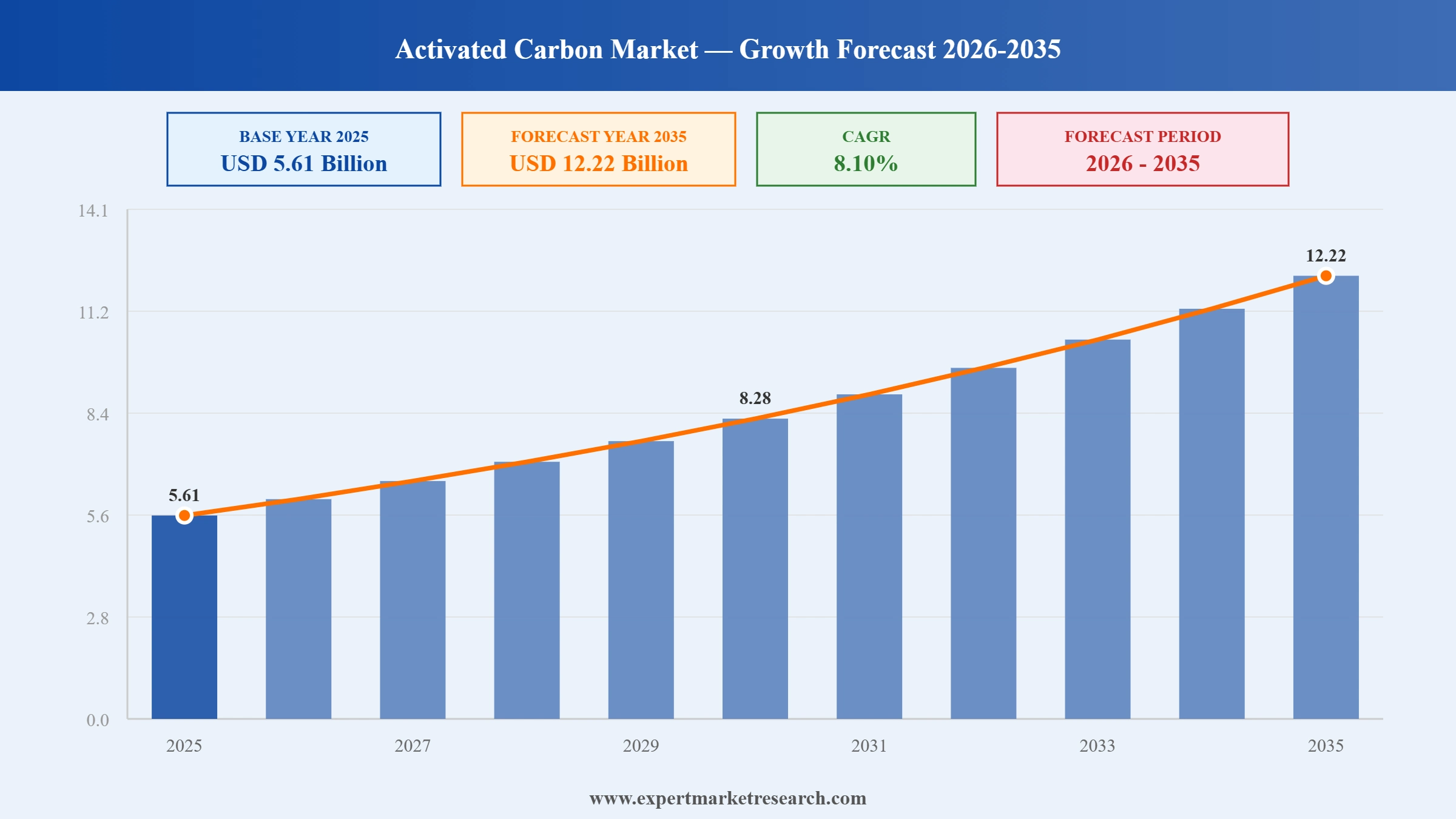

The global activated carbon market reached a value of USD 5.61 Billion at 2025 and is projected to expand at a CAGR of around 8.10% during the forecast period of 2026-2035. With accelerating global demand for water and air purification, tightening environmental regulations on industrial emissions and PFAS contaminants, and growing applications in gold recovery, gas storage, and food and beverage processing, the market is expected to reach USD 12.22 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

| Global Activated Carbon Market Report Summary | Description | Value |

| Base Year | USD Billion | 2025 |

| Historical Period | USD Billion | 2019-2025 |

| Forecast Period | USD Billion | 2026-2035 |

| Market Size 2025 | USD Billion | 5.61 |

| Market Size 2035 | USD Billion | 12.22 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 8.10% |

| CAGR 2026-2035 - Market by Region | Middle East and Africa | 8.4% |

| CAGR 2026-2035 - Market by Country | India | 9.1% |

| CAGR 2026-2035 - Market by Country | China | 8.7% |

| CAGR 2026-2035 - Market by Type | Powdered Activated Carbon | 8.8% |

| CAGR 2026-2035 - Market by Application | Air Treatment | 9.0% |

| Market Share by Country 2025 | Canada | 2.1% |

Activated carbon is a highly porous form of carbon produced by heating organic raw materials such as coal, coconut shells, or wood in the absence of oxygen. A single gram can have a surface area exceeding 500 square metres, giving it extraordinary capacity to adsorb contaminants from both liquid and gas streams. The US EPA recognises granular activated carbon as a Best Available Technology for removing PFAS, volatile organic compounds, and other regulated contaminants from drinking water, a designation formalised in its April 2024 National Primary Drinking Water Regulation.

The activated carbon market covers the global production and application of this material across water treatment, air purification, food and beverage processing, pharmaceuticals, and gold mining. Water treatment is the largest end-use segment, accounting for an estimated 31.6% of global demand in 2026. The market is served by three primary product forms: powdered, granular, and pelletised activated carbon, each suited to different treatment system configurations and end-use requirements.

The most significant growth driver is regulatory pressure around PFAS contamination in drinking water. The US EPA's April 2024 final rule set enforceable limits of 4 parts per trillion for PFOA and PFOS, and the Infrastructure Investment and Jobs Act dedicated USD 9 billion to help communities address PFAS in drinking water, creating a structural government funding base for long-term granular activated carbon procurement across municipal water systems nationwide.

Industrial expansion across Asia-Pacific and tightening air emission standards are further broadening demand. China's Blue Sky Protection Campaign has driven widespread adoption of activated carbon in gas-phase applications across power plants and manufacturing. In February 2026, Calgon Carbon committed nearly USD 100 million to expand reactivation capacity at its Columbus, Ohio facility, adding 27 million pounds of annual capacity by Q1 2028, directly reflecting the scale of investment now flowing into the activated carbon supply chain.

The global activated carbon market is entering a high-growth phase, driven by intensifying environmental regulations targeting water pollutants including PFAS, mercury, and emerging organic contaminants, alongside rising industrial demand for air purification and solvent recovery. The acceleration of water infrastructure investment programmes across Asia Pacific, the United States, and Europe is creating sustained demand for both powdered and granular activated carbon grades, while specialty applications in gold recovery, pharmaceutical purification, and capacitive deionisation are opening additional high-value growth avenues for market participants.

The U.S. Environmental Protection Agency published a request for public comments on its draft Sixth Contaminant Candidate List (CCL 6) on April 6, 2026, proposing to regulate all PFAS under the Safe Drinking Water Act. The proposal directly expands compliance-driven demand for granular activated carbon, which the EPA identifies as a primary certified treatment technology for PFAS removal in municipal drinking water systems.

Calgon Carbon Corporation, a wholly owned subsidiary of Kuraray Co., Ltd. (TYO: 3405), announced on February 26, 2026 a nearly $100 million investment to expand drinking water carbon reactivation capacity at its Columbus, Ohio plant, adding approximately 27 million pounds per year of new reactivation capacity. The company simultaneously announced the development of a new Tyger River Plant at an 83-acre site secured in Moore, South Carolina, to serve U.S. utilities preparing for PFAS compliance.

A U.S. federal district court denied the EPA's request to vacate PFAS drinking water limits on January 21, 2026, preserving compliance requirements under the Safe Drinking Water Act for public water systems. The ruling maintains regulatory demand for granular activated carbon, which the EPA designates alongside ion exchange resins and reverse osmosis as an approved treatment technology for PFAS removal in drinking water

Ingevity Corporation appointed Ruth Castillo as President of its Performance Materials segment, which encompasses its activated carbon business serving automotive evaporative emissions control applications, in November 2025. The appointment reflects Ingevity's strategic focus on strengthening its activated carbon leadership as regulatory tightening of vehicle evaporative emission standards in North America, Europe, and Asia drives growing demand for high-performance carbon canisters in passenger and light commercial vehicles.

PFAS Regulatory Catalyst: The finalisation of stringent per- and polyfluoroalkyl substance maximum contaminant levels by the US Environmental Protection Agency and advancing European PFAS restriction frameworks are creating a structural demand surge for activated carbon in drinking water and wastewater treatment. Municipal water utilities, industrial operators, and military facility managers are investing in granular and powdered activated carbon filtration systems to achieve compliance with PFAS concentration limits, representing a multi-year volume growth catalyst for the global activated carbon market.

Asia Pacific Infrastructure Growth: Accelerating investment in municipal water treatment infrastructure across China, India, Southeast Asia, and South Korea is driving the fastest regional demand growth in the global activated carbon market. Government programmes targeting universal safe drinking water access, industrial effluent compliance, and urban air quality improvement are supporting substantial procurement volumes for both powdered and granular activated carbon grades, with China's domestic production capacity simultaneously expanding to meet both domestic consumption and export market requirements.

Gold Mining Expansion: Sustained strength in gold prices is stimulating investment in gold mining operations globally, driving growing demand for granular activated carbon in carbon-in-pulp and carbon-in-leach gold extraction processes. Activated carbon plays a critical role in gold recovery circuits, adsorbing dissolved gold from cyanide leach solutions with high efficiency. Expanded gold production in West Africa, Latin America, and Australia is translating into incremental activated carbon volume demand for the gold treatment application segment.

Automotive Emission Regulations: Increasingly stringent evaporative emission control regulations in the United States, European Union, China, and India are driving demand for high-capacity activated carbon in automotive carbon canisters that capture fuel vapours from vehicle tanks and engines. The transition to lower Reid Vapour Pressure fuels and extended refuelling emission standards is requiring higher-performance activated carbon formulations with greater butane working capacity, supporting premium product development investment by manufacturers including Ingevity, Kuraray, and others.

Coconut Shell Feedstock Premium: Coconut shell-derived activated carbon commands a growing premium in water treatment and food and beverage applications due to its superior hardness, low ash content, and enhanced adsorption selectivity relative to coal and wood-based alternatives. Supply chain dynamics in key producing countries including the Philippines, Indonesia, and Sri Lanka influence feedstock availability and pricing for coconut shell carbon producers. Growing buyer preference for sustainably sourced, food-contact approved activated carbon is reinforcing the coconut shell segment's market position in premium application categories.

"Activated Carbon Market Report and Forecast 2026-2035" offers a detailed analysis of the market based on the following segments:

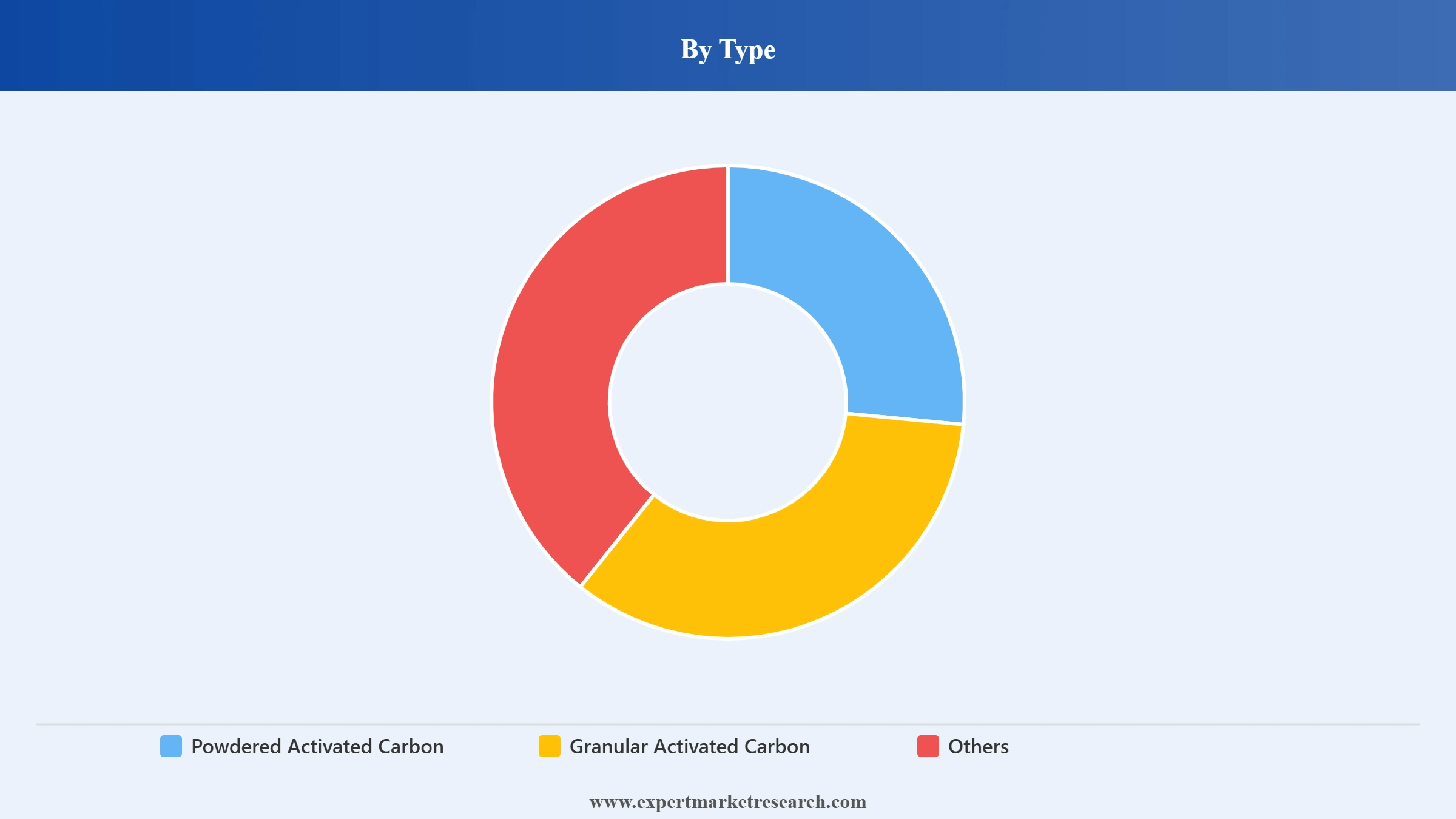

Market Breakup by Type

Key Insight: Granular activated carbon holds the largest share in the global activated carbon market by type, driven by its dominant use in fixed-bed water treatment systems, air purification installations, and gold recovery operations that require consistent particle size, high mechanical strength, and reactivation potential for multiple service cycles. Powdered activated carbon is the fastest-growing type segment, registering a CAGR of 7.8%, driven by its widespread use in municipal water treatment for taste, odour, and emerging contaminant removal, its application in wastewater treatment for industrial effluent compliance, and its growing use in food and beverage processing applications requiring fine particle distribution.

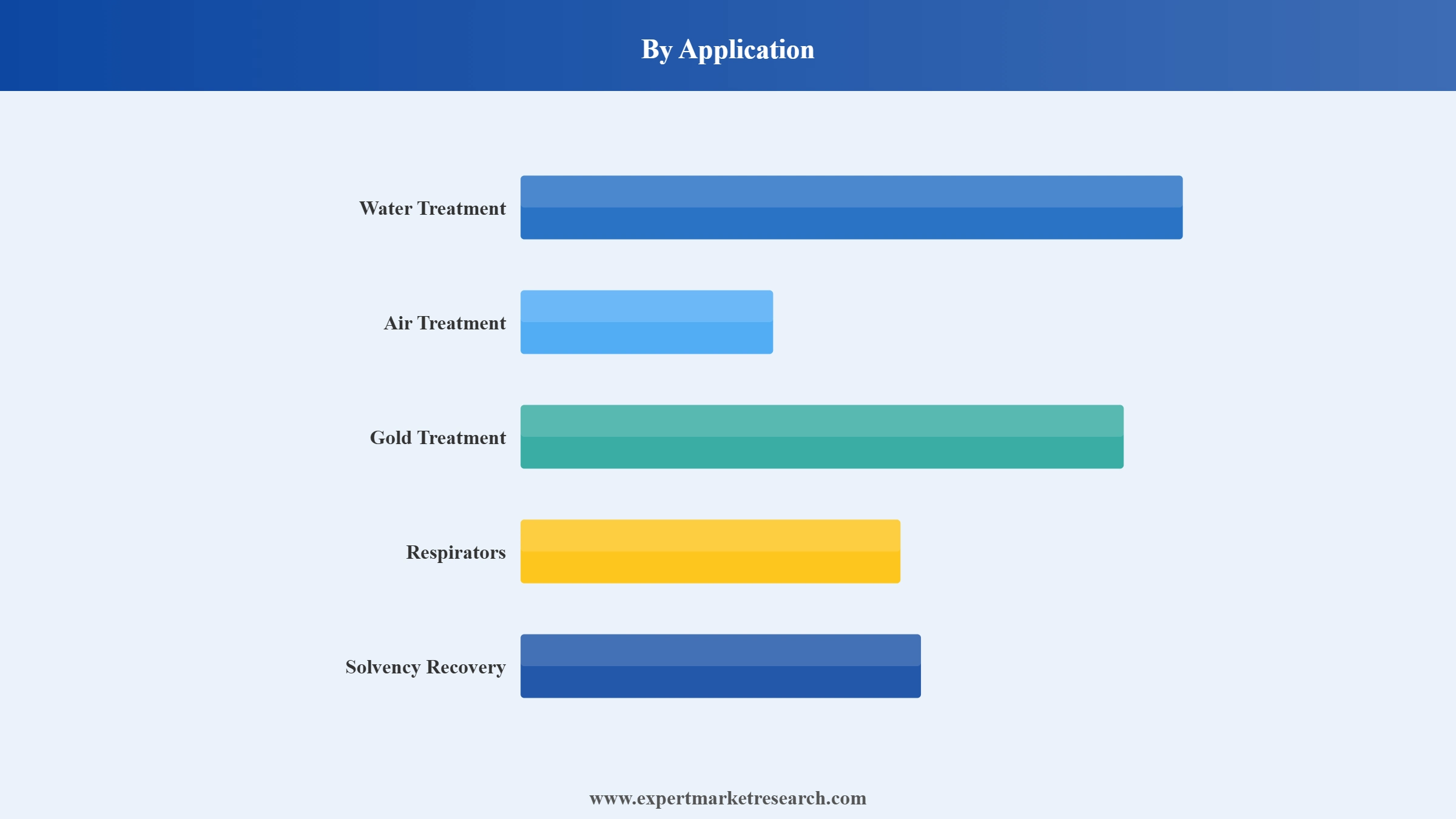

Market Breakup by Application

Key Insight: Water treatment represents the dominant application segment in the global activated carbon market, accounting for the largest volume share driven by municipal drinking water purification, industrial wastewater treatment, and the accelerating investment in PFAS removal infrastructure across North America and Europe. Water treatment is also the fastest-growing major application at a CAGR of 8.3%, underpinned by tightening global water quality regulations and expanding treatment infrastructure investment in Asia Pacific and developing regions. Air treatment is the second-largest application segment, with growing industrial VOC emission control requirements and urban air quality improvement programmes driving demand across manufacturing, chemical processing, and food production sectors.

Market Breakup by Feedstock

Key Insight: Coal-based activated carbon holds the largest feedstock share in the global activated carbon market, driven by its cost competitiveness, broad availability, and suitability for large-volume industrial water and air treatment applications. Coal-derived activated carbon dominates the granular grades used in fixed-bed water treatment and industrial gas purification systems. Coconut shell-based activated carbon is the highest-growth and highest-value feedstock segment, commanding a premium for water treatment, food and beverage, pharmaceutical, and respirator applications where its superior pore structure, low ash content, and food-contact safety approvals provide distinct performance advantages over coal and wood-based alternatives.

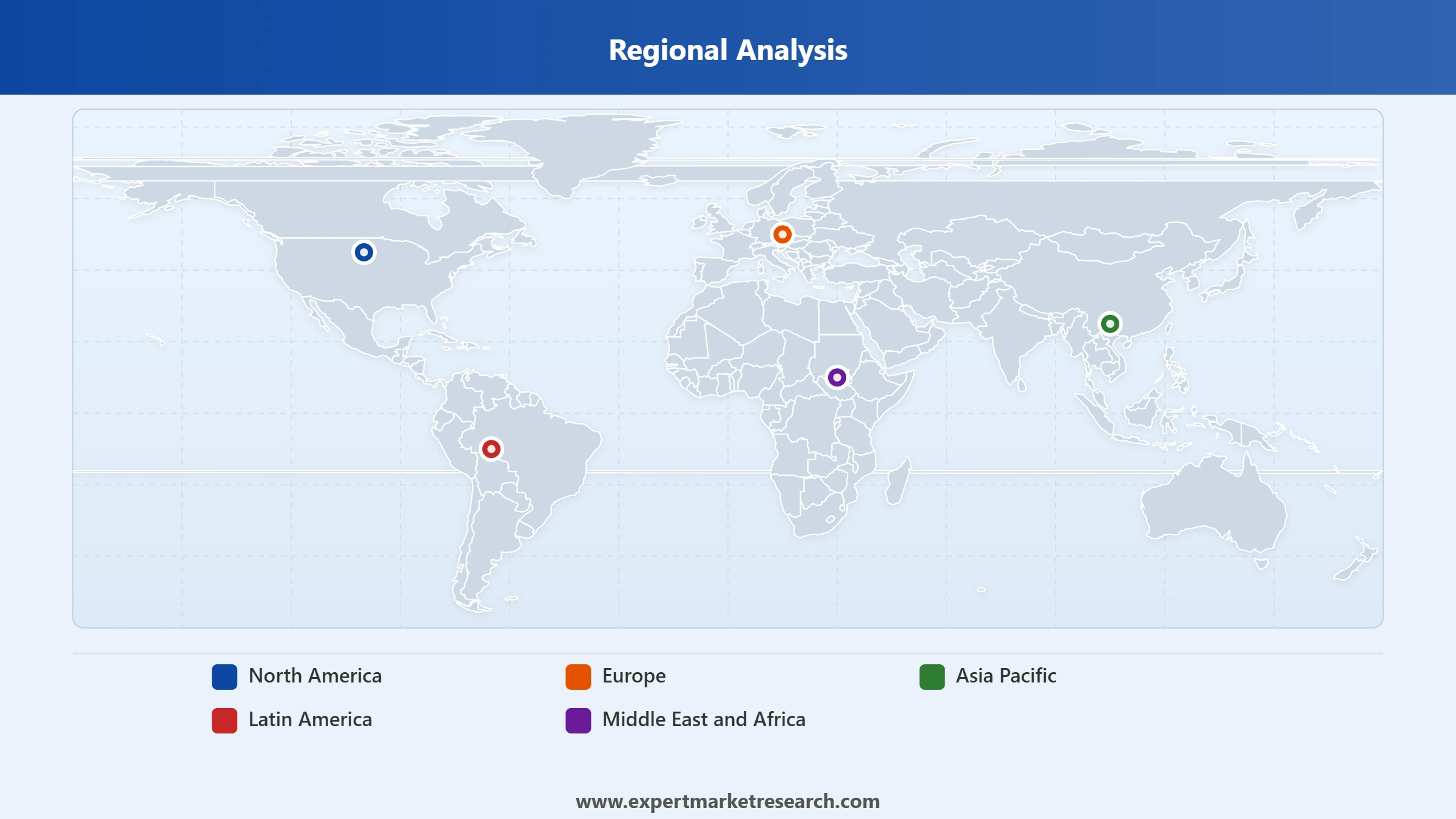

Market Breakup by Region

Key Insight: Asia Pacific dominates the global activated carbon market and is the fastest-growing region at a CAGR of 9.5%, underpinned by large-scale municipal water treatment infrastructure investment in China, India, and Southeast Asia, growing industrial emission control requirements, and the dominant production base for coconut shell and coal-based activated carbon in the Philippines, China, Indonesia, and Sri Lanka. North America is the second-largest market, driven by substantial PFAS remediation investment following US EPA regulatory action on drinking water standards, automotive evaporative emission control demand, and industrial air treatment applications across chemical manufacturing and food processing sectors.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Type, granular activated carbon holds the largest market share due to its widespread use in fixed-bed water and air treatment systems requiring high mechanical stability and reactivation capability

Granular activated carbon's market leadership reflects its technical suitability for continuous-operation fixed-bed treatment systems deployed in municipal water utilities, industrial effluent treatment plants, and air purification installations. The particle size and mechanical strength of granular grades enable efficient backwashing, extended service cycles, and thermal reactivation at commercial facilities operated by companies including Jacobi Carbons, Norit, and Ingevity. The gold treatment sector's reliance on granular carbon for carbon-in-pulp and carbon-in-leach circuits further reinforces the segment's volume dominance in the global activated carbon market.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Powdered activated carbon is the most dynamic growth category in the global activated carbon market, gaining market share in water treatment applications where its fine particle distribution enables rapid adsorption kinetics and flexible dosing in response to varying contaminant loads. In September 2025, Kuraray's PFAS-selective activated carbon development targeted both powdered and granular grades optimised for PFAS removal, reflecting the segment's growing importance in regulatory compliance applications. Powdered activated carbon is also gaining traction in pharmaceutical active ingredient purification, specialty food processing, and capacitive deionisation water desalination applications that benefit from its fine particle characteristics.

By Application, water treatment accounts for the dominant market share due to its large-scale deployment in municipal drinking water purification and the accelerating PFAS remediation investment cycle

Water treatment's dominant position in the global activated carbon market is underpinned by the universal requirement for safe drinking water across all geographies and the growing complexity of water quality challenges including organic micropollutants, pharmaceuticals, and PFAS compounds. Municipal water authorities globally represent the largest single buyer segment for both powdered and granular activated carbon, with procurement volumes driven by treatment capacity expansion, regulatory compliance upgrades, and infrastructure rehabilitation programmes. North American and European PFAS regulatory developments are creating significant incremental demand for high-adsorption-capacity activated carbon in water treatment fixed-bed systems.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Air treatment is the second most significant application in the global activated carbon market, serving industrial VOC emission control, solvent recovery, automotive evaporative emission systems, and indoor air quality improvement requirements. In November 2025, Ingevity's appointment of Ruth Castillo to lead its Performance Materials segment highlighted the strategic importance of automotive carbon canister applications, which are growing as evaporative emission standards tighten across major vehicle markets globally. Industrial air treatment demand is further supported by expanding manufacturing sector investment in Asia Pacific, where environmental compliance requirements for chemical processing, pharmaceutical, and food manufacturing facilities are increasing.

Asia Pacific dominates the market due to its large-scale water treatment investment programmes, dominant production infrastructure, and rapidly expanding industrial emission control requirements

Asia Pacific's leadership in the global activated carbon market reflects the convergence of the world's largest production base with the fastest-growing consumption growth. China's activated carbon manufacturing sector produces the majority of global coal-based granular activated carbon supply, supporting both domestic water treatment and industrial purification demand while serving as a key export source for global markets. India's Jal Jeevan Mission and associated water infrastructure programmes represent a major multi-year demand driver for both powdered and granular activated carbon, with ongoing investment in rural and urban water treatment infrastructure creating sustained procurement requirements through the forecast period.

North America

North America is the second-largest activated carbon market globally, characterised by high per-capita consumption driven by stringent water quality regulations, large-scale automotive evaporative emission control applications, and well-established industrial air treatment requirements. The US EPA's finalisation of PFAS maximum contaminant levels for drinking water is expected to be the single largest demand driver for granular activated carbon in the forecast period, with water utilities across the United States requiring substantial capital investment in filtration infrastructure. In March 2025, Cabot Corporation expanded its EVERSORB portfolio specifically to serve this growing North American water treatment opportunity.

Europe

Europe is the third-largest market for activated carbon globally and is expected to grow at a significant rate through the forecast period, driven by stringent European Union water quality directives, PFAS restriction regulations under the EU Chemicals Strategy for Sustainability, and strong demand from pharmaceutical, food and beverage, and chemical processing industries. In July 2025, Jacobi Carbons's European reactivation capacity expansion directly targeted this growing demand, enabling water utilities and industrial operators to manage spent carbon service cycles more efficiently while meeting circular economy obligations. Germany, Netherlands, and the United Kingdom represent the largest national activated carbon markets within the European region.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The global activated carbon market is fragmented, featuring a mix of large multinational specialty chemical companies, regional activated carbon specialists, and commodity producers primarily concentrated in Asia Pacific. Competitive differentiation is driven by raw material sourcing strategy, production technology, product quality consistency, application engineering expertise, and the ability to support reactivation services that reduce total lifecycle cost for major water utility and industrial customers.

Founded in 1926 and headquartered in Tokyo, Japan, Kuraray Co., Ltd. is a leading global manufacturer of activated carbon through its Kuraray Chemical subsidiary, producing a comprehensive range of granular, powdered, and specialty activated carbon products for water treatment, automotive emission control, gas storage, and pharmaceutical purification applications. Kuraray's activated carbon portfolio includes FILTRACARB granular grades, coconut shell-derived premium products, and specially engineered grades for PFAS removal, serving customers across North America, Europe, and Asia Pacific.

Oxbow Activated Carbon LLC is a US-based activated carbon manufacturer and distributor serving water treatment, air purification, and industrial process applications across North American markets. The company provides both virgin and reactivated activated carbon products with a focus on delivering reliable supply, quality consistency, and technical support to municipal water utilities and industrial customers requiring compliant solutions for contaminant removal and emission control applications.

Founded in 1973 and headquartered in Colombo, Sri Lanka, Haycarb (Pvt) Ltd. is one of the world's leading producers of coconut shell-based activated carbon, with manufacturing facilities in Sri Lanka, Thailand, and Indonesia. Haycarb produces a comprehensive range of activated carbon products for water purification, gold recovery, food and beverage processing, gas purification, and automotive emission control applications, serving customers across more than 60 countries through its global distribution and technical support network.

Founded in 1985 and headquartered in Gujarat, India, Indo German Carbons Limited (IGCL) is a specialist activated carbon manufacturer serving water treatment, food processing, pharmaceutical, and industrial purification applications primarily across South Asian and international markets. The company produces wood-based and coal-based activated carbon products and operates technical service capabilities supporting customer formulation and application development requirements in key industrial sectors.

Other key players in the market are Shinkwang Chemical, S.I.C.A.V. Spa, Century Chemical Works, Cabot Corporation, Osaka Gas Chemicals Co., Ltd., Donau Carbon GmbH, Norit Nederland B.V., Carbon Activated Corporation, Ingevity Corporation, Silcarbon Aktivkohle GmbH, CPL Activated Carbons, Eurocarb Products Ltd., Euroquarz GmbH, Puragen Activated Carbons, Active Carbon India Ltd., and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Capitalise on the accelerating global demand for activated carbon solutions driven by PFAS regulations, water infrastructure investment, and industrial emission control requirements with our comprehensive global activated carbon market report for 2026. Whether you are an activated carbon manufacturer optimising your product portfolio strategy, a water utility assessing procurement options, an investor evaluating environmental materials opportunities, or an industrial operator managing purification compliance, our research provides the data-driven insights you need. Access detailed segment forecasts, competitive profiles, and regional analysis. Download your free sample today and explore the significant growth opportunities in the global activated carbon market.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

The global market for activated carbon reached a value of approximately USD 5.61 Billion in 2025.

The market is projected to grow at a CAGR of 8.10% between 2026 and 2035.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035, reaching a value of around USD 12.22 Billion by 2035.

The major drivers of the market include the rising demand for water filtration and air purification and increasing rising applications in the mining industry, automotive sector, and gold purification processes.

The key activated carbon market trends include rising coconut production, advancements in technology, and favourable regulations of various governments to improve water and air quality.

North America, Europe, the Asia Pacific, Latin America, and the Middle East and Africa are the major regions in the market.

the significant types of activated carbon in the market are powdered activated carbon, and granular activated carbon, among others.

The various applications of activated carbon in the market are water treatment, air treatment, gold treatment, respirators, and solvency recovery.

The primary feedstocks for activated carbon in the market are coconut shell, and wood/coal, among others.

The major players in the market, according to the report, are Kuraray Co., Ltd., Oxbow Activated Carbon LLC, Haycarb (Pvt) Ltd., Indo German Carbons Limited (IGCL), Shinkwang Chem. Ind. Co., Ltd, S.I.C.A.V. Spa, Century Chemical Works Sdn. Bhd, Cabot Corporation, Osaka Gas Chemicals Co., Ltd., Donau Carbon GmbH, Norit Nederland B.V., Carbon Activated Corporation., Ingevity Corporation, Silcarbon Aktivkohle GmbH, CPL Activated Carbons, Eurocarb Products Limited, Euroquarz GmbH, Puragen LLC, and Active Carbon India Pvt. Ltd., among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Type |

|

| Breakup by Application |

|

| Breakup by Feedstock |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.