Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

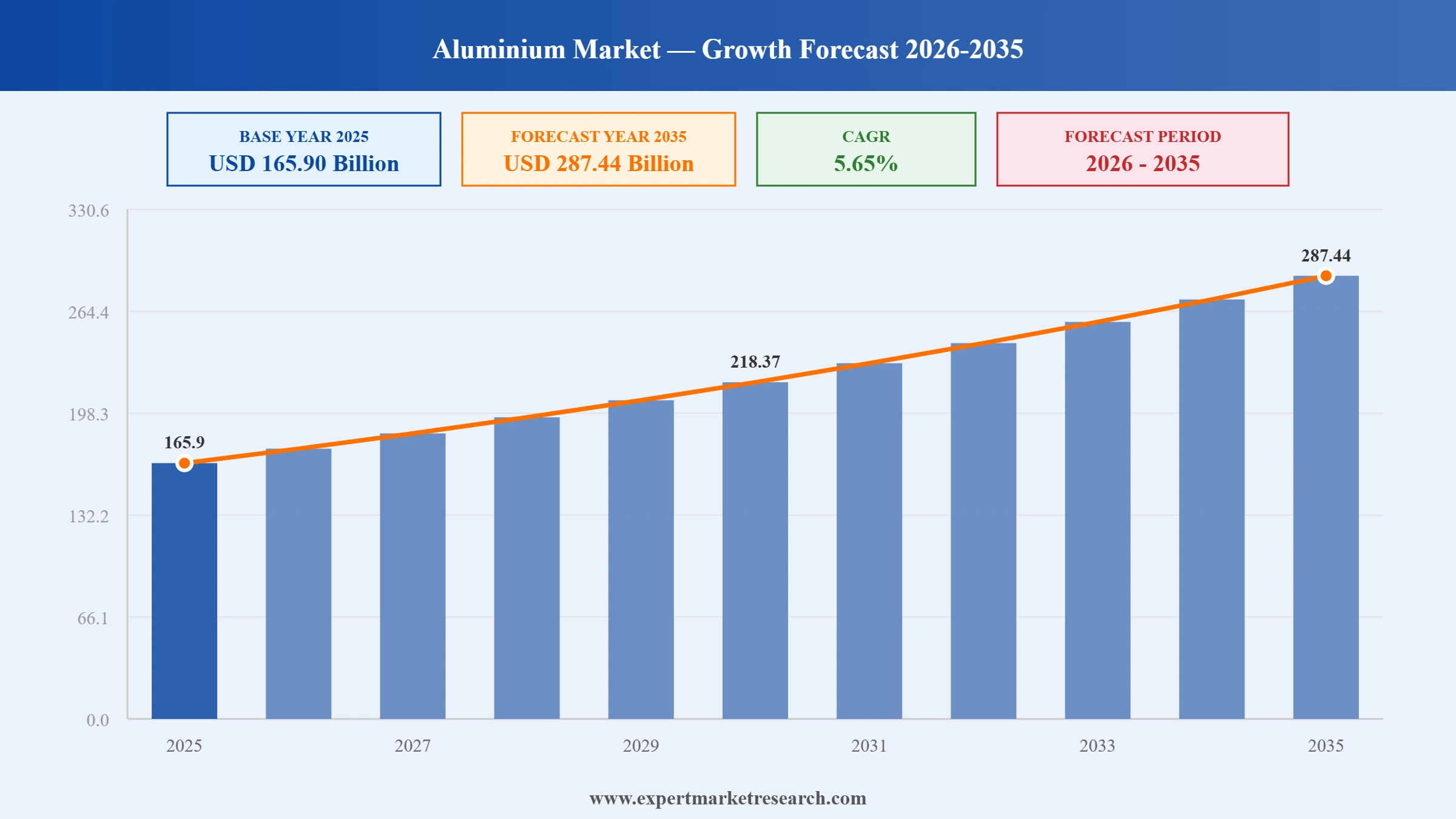

The global aluminum market attained a value of USD 165.90 Billion in 2025 and is projected to expand at a CAGR of 5.65% through 2035. The market is further expected to achieve USD 287.44 Billion by 2035. Rising investments in renewable energy infrastructure and light-weighted electrical mobility applications are boosting the demands for highly efficient and eco-friendly aluminum products by pushing manufacturers to increase recycling capabilities and develop advanced alloys.

The quick process of industrial electrification raises the demand for certain aluminum products utilized in batteries and high-voltage power grid systems, accelerating the overall aluminum market value. Meanwhile, companies manufacturing beverages packages are switching to highly recyclable aluminum cans, compelling manufacturers to build up their capacity for secondary aluminum processing, recycling collaboration, and rolling equipment development.

Another significant trend shaping the aluminum market globally is Rio Tinto's commercialization of its low-carbon aluminum portfolio through the growth of supply contracts with the automotive and packaging sectors that aim at cutting down their Scope 3 emissions. The company continues to scale up production of aluminum produced through hydro-powered smelting and enhances its traceability in the supply chain. On the other hand, in September 2025, Novelis released its 2025 Sustainability Report, highlighting carbon reduction, recycling progress, and circular aluminum manufacturing advancements. This initiative corresponds to the objectives of decarbonization in industries since according to the estimates of the International Aluminium Institute, the global aluminum demand may grow by almost 40% until 2030, and low-carbon aluminum will take a significant part of procurement in transportation, construction, and renewable energy sectors.

The global aluminum market goes through structural changes because of increased investments in the development of new alloys, technologies of circular production, and digital smelting. Manufacturers are interested in using light materials in order to boost the energy efficiency of electric cars, aerospace parts, and construction systems while reducing the level of emissions in production. Increased use of AI for process optimization and predictive maintenance and quality monitoring enables manufacturers to improve efficiency of production without damaging the product. For example, in November 2025, Sortera raised USD 45 million to scale AI-driven aluminum upcycling, expanding recycled metal production and domestic circular supply chains.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

| Global Aluminium Market Report Summary | Description | Value |

| Base Year | USD Billion | 2025 |

| Historical Period | USD Billion | 2019-2025 |

| Forecast Period | USD Billion | 2026-2035 |

| Market Size 2025 | USD Billion | 165.90 |

| Market Size 2035 | USD Billion | 287.44 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 5.65% |

| CAGR 2026-2035 - Market by Region | North America | 4.7% |

| CAGR 2026-2035 - Market by Country | India | 6.9% |

| CAGR 2026-2035 - Market by Country | UK | 6.3% |

| CAGR 2026-2035 - Market by Type | Secondary | 6.2% |

| CAGR 2026-2035 - Market by End Use | Packaging and Foil | 6.4% |

| Market Share by Country | Australia | 2.9% |

MQP developed the ultra-clean aluminum grain refiner, which resulted in better castability and higher performance in automotive and aerospace sectors. Firms are able to produce high purity refineries that can cater to increased requirements for premium aluminum parts in the manufacturing sector.

Eckart launched VERSALAN aluminum pigment preparation, which offers better dispersion, efficiency, and metallic appearance for industrial coating applications. Companies can hence produce high-end aluminum pigments for coatings that can be used in automotive, construction, and packaging sectors, accelerating the aluminum market value.

Alcoa made an announcement of a takeover deal worth USD 4.1 billion for the bauxite, alumina, and aluminum assets of South32. Firms may engage in strategic takeovers and upstream integration to enhance the security of their raw material sourcing and competitiveness.

NALCO launched IA91 aluminum alloy ingots, increasing the availability of such high-performance materials in the domestic market. Producers can diversify specialized alloys to meet rising demands from lightweight mobility and engineering industries, leveraging such trends in the aluminum market.

Moving towards green aluminum is becoming a critical factor for aluminum market players aiming to fulfill corporate net-zero commitments and comply with new carbon regulations. Major companies are developing renewable energy-based smelters and inert anodes to minimize emissions without compromising the efficiency of production processes. For example, in June 2026, Rio Tinto commissioned a USD 1.5 billion low-carbon aluminum project in Canada, expanding sustainable production with advanced AP60 smelting technology. Furthermore, the implementation of the Carbon Border Adjustment Mechanism (CBAM) in the European Union drives buyers to prefer more sustainable sources, motivating suppliers to enhance their capacities in this sphere.

Car manufacturers are actively switching from steel to high-alloy aluminum due to their better performance in terms of enhancing the efficiency of electric vehicles and prolonging their driving distance. This demand drives manufacturers to innovate their processes and create lightweight aluminum extrusions, batteries, and even parts designed to provide safety and stability. In June 2026, Ferrari, BMW, and Tesla expanded aluminum wiring adoption, reducing vehicle weight, lowering costs, and improving EV efficiency, accelerating the aluminum market value.

Secondary aluminum production is gaining traction as industry players embrace circular economy approaches to reduce production costs and carbon footprint. It takes considerably less energy to recycle aluminum as opposed to producing it from scratch, hence opening up new aluminum market opportunities. Companies like Emirates Global Aluminium are increasing their offering of low-carbon recycled aluminum through its RevivAL product range for use in automotive, construction, and packaging industries. In July 2026, Emirates Global Aluminium inaugurated the UAE's largest aluminum recycling plant, expanding low-carbon metal production and circular economy initiatives.

Expansion of the renewable energy production base is increasing the demand in the aluminum market, for applications in the solar, wind energy, and electricity transmission sectors. Aluminum's excellent corrosion-resistance, light weight, and electrical conductivity make it an important metal in the manufacturing of solar panel frames, wind turbine parts, and electricity transmission cables. According to the International Energy Agency, the world is consistently achieving record levels of installations of renewable energy generation capacities, which need considerable amounts of lightweight industrial metals. In support of this trend, China and India are stepping up their investments in solar manufacturing and electricity transmission infrastructures. Similarly, in June 2026, AM Green and Mitsui partnered to advance low-carbon aluminum production, renewable-powered manufacturing, and global green metals supply chains.

Artificial intelligence (AI), industrial automation, and digital twins are becoming popular among companies in the aluminum market in order to increase production efficiency, reduce energy usage, and provide quality products constantly. Smart smelters allow predicting possible failures in equipment, providing optimization of furnaces, and reducing downtime using real-time monitoring technology. Companies like Norwegian company Norsk Hydro are increasing the implementation of digital analysis and process optimization through AI at several production sites to enhance energy efficiency and operational efficiency. On the other hand, in November 2025, Alba expanded AI collaboration with ARRAY Innovation, enhancing aluminum smelter efficiency, safety, energy optimization, and predictive decision-making.

The Expert Market Research’s report titled “Aluminum Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

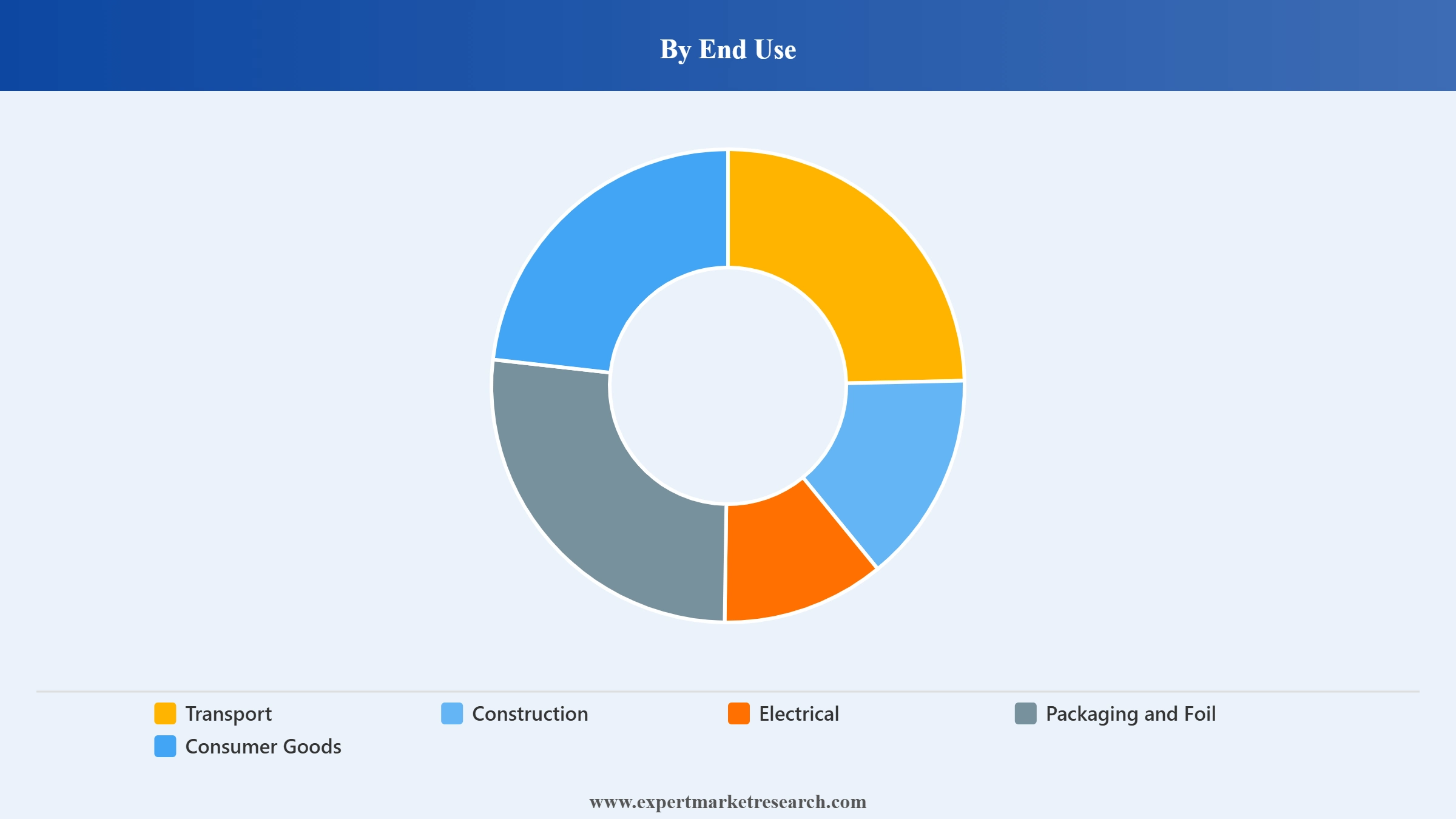

Market Breakup by End Use

Key Insight: The aluminum market caters to many industries that have their own specific performance needs. Transportation remains the dominant industry because of the efficiency created with lightweight structures. The construction industry continues contributing demand with the help of durable construction solutions and architecture. The electrical industry is rapidly expanding its share with the rising investments in electrification and renewables. Packaging and foil record notable demand because of recycling and food preservation purposes, whereas the consumer industry uses aluminum due to its appealing look and lightness.

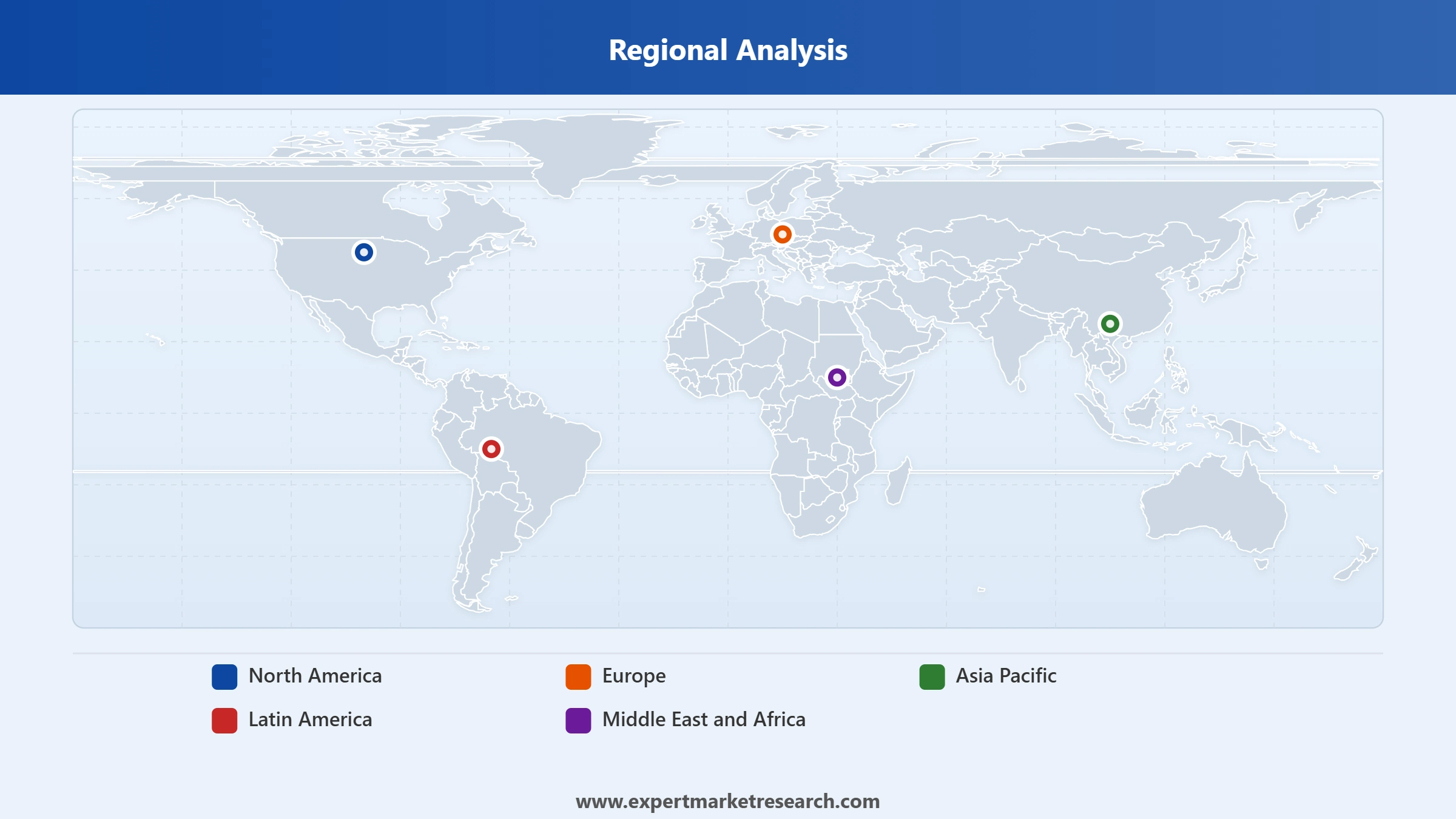

Market Breakup by Region

Key Insight: The Asia Pacific dominates the global aluminum market with manufacturing excellence, efficient supply chains, and rising industrial demand. North America enjoys a competitive edge owing to its advanced automotive manufacturing processes, aerospace manufacturing, and high recycling rates. Europe is focusing on sustainable aluminum production, initiatives on circular economy, and carbon-neutral manufacturing. Latin America is contributing to the growth of the global industry by virtue of its rich mineral endowment, infrastructure development, and rising exports. The Middle East and Africa are positioning themselves for success by means of competitive smelting operations and diversified industrialization.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By end use, the transport sector registers the largest share of the market due to lightweight mobility demand

The transport segment constitutes the major end-user category in the global aluminum market, since automakers, aerospace makers, rail makers, and naval manufacturers are placing more emphasis on lightweight materials to boost fuel efficiency and minimize environmental impact. There is a growing use of aluminum by manufacturers of electric vehicles in the construction of battery housings, body structure, wheels, and chassis, thus allowing the vehicles to travel farther without posing any safety issues. Manufacturers of aircraft are replacing other heavy metals with aluminum alloys, while makers of commercial vehicles are making use of lightweight structures to increase cargo carrying capacity and enhance efficiency. In June 2026, Hindalco launched an aluminum bicycle components plant, expanding lightweight mobility solutions and value-added manufacturing capabilities in India.

The aluminum market witnesses rapid growth in electrical applications due to higher investment in renewable energy generation facilities, transmission systems, and electrification projects. The superior conductivity, high resistance against corrosion, and lighter weight than copper are key factors that enable its usage in power cables, transformers, substations, and overhead transmission lines. Higher installation of solar parks, wind farms, EV charging stations, and smart grid networks is leading to higher demand for aluminum. In June 2026, Hitachi Energy and FRIEM partnered to advance electrified aluminum smelting, metal refining, and green hydrogen production solutions.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Asia Pacific dominates the market owing to robust manufacturing and infrastructure expansion

Asia Pacific holds the largest share of the global aluminum market revenue due to its advanced manufacturing base, increased construction activities, and rapid growth in the automotive industry. The ongoing investments made by countries like China, India, Japan, and South Korea in the development of their transportation networks, renewable energy generation plants, consumer electronics industry, and other industrial production facilities ensure a constant need for both primary and secondary aluminum. In October 2025, Evonik opened its Alu5 specialty alumina plant in Japan, expanding Asian supply for batteries and advanced coatings.

The Middle East and Africa represent the fastest growing regional aluminum markets, with manufacturers focusing on developing the production capacities of aluminum through the use of energy-efficient and low carbon smelting technology in addition to pursuing an industrial diversification strategy. Downstream manufacturing capacities, renewable powered industrial complexes, construction activities, and exports of aluminum are adding value to the regional competitiveness of the market. In June 2026, Ghana signed a EUR 300 million deal with Danieli, expanding aluminum processing, value-added manufacturing, and regional industrial capacity.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

With aluminum market players concentrating on sustainable manufacturing processes, recycled aluminum production, and the development of high-performance alloys in order to win industrial contracts in the future, the global market is growing ever more competitive. Inert anode technology, artificial intelligence-driven smelting plants, digital supply chains, and recycling loops are some of the key focus areas for producers.

Moreover, with the help of strategic collaborations with auto manufacturers, aircraft manufacturers, renewable energy companies, and packaging businesses, producers are developing additional revenue streams from their aluminum products. Leading aluminum companies are also focusing on downstream processing and regional manufacturing in order to decrease the risk associated with the supply chain. The demand for certified low-carbon materials with enhanced traceability is growing among industrial consumers.

Established in 2007 and based out of Moscow, Russia, RusAL is one of the leading aluminum producers with expertise in producing low-carbon aluminum products using hydropower generation. The company produces primary aluminum, alloys, billets, and slabs that cater to the transportation, packaging, construction, and electrical industries and develops inert anode and recycled aluminum manufacturing to improve sustainable manufacturing operations.

Established in 2001 and based out of Beijing, China, Chalco Aluminum Co. Ltd offers its services in bauxite mining, alumina refining, aluminum smelting, and downstream fabrication activities. The company caters to automotive, aerospace, construction, and industrial manufacturing industries and invests in intelligent manufacturing systems, efficient smelters, and high-strength aluminum products for advanced industrial applications.

Rio Tinto plc, founded in 1873, is based in London, United Kingdom and offers its customers aluminum with reduced carbon content, primary metals, billets and value-added products. Rio Tinto is developing the technology of inert anode for the production of low-carbon aluminum, renewable energy-based smelting processes and process optimization. The company is improving the sustainable aluminum value chain through collaborations with customers.

Founded in 1994, China Hongqiao Group Co., Ltd. is based in Binzhou, China and is one of the biggest aluminum producers in the world. The company is offering its customers aluminum alloy, rolled and fabricated aluminum for transportation, consumer goods, packaging and construction industry sectors while increasing the renewable-based aluminum production and intelligent manufacturing technologies.

Other key players in the market include Alcoa Corporation, Norsk Hydro ASA, Alux do Brasil, and Companhia Brasileira de Alumínio (CBA), among others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Unlock the latest insights with our aluminum market trends 2026 report. Discover regional growth patterns, consumer preferences, and key industry players. Stay ahead of competition with trusted data and expert analysis. Download your free sample report today and drive informed decisions in the market.

Saudi Arabia Aluminium Market

South Korea Aluminium Market

Australia Aluminium Market

Vietnam Aluminium Market

Canada Aluminium Market

Mexico Aluminium Market

Upto 15% Off

USD

$4399 $3959

$2999 $2699

$5599 $4759

$6659 $5660

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market reached an approximate value of USD 165.90 Billion.

The market is projected to grow at a CAGR of 5.65% between 2026 and 2035.

The market is estimated to witness healthy growth in the forecast period of 2026-2035 to reach a value of around USD 287.44 Billion by 2035.

The key strategies driving the market include technological innovation, sustainable production practices, and increased use of recycled aluminium. Companies are expanding capacity, forming strategic partnerships, and entering new markets to meet demand from automotive, construction, and aerospace sectors. Customization, lightweight solutions, and digital manufacturing are also critical growth enablers.

The key trends propelling the aluminium market growth includes the growing transportation industry and increasing downstream industries.

The major regions in the aluminium market are North America, Latin America, Europe, Middle East and Africa, and Asia Pacific.

The various end uses of aluminium in the market are transport, construction, electrical, machinery and equipment, packaging and foil, and consumer goods, among others.

The key players in the market report include W RusAL, Chalco Aluminum Co. Ltd, Rio Tinto plc, China Hongqiao Group Co., Ltd., Alcoa Corporation, Norsk Hydro ASA, Alux do Brasil, and Companhia Brasileira de Alumínio (CBA), among others.

Asia Pacific dominates the market, driven by robust industrial growth, high consumption, and a vast manufacturing base.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| Report Features | Details |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by End Use |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Trade Data Analysis |

|

| Competitive Landscape |

|

| Companies Covered |

|

Single User License

One User

USD 4,399

USD 3,959

tax inclusive*

Datasheet

One User

USD 2,999

USD 2,699

tax inclusive*

Five User License

Five User

USD 5,599

USD 4,759

tax inclusive*

Corporate License

Unlimited Users

USD 6,659

USD 5,660

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.