Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

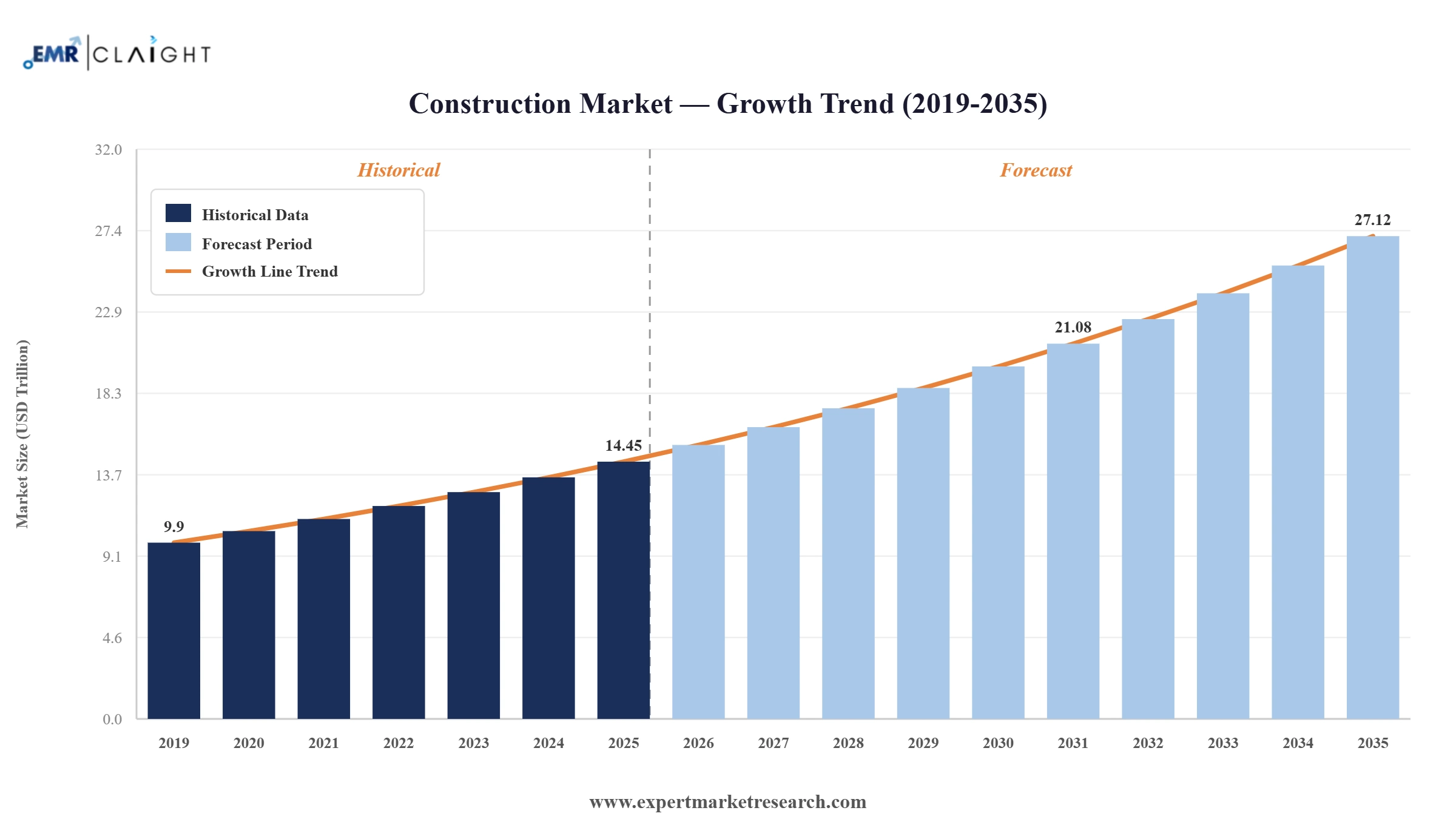

The Global Construction Market reached a value of USD 14.45 Trillion at 2025 and is projected to expand at a CAGR of around 6.50% during the forecast period of 2026-2035. With the rise of modular construction, accelerating green-building investments, large-scale data center build-outs, and digital project delivery, the market is expected to reach USD 27.12 Trillion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The Global Construction Market is being reshaped by digital project delivery, modular and prefabricated construction, AI and robotics adoption, and an unprecedented data center build-out, alongside the industry-wide push to decarbonise materials and operations.

Bechtel Corporation appointed John Platt as senior vice president of EPC transformation, charged with overhauling project delivery using advanced digital technologies, AI, automation, and robotics. The role anchors Bechtel's collaboration with NVIDIA, which translates the Omniverse AI factory blueprint into a modular, repeatable delivery model designed to compress time from project approval to operational readiness through standardised design, procurement, and integrated digital twins. The move signals Bechtel's intent to accelerate large complex builds, particularly in data centers, semiconductors, and advanced manufacturing, where speed-to-market and digital readiness define competitive advantage.

HOCHTIEF Aktiengesellschaft is participating in one of the largest highway projects in the Netherlands, with construction now scheduled to start in January 2026 and the new A15 section and additional A12/A15 lanes targeted for completion by the end of 2031. The project includes 45 bridge structures and ten traffic junctions, anchoring an integrated road network upgrade. The contract reinforces ACS Group's leadership in long-duration European highway concessions and PPP-style delivery, building on its earlier German rail and Munich transit wins for sustained public infrastructure pipeline visibility through 2031.

VINCI SA's Australian subsidiary Seymour Whyte secured three construction contracts worth EUR 431 million in total, covering the southern section of the Coomera Connector on the Gold Coast, road renovation and a new bridge in Moreton Bay, and the design and build of the M5 Motorway Westbound Upgrade in Sydney. The contract slate underlines VINCI's push to expand its civil engineering footprint in Australia, leveraging Seymour Whyte's local presence and delivery expertise across road and bridge programmes in Queensland and New South Wales.

HOCHTIEF Aktiengesellschaft, an ACS Group company, was awarded a major contract by Deutsche Bahn to refurbish a 42-km double-track section of the right-bank Rhine railway from Wiesbaden to Lorchhausen, worth more than EUR 170 million. The scope includes ten level crossings, twelve train stations to be newly built or converted, and two pedestrian underpasses, with works planned from July to December 2026 and preparations starting in summer 2025. The contract reinforces HOCHTIEF's leadership in European rail modernisation and ACS Group's strategic emphasis on government-funded transport infrastructure.

A HOCHTIEF Aktiengesellschaft joint venture was awarded a contract in the high three-digit million-euro range for the construction of the second main line of the Munich S-Bahn rail network, a flagship German urban transport programme. The contract underscores ongoing public investment in suburban rail capacity in Bavaria's largest metropolitan area and reflects HOCHTIEF's strength in heavy and civil engineering construction. The win adds to ACS Group's pipeline of European mobility infrastructure projects and reinforces the role of large contractors in delivering complex multi-year transit programmes.

Building Information Modelling has matured from 3D rendering to a mainstream operating system for project delivery, with around 65% of global construction projects now using BIM workflows and over half of new builds requiring it from the outset. The global BIM market is forecast to grow from approximately USD 4.69 billion in 2025 to USD 5.42 billion by 2026, embedding model-driven design, scheduling, energy planning, and end-of-life deconstruction. The trend is fuelling Global Construction Market growth by reducing rework, improving cost certainty, and giving large contractors a measurable productivity edge over traditional delivery models.

Modular and prefabricated construction is scaling rapidly as owners push for faster schedules, stronger cost certainty, and lower environmental impact. The global modular construction market is projected to reach USD 189.1 billion by 2032, growing at a 6.9% CAGR from 2025. Adoption is rising in healthcare, hospitality, multifamily housing, and data centers, where standardisation, factory quality, and rapid site assembly compress project timelines. The trend is creating new demand for industrial-grade modular factories, integrated logistics, and digital coordination platforms, attracting investment from Lendlease, Skanska, and large public-sector authorities seeking measurable delivery acceleration.

AI, robotics, and automation are moving beyond pilot programmes to become integral to construction project delivery, optimising scheduling, quality control, safety prediction, and physically demanding tasks such as bricklaying and material handling. The AI-in-construction market is forecast to grow from approximately USD 4.86 billion in 2025 to USD 22.68 billion by 2032. Bechtel's February 2026 NVIDIA collaboration on Omniverse-based AI factory delivery exemplifies the shift, while smaller contractors are deploying robotic layout, drones, and computer-vision QA. The trend is restructuring labour models, capital allocation, and competitive differentiation across the global construction landscape.

Decarbonisation is rapidly reshaping global construction supply chains, with the green building materials market forecast to grow at a 10.4% CAGR from USD 26.6 billion in 2024 toward 2030. Customers are demanding low-carbon concrete, mass timber, recycled steel, and embodied-carbon disclosures across procurement scorecards. Government incentives, EU Construction Products Regulation, and large client commitments from data center hyperscalers and public agencies are reinforcing the shift, encouraging suppliers and contractors to invest in CarbonCure-style admixtures, electric fleets, and integrated lifecycle reporting. The trend is altering bid evaluation criteria and capital expenditure plans across major contractors globally.

“Construction Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

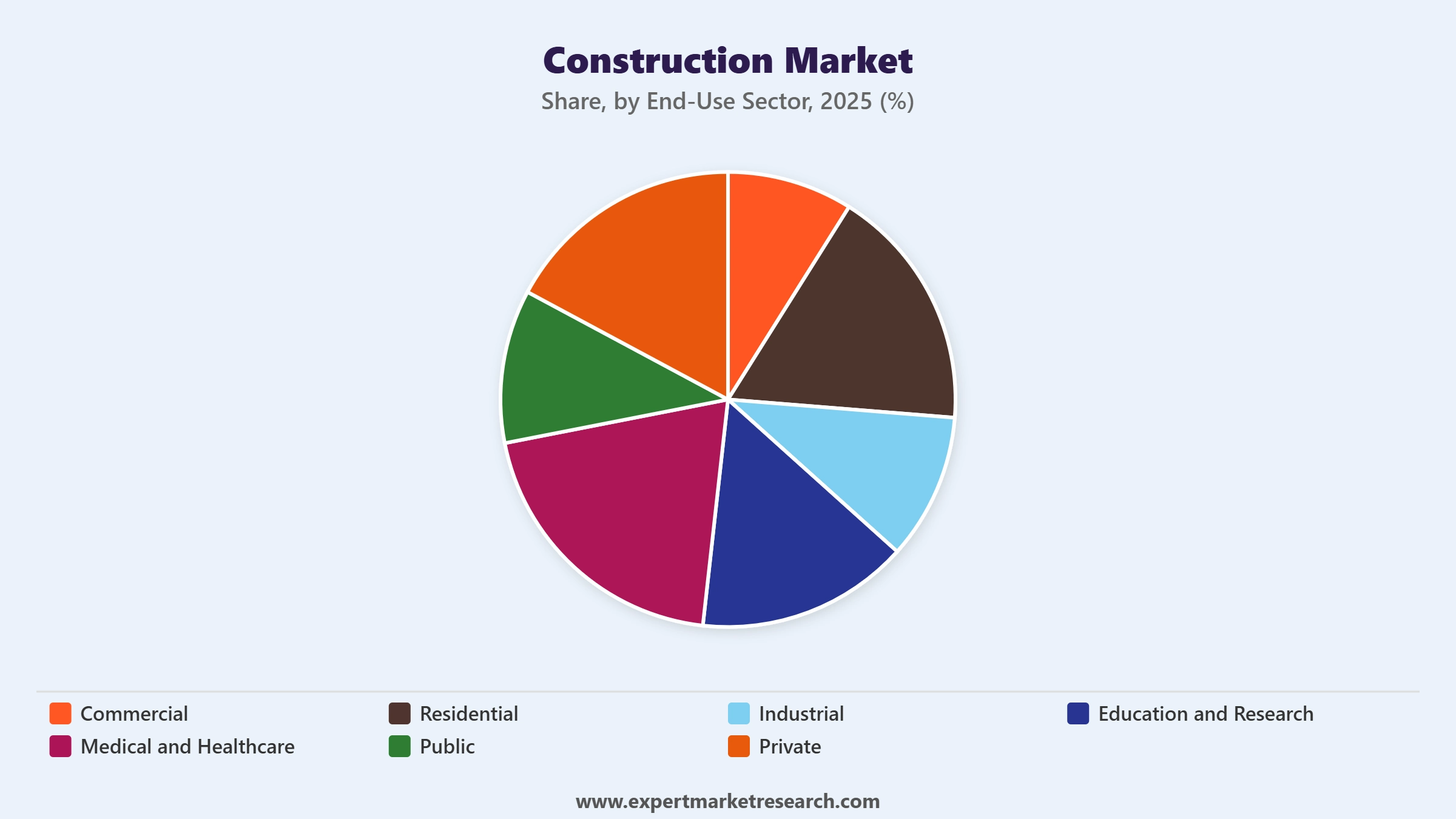

Market Breakup by End-Use Sector

Key Insight: The Commercial sector commands a leading share of demand, anchored by office, retail, hospitality, and the explosive growth of data center construction tied to hyperscaler capex. Residential remains the volume backbone, supported by housing demand in Asia Pacific and steady multifamily growth in North America and Europe, while Industrial spending is rising on the back of advanced manufacturing, semiconductor fabs, and reshoring investments. Public projects dominated by transport, utilities, and social infrastructure benefit from the US Infrastructure Investment and Jobs Act and similar programmes in Europe and Asia. Companies including ACS Group, VINCI SA, China Communications Construction, Bechtel, and Fluor lead delivery across these verticals.

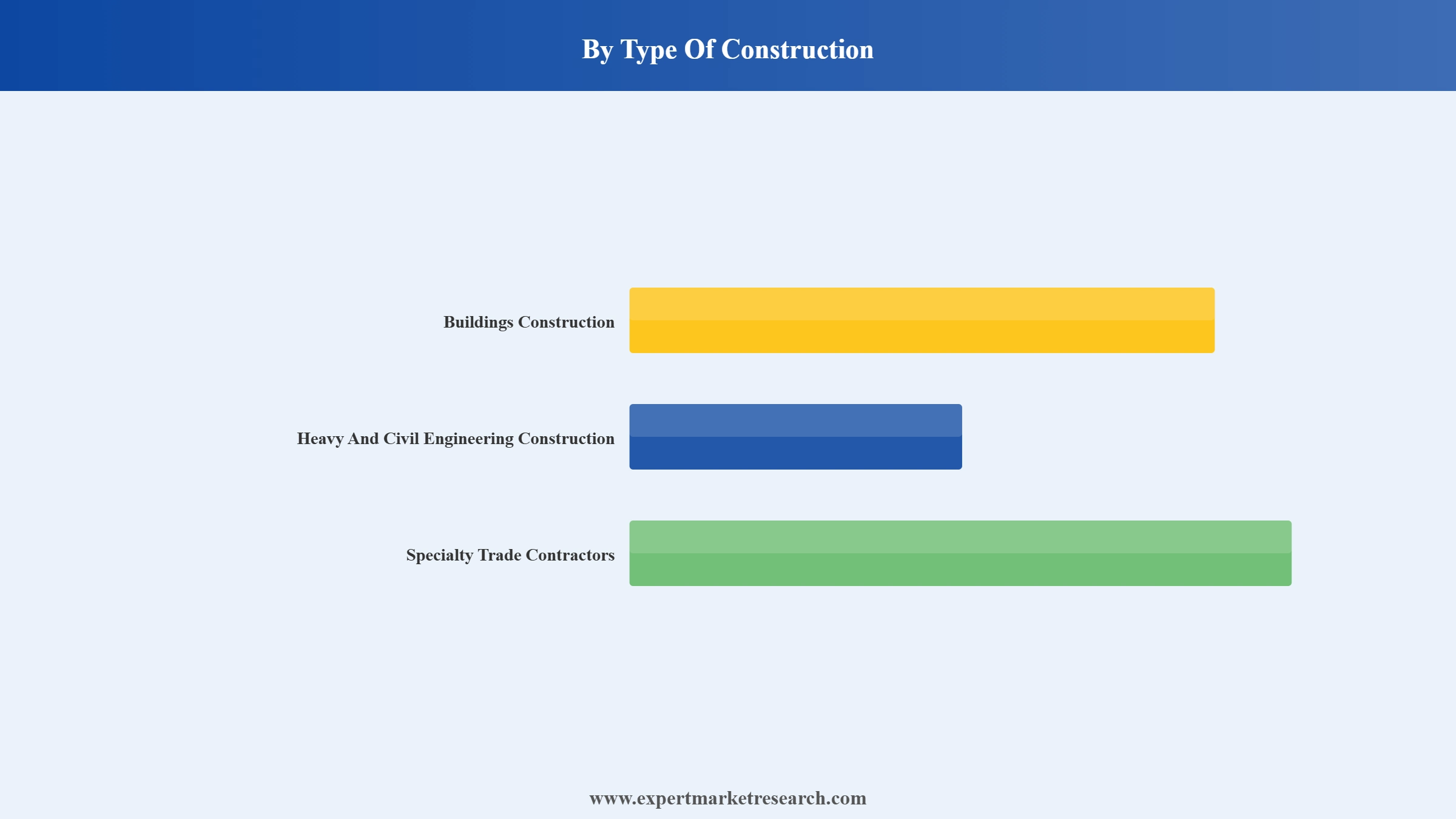

Market Breakup by Type Of Construction

Key Insight: Buildings Construction represents the largest type by spend, capturing residential, commercial, and mixed-use programmes worldwide. Heavy and Civil Engineering Construction is the strategic growth pillar, supported by major rail, highway, port, and energy infrastructure programmes such as HOCHTIEF's Wiesbaden-Lorchhausen rail contract, Munich S-Bahn mainline win, and Netherlands A15 highway project. Specialty Trade Contractors capture growing share as digital MEP, modular interior fit-outs, and façade systems become more sophisticated, while Land Planning and Development benefits from masterplan-led development across new economic zones, smart cities, and free-zone industrial parks across Asia, the Middle East, and parts of Africa.

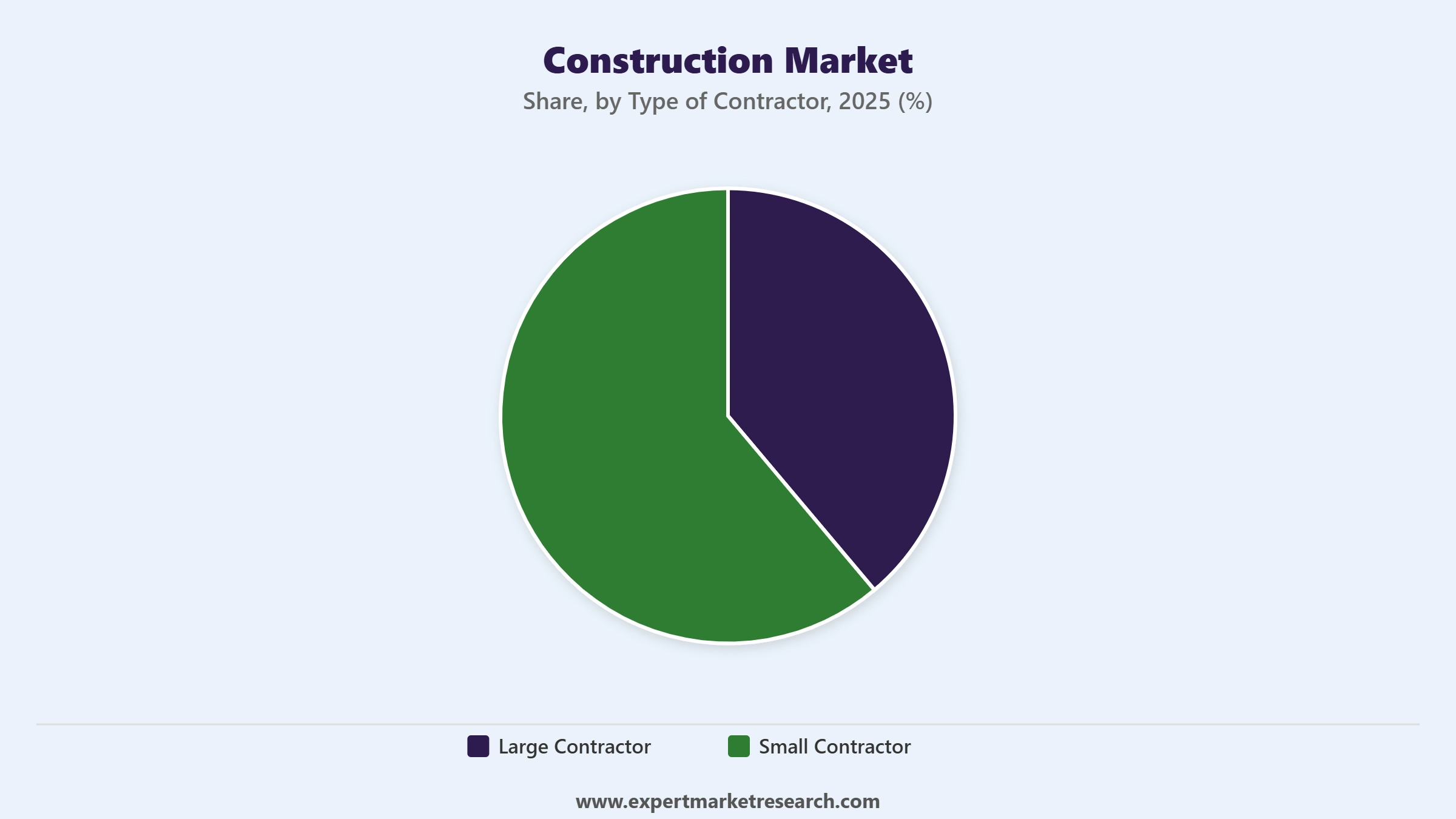

Market Breakup by Type of Contractor

Key Insight: Large Contractors, including ACS Actividades de Construccion y Servicios, VINCI SA, Bouygues SA, China State Construction Engineering, and Bechtel Corporation, capture the majority of revenue across megaprojects in transport, energy, data centers, and complex commercial buildings. Their advantages lie in balance-sheet capacity, multi-discipline expertise, integrated supply chains, and digital delivery platforms. Small Contractors remain the volume backbone for residential, fit-out, and specialty trade work, particularly in fast-growing emerging markets, and play a decisive role in last-mile delivery. Industry digitalisation and prefabrication are gradually shifting share towards integrated large contractors with deep technology investments.

Market Breakup by Region

Key Insight: Asia Pacific leads the global construction market, anchored by China's mature ecosystem, India's accelerating urbanisation, and rising spend across ASEAN, with China State Construction Engineering, China Communications Construction, China Railway Engineering, L&T, Tata Projects, and Hindustan Construction Company among the dominant operators. North America is supported by data center hyperscaler capex, the US Infrastructure Investment and Jobs Act, and major industrial reshoring projects, with Bechtel, Fluor, Kiewit, PCL, Lennar, and D.R. Horton leading. Europe is anchored by ACS Group / HOCHTIEF, VINCI, Bouygues, STRABAG, Skanska, Ferrovial, and Eiffage, while the Middle East and Latin America benefit from energy and transport investments.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Within the End-Use Sector segmentation, Commercial and Residential dominate global construction spend. Commercial leads with strong contributions from office towers, retail, hospitality, and the rapidly expanding data center segment driven by hyperscaler capex from Amazon, Microsoft, Google, and Meta. Residential, especially multifamily and mid-rise, anchors volume across Asia Pacific and North America, supported by housing demand in India, China, and the United States. Lennar Corporation and D.R. Horton, Inc. lead US homebuilding, while CapitaLand Limited and Lendlease Group are dominant in Asia Pacific multifamily and mixed-use, illustrating how scale and integrated land-development capabilities determine share within these high-volume end-use sectors today.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Within the Type of Construction segmentation, Buildings Construction and Heavy and Civil Engineering Construction are the most influential. Buildings Construction captures the largest absolute spend across residential, commercial, and mixed-use projects globally. Heavy and Civil Engineering Construction is the high-growth pillar, supported by mega-programmes including HOCHTIEF's German rail and Munich S-Bahn wins, VINCI's Australian Coomera Connector and M5 Westbound contracts, and ongoing US, EU, and Asia-Pacific infrastructure programmes. China Communications Construction Company, China Railway Engineering Corporation, and Power Construction Corporation of China lead heavy civil delivery, while integrated European players such as ACS Group, VINCI, and Bouygues anchor pan-European pipeline strength.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Within the Type of Contractor segmentation, Large Contractors capture a disproportionate share of revenue and complex project delivery. ACS Actividades de Construccion y Servicios, VINCI SA, Bouygues SA, China State Construction Engineering, China Communications Construction, Bechtel Corporation, Fluor Corporation, and Kiewit Corporation dominate megaproject backlogs across data centers, semiconductors, transit, and energy. Their balance-sheet strength, integrated supply chains, digital delivery investments, and BIM-led operating models reinforce structural advantages. Small Contractors retain the residential and fit-out volume, but the rise of modular construction, AI-enabled scheduling, and Bechtel's NVIDIA-powered Omniverse delivery model is gradually shifting share towards technology-led integrated large contractors with global reach.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Asia Pacific is the leading regional market in global construction, anchored by China's mature delivery ecosystem, India's accelerating urbanisation, and steady spend across ASEAN economies. China State Construction Engineering, China Communications Construction Company, China Railway Engineering Corporation, Power Construction Corporation of China, Yunnan Zhiling Construction Engineering, and Zhejiang Yijian Construction Group lead Chinese delivery across infrastructure, residential, and industrial projects. India's L&T Engineering & Construction Division, Tata Projects, and Hindustan Construction Company are scaling capacity to meet metro rail, expressway, airport, and renewable-energy demand. Southeast Asian growth in data centers, semiconductors, and mixed-use developments reinforces regional momentum, while CapitaLand and Lendlease drive integrated commercial-residential masterplans across Singapore, Australia, and Indonesia.

Europe represents a mature, technology-led regional market underpinned by major government infrastructure programmes and net-zero policy. ACS Actividades de Construccion y Servicios with HOCHTIEF, VINCI SA, Bouygues SA, STRABAG International, Skanska AB, Ferrovial SE, and Eiffage SA dominate the contractor landscape. Recent flagship wins include HOCHTIEF's EUR 170 million Deutsche Bahn Wiesbaden-Lorchhausen rail contract, the high three-digit million-euro Munich S-Bahn mainline contract, and the Netherlands A15/A12 highway programme starting January 2026. Investment is anchored by EU Recovery and Resilience funding, member-state transport budgets, and rising demand for sustainable building materials, with green-building procurement increasingly weighted alongside cost and schedule criteria.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The Global Construction Market is large, diverse, and highly fragmented globally, but consolidated at the megaproject end where ACS Actividades de Construccion y Servicios, VINCI SA, Bouygues SA, China Communications Construction, Bechtel Corporation, and Fluor Corporation set the pace. Competitive priorities have shifted decisively towards digital project delivery, modular execution, AI-led scheduling, and decarbonised materials.

Recent flagship wins, such as HOCHTIEF's Deutsche Bahn rail contract, VINCI's EUR 431 million Australian package, the Munich S-Bahn mainline win, and Bechtel's February 2026 NVIDIA partnership for AI-driven Omniverse delivery, underscore how technology and integrated services are reshaping competitive positioning. Asia Pacific is dominated by China State Construction Engineering, China Railway Engineering, Power Construction Corporation, and L&T, while Skanska AB, Ferrovial SE, and STRABAG International continue to anchor Nordic, Iberian, and Central European delivery.

Founded in 1997 and headquartered in Madrid, Spain, ACS Group is one of the world's largest construction and infrastructure companies, with HOCHTIEF Aktiengesellschaft as its core German subsidiary. Its 2025-2026 wins include the EUR 170 million Deutsche Bahn rail contract, the Munich S-Bahn mainline JV, and Netherlands A15 highway involvement.

Founded in 1899 and headquartered in Rueil-Malmaison, France, VINCI SA is a global concessions and construction major. In July 2025, its Australian subsidiary Seymour Whyte secured EUR 431 million in contracts spanning the Coomera Connector, Moreton Bay bridge, and the Sydney M5 Motorway Westbound Upgrade, expanding VINCI's Australian footprint.

Founded in 1898 and headquartered in Reston, USA, Bechtel Corporation is a leading EPC company with deep capabilities across infrastructure, energy, and advanced manufacturing. In February 2026, Bechtel established a new EPC transformation senior vice-president role and deepened its NVIDIA Omniverse partnership for AI-driven project delivery.

Founded in 2005 and headquartered in Beijing, China, China Communications Construction Company is one of the world's largest infrastructure groups, delivering ports, highways, bridges, and rail across China and the Belt and Road economies. Its scale, integrated supply chain, and government backing underpin its global heavy-civil leadership today.

Other key players in the market are HOCHTIEF Aktiengesellschaft, Bouygues SA, STRABAG International GmbH, Power Construction Corporation of China, China State Construction Engrg. Corp. Ltd., Skanska AB, Ferrovial SE, Fluor Corporation, PCL Constructors Inc., Eiffage S.A., Kiewit Corporation, Lennar Corporation, D.R. Horton, Inc., CIMIC Group, Shimizu Corporation, Lendlease Group, CapitaLand Limited, L&T Engineering & Construction Division, Tata Projects Ltd, Hindustan Construction Company, China Railway Engineering Corporation, Yunnan Zhiling Construction Engineering Co., Ltd., Zhejiang Yijian Construction Group Co, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Discover the latest insights on the Global Construction Market 2026 with our comprehensive report. Stay ahead of the curve with valuable data on modular construction innovations, BIM and AI adoption, and top growth regions. Whether you are bidding on a flagship infrastructure project, expanding your data center delivery capability, or scaling residential supply, this report gives you the clarity you need. Download your free sample now and discover the key opportunities in the thriving Global Construction industry.

United Kingdom Construction Market

South Korea Construction Market

Australia Construction Market

Prefabricated Buildings Construction Trends

Construction Chemicals Building Material Insights

Construction Aggregates Demand Analysis

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

The market size of construction industry was valued at USD 14.45 Trillion in 2025.

The market is projected to grow at a CAGR of 6.50% between 2026 and 2035.

The revenue generated from the construction market is expected to reach USD 27.12 Trillion in 2035.

The increasing adoption of building information modelling (BIM), the rise of modular construction, emphasis on green building practices, technological advancements and automation are the major trends impacting the construction industry growth rate.

The market is categorised according to the end use, which includes commercial, residential, industrial, education and research, public, private, medical and healthcare and others.

The market key players are ACS, ACTIVIDADES DE CONSTRUCCIÓN Y SERVICIOS, S.A., HOCHTIEF Aktiengesellschaft, VINCI SA, China Communications Construction Company Limited, Bouygues SA, STRABAG International GmbH, Power Construction Corporation of China, China State Construction Engrg. Corp. Ltd., Skanska AB, Ferrovial SE, Fluor Corporation, PCL Constructors Inc., Eiffage S.A. (Eiffage Construction), Bechtel Corporation, Kiewit Corporation, Lennar Corporation, D.R. Horton, Inc., CIMIC Group, Shimizu Corporation, Lendlease Group, CapitaLand Limited, L&T Engineering & Construction Division, Tata Projects Ltd, Hindustan Construction Company, China Railway Engineering Corporation, Yunnan Zhiling Construction Engineering Co., Ltd., Bechtel Corporation, and Zhejiang Yijian Construction Group Co, among others.

The market is broken down into North America, Europe, Asia Pacific, Latin America, the Middle East, and Africa.

The Asia-Pacific region is the fastest-growing region in the global Construction market, driven by rising demand across industrial, automotive, and power sectors.

The construction sector presents extensive prospects for advancing innovation, fostering sustainable progress, and expanding infrastructure.

Factors such as economic downturns, regulatory obstacles, and fluctuations in material expenses serve as constraints on the demand for the construction sector.

The top five companies in the construction market are Fluor Corporation, PCL Constructors Inc., Eiffage S.A. (Eiffage Construction), Bechtel Corporation, and Kiewit Corporation.

North America had the largest share of the market.

The heavy and civil engineering construction category dominated the market.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| Report Features | Details |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by End-Use Sector |

|

| Breakup by Type Of Construction |

|

| Breakup by Type of Contractor |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.