Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

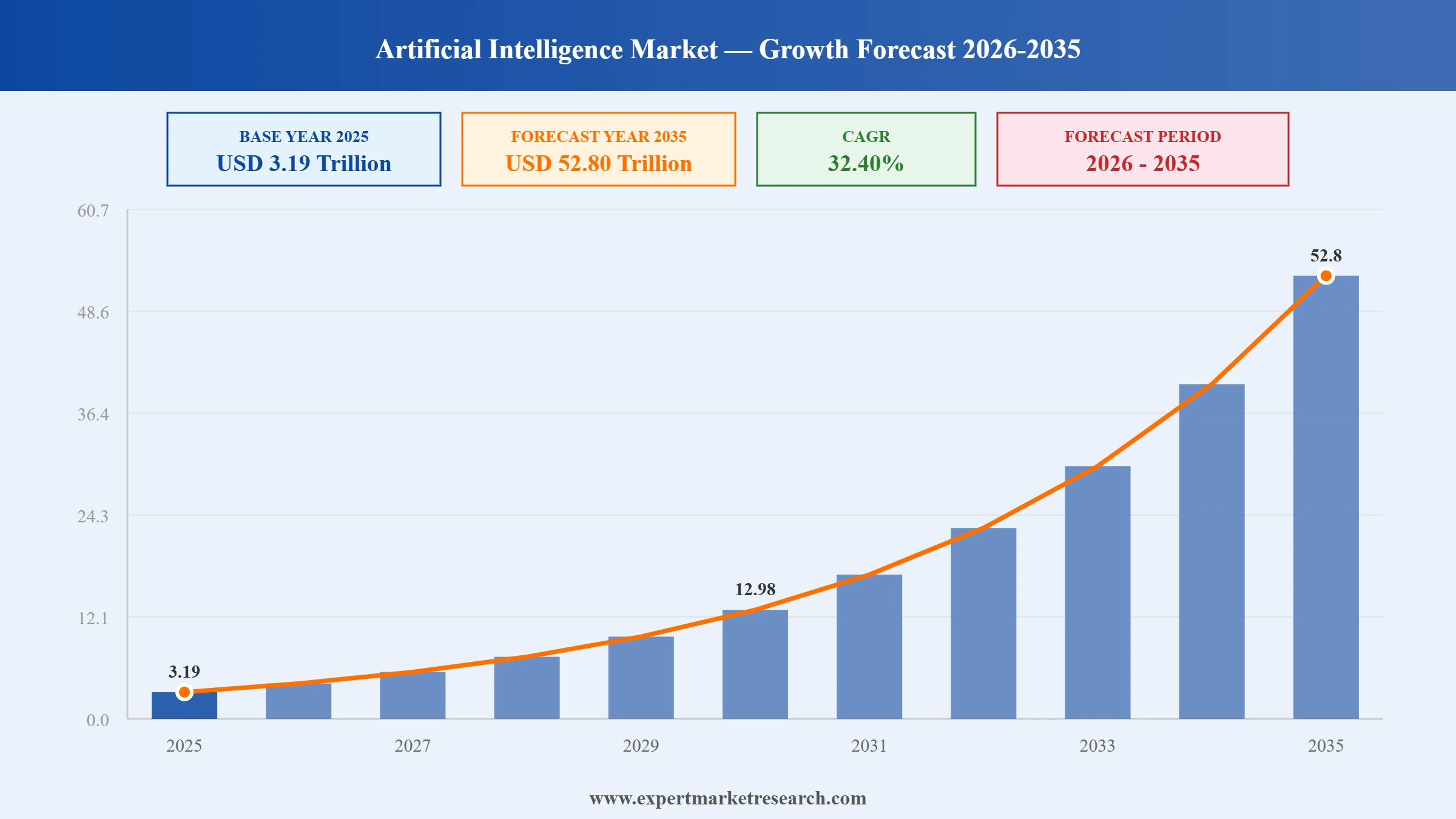

The global artificial intelligence market was valued at USD 3.19 Trillion in 2025 and is projected to reach USD 52.80 Trillion by 2035 expanding at a CAGR of 32.40% over the forecast period 2026 and 2035, according to Expert Market Research. This trajectory represents one of the most aggressive compound growth rates recorded across any major technology market driven by enterprise adoption, generative AI proliferation, escalating cloud AI infrastructure investment, and the systematic embedding of machine intelligence across healthcare, finance, manufacturing, retail, and public sector applications worldwide.

Artificial intelligence has transitioned from a specialised research capability into a foundational economic infrastructure. Governments are releasing national AI policy frameworks. Corporations are treating AI investment as a strategic imperative equivalent to electrification in prior industrial eras. Frontier model development is accelerating capability at a pace that continues to exceed most forecasts from even two years prior.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The artificial intelligence market encompasses the global commercial ecosystem of hardware, software, and services that enable the development, training, deployment, and operationalisation of intelligent systems capable of performing tasks that historically required human cognition. The market includes semiconductor and computing hardware for AI workloads, foundational model platforms, machine learning frameworks, natural language processing tools, computer vision systems, robotics software, AI-as-a-service platforms, and the professional services that design and integrate these systems into enterprise environments.

The market serves every vertical industry and virtually every functional department within organisations of all sizes, making it structurally distinct from most technology markets in its breadth of end-user application and geographic demand diversity.

Enterprise adoption of AI across healthcare, financial services, manufacturing, retail, logistics, and professional services is the primary demand engine of the global AI market. Organisations are deploying AI for predictive analytics, customer service automation, supply chain optimisation, fraud detection, medical imaging analysis, drug discovery, and personalised content delivery. The transition from experimental pilots which characterised most enterprise AI investment through 2022 to production deployment at scale is expanding both the volume and the contract value of AI software and services procurement. AI spending is increasingly classified as operational infrastructure investment rather than R&D expenditure, embedding it within recurring capital budgets rather than discretionary innovation funds.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Generative AI and large language models represent the most commercially significant AI capability wave since the development of deep learning. The proliferation of foundational models including GPT-family models from OpenAI, Gemini from Google DeepMind, Claude from Anthropic, and Llama from Meta has democratised access to sophisticated AI capability for enterprises of all sizes through API-accessible cloud services. Meta's April 2026 release of Llama 4 as a multimodal open-weight model further accelerates enterprise adoption by enabling deployment of advanced AI without dependency on proprietary API relationships. Generative AI is driving incremental revenue across software (AI-native applications and workflow tools), hardware (GPU and accelerator demand for inference workloads), and services (AI integration consulting and implementation).

National governments across every major economy have introduced dedicated AI investment programmes and governance frameworks that simultaneously accelerate domestic AI capability development and create procurement demand for AI technology and services. The US White House National Policy Framework for Artificial Intelligence, released March 20, 2026, outlined federal legislative priorities that emphasise innovation, uniformity, and preemption of fragmented state regulation. The EU AI Act, now in phased implementation with GPAI rules effective August 2, 2025, creates a compliance-driven AI services market estimated to generate substantial professional services and compliance technology revenue across EU member states. China's series of AI regulations including the April 2026 Anthropomorphic Interaction Services measures reflects the government's dual objective of enabling world-leading AI development while maintaining regulatory control over consumer-facing AI applications.

Cloud computing infrastructure is the enabling layer that makes AI deployment economically accessible and operationally scalable for organisations that lack the capital to build on-premise AI compute infrastructure. Hyperscale cloud providers including Amazon Web Services, Microsoft Azure, and Google Cloud have made AI the central competitive differentiator in their platform strategies, integrating AI capabilities at every layer from raw compute to application-level services. The availability of GPU cloud instances, managed AI model APIs, AI development tools, and pre-trained model libraries through cloud marketplaces has dramatically reduced the time-to-deployment for enterprise AI projects. Cloud AI deployment is the dominant and fastest-growing deployment mode within the AI market, driven by elasticity, global accessibility, and the opex-versus-capex economic model that cloud infrastructure enables.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Generative AI is restructuring product development cycles across software, media, pharmaceutical, automotive, and consumer goods industries. In software development, AI coding assistants are demonstrably compressing development timelines; in drug discovery, AI-driven molecular generation is reducing early-stage research costs; in media and entertainment, generative AI is enabling content creation at scales and speeds previously requiring substantially larger production teams. The commercial value of generative AI lies not in replacing human creativity but in amplifying the productive output of human teams a dynamic that is expanding total addressable market by making AI tools economically justifiable for organisations and functions that previously lacked the budget for dedicated AI investment.

Agentic AI systems that plan and execute multi-step tasks autonomously with minimal human intervention represents the next commercial frontier beyond the conversational AI and generative content tools that defined the 2023-2025 AI adoption cycle. Agentic systems are capable of browsing the web, writing and executing code, managing files, communicating with external systems, and completing complex research or operational tasks that previously required human time and attention. Enterprise deployment of AI agents for functions including customer onboarding, procurement, IT operations, and financial reconciliation is generating a new category of AI software investment that extends beyond model API costs to include orchestration platforms, tool integrations, and governance frameworks. The agentic AI segment is expected to represent a disproportionate share of incremental AI market growth through the late forecast period.

The emergence of binding AI regulation most advanced in the EU but accelerating across major economies is creating a structurally significant compliance technology and advisory services market within the broader AI ecosystem. The EU AI Act's provisions covering high-risk AI systems, transparency requirements for GPAI model providers, and conformity assessment obligations are generating demand for AI audit, documentation, risk classification, and governance platform products. The May, 2026 EU Digital Omnibus amendments introduced targeted simplifications to GPAI governance obligations while adding new substantive policy provisions, indicating that regulatory evolution will be continuous rather than settled. For AI vendors, regulatory compliance is both a cost centre and a competitive differentiator organisations that can credibly demonstrate regulatory compliance are better positioned in government and regulated-industry procurement.

Edge AI the deployment of AI inference workloads on devices at or near the source of data generation rather than in centralised cloud infrastructure is expanding the market for AI hardware beyond datacenter GPUs into automotive, industrial, consumer electronics, and telecommunications applications. Edge AI enables real-time AI processing for applications including autonomous driving, industrial quality inspection, smart grid management, and next-generation smartphone features without the latency constraints of cloud round-trip communication. The combination of increasingly capable AI accelerator chips optimised for low-power edge deployment and software frameworks for model compression and quantisation is making edge AI commercially viable across a rapidly expanding range of end-use cases.

The global AI market faces structural challenges that intensify as the technology scales and its societal impact deepens. Data privacy and security risks represent the most operationally pervasive challenge: AI systems require large volumes of training data that may include sensitive personal, financial, or health information, creating regulatory liability under frameworks including GDPR, HIPAA, and the EU AI Act's data governance provisions. AI hallucination the generation of confidently stated factually incorrect outputs remains a persistent quality concern in high-stakes enterprise deployments, particularly in legal, medical, and financial contexts where accuracy is non-negotiable. Cybersecurity risk is expanding: AI systems are both high-value attack targets and capable tools for malicious actors seeking to generate phishing content, automate vulnerability discovery, or create deepfake misinformation at scale. Talent scarcity across AI research, engineering, and ethics disciplines constrains the pace of both commercial deployment and responsible governance investment.

Several structural dynamics constrain the pace of AI market expansion below its theoretical ceiling. Energy consumption is an increasingly recognised physical constraint: training frontier AI models and operating large-scale inference infrastructure at the scale the market demands requires power and cooling investment that is outpacing grid capacity in many data centre markets, creating real bottlenecks in hyperscaler expansion plans. The concentration of foundational model development capability among a small number of well-capitalised organisations creates ecosystem dependency risks for the enterprises, startups, and governments that build on top of these platforms. Regulatory uncertainty across jurisdictions introduces investment hesitation: organisations making multi-year AI platform commitments must forecast regulatory environments that are actively evolving, creating planning complexity particularly for global deployments. The EU AI Act's compliance timelines, US federal preemption debates, and China's expanding AI product regulations each create distinct and non-harmonised compliance landscapes that multinational AI vendors must navigate simultaneously.

The global AI market presents transformative, durable, and expanding commercial opportunities across every market tier. The shift from cloud AI to edge AI creates a multi-billion dollar hardware opportunity for chip designers, device manufacturers, and embedded software developers as AI inference migrates from datacenters to endpoints. The AI governance and compliance services market is an entirely new commercial category generated by regulatory frameworks one that is structurally recurring and growing in step with the complexity and volume of AI deployments. Emerging market AI adoption across India, Southeast Asia, the Middle East, and Latin America represents an underpenetrated growth frontier where digital infrastructure investment and government AI development ambitions are creating enabling conditions for rapid AI market expansion from a relatively low base. AI applications in healthcare, particularly medical imaging, diagnostic support, drug discovery, and personalised treatment planning, represent one of the highest-value enterprise AI segments given healthcare's combination of data richness, outcome importance, and willingness to invest in accuracy-improving technology.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

“Artificial Intelligence Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

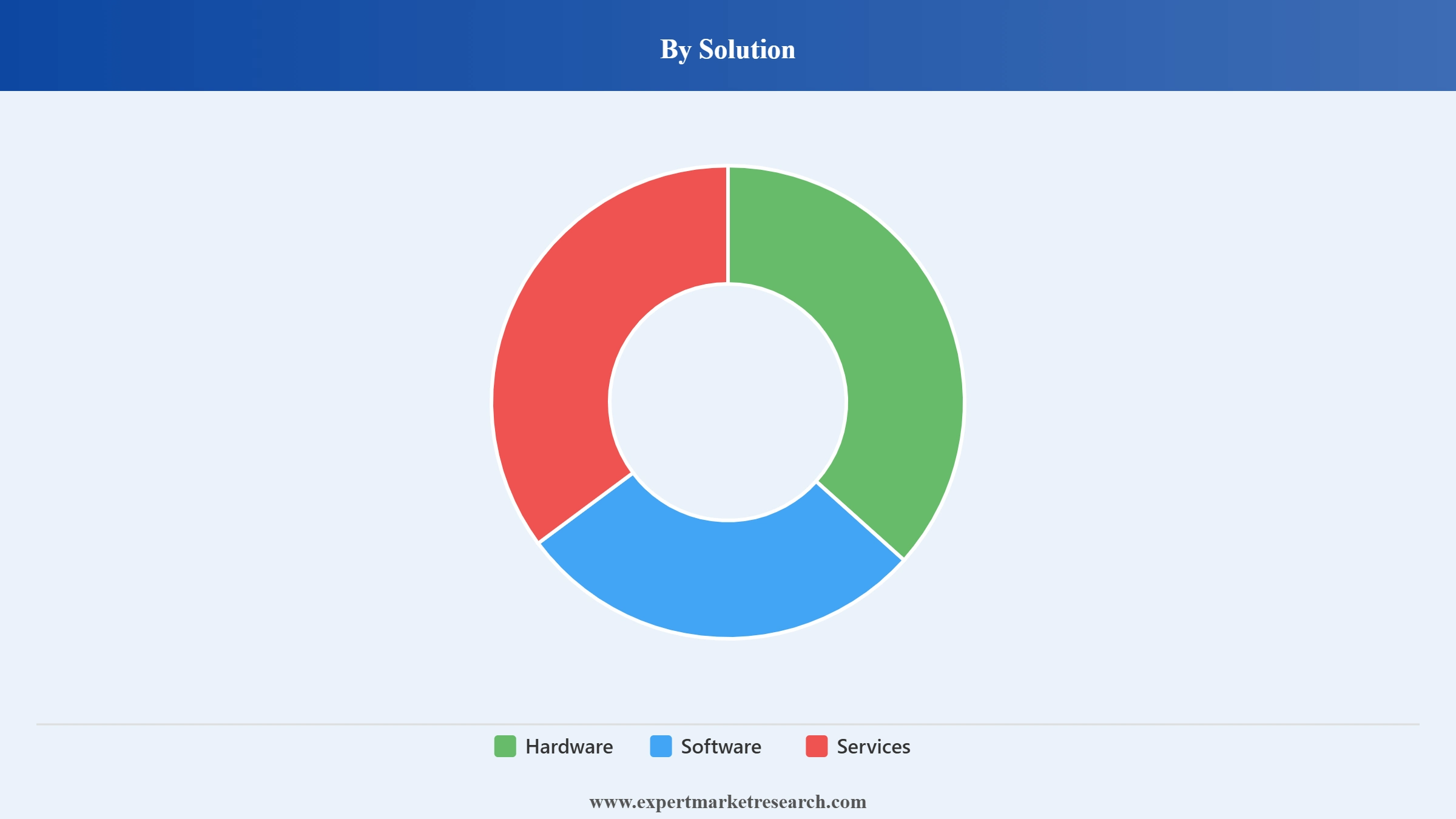

Market Breakup by Solution

Hardware encompasses AI-specific semiconductors including GPUs, TPUs, neural processing units, and field-programmable gate arrays, as well as the servers, networking equipment, and data centre infrastructure required to support AI training and inference workloads. NVIDIA Corporation dominates the AI hardware segment through its H100 and Blackwell GPU architectures, with demand substantially exceeding supply across the enterprise and hyperscaler buyer base.

Software encompasses AI platforms and frameworks, foundational model APIs, MLOps tooling, AI application development environments, and vertical-specific AI software products. Software is the largest revenue segment by offering within the AI market and the primary driver of the market's recurring revenue base.

Services encompasses AI strategy consulting, model training and fine-tuning services, AI integration and implementation, managed AI operations, and AI governance and compliance advisory. Services is the fastest-growing offering segment by revenue as enterprise demand for implementation capability exceeds available internal expertise.

Market Breakup by Technology

Machine Learning is the dominant and broadest technology sub-segment, encompassing supervised, unsupervised, and reinforcement learning approaches that form the algorithmic foundation of most commercial AI applications.

Natural Language Processing is the fastest-growing technology segment, driven by the commercial explosion of large language models, generative AI writing tools, conversational AI assistants, and AI-powered document processing systems.

Computer Vision serves manufacturing quality inspection, medical imaging, retail analytics, autonomous vehicles, and security applications with growing commercial maturity.

Robotics Process Automation and Others encompass autonomous systems, expert systems, recommendation engines, and the emerging agentic AI category.

Market Breakup by Type

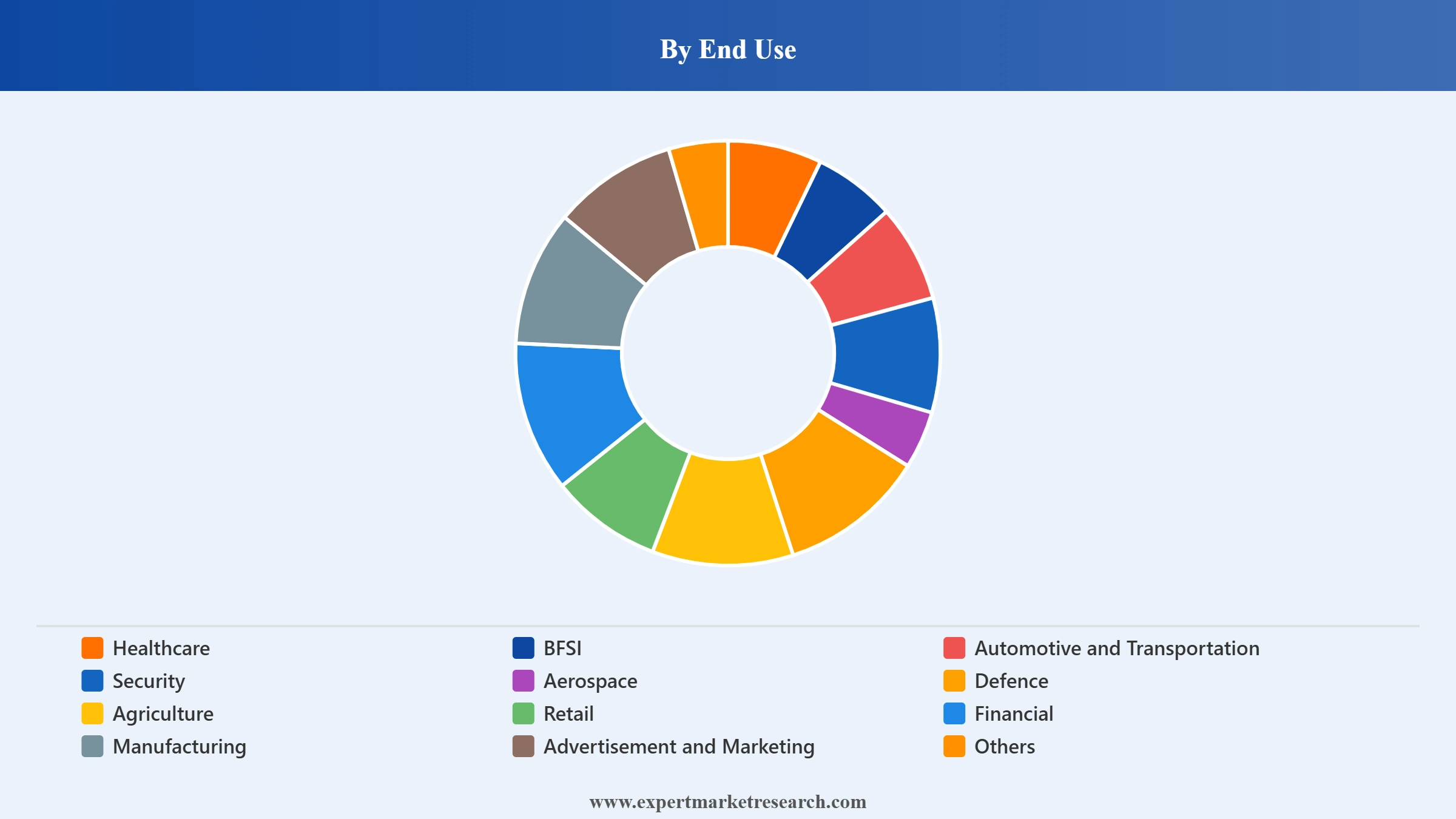

Market Breakup by End Use

Healthcare, BFSI, Retail and E-Commerce, Manufacturing, IT and Telecom, Government and Defence, Education, and Others each represent distinct AI application ecosystems with different technology requirements, procurement timelines, and regulatory contexts. Healthcare and BFSI collectively represent the highest per-deployment AI spending due to the combination of data complexity, outcome stakes, and regulatory compliance requirements that characterise both verticals.

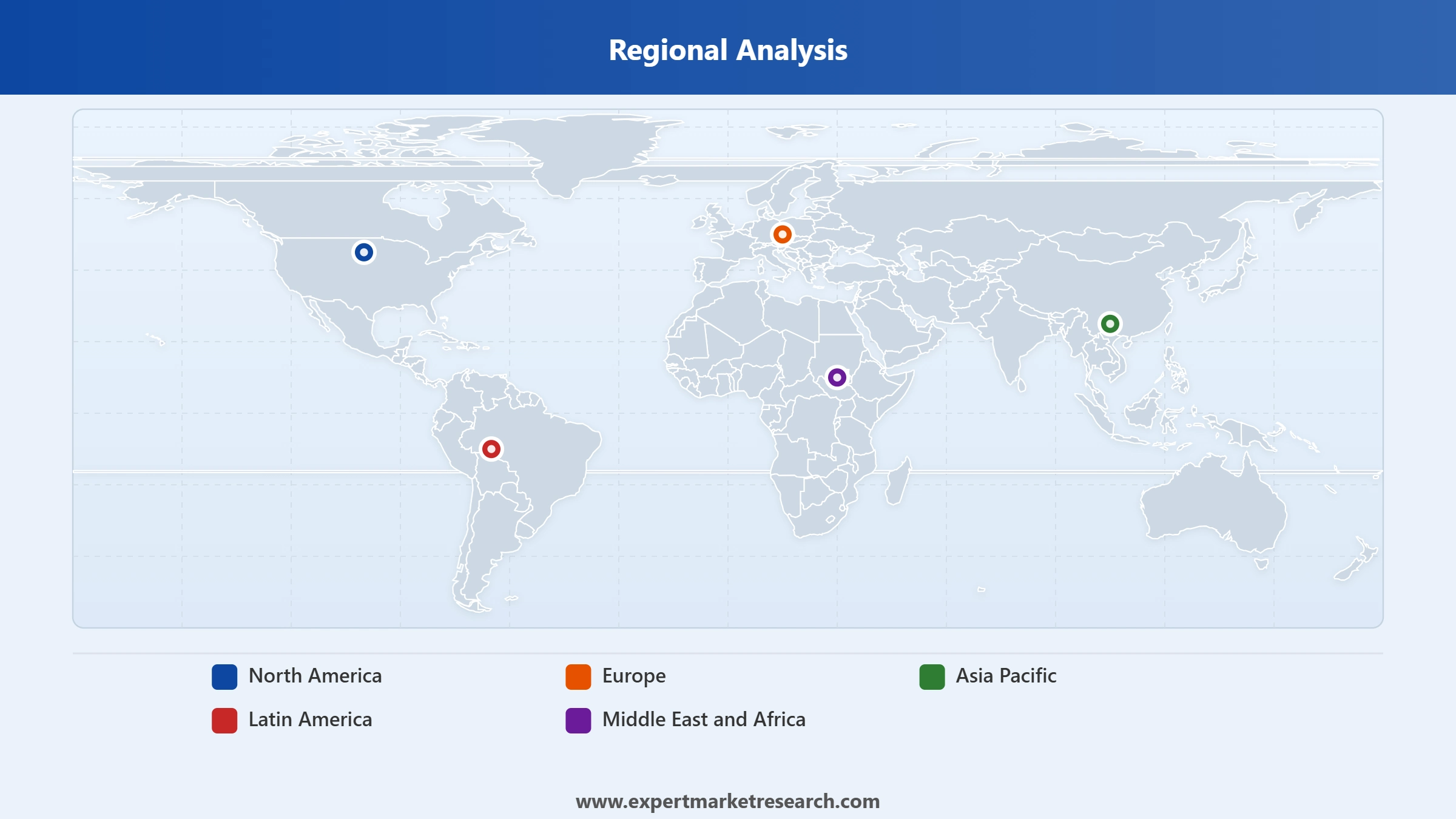

Market Breakup by Region

The companies are pioneers in computer technology, spanning hardware, software, and cognitive solutions, fostering advancements in technology, and business.

Microsoft Corporation Microsoft is the world's largest enterprise AI platform provider through its Azure AI cloud services and its integration of OpenAI's GPT models across Microsoft 365, GitHub Copilot, Azure OpenAI Service, and Dynamics 365. Microsoft's AI revenue generation spans cloud infrastructure, productivity software, and developer tools, positioning it as the dominant commercial beneficiary of the enterprise AI adoption cycle.

Alphabet Inc. (Google) Google DeepMind leads foundational AI research, with the Gemini multimodal model family powering Google Search AI Overviews, Google Cloud Vertex AI, and enterprise products across Workspace and Maps. Google's integration of AI into its core search advertising infrastructure makes it the largest revenue-generating AI-adjacent business globally.

AWS provides the largest cloud infrastructure base for AI training and inference globally, with purpose-built AI services including Amazon Bedrock, SageMaker, and the Trainium and Inferentia custom AI chip families targeting cost-efficient large-scale AI deployment.

NVIDIA Corporation NVIDIA is the dominant supplier of AI accelerator hardware, with its H100, H200, and Blackwell GPU architectures commanding the majority of AI training compute procurement. NVIDIA's CUDA software ecosystem creates a structural advantage that has proven durable against AMD and Intel competitive entries.

Meta's open-weight Llama model family with Llama 4 released April, 2026 in multimodal form has established Meta as the leading provider of open-source foundational AI models, enabling enterprise and developer deployments independent of proprietary API relationships and driving a significant portion of the global AI research and fine-tuning ecosystem.

Other players in the global artificial intelligence market are Cisco Systems, Inc, Amazon Web Services (AWS), Alphabet Inc., Meta Platforms, Inc., Apple Inc., and NVIDIA Corporation, among others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

North America is the largest regional market in the global AI landscape, anchored by the United States' concentration of hyperscale cloud infrastructure, frontier AI model development, venture capital investment, and enterprise AI adoption.

United States The US is home to the world's leading AI companies including NVIDIA, Google, Microsoft, Meta, Amazon, and OpenAI, and hosts the majority of global AI venture investment. The White House's March, 2026 National Policy Framework for AI has set the legislative direction for federal AI governance, emphasising innovation-first policy, federal preemption of state laws, and targeted protections for children and workers.

Asia Pacific is the fastest-growing regional AI market, driven by China's state-backed AI development programme, India's expanding AI adoption across IT services and enterprise, Japan's industrial AI deployment in manufacturing, and South Korea's investment in AI-integrated semiconductor and electronics industries.

India's government AI initiatives, expanding pool of AI engineering talent, and the deployment of AI across banking, agriculture, healthcare, and e-commerce are creating one of the world's most rapidly growing AI demand environments.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Europe's AI market is shaped by the EU AI Act's phased implementation, which has created both compliance overhead and a significant market opportunity for AI governance tools and advisory services. Germany, France, and the United Kingdom are the largest European AI markets, with deep enterprise AI adoption in automotive manufacturing, financial services, and pharmaceuticals.

The Middle East is an emerging AI market of growing strategic significance, with Gulf state governments deploying AI as a central pillar of economic diversification strategies. Saudi Arabia's national AI strategy and UAE's AI Ministry have attracted global AI company investment and partnerships.

Brazil and Mexico lead Latin American AI adoption, with financial services AI, agricultural technology AI applications, and digital commerce AI representing the primary growth vectors.

United States Artificial Intelligence Market

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

The global AI market was valued at USD 3.19 Trillion in 2025, according to Expert Market Research.

The AI market is projected at a CAGR of 32.40% between 2026 and 2035, one of the highest sustained growth rates across any major technology market.

The global AI market is projected to reach USD 52.80 Trillion by 2035, growing at a CAGR of 32.40%, according to Expert Market Research.

Machine Learning is the dominant technology segment within the global AI market. Natural Language Processing is the fastest-growing segment, driven by large language models and generative AI adoption.

North America leads the global AI market, anchored by the United States which hosts the world's leading AI companies, the largest AI cloud infrastructure, and the highest enterprise AI adoption rates. Asia Pacific is the fastest-growing region.

Key players in the global AI market include Microsoft, Alphabet (Google), Amazon Web Services, NVIDIA, Meta Platforms, IBM, Baidu, Salesforce, Oracle, and SAP, among others profiled in the full Expert Market Research AI Market Report.

Key growth drivers include enterprise AI adoption across industries, generative AI and large language model proliferation, government national AI strategies and investment, cloud infrastructure enabling scalable AI deployment, and agentic AI expanding automation capability into complex multi-step workflows.

Key challenges include data privacy and security risks, AI hallucination and accuracy limitations in high-stakes use cases, escalating energy consumption for AI infrastructure, cybersecurity vulnerabilities, regulatory compliance complexity across multiple national frameworks, and AI talent scarcity.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Solution |

|

| Breakup by Technology |

|

| Breakup by Type |

|

| Breakup by End Use |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

| Report Price and Purchase Option | Explore our purchase options that are best suited to your resources and industry needs. |

| Delivery Format | Delivered as an attached PDF and Excel through email, with an option of receiving an editable PPT, according to the purchase option. |

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.