Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

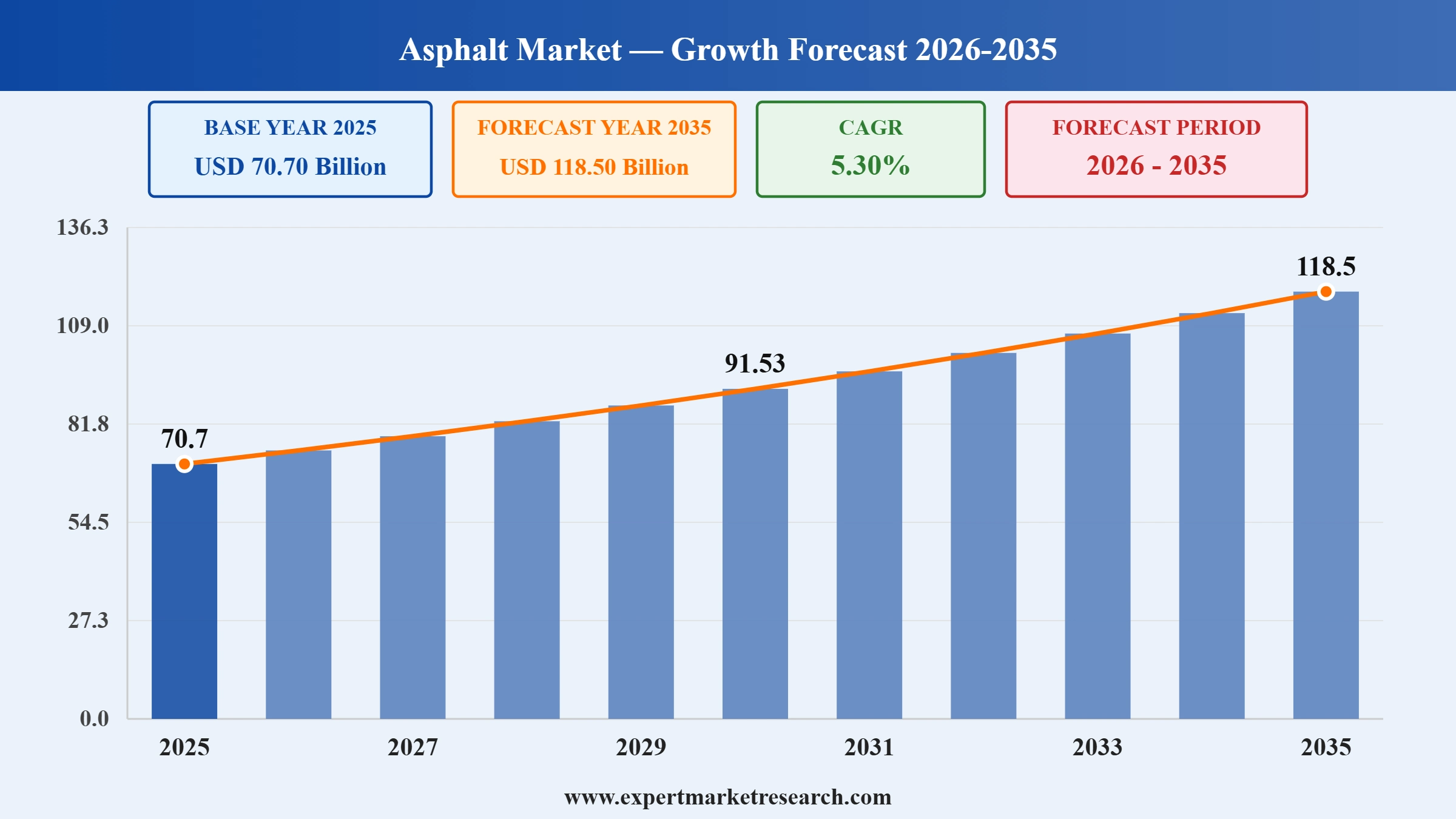

The global asphalt market was valued at USD 70.70 Billion in 2025. The market is expected to grow at a CAGR of 5.30% during the forecast period of 2026-2035 to reach a value of USD 118.50 Billion by 2035. Expanding road construction and highway rehabilitation projects are driving the overall growth in the market.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The global asphalt market is experiencing steady consolidation and geographic expansion, supported by sustained infrastructure spending under government programmes in North America and large-scale urbanisation across Asia. Acquisition-led growth is the dominant strategy among leading contractors, who are acquiring hot-mix plant assets and regional operators to deepen market presence. Sustainability is beginning to reshape product development, with bio-based and recycled asphalt alternatives gaining traction as environmental regulations tighten.

In February 2026, Construction Partners Inc. acquired GMJ Paving Company, a leading asphalt paving contractor for public infrastructure projects in the Houston metro area, adding its twelfth hot-mix plant in the region. The strategically located Baytown plant complements CPI's existing liquid asphalt terminal, strengthening its production throughput and market position in the US asphalt sector.

In October 2025, Construction Partners Inc. acquired eight hot-mix asphalt plants and associated crews from affiliates of Vulcan Materials Company in the Houston metro area. Integrated into Durwood Greene Construction, the transaction significantly expanded CPI's capacity in one of the fastest-growing infrastructure markets in the US asphalt sector.

In May 2025, Construction Partners Inc. acquired PRI of East Tennessee and Pavement Restorations Inc., adding a hot-mix asphalt plant in Knoxville and a specialised pavement preservation business. The deal extended CPI's infrastructure footprint into northeastern Tennessee and strengthened its pavement preservation service line within the US asphalt market.

In February 2025, Construction Partners Inc. acquired Mobile Asphalt Company LLC, adding five hot-mix asphalt plants serving southwest Alabama. The transaction expanded CPI's production and paving capabilities in the Mobile metro area, a high-growth corridor benefiting from Port of Mobile activity and Gulf Coast development.

Road construction and rehabilitation dominate global asphalt demand, with roadways accounting for approximately 68% of total consumption. In the global asphalt market, publicly funded highway programmes and urban resurfacing contracts provide a stable, recurring demand base that is relatively insulated from cyclical downturns, sustaining contractor backlogs and plant utilisation rates.

Sustainability regulation is accelerating the adoption of warm-mix asphalt, which reduces production temperatures and greenhouse gas emissions, alongside recycled asphalt pavement programmes that cut raw material costs. In 2024, Fraport AG partnered with startup B2Square to test bio-asphalt made from cashew-based organic bitumen at Frankfurt Airport, signalling the direction of asphalt market growth toward low-emission formulations.

Asia Pacific, led by China and India, commands the largest regional share of the global asphalt market, representing nearly 39% of revenues in 2024. Both countries are executing multi-year highway and urban road expansion programmes. India's National Infrastructure Pipeline and China's ongoing transport corridors are generating sustained, large-volume asphalt procurement contracts throughout the forecast period.

Beyond roadways, roofing represents a structurally important application segment for asphalt, covering waterproofing membranes, prepared roofing products, and asphalt pitches. Residential and commercial construction growth in North America and the Middle East supports consistent roofing asphalt demand, reducing market revenue dependence on public-sector road programmes.

Environmental compliance pressure is pushing asphalt producers toward bio-based binders and additive reformulations that reduce fossil-derived bitumen dependency. Early-stage trials at airports and industrial facilities are validating durability credentials, and the long-term shift toward low-carbon asphalt aligns with global net-zero commitments within the global asphalt market growth trajectory.

The report by Expert Market Research's titled "Global Asphalt Market Report and Forecast 2026-2035", offers a detailed analysis of the market based on the following segments:

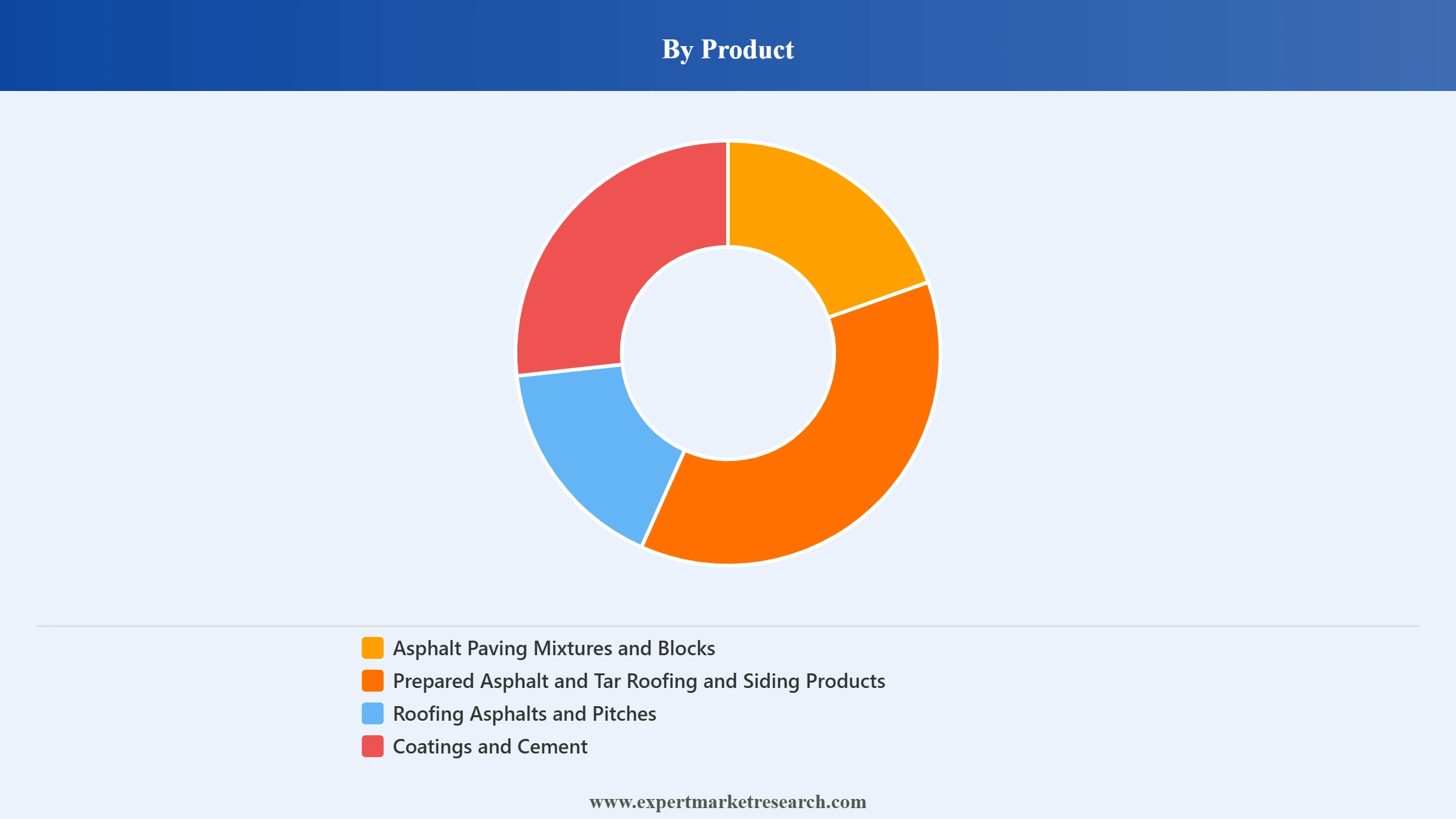

Market Breakup by Product

Key Insight: Asphalt paving mixtures and blocks dominate the global asphalt market by value and volume, driven by road construction representing approximately 70% of paved surface applications worldwide. Prepared roofing and siding products provide an important secondary revenue stream, particularly in North America where residential re-roofing cycles generate consistent annual demand. Roofing asphalts, pitches, and coatings serve both new construction and weatherproofing maintenance, offering a demand base insulated from road budget fluctuations.

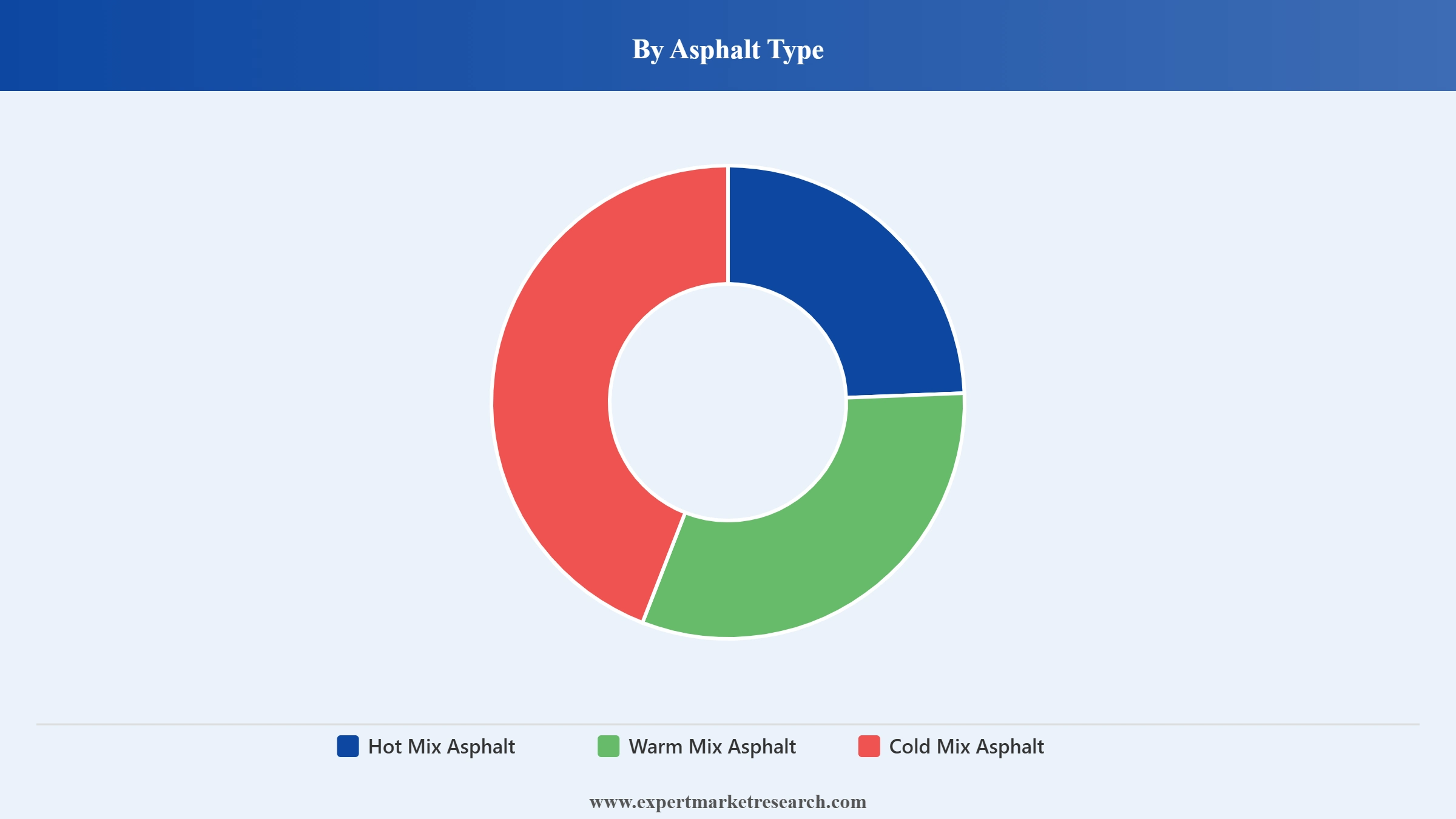

Market Breakup by Asphalt Type

Key Insight: Hot mix asphalt dominates by production volume, offering superior durability and compaction strength for high-traffic highway and urban road applications. Warm mix asphalt is the fastest-growing type, produced at lower temperatures reducing energy consumption and emissions while maintaining performance parity with hot mix in most pavement specifications. Cold mix asphalt fills a niche for remote-location repairs, temporary patching, and applications where heating infrastructure is unavailable.

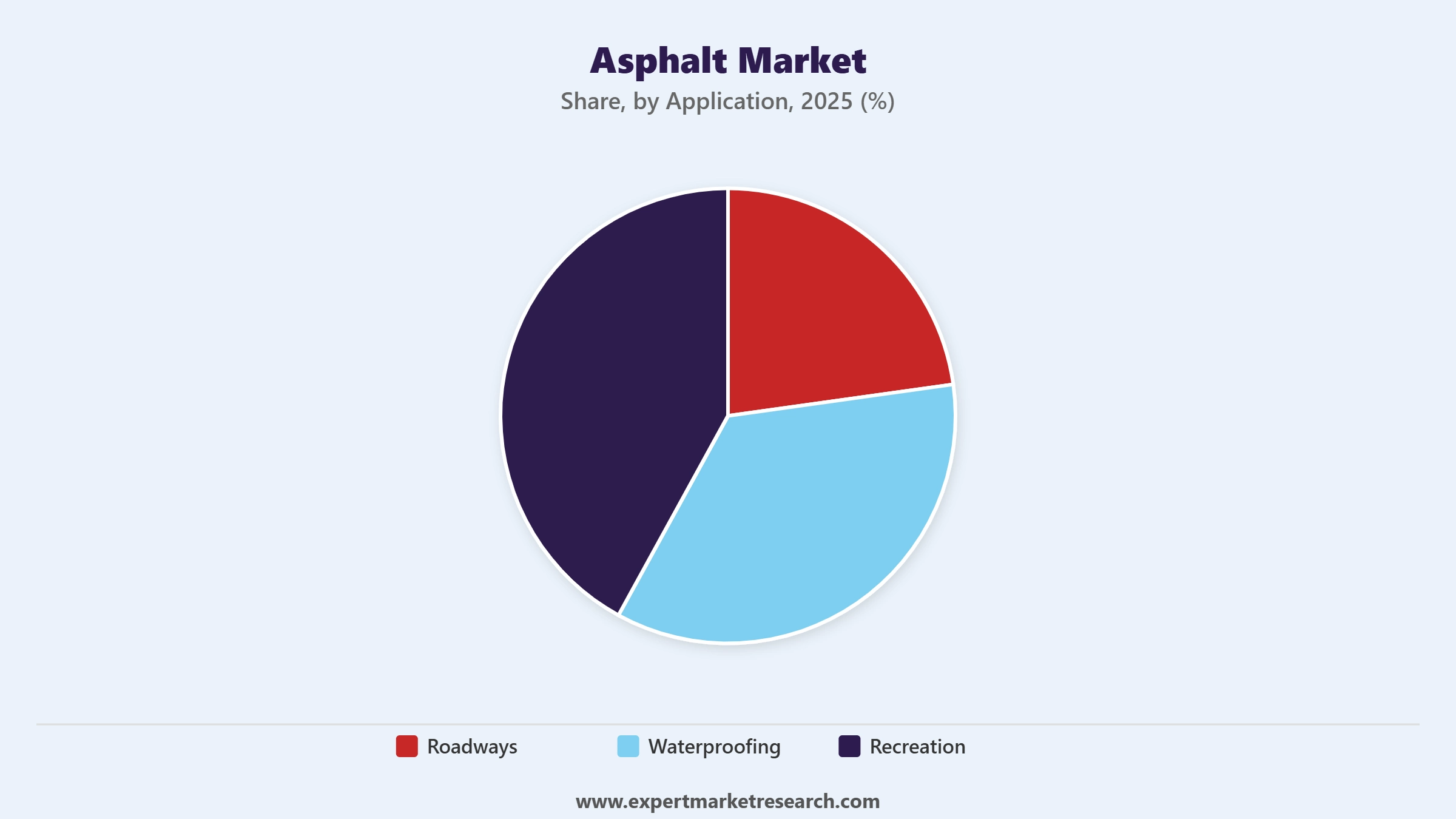

Market Breakup by Application

Key Insight: Roadways account for the dominant share of global asphalt consumption, encompassing highway construction, urban road resurfacing, airport runways, parking facilities, and bridge deck overlays. Waterproofing is a growing secondary application, with asphalt membranes widely used in tunnels, basements, and roofing structures. Recreation, including sports surfaces, cycling tracks, and walking paths, is a niche but growing segment supported by municipal investment in public amenities across urbanising regions.

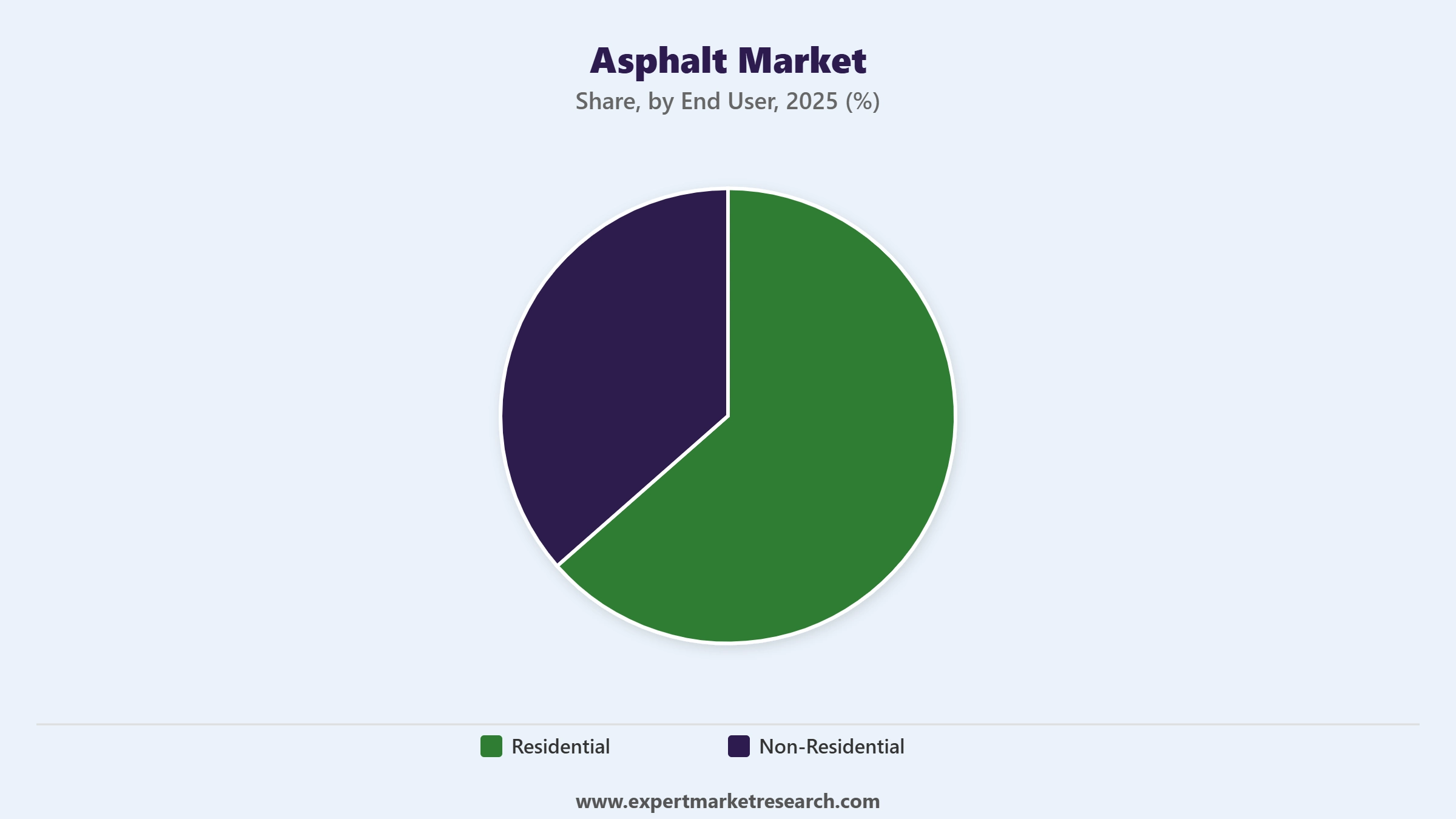

MarketBreakup by End User

Key Insight: Non-residential end users including government road agencies, municipalities, airport authorities, and industrial park developers account for the dominant share of the global asphalt market, driven by public procurement of road construction and rehabilitation projects. Residential asphalt demand, primarily for driveways, private roads, and car parks, provides a stable supplementary revenue stream that correlates with housing construction cycles and renovation activity.

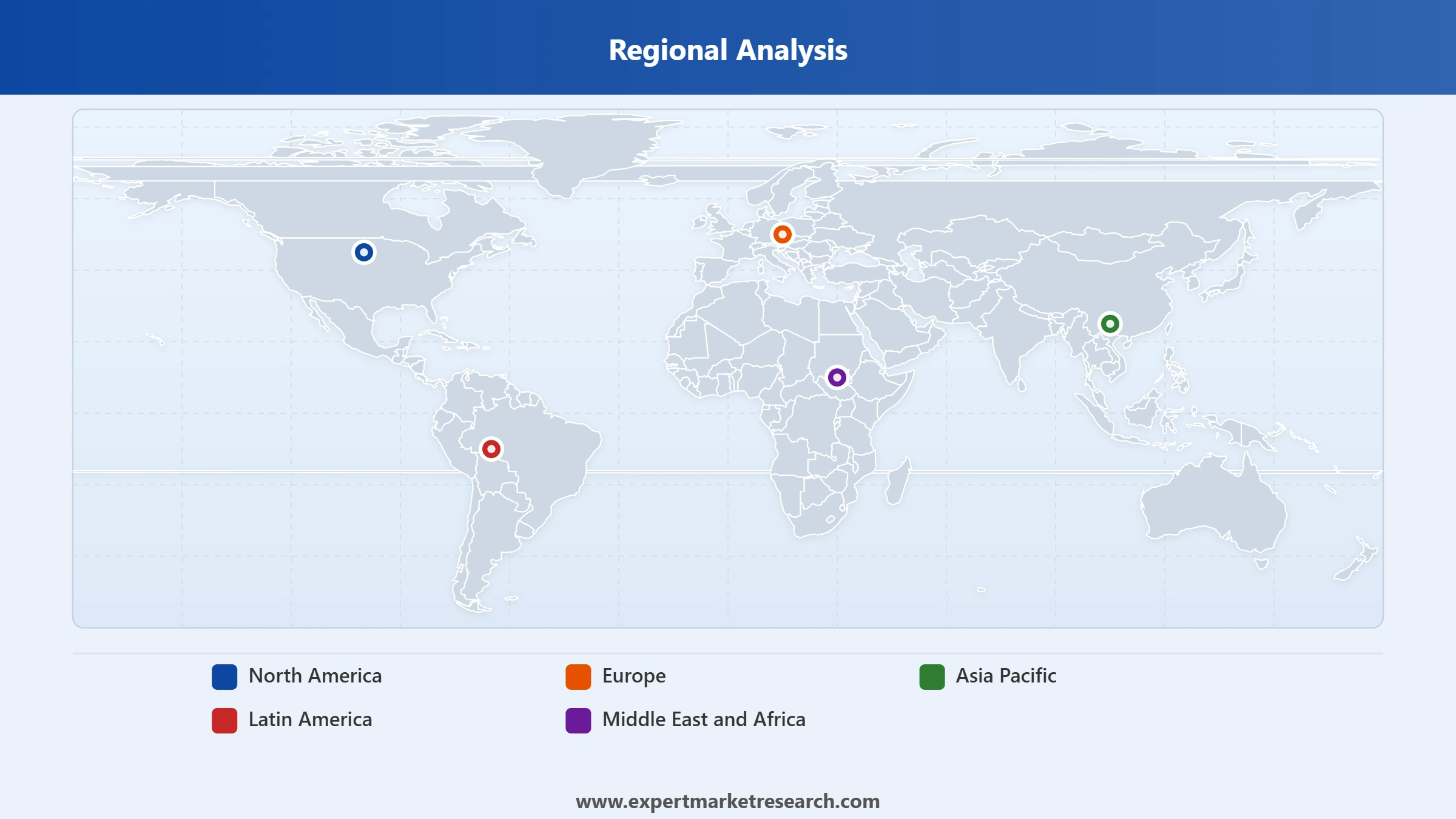

Market Breakup by Region

Key Insight: Asia Pacific holds the largest regional market share, accounting for approximately 39% of global asphalt revenues in 2024, driven by China and India's infrastructure build-out and Southeast Asia's urbanisation. North America is a mature but active market, supported by the US Bipartisan Infrastructure Law allocating significant federal funding for highway rehabilitation. The Middle East and Africa is a fast-growing region, backed by Gulf Cooperation Council megaproject spending and Sub-Saharan road network expansion programmes.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By product, asphalt paving mixtures and blocks dominate the market due to roadways' commanding share of global asphalt consumption

Asphalt paving mixtures and blocks lead the global asphalt market as roadways account for approximately 70% of all paved surfaces worldwide. Highway construction, urban resurfacing, and airport runways generate consistent large-volume procurement contracts, anchoring the product segment's dominant position. Government infrastructure spending in both developed and emerging economies maintains a predictable demand floor that sustains output volumes through economic cycles.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Prepared roofing and siding products form the second-largest product segment, with the North American re-roofing cycle generating recurring annual volumes independent of road budget cycles. In October 2025, Construction Partners reported a record backlog of USD 3.0 billion, confirming strong forward demand in the US paving and construction market. Roofing asphalt demand correlates with housing and commercial real estate activity, providing a counter-cyclical revenue buffer for producers.

By asphalt type, hot mix asphalt accounts for the dominant share of the market due to superior durability and universal applicability in road paving

Hot mix asphalt dominates the global asphalt market because it delivers the compaction strength and surface durability required for high-traffic roads, airport runways, and major urban arteries. Produced at temperatures between 150 and 190 degrees Celsius, it achieves dense, waterproof surfaces that extend pavement life and withstand heavy axle loads. Its decades-long track record in highway engineering makes it the default specification for public procurement in most jurisdictions.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Warm mix asphalt is the fastest-growing type, increasingly specified for lower production temperatures that reduce energy use, binder oxidation, and carbon emissions. European sustainability regulations and US state-level environmental standards are driving specification changes in favour of warm mix on eligible projects. As formulation technology matures and performance data accumulates, warm mix's cost-per-kilometre competitiveness with hot mix in the asphalt market is expected to improve further.

By application, roadways account for the dominant share of the market due to road infrastructure's central role in economic connectivity

Roadways represent the primary and dominant application in the global asphalt market, underpinned by national and subnational road network maintenance requirements that generate recurring annual paving demand. Highway expansion in India under the National Infrastructure Pipeline, urban road rehabilitation in China, and FHWA-funded programmes in the United States ensure road applications maintain their commanding share throughout the forecast period.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Waterproofing is the fastest-growing application, driven by expanding tunnel construction, below-grade infrastructure, and flat-roof commercial building activities across Asia and the Middle East. Recreation surfaces including cycling paths, athletics tracks, and multi-use courts are growing with municipal investment in public infrastructure, providing diversification from road programme budget cycles that can slow hot-mix demand in years of fiscal constraint.

By end user, non-residential accounts for the dominant share of the market due to government road agency and infrastructure procurement driving the majority of asphalt volume

Non-residential end users led by government road agencies, municipalities, and airport authorities command the dominant share of the global asphalt market. Publicly funded projects, including state and national highway construction and urban resurfacing programmes, provide the majority of volume demand. In February 2026, Construction Partners Inc. reported its twelfth hot-mix plant in the Houston metro area through the GMJ acquisition, reflecting how infrastructure investment cycles generate sustained non-residential asphalt demand.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Residential asphalt demand for driveways, private access roads, and car parks delivers consistent supplementary volumes tied to housing construction and renovation activity. In high-growth markets like the Sunbelt in the United States, suburban residential development supports ongoing private paving contracts. The residential segment's lower order values but high frequency of projects makes it a stable revenue base that complements the large-scale public contracts that dominate non-residential asphalt procurement.

Asia Pacific dominates the market due to large-scale infrastructure build-out, rapid urbanisation, and government road investment programmes

Asia Pacific leads the global asphalt market, holding approximately 39% of total revenues in 2024, underpinned by China's Belt and Road-related infrastructure expansion, India's National Infrastructure Pipeline targeting thousands of kilometres of new highway, and Southeast Asia's urban road construction boom. The region's combination of high population density, expanding logistics networks, and government capital expenditure on transport infrastructure creates a structurally elevated and sustained asphalt demand base that outpaces all other regions.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

North America is the most active developed-market region, supported by the US Bipartisan Infrastructure Law directing significant federal investment toward highway rehabilitation and bridge replacement. In February 2026, Construction Partners completed its twelfth hot-mix plant acquisition in the Houston metro area, reflecting strong contractor expansion activity in the US asphalt market. Canada's ongoing Trans-Canada Highway maintenance and provincial road resurfacing budgets add further volume to the region's stable and long-term asphalt demand pipeline.

The global asphalt market is moderately consolidated, combining major oil and gas companies that produce bitumen as a refining by-product with specialist aggregate and paving contractors that manufacture and apply asphalt across end-use segments. Large energy companies such as BP, ExxonMobil, and Chevron supply bitumen to construction and roofing manufacturers, while integrated civil contractors compete on project execution capability and regional plant networks.

Competitive dynamics are shaped by raw material cost management, plant proximity to project sites, technical expertise in mix design, and the ability to scale with government contract awards. Sustainability differentiation is emerging as a competitive factor, with producers investing in recycled asphalt pavement capabilities, warm-mix technologies, and bio-based binder development to meet evolving regulatory requirements and client ESG specifications.

Headquartered in Swindon, United Kingdom, and part of the LafargeHolcim group, Aggregate Industries is a leading supplier of aggregates, asphalt, ready-mixed concrete, and precast products across the UK and continental Europe. Its vertically integrated operations spanning quarry to paving site give it a cost and logistics advantage in UK road and infrastructure markets.

Founded in 1909 and headquartered in London, BP is a global integrated energy company and one of the world's largest bitumen producers. BP's bitumen operations supply road construction and roofing markets across Europe, Asia, and the Americas, leveraging its refinery network to provide consistent quality bitumen as a core by-product of crude oil refining operations.

Founded in 1906 and headquartered in San Pedro Garza Garcia, Mexico, Cemex is a global building materials company operating cement, aggregates, ready-mix concrete, and asphalt businesses across over 50 countries. Its asphalt segment benefits from vertical integration with aggregate quarries and a strong presence in key construction markets across Latin America, the United States, and Europe.

Founded in 1999 through the merger of Exxon and Mobil and headquartered in Spring, Texas, ExxonMobil is one of the world's largest publicly traded oil and gas companies. Its refining operations produce bitumen as a downstream product, supplying paving and roofing asphalt markets globally. ExxonMobil's scale, technical R&D capabilities, and global distribution network underpin its position in the global asphalt market.

Other key players in the market are Anglo American Plc, Atlas Roofing Corporation, Chevron Corporation, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Access comprehensive intelligence on the global asphalt market with our latest research report. Discover how road infrastructure investment cycles, warm-mix and recycled asphalt adoption, and Asia Pacific urbanisation are reshaping demand dynamics across all major regions and product types. Whether you operate in bitumen refining, aggregate supply, road construction, or roofing manufacturing, this report equips you with the data to act strategically. Download your free sample today and explore the key growth opportunities in the asphalt industry.

United States Asphalt Shingle Market

Philippines Asphalt Market

Asphalt Additives Market

Brazil Asphalt Market

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

The market is projected to grow at a CAGR of 5.30% between 2026 and 2035.

The major drivers of the market include the rising uses of asphalt in roadways and pavements and the increasing adoption of emulsified asphalt along with polymer-modified asphalt.

Increasing construction activities and growing emphasis on infrastructure development are the key trends propelling the market growth.

The major regions in the market are North America, Latin America, the Middle East and Africa, Europe, and the Asia Pacific.

The various products in the market are asphalt paving mixtures and blocks, prepared asphalt and tar roofing and siding products, and roofing asphalts and pitches, coatings and cement.

The different asphalt types are hot mix asphalt, warm mix asphalt, and cold mix asphalt.

The significant applications of asphalt include roadways, waterproofing, and recreation, among others.

The key players in the market are Aggregate Industries Ltd., Anglo American Plc, Atlas Roofing Corporation, BP Plc, Cemex, Chevron Corporation, and Exxon Mobil Corporation, among others.

In 2025, the global asphalt market reached an approximate value of USD 70.70 Billion.

The market is expected to maintain a steady growth rate and attain a valuation of USD 118.50 Billion by 2035.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Product |

|

| Breakup by Asphalt Type |

|

| Breakup by Application |

|

| Breakup by End User |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Trade Data Analysis |

|

| Price Analysis |

|

| Competitive Landscape |

|

| Companies Covered |

|

| Report Price and Purchase Option | Explore our purchase options that are best suited to your resources and industry needs. |

| Delivery Format | Delivered as an attached PDF and Excel through email, with an option of receiving an editable PPT, according to the purchase option. |

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.