Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

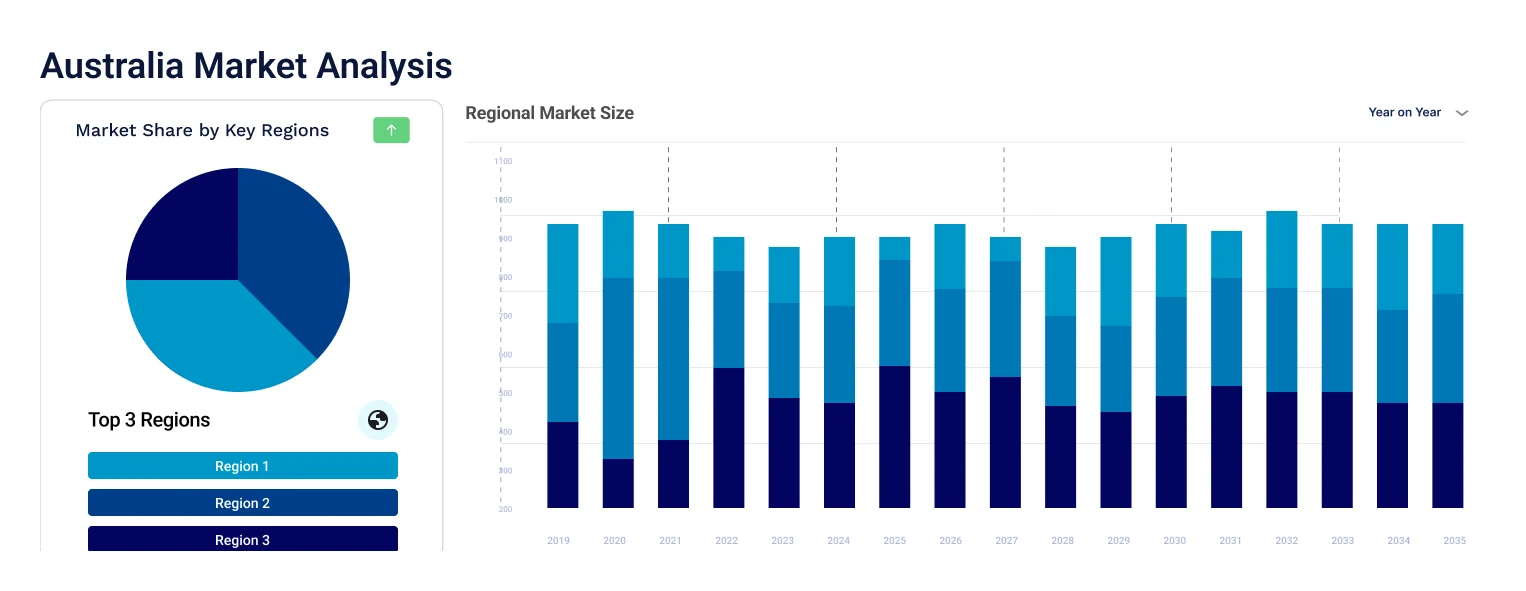

The Australia data center market attained a value of USD 6.77 Billion in 2025 and is projected to expand at a CAGR of 6.30% through 2035. The market is further expected to achieve USD 12.47 Billion by 2035. Rising government digital service mandates and defense cloud adoption are driving sustained demand for sovereign, high-security data centers. They are also creating long-term contracts for operators with accredited facilities and energy-resilient designs across the nation.

AI-driven workloads and hyperscale cloud demand now collide with power, land, and grid constraints around major enterprise hubs. As a response, in November 2025, NEXTDC announced its membership of Data Centres Australia (DCA), the new peak body established to unite and advance the country’s rapidly expanding data center and AI infrastructure sector. This development signals how hyperscale operators are competing to secure capacity near Sydney’s latency-sensitive enterprise clusters while managing energy availability and grid constraints nationally, accelerating the Australia data center market value.

Colocation providers are shifting their focus toward modular expansion and customer-specific power blocks. Players like NEXTDC and CDC Data Centers are investing in edge-adjacent facilities to support industries, government workloads, and defense contracts. Enterprises also demand sovereign data residency, pushing operators to emphasize compliance, security accreditation, and local ownership structures, redefining the Australia data center market trends and dynamics. In June 2025, Schneider Electric introduced new data center infrastructure specifically designed for next-generation artificial intelligence cluster architectures, for extreme rack power densities projected to reach 1 megawatt and beyond.

Compound Annual Growth Rate

6.3%

Value in USD Billion

2026-2035

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Australia saw the formal introduction of Data Centres Australia (DCA), the new leading organization uniting industry figures to advocate for innovation, resilience, and sustainable progress. The formation of DCA strengthens policy advocacy and sustainability coordination, improving regulatory clarity and investment confidence for hyperscale and sovereign data center developers across Australia.

Datadog, Inc. introduced its complete array of products and services in the Asia-Pacific (Sydney) Region of Amazon Web Services (AWS). Datadog’s expanded presence increases demand for high-performance, low-latency data centers supporting observability, security, and cloud-native workloads within Australia.

Nokia revealed it has been chosen by ResetData to deliver a networking infrastructure that facilitates its prompt deployment of sovereign ‘AI Factory’ data centers. This Australia data center market development highlights rising demand for AI-ready, sovereign data centers requiring advanced networking, edge integration, and rapid deployment capabilities nationwide.

HubSpot revealed the opening of its inaugural data center in Australia, showcasing its dedication to investing in the area for the long term. HubSpot’s local data center launch reinforces Australia’s position for global SaaS firms seeking data residency compliance and closer proximity to Asia-Pacific customers.

Hyperscale data center expansions are reshaping the Australian market. AirTrunk’s SYD1 AI-ready hall and similar builds reflect demand for high-density computing to support AI, machine learning, and analytics workloads. These facilities often exceed 100 kW per rack, requiring advanced cooling and power management. Enterprises and cloud providers are investing heavily in local capacity to reduce latency and meet sovereign data needs, reshaping the Australia data center market trends. In December 2025, NEXTDC Limited confirmed that it has agreed a Memorandum of Understanding with OpenAI, enabling Australia to become a regional infrastructure partner under the Open AI for Countries program. Operators with liquid cooling and AI-optimized infrastructure are winning pre-leases and customer commitments earlier in the project lifecycle than traditional colocation models.

Sovereign data requirements have become a major trend in the market as federal and state government agencies require onshore data residency for sensitive workloads, particularly in defense, finance, and healthcare sectors. Operators like NEXTDC, Equinix, and CDC Data Centres are expanding facilities with certified security, privacy, and compliance accreditations to capture this demand in the Australia data center market. In October 2025, SouthernCrossAI (SCX.ai) and SambaNova announced the launch of Australia’s first ASIC‑based sovereign AI cloud, a breakthrough platform engineered to empower regional governments and enterprises with secure, onshore AI infrastructure. These expansions tie directly to government digital transformation initiatives and protective data legislation that limit cross-border data transfer.

Major operators are signing renewable power purchase agreements and investing in on-site solar and battery storage to reduce carbon impact. Australian energy policy encourages renewable uptake through incentives and grid access priority, which influences site selection and operating cost structures. In December 2025, the 600MW/1.6GWh Melbourne Renewable Energy Hub commenced commercial operations in Victoria, Australia. The battery energy storage system (BESS) project has been jointly developed by Singapore-based Equis’s Australian subsidiary and the Victorian government’s State Electricity Commission (SEC). Firms are publishing net zero roadmaps and collaborating with utilities to manage peak demand, supporting the overall Australia data center market dynamics. Innovative approaches like waste heat reuse pilot projects and modular cooling systems are emerging.

Edge and regional data center growth is gaining major momentum as they support latency-sensitive applications, IoT deployments, and distributed enterprise needs. Operators are building micro-data centers near major regional hubs to serve mining, manufacturing, and logistics sectors requiring real-time processing. The Australian government’s regional digital infrastructure plans and investment incentives support this decentralization. In December 2025, Myriota launched HyperPulse, a commercial 5G Non-Terrestrial Network (NTN) offering global connectivity for Internet of Things (IoT) devices in areas far beyond traditional mobile coverage. Edge facilities reduce backhaul costs and improve performance for remote users, accelerating the Australia data center market value.

Modular design and scalability are emerging strategic trends in the market. Operators now favor phased, prefabricated builds that reduce capital intensity and construction risk while matching demand growth. Companies like NEXTDC and AirTrunk are adopting modular data halls and standardized pods to accelerate delivery and improve utilization. Modular approaches also allow easier integration of new cooling technologies and power upgrades without disrupting live operations. In April 2025, Australian data center firm DXN signed a deal to provide a ground station company with prefabricated data center modules. This Australia data center market trend aligns with enterprise demand for predictable deployment schedules and capacity flexibility.

The EMR’s report titled “Australia Data Center Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

Market Breakup by Component

Key Insight: Component demand in the Australia data center market is shaped by operational certainty and lifecycle efficiency. Solution components dominate because operators prefer integrated power, cooling, and monitoring stacks that reduce deployment risk and commissioning delays. These solutions support standardized expansion and predictable performance. Services are expanding their shares quickly as facilities become denser and more complex. Operators rely on managed maintenance, energy optimization, compliance audits, and remote monitoring to control costs and uptime.

Market Breakup by Enterprise Size

Key Insight: Large enterprises presently anchor majority of the data center demand in Australia due to scale, compliance exposure, and continuous capacity needs. They secure long-term contracts and drive investments in redundancy, security, and sustainability. Small and medium enterprises are growing at a comparatively faster pace as digital transformation accelerates. SMEs seek scalable access to enterprise-grade infrastructure without capital burden. Operators respond with flexible capacity blocks and bundled services.

Market Breakup by Type

Key Insight: Colocation dominates the market by a high margin because it offers flexibility, interconnection, and control for hybrid IT environments. Enterprises favor colocation to balance cloud scalability with physical oversight and compliance, driving the overall growth of the Australia data center market. Hyperscale is growing fast as AI, analytics, and cloud platforms expand rapidly. These facilities require high-density power and specialized cooling.

Market Breakup by End Use

Key Insight: IT and telecommunications dominate through scale, connectivity needs, and continuous infrastructure upgrades. These users drive early adoption of advanced cooling, automation, and interconnection density. Government demand is also expanding rapidly due to sovereign data mandates and digital public services. Public sector workloads prioritize security, availability, and certified facilities, broadening the Australia data center market scope. BFSI, media, energy, and other sectors add demand diversity with varying sensitivity to latency and regulation.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Solution components largely drive the market growth due to integrated infrastructure and energy optimization

Solution offerings dominate the data center market in Australia as operators prioritize integrated infrastructure stacks over standalone services. Solutions include power systems, cooling architecture, racks, monitoring software, and security frameworks delivered as unified platforms. In May 2024, OVHcloud announced the launch of its third data center in Sydney, powered by its latest water-cooling technology. Hyperscale and colocation operators prefer turnkey solutions that shorten build timelines and reduce operational risk.

Services emerge to be the fastest-growing component as data centers shift toward managed operations and lifecycle support. Operators increasingly outsource maintenance, energy optimization, remote monitoring, and compliance audits to specialist providers. The service category’s growth in the Australia data center market dynamics is driven by complexity introduced by AI workloads, liquid cooling, and hybrid energy systems. Enterprises leasing colocation space also demand managed services to reduce internal IT burden.

By enterprise size, large enterprises account for the largest share of the market revenue due to scale and compliance requirements

Large enterprises anchor majority of the demand in the Australia data center market due to scale, regulatory exposure, and continuous workload growth. Banks, cloud providers, telecom firms, and government contractors require large footprints, redundant power, and strict compliance. These enterprises favor long-term colocation and hyperscale contracts that guarantee capacity and pricing stability. They influence facility design by demanding higher densities, enhanced security, and sovereign data controls.

SMEs experience fast-paced growth in the Australia data center market as digital transformation accelerates further. Many SMEs migrate from on-premise infrastructure to colocation and managed data center services. They seek cost predictability, scalability, and access to enterprise-grade infrastructure without heavy capital investment. In November 2022, DigitalOcean Holdings, Inc. the cloud for developers, startups and SMBs, announced it is expanding its global presence with a new data center in Sydney, Australia (SYD1). Cloud adoption, e-commerce growth, and remote operations push SMEs toward outsourced facilities.

By type, the colocation category dominates the market due to flexibility and enterprise hybrid strategies

Colocation secures a substantial share of the Australia data center market revenue due to flexibility and hybrid IT strategies. Enterprises use colocation to combine cloud scalability with physical control over infrastructure. Operators offer carrier-dense facilities, scalable power blocks, and strong interconnection ecosystems. In May 2025, ASX announced the launch of ASX Colo OnDemand, a new infrastructure service that gives customers access to scalable and secure infrastructure. Colocation supports compliance, latency management, and disaster recovery.

Hyperscale is the fastest-growing type as cloud, and AI workloads surge rapidly. Global cloud providers and large enterprises demand massive, high-density campuses. Operators design hyperscale facilities with liquid cooling readiness and dedicated power infrastructure. Growth is driven by AI training, data analytics, and SaaS expansion.

By end use, IT and telecom account for the dominant share of the market driven by cloud and connectivity growth

IT and telecommunications dominate end-use demand as cloud platforms, networks, and digital services expand. Telecom operators deploy core and edge infrastructure inside data centers. Cloud providers scale rapidly to support enterprise workloads. These users demand high connectivity, redundancy, and interconnection density. Operators design facilities around carrier neutrality and network performance. IT and telecom clients sign long-term contracts and drive early adoption of advanced cooling and automation. Their demand shapes facility design standards across the Australia data center market.

Government is the fastest-growing end-use category due to digital public services and data sovereignty mandates. Federal and state agencies migrate workloads to accredited local data centers. In this category, demand focuses on security, compliance, and availability as oerators expand facilities certified for government use. Long procurement cycles result in stable contracts.

Leading Australia data center market players are focusing on high-density campuses, liquid cooling readiness, and long-term power procurement to secure pre-commitments. Opportunities are strongest around government cloud, regulated industries, and enterprise hybrid deployments requiring local data residency. Operators are also differentiating through faster build cycles, modular halls, and energy-efficient designs to manage grid constraints. Sustainability credentials and renewable sourcing have emerged to be commercial necessities. International investors remain active, supporting capacity expansion despite power accessibilty challenges.

Australia data center companies that secure land, grid approvals, and anchor tenants early gain advantage. The market rewards disciplined phasing, deep enterprise relationships, and operational transparency. Execution speed and energy strategy now define competitive positioning more than the company’s footprint in the market. This shift is reshaping procurement timelines and investment screening across Australia for local and foreign developers.

AirTrunk Operating Pty Ltd., established in 2015 and headquartered in Sydney, Australia, specializes in hyperscale data center campuses supporting cloud and AI workloads. AirTrunk focuses on high-density design, liquid cooling readiness, and long-term renewable power agreements. Its developments target large anchor tenants seeking rapid capacity delivery.

Founded in the year 2010 and headquartered in Brisbane, Australia, Nextdc Ltd. operates a national network of carrier-neutral colocation data centers. The company targets enterprises, cloud providers, and government agencies requiring sovereign data control. It invests in modular expansion, interconnection density, and compliance certifications.

CDC Data Centres Pty Ltd. was established in 2007 and is headquartered in Canberra, Australia. The company focuses on secure, sovereign data centers serving government and critical infrastructure clients. CDC emphasizes high-security design, compliance accreditation, and resilient power architecture. Its facilities support defense, intelligence, and regulated workloads.

Fujitsu Ltd. was founded in 1935 and is headquartered in Tokyo, Japan. In Australia, Fujitsu operates data centers supporting enterprise IT, cloud, and government workloads. The company integrates data center services with managed IT, cybersecurity, and systems integration. Fujitsu focuses on hybrid cloud, sovereign data solutions, and modernization projects by combining infrastructure with services.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Other key players in the market include Equinix Inc., Global Switch Holdings Limited, Digital Realty Trust Inc., Leaseweb Global B.V., Telstra Corporation Limited, and Macquarie Technology Group Limited, among others.

Unlock the latest insights with our Australia data center market trends 2026 report. Discover regional growth patterns, consumer preferences, and key industry players. Stay ahead of competition with trusted data and expert analysis. Download your free sample report today and drive informed decisions in the market.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market reached an approximate value of USD 6.77 Billion.

The market is projected to grow at a CAGR of 6.30% between 2026 and 2035.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach a value of around USD 12.47 Billion by 2035.

Key strategies driving the market include securing power agreements, phasing developments, investing in liquid cooling, targeting government workloads, pre-leasing capacity, strengthening grid partnerships, and prioritizing sustainability reporting to attract hyperscale and enterprise customers nationally.

The key trends aiding the market expansion include increase in web-enabled services, technological advancements and innovations, and introduction of sustainable practices in data centers.

The major components of data centers are solution and service.

The different types of data center are colocation, hyperscale, and edge among others.

The key players in the market include AirTrunk Operating Pty Ltd., NEXTDC Ltd., CDC Data Centres Pty Ltd., Fujitsu Ltd., Equinix Inc., Global Switch Holdings Limited, Digital Realty Trust Inc., Leaseweb Global B.V., Telstra Corporation Limited, and Macquarie Technology Group Limited, among others.

Key challenges include limited grid capacity, long approval timelines, rising power costs, construction inflation, land scarcity, and balancing sustainability targets with hyperscale demand while securing anchor tenants early nationwide consistently.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Component |

|

| Breakup by Enterprise Size |

|

| Breakup by Type |

|

| Breakup by End Use |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.