Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

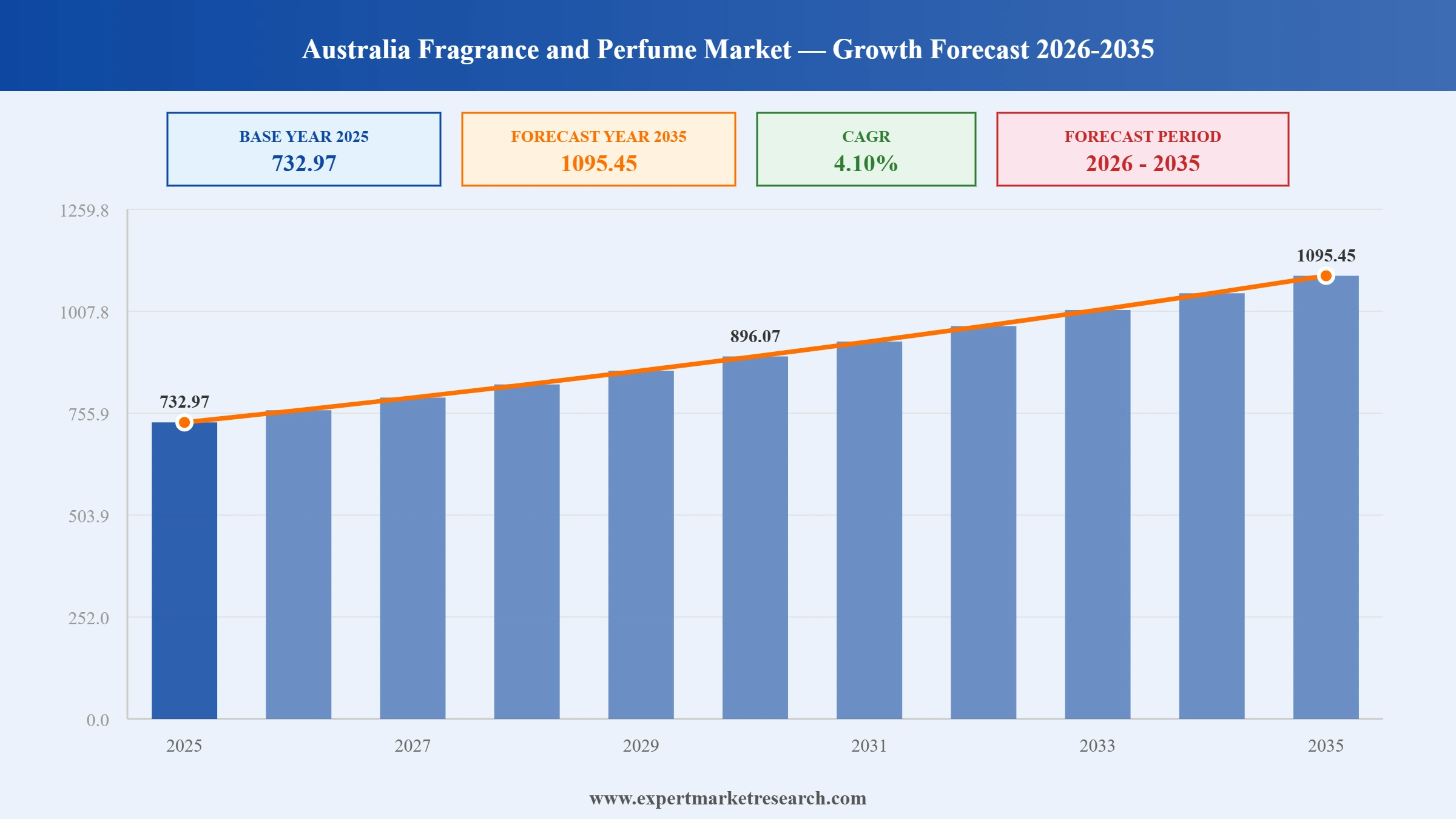

The Australia fragrance and perfume market attained a value of USD 732.97 Million in 2025 and is projected to expand at a CAGR of 4.10% through 2035. The market is further expected to achieve USD 1095.45 Million by 2035. Premium refillable fragrance formats are helping brands retain high-income consumers, improve sustainability credentials, and stabilize margins. Brands are also reducing packaging dependency and encouraging repeat purchases through loyalty-linked refill programs.

Selective retail expansion and tourism recovery are accelerating fragrance demand across Australia. Duty-free retailers at Sydney and Melbourne airports are reporting strong fragrance category rebounds. Meanwhile, influencer-led niche brand launches are shortening product adoption cycles. Companies are investing in limited-batch releases to test demand growth before scaling. This lowers inventory risk and improves capital efficiency, accelerating the overall Australia fragrance and perfume market growth. Such controlled launches also allow brands to negotiate better shelf positioning with specialty retailers, strengthening long-term channel partnerships.

Companies are looking for broader sustainability roadmap while targeting margin protection in high-value segments. In June 2025, L’Oréal expanded its fragrance portfolio by introducing refill-enabled formats across premium department stores. Refillable SKUs are enabling brands to retain loyal customers while increasing lifetime value per user. The strategy also reduces packaging costs over time, which is becoming commercially relevant as glass and aluminum input prices remain volatile.

The Australia fragrance and perfume market dynamics continues to shift toward premium and niche positioning rather than mass-volume growth. Urban consumers are favoring extrait concentrations, limited editions, and artisanal blends. Brands like Mecca Brands and Goldfield & Banks are investing in exclusive launches and controlled distribution to maintain dominance. For example, in May 2025, Goldfield & Banks announced the debut of its Pacific Rock Flower fragrance through an exclusive pop-up collaboration with Heinemann Oceania at Sydney International Airport. This approach allows companies to command higher per-unit pricing while reducing dependency on discount-heavy retail cycles.

Technology-backed retail execution is further shaping competitive strategies. Major players are using AI-driven scent profiling, loyalty data, and online-to-offline integration to refine product assortments. For example, Ninu offers a customizable smart perfume that can be adjusted through a smartphone app. Such developments in the Australia fragrance and perfume market indicate that future growth will rely less on store expansion and more on data-led product planning, selective collaborations, and higher inventory efficiency. Companies that align fragrance innovation with premium storytelling and operational discipline are expected to secure stronger margins across Australia.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Lacoste launched its new Original Pour Femme fragrance, a fruity floral amber scent. Such developments are encouraging competitors to invest in contemporary floral-amber blends that balance mass appeal with premium brand cues in Australian retail.

The Estée Lauder Companies and Jo Malone London launched the Jo Malone London Scent Advisor, a digital tool powered by AI aimed at assisting customers in choosing fragrances. TThus, with AI-driven fragrance discovery, companies can reduce purchase hesitation. They can fund digital scent tools that improve conversion, personalization, and repeat buying across online and offline channels.

Delta Goodrem announced the release of the fragrance line called ‘Within’ in Chemist Warehouse locations across Australia. Using such developments in the Australia fragrance and perfume market, brands can scale volumes quickly by pairing personal storytelling with wide physical distribution, creating opportunities for accessible premium fragrance positioning.

Phlur officially announced its debut in Australia via Mecca, bringing its cult-favorite perfumes like Missing Person and Heavy Cream. Such advancements reflect strong demand for viral and minimalist fragrances, encouraging other companies to fund niche brand partnerships and limited launches through specialty retailers to test demand before broader rollouts.

Sustainability-led product design is reshaping the Australia fragrance and perfume market, particularly in premium consumer segments. Global brands are introducing refillable bottles and reduced packaging formats to protect margins and meet regulatory expectations. Refillable formats encourage repeat purchases while reducing logistics costs, retaining demand in the market. For instance, Beautys, in September 2025, announced its handcrafted Australian-made refillable perfumes and air fresheners, offering cruelty-free, vegan luxury fragrances and home scents made in Tasmania.

Australia is witnessing strong growth of niche and locally developed fragrance brands, supported by premium retail partnerships. Companies such as Goldfield & Banks and Who Is Elijah are focusing on Australian-sourced botanicals and limited-run collections. These products allow higher price realization and tighter inventory control. Local brands are leveraging storytelling around origin and craftsmanship to differentiate from global mass brands. For example, Australian fragrance brand Flâner Fragrances opened its first pop-up store in Fitzroy in August 2023, offering a wide range of domestically sourced botanical ingredients. This trend in the Australia fragrance and perfume market benefits specialty retailers seeking exclusivity, while manufacturers gain flexibility in pricing and faster response to demand changes.

Technology-backed personalization is becoming a core driving factor for fragrance retail strategies across Australia. Major retailers are using loyalty data and AI-led scent profiling to refine product launches. Government-backed digital capability grants under Australia’s Modern Manufacturing Initiative have encouraged investment in data systems. Personalized fragrance discovery reduces return rates and improves conversion. Brands that align product launches with customer data are achieving higher sell-through rates, accelerating the Australia fragrance and perfume market value. Leveraging siuch trends, firms like Unity Scents Pty Ltd are offering a roll-on applicator designed to reduce waste and avoid the discomfort associated with traditional spray perfumes, since February 2025.

The rebound of international travel is directly supporting fragrance sales across Australia’s duty-free and travel retail channels. Airports remain high-margin sales points for premium fragrance brands. Fragrance brands are launching travel-exclusive SKUs and concentrated formats to capture impulsive demand. In August 2024, L'Occitane Group introduced an activation for its body care brand, Sol de Janeiro, at Melbourne Airport's T2 Departures in partnership with Lotte Duty Free. Travel retail allows brands to test new products with global consumers, widening the Australia fragrance and perfume market scope. These channels also help manufacturers move higher volumes without heavy promotional discounting, supporting profitability and inventory efficiency.

Regulatory oversight is influencing formulation, labeling, and sourcing strategies in the Australia market. The Australian Industrial Chemicals Introduction Scheme (AICIS) has tightened reporting requirements for fragrance ingredients. This is pushing companies to reformulate and invest in compliant supply chains. Large-scale players are prioritizing transparent ingredient disclosure and allergen-safe products. Compliance-driven reformulation often leads to premium repositioning and higher pricing. Brands that adapt early gain smoother approvals and faster product launches, reshaping the overall Australia fragrance and perfume market dynamics. Go-To Skincare expanded into fragrance product development, launching its first trio of oil-based, alcohol and allergen-free perfumes ‘Into The Woods’, ‘Into The Garden’, and ‘Into The Bakery’ in October 2025. This regulatory environment favors organized players with strong R&D capabilities, while small-scale brands increasingly partner with certified manufacturers to remain competitive.

The EMR’s report titled “Australia Fragrance and Perfume Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

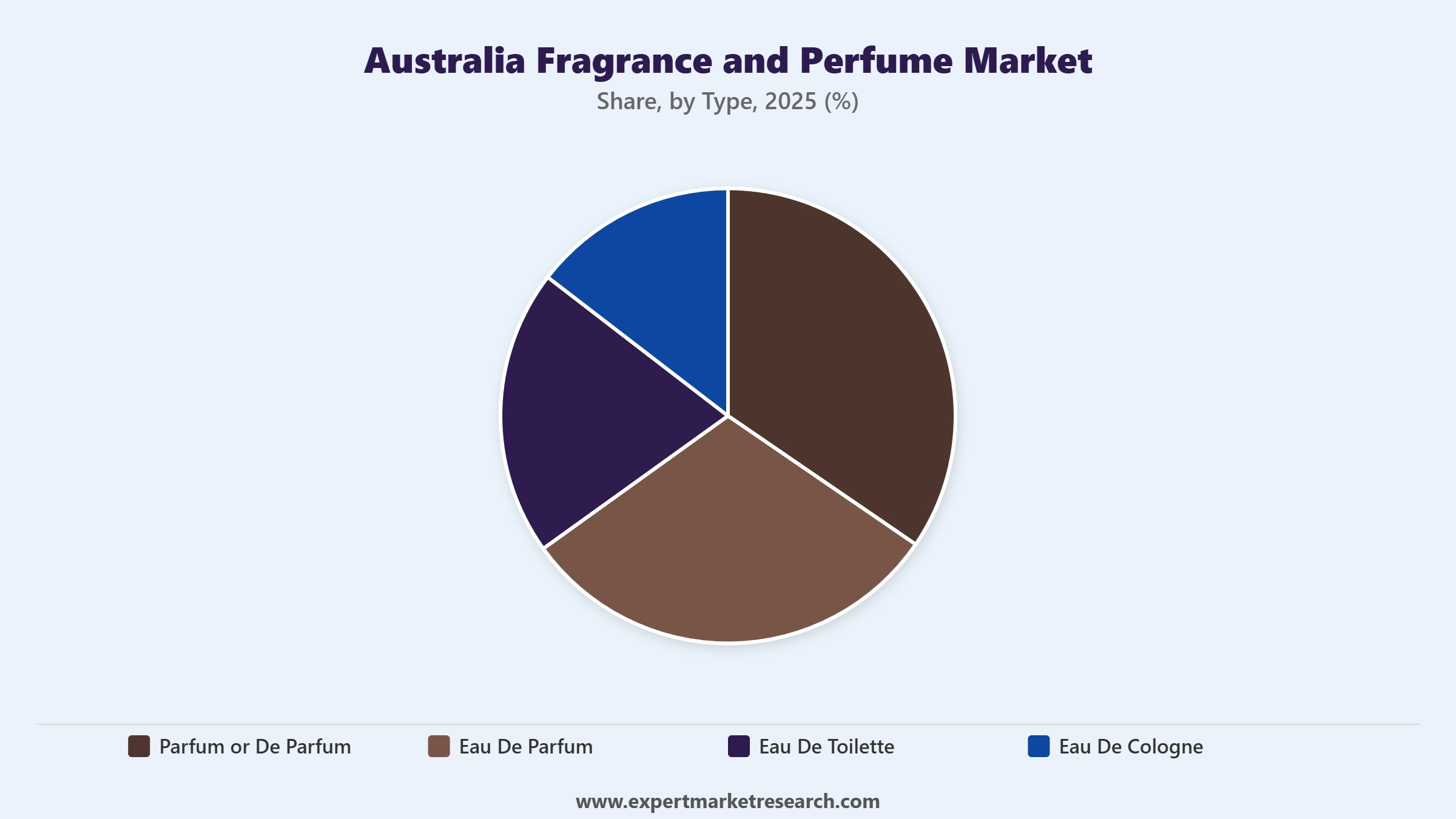

Market Breakup by Type

Key Insight: Eau De Toilette supports freshness-driven and climate-friendly usage, while Eau De Cologne remains niche, focused on simplicity and heritage cues. Eau De Parfum largely accelerates the Australia fragrance and perfume market growth due to balance, familiarity, and broad applicability. Parfum gains strong momentum as premium buyers pursue longevity and exclusivity. In November 2025, Pixi announced the launch of Pixi Perfume, a trio of perfumes made with botanical extracts and mood-enhancing properties. Brands use EDT and EDC to widen entry points, EDP to stabilize volumes, and Parfum to lift margins. This tiered approach helps companies manage pricing ladders, reduce cannibalization, and optimize inventory across channels.

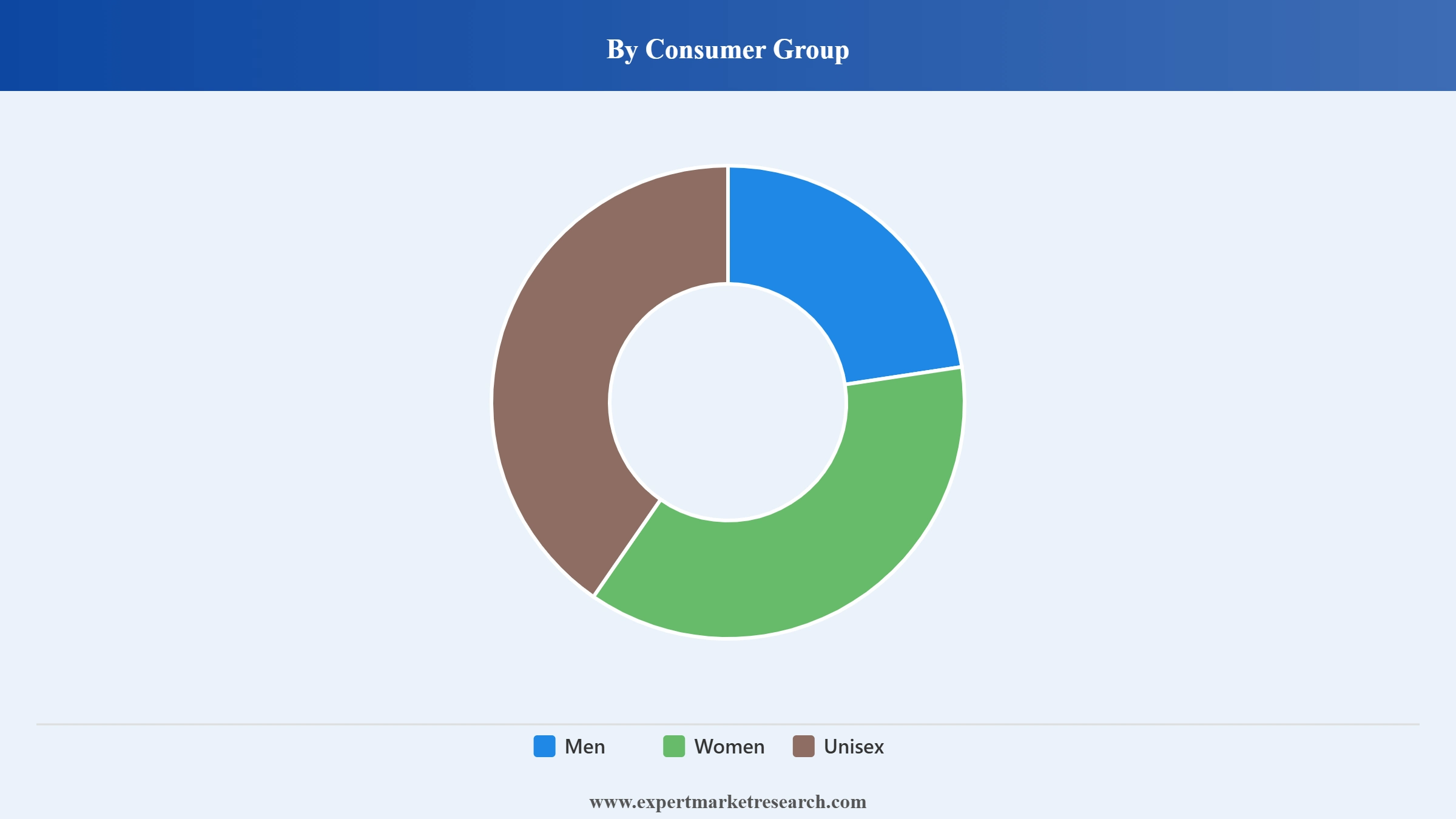

Market Breakup by Consumer Group

Key Insight: Consumer group segmentation as considered in the Australia fragrance and perfume market report highlights usage behavior over identity. Women remain the dominant volume growth contributors due to frequency and gifting-led demand. Men contribute steady value through signature scent loyalty and slower replacement cycles. Unisex fragrances grow at the fastest pace as brands emphasize inclusivity and ingredient storytelling.

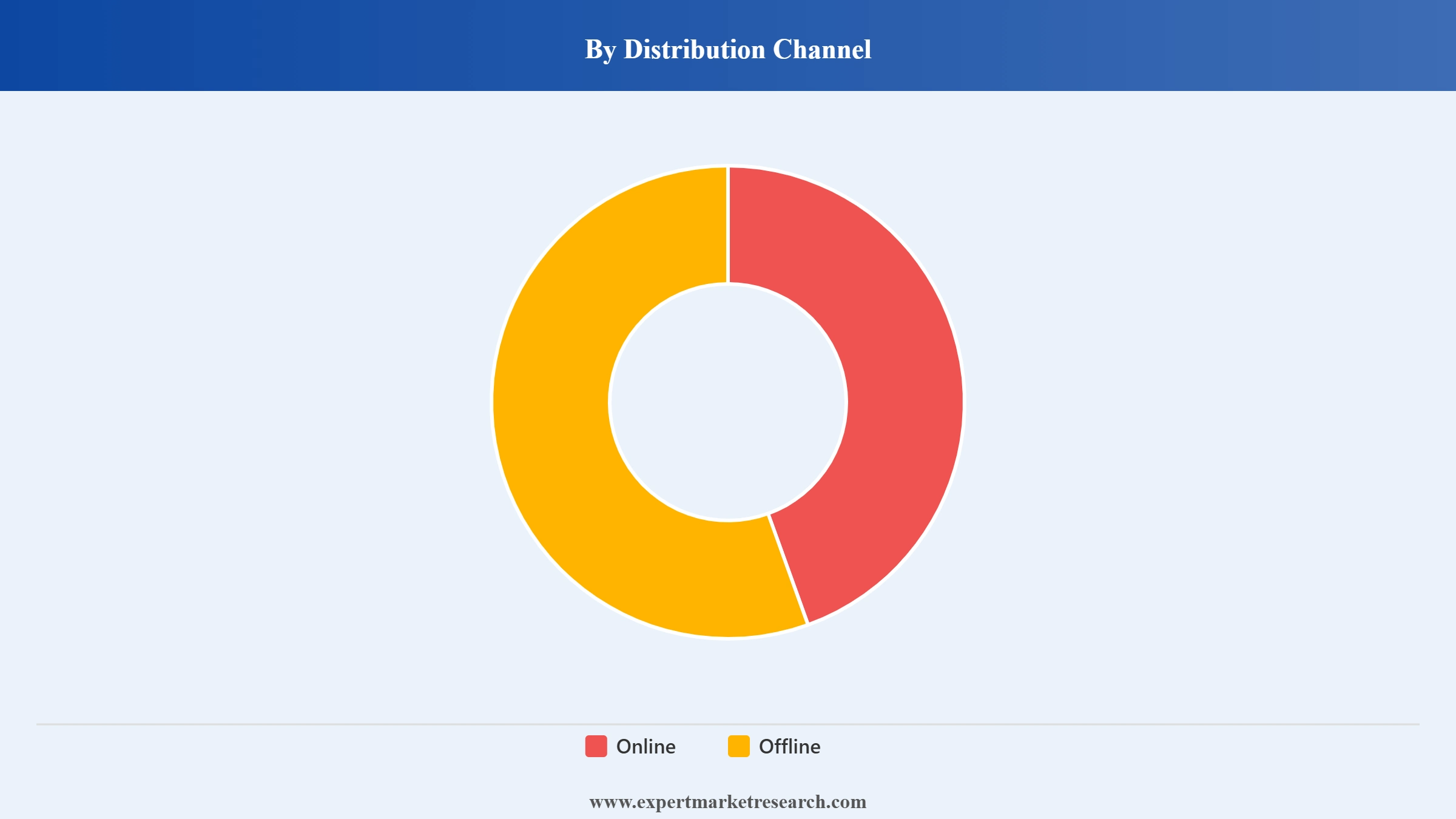

Market Breakup by Distribution Channel

Key Insight: While offline channels dominate discovery, validation, and premium gifting, online channels grow rapidly popular through convenience and repeat replenishment. Brands increasingly integrate both channels to smooth transitions between testing and purchasing. Both channels support stronger customer lifetime value and improved inventory planning. Balanced channel strategies reduce dependency on discounting and improve margin discipline. According to the Australia fragrance and perfume market analysis, the number of fragrance users is expected to amount to 5.5 million by 2030, while the user penetration is expected to hit 19.8% by the forecast period.

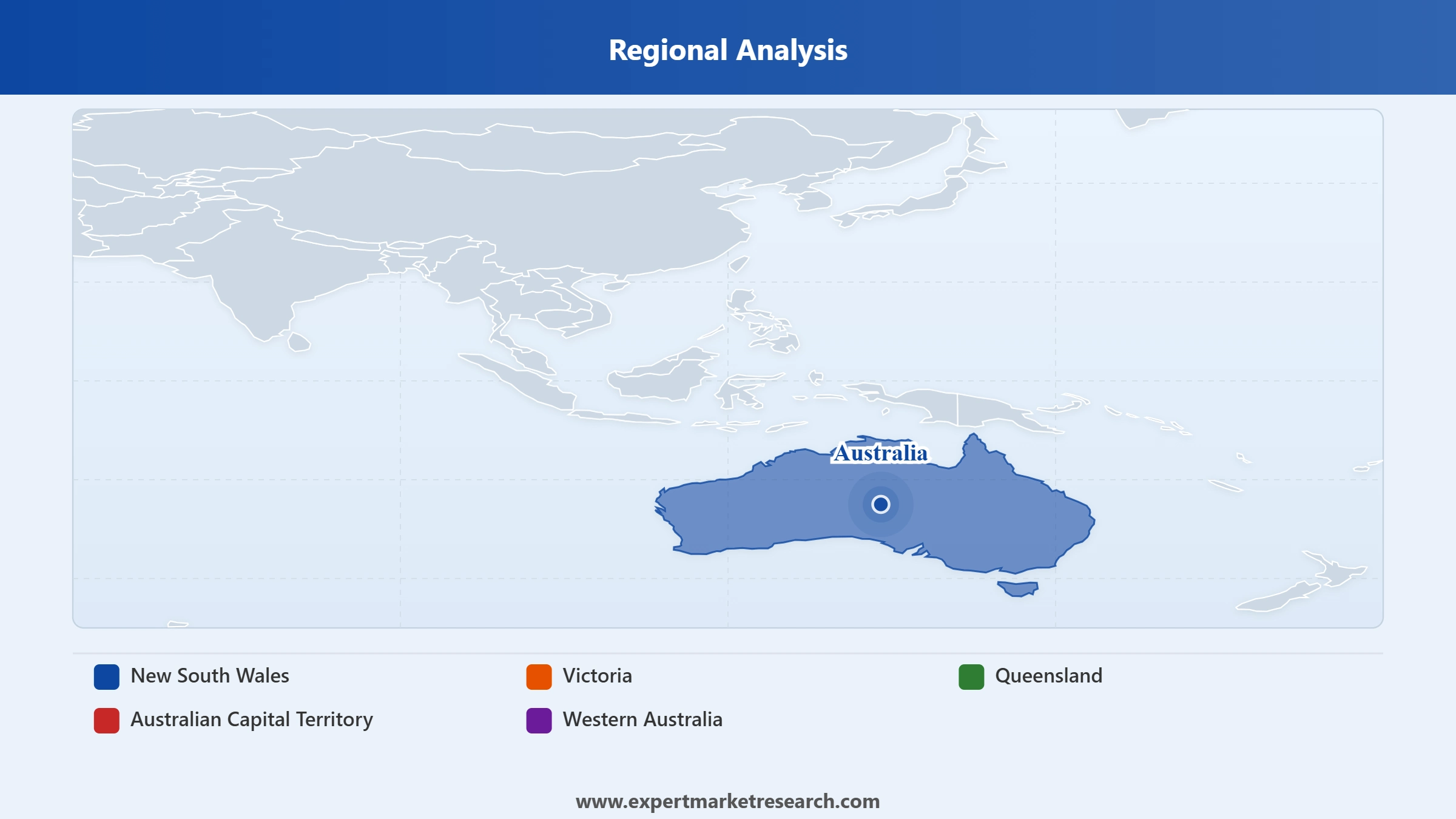

Market Breakup by Region

Key Insight: New South Wales anchors premium demand in the Australia fragrance and perfume market through flagship retail. Victoria supports design-led and niche fragrances. Queensland gains major market shares due to migration and experiential consumption. Western Australia remains selective with premium focus while the Australian Capital Territory offers stable professional demand. Other regions contribute to the market growth through online accessibility. Brands adjust launch sequencing and distribution depth accordingly. Regional strategies now shape cost control, inventory planning, and marketing allocation across Australia.

By type, Eau De Parfum registers the largest share of the market due to balanced longevity, pricing, repeat usage

Eau De Parfum currently holds the dominant share of the fragrance and perfume market in Australia because it aligns best with everyday usage patterns and retail economics. Brands prioritize EDP as it offers noticeable longevity without the intensity or pricing barriers of Parfum. Retailers prefer EDP due to higher replenishment frequency and lower consumer hesitation. Leveraging this category’s continued dominance, Merit Beauty offers Sublime Eau De Parfum as a clean and “responsible luxury” fragrance, since September 2024.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Parfum also registers fast-paced growth in the Australia fragrance and perfume market as consumers increasingly look for premium fragrances. Buyers seeking exclusivity and longevity are shifting away from lighter concentrations. Brands are positioning Parfum as statement products, often released in smaller volumes and limited channels. This supports higher per-unit margins and controlled distribution. Parfum also benefits from gifting demand and private client selling. For companies, it reduces dependency on volume-led growth while strengthening brand equity.

By consumer group, women account for the largest share of the market due to frequent usage, gifting cycles, and broader scent adoption

The women’s category, strengthened by daily consumption, social occasions, and gifting, continues to dominate the Australia fragrance and perfume market. Brands prioritize women-focused launches since replacement cycles are shorter and volume visibility is higher. Retailers allocate more shelf space to women’s fragrances due to predictable sell-through and higher SKU diversity. Women are also more receptive to limited editions and seasonal variations, allowing brands to extend product lifecycles.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Unisex fragrances also contribute to the Australia fragrance and perfume market revenue, as brands deliberately reduce gendered positioning. Younger consumers prefer ingredient-led storytelling over traditional masculine or feminine cues. Companies are launching unisex fragrances to simplify portfolios and widen addressable audiences. These products support shared household usage, increasing utilization rates per bottle. Companies like SBS are launching a limited-edition fragrances such as Alone Cologne, marketed as an essence of being alone to attract the unisex category. Growth is also driven by minimalist branding and lifestyle alignment rather than identity-based marketing.

By distribution channel, the offline category captures the dominant market share due to sensory validation and assisted premium selling

Offline channels dominate fragrance sales in Australia because scent evaluation remains sensory-led. Consumers prefer to test fragrances physically before committing, especially for premium priced products. Department stores and specialty retailers provide assisted selling, sampling, and gifting confidence. Brands rely on offline counters to communicate heritage, craftsmanship, and product differentiation. Manufacturers favor this offline channel for flagship launches due to better brand control.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The online channel presents significant Australia fragrance and perfume market opportunities as digital discovery tools to improve purchase confidence. Brands use quizzes, sampling kits, and loyalty data to personalize recommendations. Once preferences are established, consumers shift to online channels for convenience and replenishment. Direct-to-consumer platforms allow better margin capture and data ownership. Retailers benefit from reduced overheads and wider geographic reach. Online channels also support niche and unisex fragrances that rely on storytelling rather than counter presence. For example, in October 2025, Fragrance brand Kayali was made available through its own, stand-alone website as the brand launched a direct-to-consumer (D2C) platform.

New South Wales sustains its market dominance due to retail concentration and premium demand

New South Wales dominates the fragrance market due to its dense urban population and premium retail infrastructure. Sydney hosts flagship department stores, luxury malls, and international tourism flows that support high fragrance consumption. Brands prioritize New South Wales for launches due to visibility and faster sell-through. Retailers benefit from higher footfall and premium basket sizes. This region also supports niche and luxury fragrances due to higher disposable incomes. Leveraging such opportunities, in October 2025, Myer launched Australia’s first immersive multi-brand fragrance destination at its Liverpool store, showcasing Rabanne, Jean Paul Gaultier, Carolina Herrera.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Queensland represents the fastest-growing fragrance and perfume market in Australia as population migration accelerates. Lifestyle-driven consumption supports casual, everyday fragrance usage. Expanding specialty retail and tourism contribute to the rising demand. Brands are increasing regional distribution depth to capture growth beyond metropolitan hubs. Queensland consumers show openness to new brands and formats, supporting experimentation.

Leading Australia fragrance and perfume companies are focusing on premiumization, refillable formats, and controlled distribution to protect margins. Luxury brands are strengthening flagship presence and private client programs, while domestic companies invest in formulation innovation and small-batch flexibility. Opportunities lie in premium refill systems, unisex fragrance positioning, and data-led product planning.

Australia fragrance and perfume market players are also exploring faster regional launches beyond Sydney and Melbourne. Local manufacturing partnerships are gaining importance to shorten lead times and improve compliance. The competitive environment rewards companies that balance brand storytelling with operational discipline. Those investing in sustainable packaging, AI-supported scent profiling, and loyalty-driven replenishment are better positioned to capture long-term value.

Founded in 1987 and headquartered in Paris, France, LVMH plays a dominant role in Australia fragrance and perfume market dynamics through brands like Dior, Guerlain, and Givenchy. The company focuses on high-concentration variants, refillable luxury bottles, and private client engagement. In Australia, LVMH prioritizes department store exclusives and controlled rollouts.

Established in 2019 and headquartered in Australia, Arise Aromatics operates as a contract manufacturer and private-label fragrance specialist. The company caters to niche brands seeking small-batch production and fast formulation cycles. Arise focuses on natural extracts, compliant ingredient sourcing, and flexible MOQs.

Founded in 2017 and headquartered in Melbourne, Australia, MetaScent Australia specializes in AI-assisted scent development and digital fragrance profiling. The company supports brands with data-driven formulation and consumer testing tools. MetaScent’s technology helps reduce failed launches and improves scent-market fit.

Established in 2018 and headquartered in Australia, Fragrance Innovation Australia focuses on sustainable fragrance chemistry and encapsulation techniques. The company works with brands developing long-lasting and low-allergen formulations. Its expertise supports premium and functional fragrance applications.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Other key players in the market include Chanel Limited, Avon Products, Inc., and PVH Corp, among others.

Unlock the latest insights with our Australia fragrance and perfume market trends 2026 report. Discover regional growth patterns, consumer preferences, and key industry players. Stay ahead of competition with trusted data and expert analysis. Download your free sample report today and drive informed decisions in the market.

South Korea Fragrances and Perfume Market

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market reached an approximate value of USD 732.97 Million.

The market is projected to grow at a CAGR of 4.10% between 2026 and 2035.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach USD 1095.45 Million by 2035.

Stakeholders are investing in refill systems, expanding unisex portfolios, integrating digital scent tools, strengthening regional distribution, and optimizing inventory planning while building premium storytelling aligned with evolving consumer expectations.

Key trends aiding the market expansion include increasing consumer preference for natural and clean label products, the incorporation of aromatherapy elements in perfumes.

Regions considered in the market are New South Wales, Victoria, Queensland, Western Australia, and Australian Capital Territory, among others.

Based on type, the market segmentations include Parfum or De Parfum, Eau De Parfum (EDP), Eau De Toilette (EDT), and Eau De Cologne (EDC).

Men, women, and unisex are considered in the report.

The key players in the market include LVMH Moët Hennessy – Louis Vuitton, Arise Aromatics Pty Ltd, MetaScent Australia, Fragrance Innovation Australia, Chanel Limited, Avon Products, Inc., and PVH Corp, among others.

Rising raw material costs, stricter ingredient regulations, high packaging expenses, and demand volatility challenge profitability. Brands also face balancing premium positioning with accessibility while managing inventory risks across channels.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Type |

|

| Breakup by Consumer Group |

|

| Breakup by Distribution Channel |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.