Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

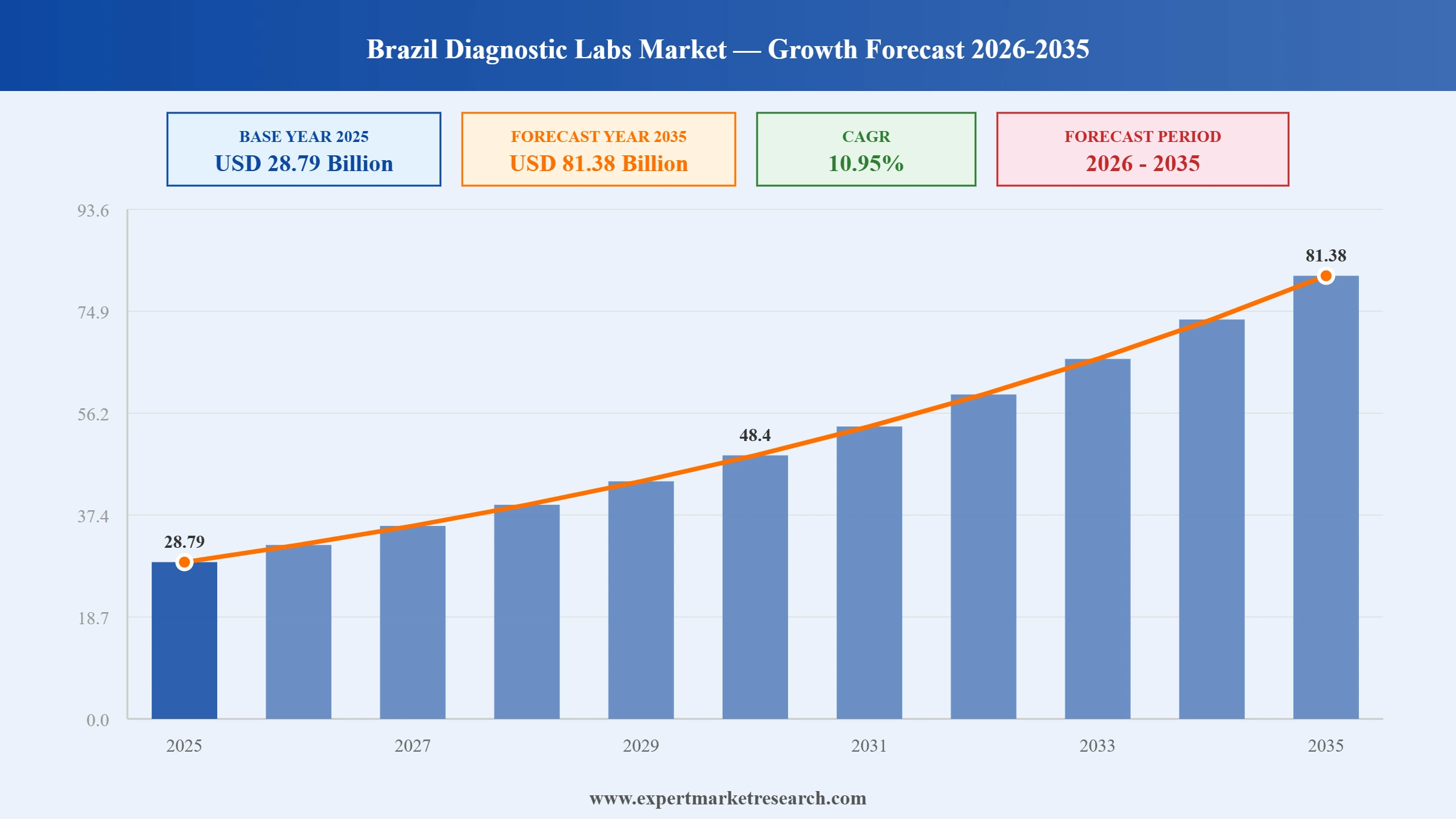

The Brazil Diagnostic Labs Market reached a value of USD 28.79 Billion at 2025 and is projected to expand at a CAGR of around 10.95% during the forecast period of 2026-2035. With rising chronic disease prevalence, growing insurance penetration, increasing genomics adoption, and large-scale modernization of laboratory infrastructure, the market is expected to reach USD 81.38 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The Brazil Diagnostic Labs Market is undergoing a structural shift driven by genomics adoption, large-scale infrastructure modernization, rising chronic disease demand, and deeper integration of digital and AI-powered diagnostic tools. These trends are collectively accelerating market growth and redefining how diagnostic services are delivered across Brazil's public and private healthcare systems.

Dasa, the largest integrated healthcare network in Brazil, initiated a comprehensive modernization program covering 18 of its centralized laboratory processing facilities, known as Nucleos Tecnico-Operacionais. The overhaul, supported by partnerships with global suppliers including Roche, Abbott, Beckman Coulter, Mindray, Stago, and QuidelOrtho, covers approximately 70% of the company's core lab processing capacity. The initiative followed the company's return to profitability in Q3 2025, with national diagnostic revenue growing 14.6% year on year.

MGI Tech expanded its collaboration with the Oswaldo Cruz Foundation's (FIOCRUZ) Diagnostic Support Unit (UNADIG) to accelerate genomic surveillance and personalized medicine in Brazil. Building on a relationship established during the COVID-19 pandemic, the expanded partnership enables UNADIG's molecular genetics laboratory to process over 2,000 samples weekly, covering oncology, infectious disease, and hereditary condition diagnostics. The initiative also reflects MGI's broader 2024 partnerships with Dasa, Grupo Sabin, and Oncoclinicas for genetic sequencing expansion.

MGI Tech formalized a strategic partnership with Oncoclinicas and Co., a leading oncology care network in Brazil, to integrate DNBSEQ-G400 medium-throughput genomic sequencers into the company's genomics department. This partnership enables Oncoclinicas to process germline panels for cancer syndrome diagnosis and somatic panels for tumor genomic profiling. In 2024, approximately 12,000 samples were sequenced at the institution, with the new technology expected to significantly increase throughput and diagnostic precision for cancer patients.

MGI Tech Co., Ltd. formalized a strategic alliance with Dasa to expand next-generation genomic sequencing capabilities across Brazil's diagnostic network. The collaboration integrates MGI's DNBSEQ sequencing platforms and lab automation technologies into Dasa's laboratory network, aiming to bring precision genomic testing for cancers and rare diseases to a wider patient base across Latin America. The partnership builds on MGI's prior inauguration of a Customer Experience Center in Sao Paulo in April 2024.

Grupo Fleury, in partnership with C2N Diagnostics, made the PrecivityAD2 blood test available exclusively in Brazil. The test detects amyloid plaque proteins from a simple blood sample, providing an alternative to costly and invasive PET scans and cerebrospinal fluid analysis for Alzheimer's disease diagnosis. Brazilian government data estimates 1.2 million Brazilians are affected by Alzheimer's, with a significant proportion yet to receive formal diagnosis, highlighting the clinical and commercial potential of this offering.

Major diagnostic chains in Brazil are investing heavily in upgrading their centralized laboratory processing infrastructure to improve throughput, standardize quality, and reduce operational costs. This wave of capital investment reflects a competitive shift toward technology-driven scale advantages. The modernization programs involve replacing legacy equipment with state-of-the-art analyzers from global medical technology suppliers. These upgrades are expected to significantly improve turnaround times, diagnostic accuracy, and financial margins for leading operators while raising entry barriers for smaller competitors. In February 2026, Dasa launched Brazil's largest-ever lab infrastructure overhaul, covering 70% of its core processing capacity across 18 facilities in partnership with Roche, Abbott, and four other global suppliers.

Brazil's public health system, the SUS, is under significant pressure to expand access to specialized diagnostic services. The government's Mais Acesso a Especialistas program has committed R$ 2.4 billion to expand specialist consultations and diagnostic exam availability by 30%, with the funding extending through 2025. This initiative is creating new revenue opportunities for private lab operators and driving demand for capacity expansion. Public-private collaboration models are emerging as a practical pathway to bridge gaps in diagnostic access, particularly in underserved regions outside the major urban centers of Sao Paulo and Rio de Janeiro.

The integration of next-generation genomic sequencing into routine diagnostic workflows is rapidly reshaping how Brazilian labs detect and manage diseases. Driven by partnerships between global technology firms and major local diagnostic networks, genomic testing is expanding from specialized oncology centers into broader clinical settings. Companies are investing in sequencing platforms to offer faster and more precise diagnoses for cancers, rare diseases, and hereditary conditions. This shift is supporting Brazil diagnostic labs market growth by opening premium testing segments and attracting investment in high-complexity lab capabilities. In September 2024, MGI Tech and Dasa formalized a strategic genomics alliance to expand precision medicine access across Brazil, integrating advanced sequencing platforms into Dasa's national diagnostic network.

Brazil's demographic profile is shifting toward an older population base, with a disproportionately high burden of chronic conditions requiring ongoing diagnostic monitoring. According to a March 2024 study, approximately 70% of Brazilians aged 60 and above live with at least one chronic illness such as diabetes, cardiovascular disease, or hypertension. This creates a sustained and growing pipeline of routine testing demand, particularly for clinical chemistry, pathology, and imaging services. The structural nature of this demand driver makes it one of the most durable growth catalysts for the diagnostics sector over the forecast period. Brazil's elderly population is projected to grow significantly through 2050, further reinforcing this trend.

The report of the Expert Market Research report titled "Brazil Diagnostic Labs Market Report and Forecast 2026 to 2035 offers a detailed analysis of the market based on the following segments:

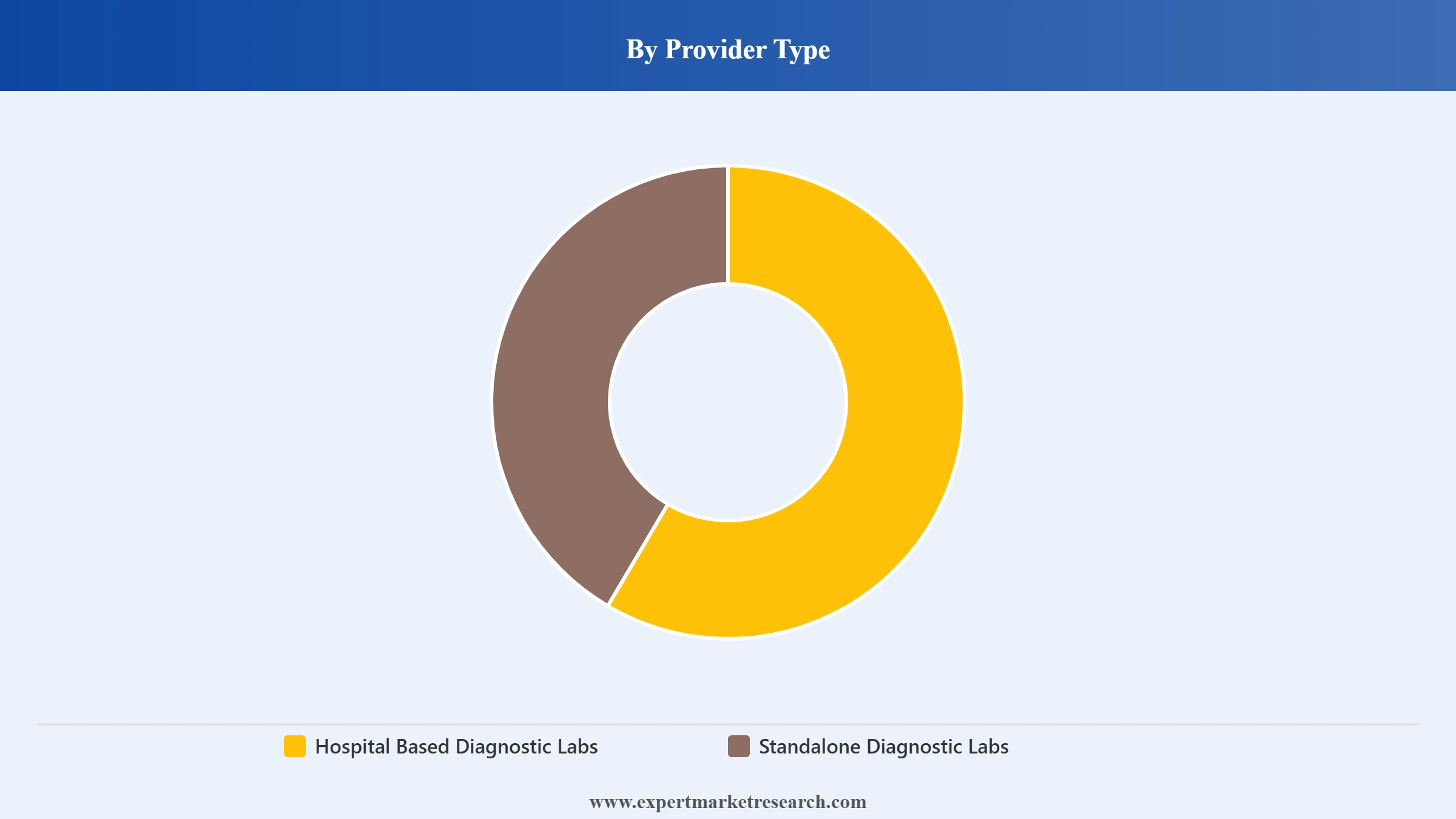

Market Breakup by Provider Type

Key Insights: Hospital-based diagnostic labs benefit from direct integration with inpatient and outpatient care pathways, with leading hospital groups such as Albert Einstein offering diagnostic medicine services as a core revenue line. Standalone labs, however, hold the larger share of the Brazilian market at approximately 55%, competing through convenient access points, faster turnaround times, and competitive pricing for corporate and retail clients. The standalone segment spans both large chain operators and independent facilities. The ongoing consolidation trend, with major networks like Dasa and Grupo Fleury acquiring regional players, is gradually professionalizing the standalone segment and upgrading service quality across Brazil's diverse geography.

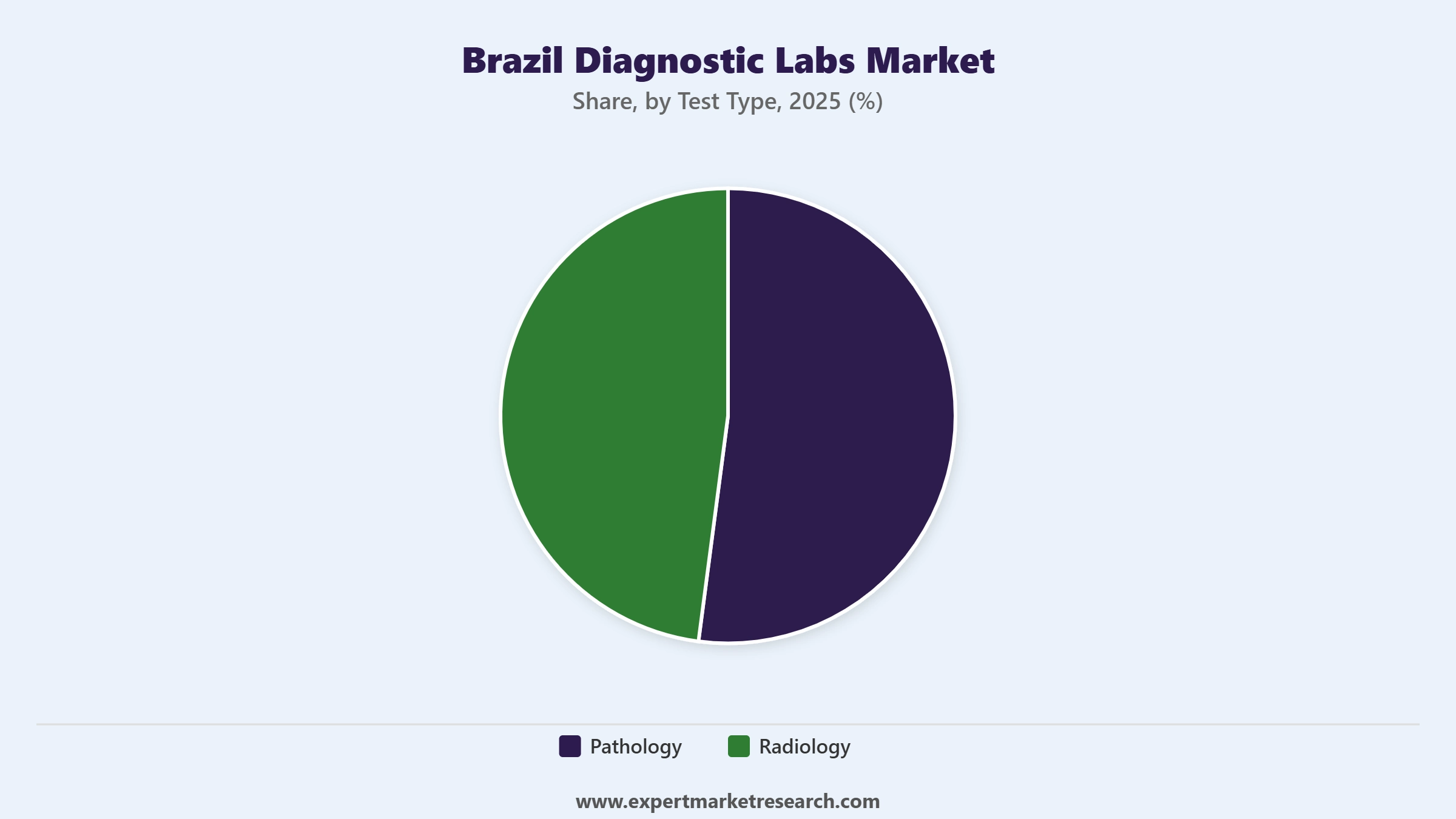

Market Breakup by Test Type

Key Insights: Pathology testing commands the largest share of the Brazilian diagnostic labs market, driven by its broad application across routine clinical chemistry, hematology, molecular diagnostics, and anatomical pathology. The rising burden of oncological conditions and infectious diseases in Brazil, including tuberculosis (41 new cases per 100,000 population in 2022 per the Pan American Health Organization) and HIV, sustains high-volume demand for pathology tests. Radiology is growing rapidly as access to CT, MRI, and ultrasound services expands beyond major urban centers, supported by investments in digital imaging infrastructure. Both segments are benefiting from increasing health insurance coverage, which reached 53.2 million beneficiaries as of December 2025.

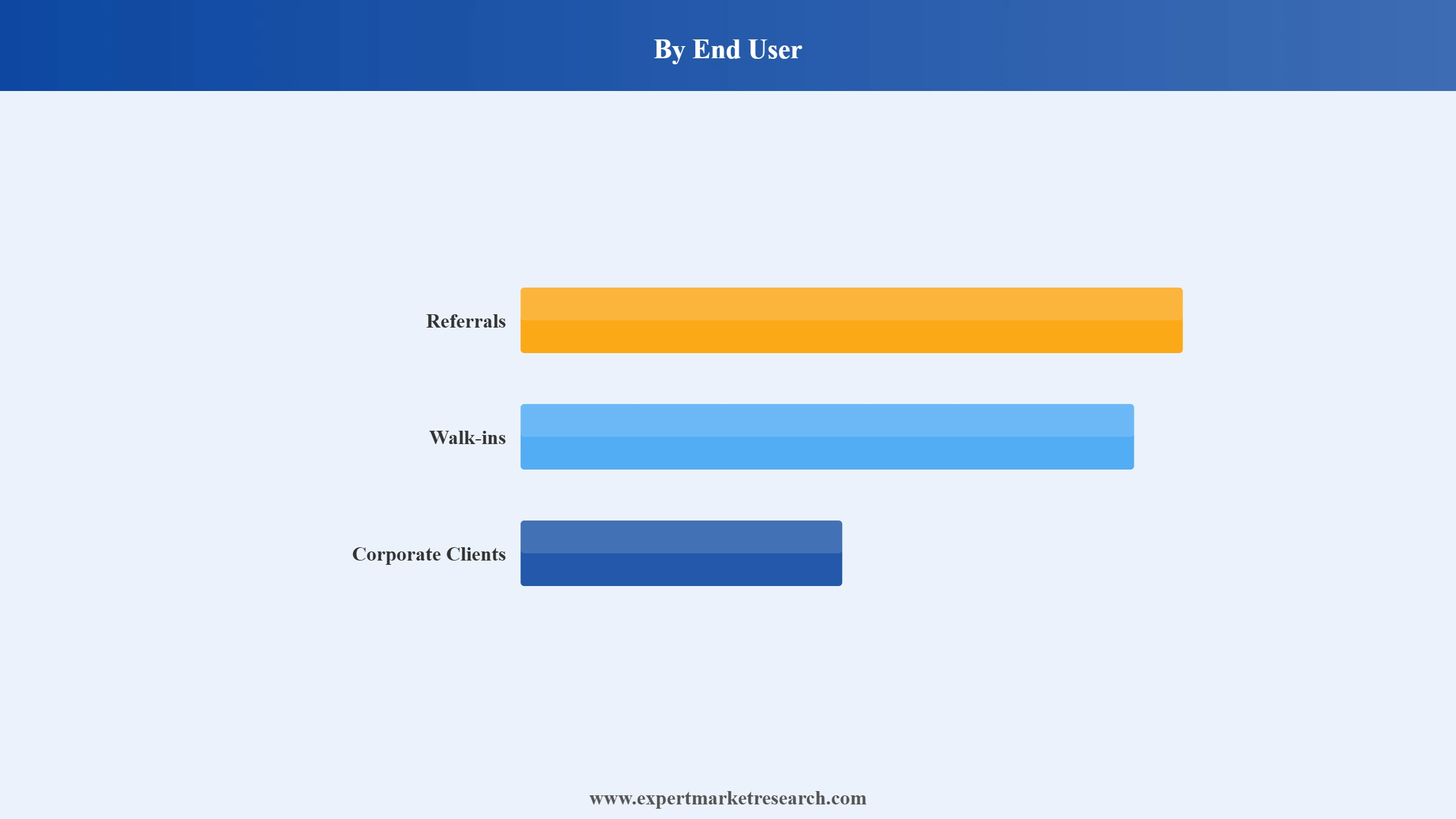

Market Breakup by End User

Key Insights: Referrals from physicians and hospital networks represent the most structured demand channel for diagnostic labs in Brazil, underpinned by health insurance authorization and care pathway requirements. Walk-in clients have grown as health awareness increases and labs expand into retail-facing formats, particularly in urban areas. Corporate clients are an increasingly important segment as employers and occupational health programs invest in preventive screening for workforce health management. The corporate segment is also linked to Brazil's private insurance market, where diagnostics form a core component of employer health benefit packages.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Provider Type

Standalone Diagnostic Labs hold the majority position within Brazil's diagnostic market, accounting for approximately 55% of the overall market by volume. Their dominance stems from widespread geographic distribution, competitive pricing relative to hospital-based labs, and established relationships with individual clinicians, corporate clients, and health insurers. The standalone segment's growth is being further reinforced by ongoing consolidation: major chains are acquiring smaller independent facilities to build scale, expand geographic reach, and negotiate better insurance reimbursement terms. Hospital-based diagnostic labs, while holding the remaining share, are differentiated by their access to complex inpatient testing pipelines and specialized diagnostic capabilities linked to tertiary care hospitals.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Test Type

Pathology is the dominant category in Brazil's diagnostic testing landscape, led by the consistently high volumes of clinical chemistry tests, hematology panels, and molecular diagnostics for infectious and oncological diseases. The country's high burden of communicable diseases, including tuberculosis and HIV, keeps pathology demand structurally elevated across both public and private health systems. Radiology is the second major segment, growing on the back of broader access to imaging equipment in secondary cities and the adoption of digital radiology solutions that reduce costs and improve turnaround times.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By End User

Corporate clients represent one of the fastest-growing demand channels within Brazil's diagnostic labs market, driven by the expansion of occupational health mandates and employer wellness programs within the country's formal private sector economy. Referrals from physicians and healthcare providers, while the largest single channel, are increasingly channeled through digital ordering platforms that improve lab workflow efficiency and reduce administrative overhead. The walk-in segment is growing in urban areas as consumer health awareness rises, with major diagnostic chains investing in flagship service centers that offer a more retail-oriented experience.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The Brazil Diagnostic Labs Market operates within a concentrated but evolving competitive structure, where a small number of large national chains command significant market share alongside a fragmented base of independent standalone labs and hospital-linked facilities. The top five diagnostic companies collectively hold an estimated 60% of the market, with consolidation through acquisitions and partnerships remaining the dominant growth strategy for leading players. Technology differentiation, particularly through genomics, AI-assisted diagnostics, and digital patient experience platforms, is becoming a key competitive priority alongside traditional factors such as turnaround time, geographic coverage, and insurance network participation.

The competitive dynamics of the market are also shaped by the rising role of public-private collaboration, as major operators seek to expand reach through SUS-linked programs while maintaining premium private-pay service lines. International players such as Quest Diagnostics add a global dimension to the competitive landscape, while domestic groups like Grupo Fleury and Sabin compete on the strength of brand recognition, physician relationships, and specialized testing portfolios.

Agilus Diagnostics is a major diagnostic services organization with an extensive network of collection and processing centers. The company focuses on providing a comprehensive range of clinical, pathology, and specialized testing services. Its capabilities span routine diagnostics to high-complexity testing, with a growing emphasis on technology-driven quality improvements and expanded reach through strategic partnerships and acquisitions.

Founded in 1999 and headquartered in Sao Paulo, Dasa is the largest integrated healthcare network in Latin America, serving over 23 million patients annually across a network of more than 450 diagnostic exam processing facilities. Operating multiple diagnostic brands including Lavoisier and Alta Excelencia Diagnostica, Dasa has invested aggressively in genomics, digital health, and infrastructure modernization. Its strategic alliances with global technology partners and consistent double-digit revenue growth in diagnostics position it as the dominant competitive force in Brazil's lab services market.

Established in 1967 and headquartered in Secaucus, New Jersey, Quest Diagnostics is one of the world's leading providers of diagnostic information services. With operations in over 50 countries and a focus on advanced laboratory testing including molecular diagnostics, genetic testing, and clinical trials services, Quest brings global capabilities to the Brazilian market. Its presence in Brazil strengthens the country's access to specialized testing methodologies and expands the availability of international-standard diagnostic services for private healthcare networks.

Founded in 1926 and headquartered in Sao Paulo, Grupo Fleury is one of Brazil's most established and trusted diagnostic and health services companies. Operating more than 250 care centers and performing over 80 million exams annually, the group offers pathology, imaging, and digital health services. Grupo Fleury's ongoing investments in specialized testing, including its exclusive availability of the PrecivityAD2 Alzheimer's blood test and AI-driven diagnostic tools, reinforce its leadership in premium diagnostics. The company holds approximately 20% market share in Brazil's diagnostics sector.

Other key players in the market are Sabin, Albert Einstein Diagnostic Medicine, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Get ahead of the curve in one of Latin America's most dynamic healthcare sectors. Our comprehensive Brazil Diagnostic Labs Market Report for 2026 delivers the granular intelligence you need to make confident business decisions, covering technology shifts, corporate moves, insurance dynamics, and segment-level demand trends. Whether you are a diagnostic lab operator, a medical technology supplier, a private equity investor, or a healthcare strategist, this report gives you the clarity and depth to act with precision. Download your free sample today and unlock the key opportunities shaping Brazil's diagnostic labs sector.

Upto 15% Off

USD

$1999 $1799

$3099 $2789

$4599 $3909

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

At 2025, the market reached an approximate value of USD 28.79 Billion.

The market is projected to grow at a CAGR of 10.95% between 2026 and 2035.

The market is projected to grow significantly during the forecast period 2026-2035 to reach USD 81.38 Billion for 2035.

The Brazil Diagnostic Labs Market is driven by a combination of structural and cyclical factors. Rising chronic disease prevalence, particularly among an aging population where approximately 70% of Brazilians aged 60 and above have at least one chronic illness, creates sustained demand for routine and specialized testing. Expanding private health insurance coverage (reaching 53.2 million beneficiaries as of late 2025) is formalizing demand and enabling labs to grow through insurer-linked reimbursement channels. Government investment through programs like Mais Acesso a Especialistas is also expanding public sector diagnostic access. Technology-led catalysts including the adoption of genomics, molecular diagnostics, and AI-assisted interpretation are opening premium-value testing segments and attracting capital investment into major lab networks.

By provider type, the Brazil Diagnostic Labs Market is divided into Hospital Based Diagnostic Labs and Standalone Diagnostic Labs. Standalone labs are the dominant segment, holding approximately 55% of the market due to their wide geographic distribution, competitive pricing, and strong relationships with individual clinicians, corporate clients, and health plan operators. Hospital-based labs serve a distinct clinical need by integrating directly with inpatient and outpatient hospital workflows, particularly for complex and urgent diagnostic testing. Consolidation activity, with major national chains acquiring standalone facilities, is reshaping both segments by reducing fragmentation and raising the competitive bar on quality and efficiency.

The most significant trends reshaping Brazil's diagnostic labs sector include the adoption of next-generation genomics and precision medicine, large-scale infrastructure modernization by major operators, the growing burden of chronic and age-related diseases sustaining structural demand growth, and public-private partnerships enabled by government healthcare access programs. Digital transformation, including AI-driven diagnostics and digital patient platforms, is also becoming a core competitive differentiator among leading operators.

The key players in the market include Agilus Diagnostics, Dasa (Diagnosticos da America S.A.), Quest Diagnostics, Grupo Fleury, Sabin, and Albert Einstein Diagnostic Medicine.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Provider Type |

|

| Breakup by Test Type |

|

| Breakup by End User |

|

| Market Dynamics |

|

| Supplier Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 1,999

USD 1,799

tax inclusive*

Single User License

One User

USD 3,099

USD 2,789

tax inclusive*

Five User License

Five User

USD 4,599

USD 3,909

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.