Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

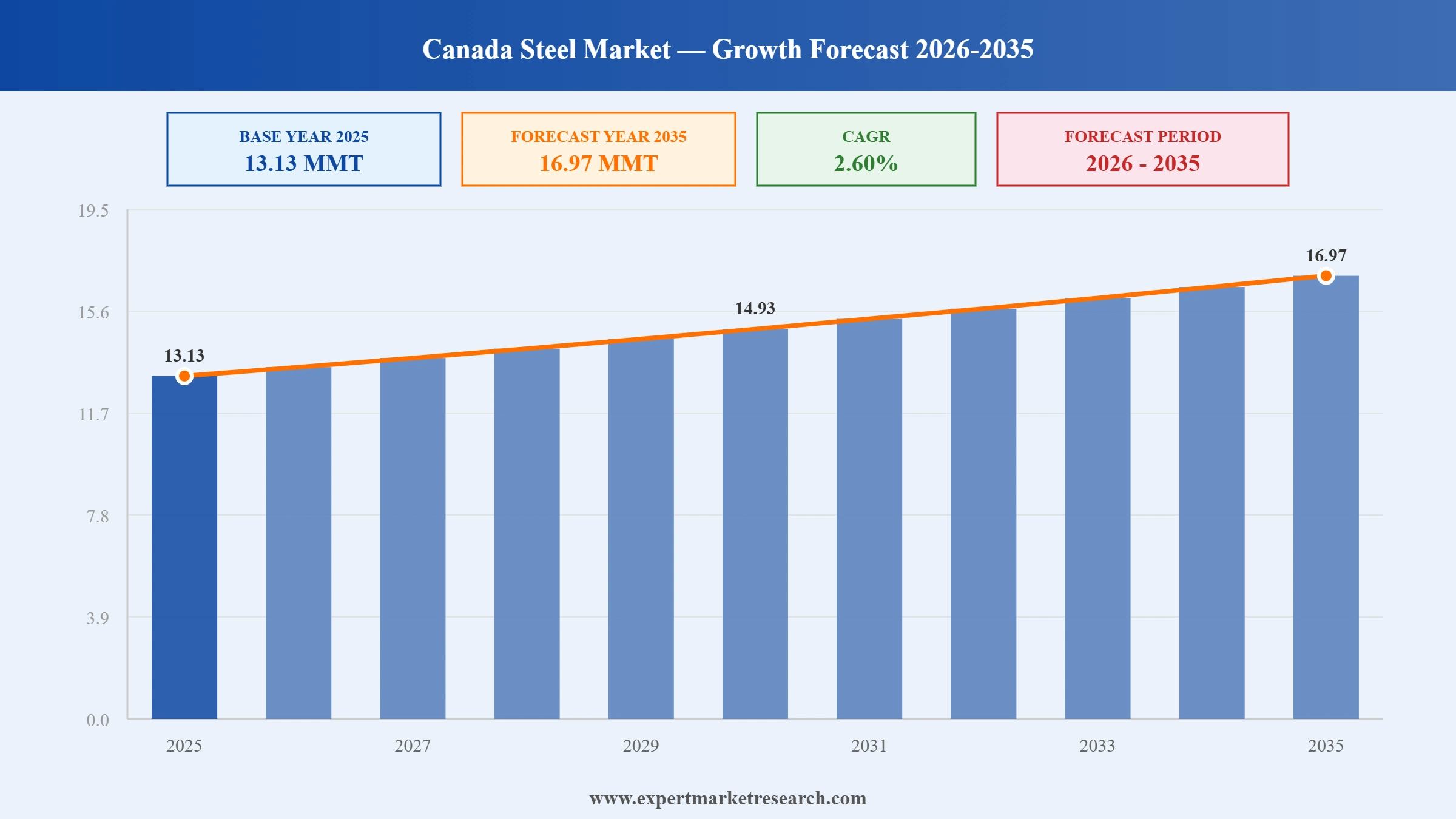

The Canada Steel Market attained a volume of 13.13 MMT in 2025 and is set to grow at a CAGR of around 2.60% through 2026-2035. Sustained public infrastructure investment, accelerating adoption of electric arc furnace and low-carbon steelmaking, and a strategic pivot toward domestic, defence, and shipbuilding demand amid US tariffs are reinforcing growth momentum. The market is on track to reach 16.97 MMT by 2035. Rising demand for structural and rebar-grade steel, advanced high-strength steel for automotive and EV manufacturing, green steel transition investments, and energy and infrastructure project pipelines are fuelling the Canada steel market.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The Canada steel market is being reshaped by a rapid green steel transition, the disruptive impact of US Section 232 tariffs, and a strategic pivot toward domestic, defence, and shipbuilding demand. Leading producers are decommissioning blast furnaces in favour of electric arc and direct-reduction technologies while diversifying their customer base within Canada.

In March 2026, Algoma Steel completed its shift to electric arc furnace steelmaking after permanently closing its blast furnace in January, and secured a CAD 500 million federal liquidity facility to support ramp-up and Canada's industrial and defence steel supply.

In January 2026, Algoma Steel signed a memorandum of understanding with South Korea's Hanwha Ocean to supply Canadian-made steel for shipbuilding, reinforcing domestic marine and defence supply chains and supporting Canada's National Shipbuilding Strategy amid US tariff pressures.

In October 2025, ArcelorMittal Dofasco hosted a groundbreaking ceremony for its transformational low-carbon direct-reduced-iron and electric-arc-furnace steelmaking project in Hamilton, Ontario, designed to significantly reduce plant emissions and modernise its flat-steel production base.

In July 2025, Algoma Steel produced its first batch of steel from its new electric arc furnace in Sault Ste. Marie, a milestone for Canadian green steel and a pivotal step in its multi-year, emissions-reducing modernisation strategy.

The green steel transition is reshaping the Canada steel market. Algoma Steel's completed electric arc furnace conversion and ArcelorMittal Dofasco's direct-reduced-iron project in Hamilton aim to cut emissions sharply, positioning low-carbon Canadian steel to gain share over high-carbon imports.

US tariffs are reshaping Canada steel market growth. The 50% Section 232 duties imposed in June 2025 curtailed access to American buyers, prompting producers such as Algoma Steel to pivot toward Canadian plate, defence, shipbuilding, energy, and infrastructure customers nationwide.

Infrastructure remains a core driver of the Canada steel market. Projects such as the Ontario Line subway, Montreal's REM network, and British Columbia highway expansions, backed by the Canada Infrastructure Bank, are sustaining structural and rebar-grade steel demand through 2035.

Automotive demand underpins the Canada steel market. Flat-rolled producers in Ontario supply high-strength sheet and coil to General Motors, Ford, and Stellantis, with rising EV manufacturing lifting demand for precision steel in battery casings and lightweight chassis components.

Shipbuilding and defence are emerging growth avenues in the Canada steel market. Algoma Steel's partnerships with Hanwha Ocean and Seaspan Vancouver Shipyards aim to qualify Canadian-made maritime and conventional-grade steel, supporting icebreaker and naval programmes while reducing import reliance.

The Expert Market Research's report titled “Canada Steel Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

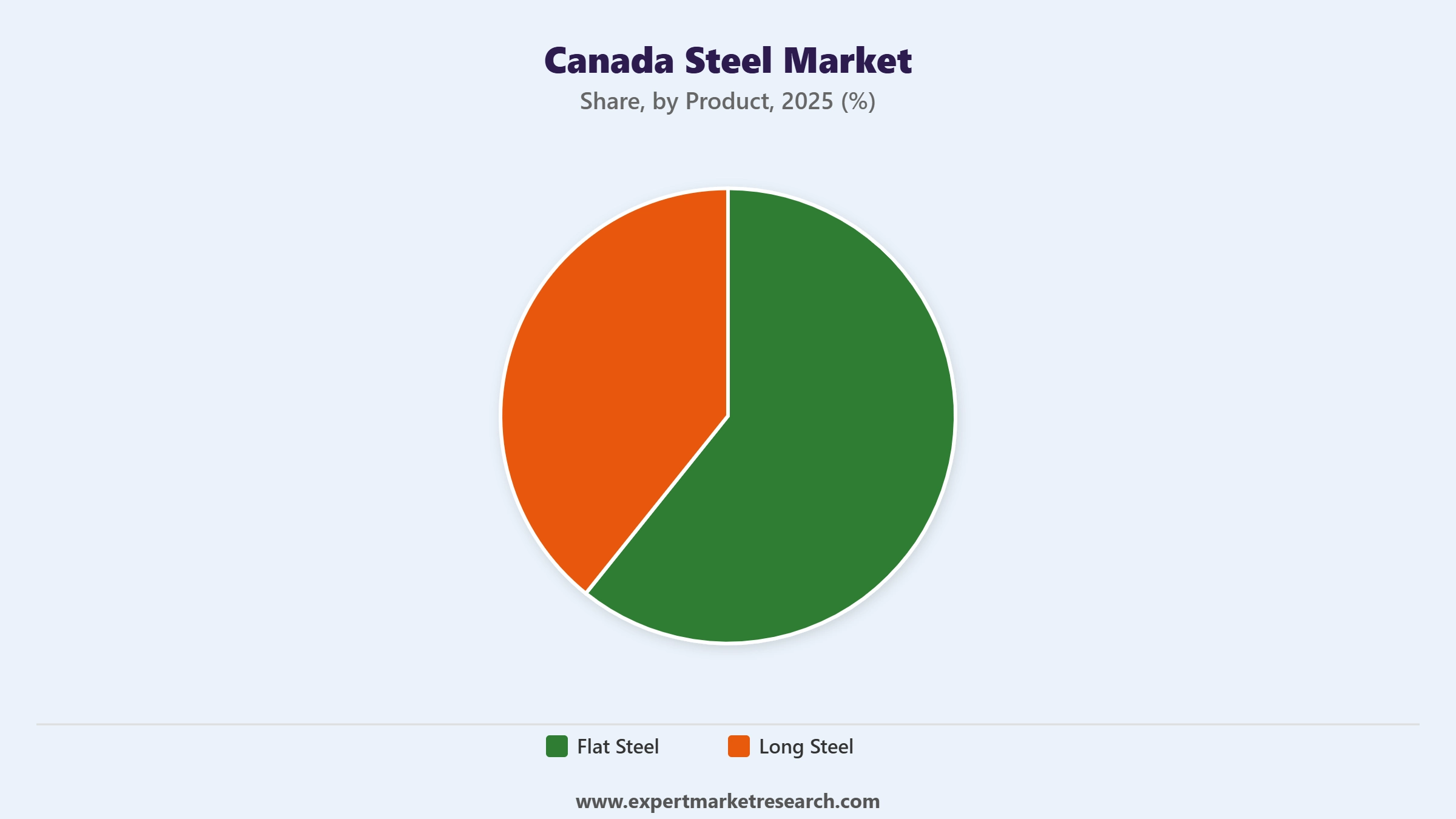

Market Breakup by Product

Key Insight: Flat steel, including hot-rolled and cold-rolled sheet, plate, and coil, anchors automotive and manufacturing demand across Ontario's auto corridor and is increasingly used in EV battery casings and chassis. Long steel, covering rebar and structural sections, is driven by sustained construction and infrastructure activity nationwide.

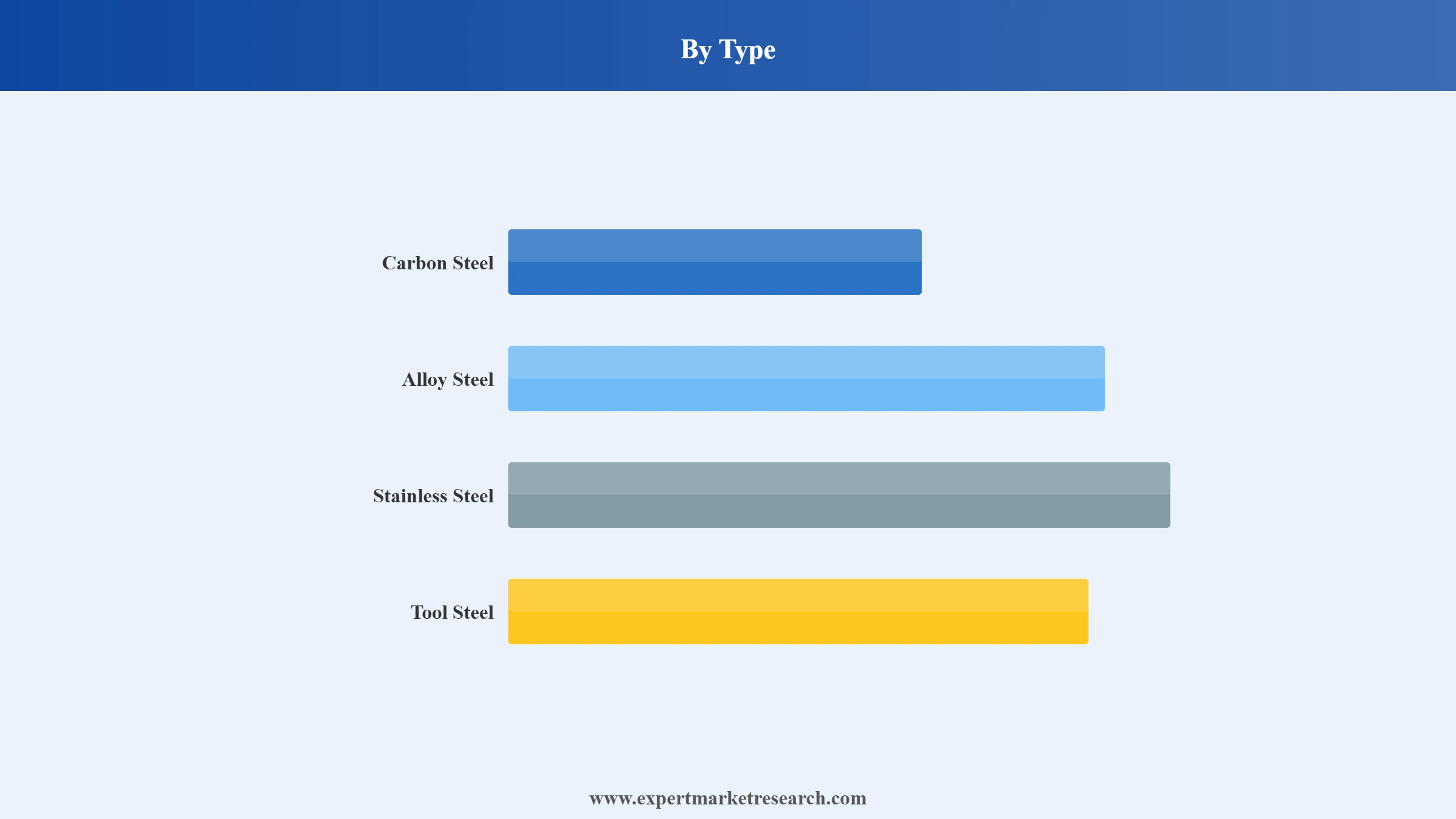

Market Breakup by Type

Key Insight: Carbon steel holds the largest share of the Canada steel market, valued for its cost-effectiveness across construction, pipelines, and general manufacturing. Alloy and stainless steel serve specialised automotive, energy, and industrial applications, while tool steel supports high-wear tooling and metal fasteners requiring superior hardness and durability.

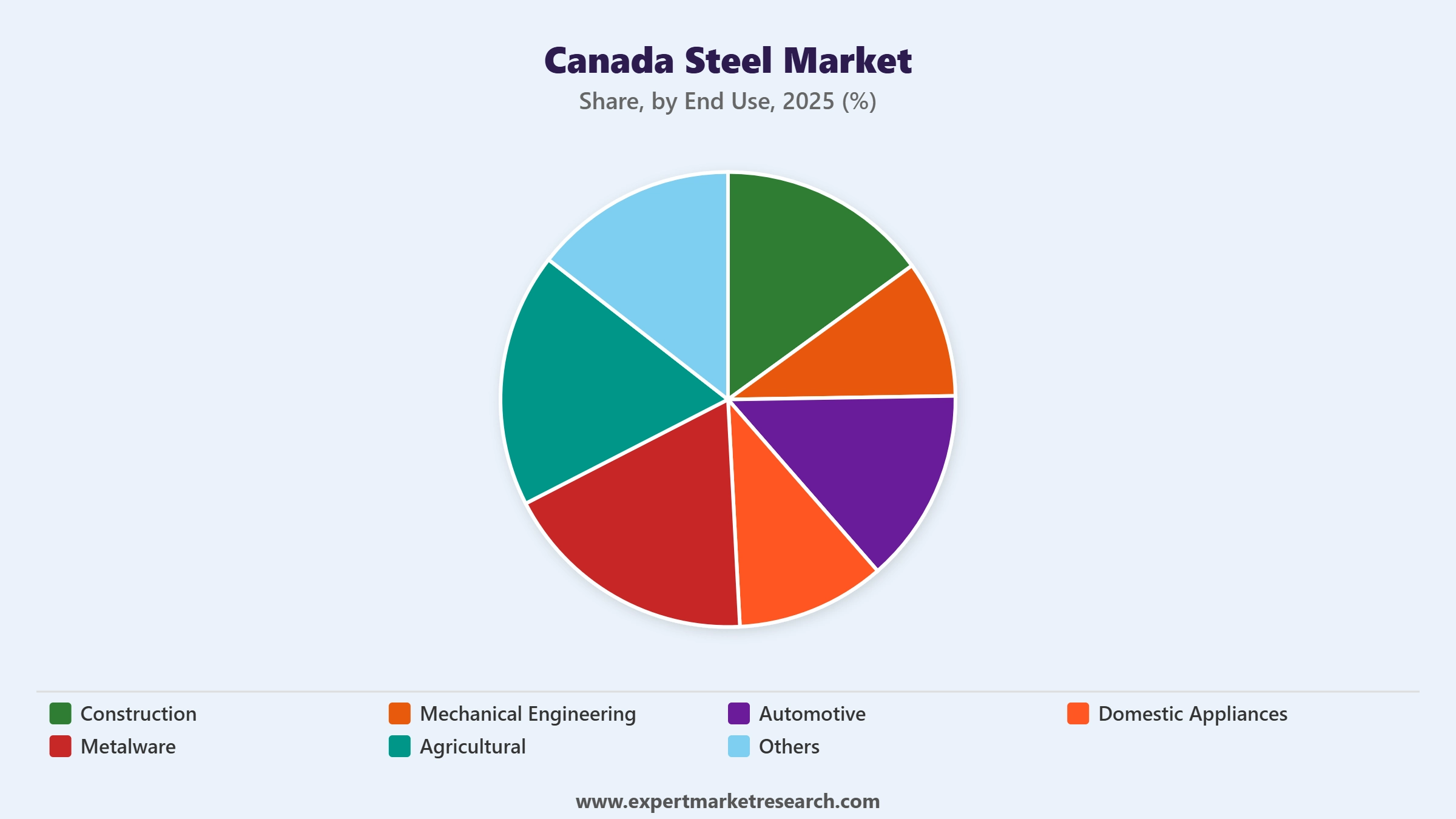

Market Breakup by End Use

Key Insight: Construction is the dominant end use in the Canada steel market, underpinned by infrastructure, transit, and building demand for structural and rebar-grade steel. Automotive is a major consumer of high-strength flat steel, while mechanical engineering, metalware, domestic appliances, and agriculture provide diversified, steady demand across the economy.

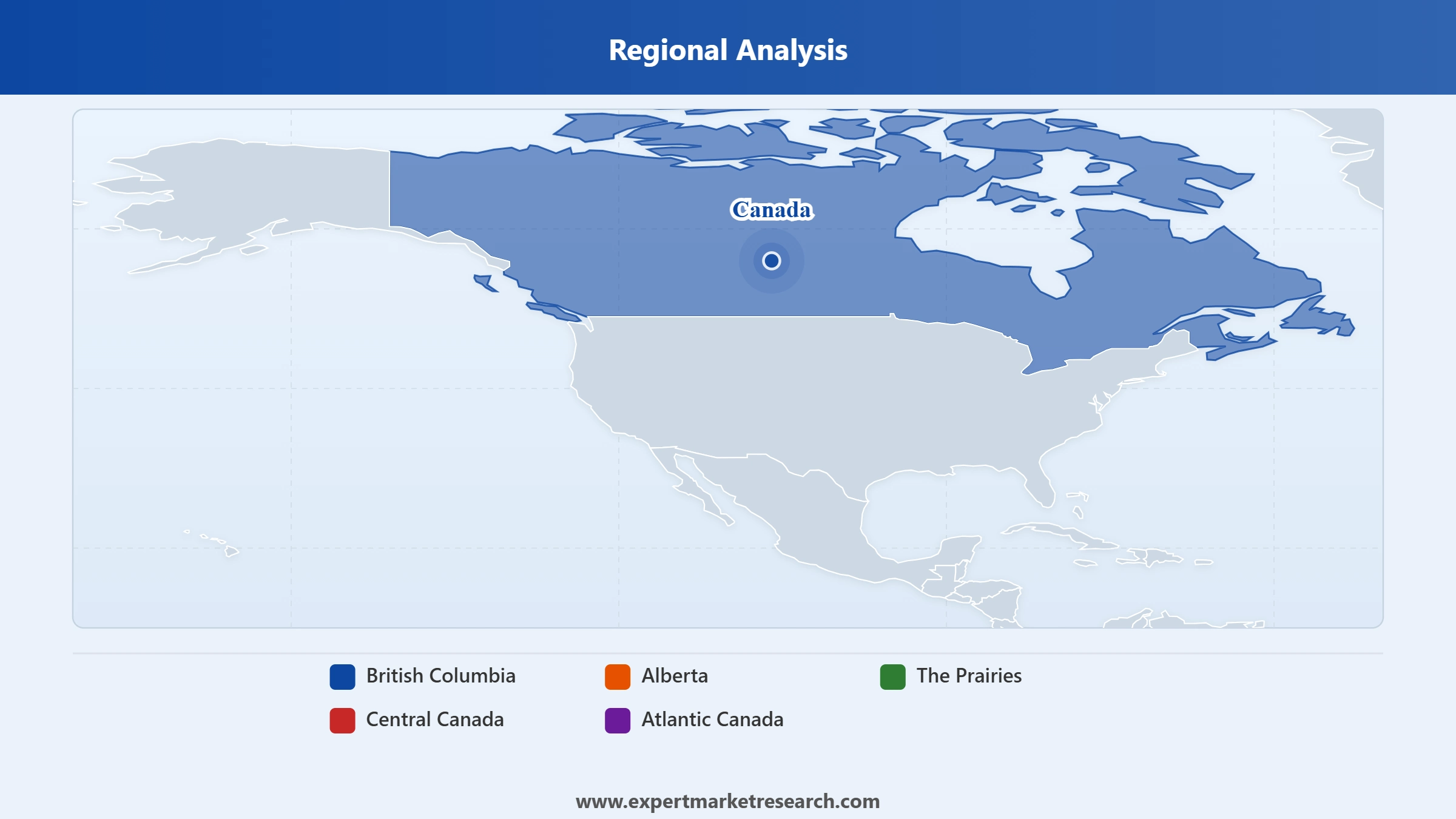

Market Breakup by Region

Key Insight: Central Canada, led by Ontario, dominates the Canada steel market, hosting the country's largest primary steelmakers and auto manufacturing base. British Columbia is the fastest-growing region, supported by infrastructure and shipbuilding, while Alberta and the Prairies benefit from energy and pipeline demand and Atlantic Canada provides steady consumption.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Product, Flat Steel dominates the market due to strong automotive, manufacturing, and clean-technology demand

Flat steel accounts for a leading share of the Canada steel market, reflecting its central role in automotive and manufacturing supply chains. Producers in Ontario's auto corridor ship large volumes of hot-rolled and cold-rolled sheet, plate, and coil to automakers and tier suppliers. Rising EV production is lifting demand for precision flat steel in battery casings and lightweight chassis components.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Long steel, including rebar and structural sections, holds a substantial share driven by construction and infrastructure activity. Public investment in transit, bridges, and highways sustains demand for reinforced and fabricated forms. As Canada advances major infrastructure pipelines, long steel demand remains resilient, complementing flat steel within the broader Canada steel market.

By Type, Carbon Steel accounts for the dominant share of the market due to its cost-effectiveness and broad application range

Carbon steel dominates the Canada steel market, prized for its strength, versatility, and low cost across construction, pipelines, automotive, and heavy machinery. Its use in beams, rebar, and tubes rises with ongoing infrastructure and energy projects, making it the backbone of domestic steel consumption and a key focus for producers ramping up electric arc furnace output.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Alloy, stainless, and tool steels serve higher-value, specialised niches. Alloy and stainless grades support automotive, energy, and industrial applications requiring corrosion resistance and strength, while tool steel meets demand for high-wear tooling and fasteners. These types command premium pricing and grow with advanced manufacturing across the Canada steel market.

By End Use, Construction accounts for the dominant share of the market due to sustained infrastructure and building investment

Construction is the largest end use in the Canada steel market, driven by public infrastructure programmes spanning transit, bridges, highways, and energy. Projects such as the Ontario Line and Montreal's REM sustain structural and rebar-grade steel demand, while the Canada Infrastructure Bank and green procurement standards reinforce a durable, low-carbon construction steel pipeline nationwide.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Automotive is a major end use, consuming high-strength flat steel for vehicle bodies and components, with EV growth lifting advanced steel demand. Mechanical engineering, metalware, domestic appliances, and agriculture add diversified consumption. In October 2025, ArcelorMittal Dofasco advanced its low-carbon project to modernise flat-steel supply for these end uses across the Canada steel market.

Central Canada dominates the market due to its concentration of primary steelmakers, auto manufacturing, and infrastructure demand

Central Canada, led by Ontario, dominates the Canada steel market, hosting most of the country's steel plants, including Algoma Steel in Sault Ste. Marie and ArcelorMittal Dofasco and Stelco in Hamilton. Ontario's auto manufacturing base and Quebec's industrial and transit projects sustain strong flat and long steel demand, anchoring national production and consumption.

British Columbia is the fastest-growing region, supported by highway expansion, port and shipbuilding activity, and infrastructure investment. Alberta and the Prairies benefit from energy, pipeline, and agricultural demand, while Atlantic Canada provides steady consumption. Across regions, infrastructure pipelines and the green steel transition continue to shape the Canada steel market.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The Canada steel market is moderately concentrated, led by a small number of integrated primary producers alongside specialised fabricators and distributors. Algoma Steel, ArcelorMittal Dofasco, and Stelco anchor primary flat and plate steelmaking, while Gerdau and others serve long-steel and specialty segments across construction, automotive, and industrial markets.

Competition centres on decarbonisation, cost efficiency, and customer diversification amid tariff disruption. Leading players are investing in electric arc furnace and direct-reduction technologies, securing government support, and pivoting toward domestic, defence, and shipbuilding demand, while fabricators compete on engineering capability, project execution, and reinforced and structural steel supply.

Founded in 1901 and headquartered in Sault Ste. Marie, Ontario, Algoma Steel is a leading Canadian producer of hot and cold rolled sheet and plate. It is the only independent primary steelmaker in Canada and completed its transition to electric arc furnace steelmaking in 2026.

Founded in 1912 and headquartered in Hamilton, Ontario, ArcelorMittal Dofasco is one of Canada's largest flat-rolled steel producers and part of ArcelorMittal. It supplies automotive, construction, and packaging markets and is advancing a low-carbon direct-reduced-iron and electric-arc-furnace project to cut emissions.

Founded in 1910 and headquartered in Hamilton, Ontario, Stelco is a major integrated flat-rolled steel producer operating Hamilton and Lake Erie works. Acquired by Cleveland-Cliffs in 2024, it supplies high volumes of flat-rolled steel to automakers and tier suppliers across Ontario's auto corridor.

Founded in 1901 and headquartered in Porto Alegre, Brazil, Gerdau is a leading long and specialty steel producer with significant North American operations. It supplies rebar, merchant bar, and structural steel to construction and industrial markets, including across Canada.

Other key players in the market include Rolled Alloys, Canam Group Inc., LMS Reinforcing Steel Group, Walters Inc., and others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Our full report for 2026-2035 provides the demand analysis, product and type segmentation, regional intelligence, and competitive benchmarking to navigate the Canada steel market with confidence. Reach out to our team to access the complete report or request a customised version.

Weathering Steel Market

Stainless Steel Market

Structural Steel Market

Electrical Steel Market

South Korea Steel Market

Saudi Arabia Structural Steel Market

North America Stainless Steel Market

Europe Stainless Steel Market

Asia Pacific Stainless Steel Market

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

The market is projected to grow at a CAGR of 2.60% between 2026 and 2035.

Canada produces its steel at 13 plants in five provinces, including Alberta, Manitoba, Ontario, Saskatchewan, and Quebec. The industry is largely concentrated in Ontario, with six plants operating there.

High-carbon steel has a high resistance to wear and tear, which makes it suitable tools and metal automotive fasteners. Manufacturers in automotive sector use high-carbon steel to produce bushings, chassis, vehicle frames, and door panels.

The key strategies driving the market include investing in green steel technologies, forming strategic partnerships, adopting Industry 4.0 innovations, focusing on product diversification, enhancing supply chain resilience, and targeting infrastructure projects. These approaches boost sustainability, efficiency, and competitiveness amid evolving market demands and regulatory pressures.

Key trends aiding market expansion rising residential and commercial construction, a growing demand for automobiles, and manufacturers investing in research to reduce the emissions of steel production.

Major countries in the market are British Columbia, Alberta, The Prairies, Central Canada, and Atlantic Canada.

The key products of steel are flat steel and long steel.

The key players in the market report include Algoma Steel Inc., ArcelorMittal Dofasco, Stelco Inc., Gerdau S/A, Rolled Alloys, Canam Group Inc., LMS Reinforcing Steel Group, Walters Inc., and others.

In 2025, the market reached an approximate volume of 13.13 MMT.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach about 16.97 MMT by 2035.

The construction segment dominates the market with uses in structural frameworks, reinforcing bars, beams, and roofing systems.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Product |

|

| Breakup by Type |

|

| Breakup by End Use |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.