Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

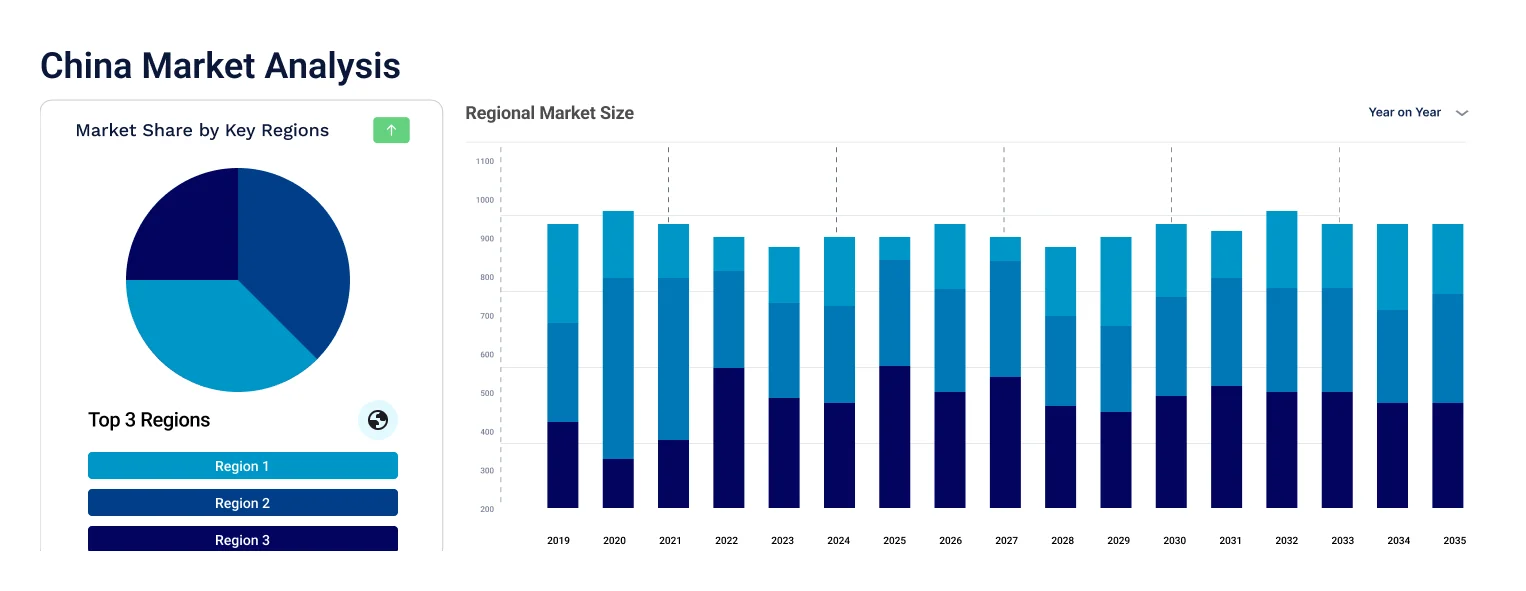

The China Laptop Market reached a value of USD 10.80 Billion at 2025 and is projected to expand at a CAGR of around 4.30% during the forecast period of 2026-2035. With accelerating AI integration in personal computing, surging demand from China's gaming and esports community, widening enterprise adoption of hybrid work devices, and rising digital connectivity in secondary cities, the market is expected to reach USD 16.45 Billion by 2035.

The China laptop demand is quite good among consumer and enterprise sectors especially the ICT sector due to the increasing adoption of work-from-homes, e-learning, and changing businesses in terms of digital transformation. According to a recent report, ICT service exports in China was reported at 58096443461 USD in 2023. Such a growing demand gives companies a chance to target both front-end consumer sales that specifically focus on younger demographics and remote workers.

Chinese consumers are getting increasingly interested in local brands due to low pricing and good local customer service. Therefore, foreign laptop market players can consider alliances, localization, and price competition when they want to enter the Chinese market.

Gaming and high-performance laptop is capturing major share in the China laptop market primarily due to the fast evolution of e-Sports, online gaming, and content creation. Manufacturers can develop high-end PCs and notebooks with top-class graphics, processors, and cooling designs to capitalize on this trend. Also, associating with gaming influencers and eSports events could pull the brand to the younger tech-savvy audience.

Compound Annual Growth Rate

4.3%

Value in USD Billion

2026-2035

| China Laptop Market Report Summary | Description | Value |

| Base Year | USD Billion | 2025 |

| Historical Period | USD Billion | 2019-2025 |

| Forecast Period | USD Billion | 2026-2035 |

| Market Size 2025 | USD Billion | 10.80 |

| Market Size 2035 | USD Billion | 16.45 |

| CAGR 2019-2025 | Percentage | XX% |

| CAGR 2026-2035 | Percentage | 4.30% |

| CAGR 2026-2035 - Market by Region | Northwestern China | 4.9% |

| CAGR 2026-2035 - Market by Region | Southwestern China | 4.6% |

| CAGR 2026-2035 - Market by Type | 2-in-1 Laptop | 4.8% |

| CAGR 2026-2035 - Market by End Use | Gaming | 5.3% |

| 2025 Market Share by Region | Southcentral China | 27.2% |

The key trends observed in the China laptop market are the increasing demand for gaming laptops, rise of thin and lightweight laptops, AI integration and performance optimization in new generation laptops, along with sustainable and eco-friendly designs.

In January 2025, Dell introduced a new series of mid-range laptops for the Chinese market, powered by the latest Intel Core processors and engineered for AI-assisted productivity tasks. The devices are positioned as daily-use alternatives for professionals and students seeking modern performance at accessible price points. This launch reflects Dell's continued commitment to China as a priority market for commercial laptop deployment, and highlights a broader industry shift toward AI-ready hardware configurations even at mid-tier price bands as the definition of standard computing capability evolves.

Industry data from 2025 indicates that AI-capable personal computers are projected to account for approximately 34% of laptop and PC shipments across Greater China during the year. This reflects a rapid adoption curve for devices equipped with dedicated neural processing units and AI acceleration chips, driven by enterprise demand for on-device productivity tools, government digitization programs, and growing consumer familiarity with AI-powered features. The shift is accelerating investment in AI-native software development, particularly among Chinese technology firms integrating proprietary models into their hardware products.

In May 2024, Chinese chip company SpacemiT launched the MuseBook, a laptop built on the company's own K1 octa-core RISC-V processor. Priced at approximately USD 300, the device targets developers, hardware engineers, and researchers working within open-source computing environments. The launch is notable for China's laptop market as it represents a concrete step toward domestic chip self-sufficiency in computing hardware, aligning with national policies encouraging indigenous semiconductor development and reducing reliance on foreign processor architectures within the technology sector.

In April 2024, Huawei launched the updated MateBook X Pro, featuring the Intel Core Ultra 9 processor alongside the company's proprietary Pangu AI system. The device combines an ultra-thin design with deep integration into Huawei's broader HarmonyOS ecosystem, enabling seamless cross-device connectivity between laptops, smartphones, and tablets. The launch reinforced Huawei's position at the premium end of China's laptop market and demonstrated the growing commercial viability of AI-native features in portable computers, a segment that is reshaping how both enterprise and individual users interact with their devices.

MSI brought its Titan 18 Pro 2024 gaming laptop to China in 2024, a flagship product equipped with the Intel i9-14900HX processor and options for either NVIDIA RTX 4080 or RTX 4090 graphics units. The machine also incorporates AI-driven performance optimization features for both gaming and content creation use cases. The launch catered to China's high-end gaming segment, where consumers consistently seek cutting-edge hardware, and signalled the intensifying competition at the premium tier of China's gaming laptop category as both international and domestic brands vie for market leadership.

AI-native computing is no longer an experimental feature in China's laptop segment. Huawei's April 2024 launch of the MateBook X Pro with Pangu AI, alongside Lenovo's integration of face recognition and smart battery optimization across its product range, marked a turning point where AI features shifted from differentiators to expectations. AI-capable PCs are on course to represent over 34% of Greater China shipments by 2025, reflecting a broad market pivot that is reshaping product development priorities and consumer purchasing criteria. This trend is a core driver of China laptop market growth across both business and personal segments.

China's esports and gaming industry has evolved into a structural demand engine for high-performance laptops. Premium gaming machines from brands including Lenovo Legion, MSI, and Alienware are seeing consistent sales growth, fuelled by a younger demographic that prioritizes frame rates, display refresh rates, and thermal management over portability. The 2024 entry of MSI's Titan 18 Pro into China with advanced AI performance features illustrates how gaming laptops are increasingly doubling as professional workstations, expanding their appeal beyond pure gaming use cases into content creation and engineering applications.

Portability has become the defining design priority in China's consumer laptop segment. Driven by hybrid work adoption, online education, and urban commuter lifestyles, consumers are gravitating toward ultra-thin models that combine long battery life with strong processor performance. Huawei's MateBook X series and Lenovo's Xiaoxin lineup exemplify this trend, with both brands investing in designs that compete directly with Apple's MacBook Air on form factor while offering competitive specifications at lower price points. The shift has also prompted mid-range vendors to prioritize chassis weight and thickness in their product roadmaps.

China's push toward semiconductor independence is beginning to influence the laptop market in tangible ways. SpacemiT's May 2024 launch of the MuseBook on a proprietary RISC-V processor demonstrated that domestically designed chips are reaching commercially deployable stages, even if initially targeting developer and institutional buyers. This development is strategically significant in the context of ongoing technology trade restrictions, as it signals the emergence of a domestically self-sufficient computing ecosystem. Government support for homegrown processor development is expected to accelerate such product launches through the forecast period.

The EMR’s report titled “China Laptop Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

On the basis of type, the market can be divided into:

Key Insight: Traditional laptops maintain the dominant share in China's market, supported by broad-based demand from students, office professionals, and gaming enthusiasts who favor the keyboard-centric format for extended productivity and gaming sessions. Their wide availability across price ranges, from budget devices under USD 500 to premium gaming machines above USD 2,000, ensures continued relevance across buyer categories. The 2-in-1 segment is growing at a faster pace at approximately 4.8% CAGR, driven by enterprise adoption among executives and field professionals who require the combined functionality of a tablet and a laptop. Brands including Lenovo, Huawei, and ASUS have invested heavily in 2-in-1 product lines to capture this hybrid demand.

On the basis of screen size, the market can be divided into:

Key Insight: The 13" to 14.9" screen size range holds the dominant position in China's laptop market, representing the sweet spot between portability and screen real estate for daily-use consumers, remote workers, and students. This range benefits from the widest product availability and the most competitive pricing among laptop categories. The 15.0" to 16.9" range follows closely, popular among business power users and gamers who prioritize multitasking and graphical performance. The above 17" segment, while smaller in volume, is showing steady growth among creative professionals and content creators who require expansive screen real estate for design, video editing, and gaming purposes.

On the basis of price, the market can be segregated into the following:

Key Insight: The USD 501 to USD 1000 price band commands the largest market share, representing a broad mid-market where consumers find an acceptable balance of performance, build quality, and affordability. This segment captures demand from students, entry-level professionals, and small business owners. The above USD 2001 tier is growing at the fastest pace, driven by premium gaming laptop upgrades, AI-capable workstation purchases, and demand for ultra-thin premium designs from Huawei, Lenovo, and Apple. The under USD 500 segment, dominated by brands like CHUWI, addresses consistent demand from first-time buyers and educational institutions in lower-tier cities.

On the basis of end use, the market can be divided into the following:

Key Insight: Personal use remains the largest end-use segment, driven by the sheer scale of China's consumer base and sustained spending on household computing devices. Business laptops are a high-value and steadily growing category, supported by enterprises digitizing their operations and a post-pandemic corporate norm of equipping employees with portable devices. Gaming is the fastest-growing end-use segment, expanding at approximately 5.3% CAGR, sustained by China's position as one of the world's largest gaming markets. The proliferation of esports platforms, streaming communities, and content creation networks means that gaming laptops now serve overlapping professional and recreational purposes.

The market can be divided into the following regions:

Key Insight: Guangdong is the leading regional market for laptops in China, anchored by Shenzhen's technology ecosystem and a dense concentration of hardware companies, design studios, and technology enterprises that drive both enterprise and consumer demand. Shanghai follows closely, supported by its financial sector, large population of knowledge workers, and a premium consumer base with high purchase power. Beijing represents a critical hub for government and enterprise laptop procurement, benefiting from the concentration of public sector institutions and headquarters of major domestic technology companies. Zhejiang and Jiangsu contribute through their sizeable manufacturing and SME bases that require business computing solutions.

| CAGR 2026-2035 - Market by | Region |

| Northwestern China | 4.9% |

| Southwestern China | 4.6% |

| North China | 4.1% |

| East China | XX% |

| Southcentral China | XX% |

| Northeast China | XX% |

By Type: Traditional laptops hold the dominant share of China's laptop market, benefiting from widespread adoption across educational institutions, corporate environments, and consumer households where a conventional keyboard-and-screen setup remains the preferred computing form. China's large student population, sustained by digitization mandates in public schools and universities, is a consistent driver of traditional laptop sales, particularly in mid-range price bands. Brands such as Lenovo, HP, and Dell have strong product lineups covering this segment extensively. The 2-in-1 segment, while smaller, is gaining meaningful share among enterprise buyers who prioritize device versatility and executives who prefer the compactness of convertible designs for travel and client-facing work.

By End Use: Personal use accounts for the largest portion of China's laptop market, underpinned by a vast consumer base that has incorporated laptops into daily domestic and academic life. The post-pandemic normalization of home-based digital activities, from online courses to streaming and social media content creation, sustains this segment's dominance. Gaming is the fastest-gaining end-use segment, with younger demographics in particular treating gaming laptops as aspirational purchases that also serve as capable general-purpose machines. Business laptops command a strong secondary share, driven by enterprises modernizing their workforce computing infrastructure, and this segment benefits from higher average selling prices which elevate its revenue contribution above its unit-volume share.

Guangdong is the most commercially active region in China's laptop market. Shenzhen, the province's technology heartland, is home to a concentration of hardware manufacturers, semiconductor companies, and consumer electronics brands that collectively generate both supply-side and demand-side activity for laptops. Enterprise demand is particularly strong, given the density of technology firms requiring high-performance business computing equipment. Consumer demand in Guangdong is similarly elevated, driven by a young, digitally connected urban population with above-average disposable income and a preference for premium devices. The region also benefits from proximity to Hong Kong, which supports cross-border technology product flows and access to international market trends that influence domestic purchasing behavior.

Shanghai is the second most significant regional market in China's laptop sector. As the country's primary financial and commercial center, Shanghai has a large base of corporate users who require reliable, portable computing for professional applications. The city's concentration of multinational headquarters, financial institutions, and creative agencies creates sustained demand for both standard business laptops and premium ultra-thin models. Shanghai's student population, served by numerous prestigious universities, also drives consistent personal and educational laptop purchases. Strong disposable income levels and an affinity for premium international and domestic technology brands position Shanghai as a high-value market where average selling prices exceed the national norm.

China's laptop market is one of the most competitive technology markets globally, featuring a blend of powerful domestic champions and established international brands competing across price, performance, and innovation dimensions. Lenovo holds an unchallenged position at the top by shipment volume, consistently ranking as the world's largest laptop vendor. Huawei has carved out a strong premium domestic segment through ecosystem integration and sleek hardware design. Global players including Dell, HP, and Apple retain strong footholds in enterprise and premium consumer categories, while Xiaomi and CHUWI compete aggressively on price and specifications.

Founded in 1984 and headquartered in Round Rock, Texas, Dell Technologies maintains a strong presence in China's laptop market through its commercial and consumer product lines. The XPS and Latitude series serve premium and enterprise buyers respectively, known for build quality, security features, and enterprise-grade manageability. Dell operates a robust distribution network in China across both offline retail partners and digital platforms, focusing on corporate procurement relationships. In early 2025, Dell introduced new mid-range AI-ready laptops specifically for China, reflecting its commitment to maintaining market relevance as AI PC adoption accelerates across the country.

Founded in 1987 and headquartered in Shenzhen, Huawei is one of China's most recognized laptop brands through its MateBook product family. The MateBook X Pro, featuring proprietary Pangu AI integration and seamless HarmonyOS ecosystem connectivity, is the flagship of Huawei's ultra-premium segment. Despite trade restrictions limiting its access to certain international markets, Huawei has leveraged the domestic market effectively, offering deeply integrated hardware-software experiences that appeal to loyal Chinese consumers and enterprise buyers. Huawei's investment in domestic chip development further differentiates its competitive positioning over the longer term.

Founded in 1984 with dual headquarters in Beijing and North Carolina, Lenovo is the world's largest laptop manufacturer by shipment volume. In China, it commands the largest market share through a portfolio spanning the ThinkPad business series, Yoga and IdeaPad consumer lines, and the Legion gaming range. Lenovo's scale provides significant advantages in component sourcing, distribution reach, and product development cycles. The company has incorporated AI features into multiple product lines, including smart battery management and intelligent performance optimization, positioning itself at the intersection of mass-market scale and technology leadership.

Founded in 1976 and headquartered in Cupertino, California, Apple occupies the premium end of China's laptop market through the MacBook Air and MacBook Pro families. Apple's silicon-powered laptops have generated strong consumer interest in China owing to their processing performance, battery life, and integration with the iOS and iPadOS ecosystems, which are popular among Chinese consumers. While Apple faces intense competition from domestic brands at lower price points, the MacBook retains aspirational appeal among young professionals, creatives, and students who prioritize design and performance above cost. Apple's strong retail and online presence in China supports consistent sales across the premium bracket.

Other key players in the market are HP Inc., Xiaomi Inc., Asustek Computer Inc., CHUWI Innovation Technology Co., Ltd., and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Get ahead in one of Asia's most dynamic technology markets with our in-depth China Laptop Market report for 2026. From AI PC adoption rates and gaming laptop demand to regional sales hotspots and the competitive strategies of brands like Lenovo and Huawei, this report gives you the intelligence to move decisively. Whether you are a device manufacturer optimizing your China lineup, a distributor planning channel strategy, or an investor evaluating market positioning, this is the data you need. Download your free sample today and explore what is driving China's thriving laptop market.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the China laptop market reached an approximate value of USD 10.80 Billion.

The market is projected to grow at a CAGR of 4.30% between 2026 and 2035.

The market is estimated to witness healthy growth in the forecast period of 2026-2035 to reach a value of around USD 16.45 Billion by 2035.

The major drivers of the market are the rapid transition to remote working and online schooling, the increasing gaming population, and the technological improvements in hardware and software applications.

The key trends of the market include the increasing demand for gaming laptops, rise of thin and lightweight laptops, AI integration and performance optimization in new generation laptops, along with sustainable and eco-friendly designs.

The major regions in the market are Shanghai, Zhejiang, Guangdong, Jiangsu, and Beijing.

The various types considered in the market report traditional laptops and 2-in-1 laptops.

The screen sizes considered in the market report are upto 10.9”, 11” to 12.9”, 13” to 14.9”, 15.0” to 16.9” and more than 17”.

The major players in the market are Dell Technologies Inc., Huawei Technologies Co., Ltd., Lenovo Group Ltd., Apple Inc., HP Inc., Xiaomi Inc., Asustrek Computer Inc., CHUWI Innovation Technology Co., Ltd., among others.

The various end use segments included in the market report are personal, business, and gaming.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Type |

|

| Breakup by Screen Size |

|

| Breakup by Price |

|

| Breakup by End Use |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.